Day: April 25, 2026

44 articlesGoods and Services Tax

Goods and Services Tax

Bombay HC Rejected GST Writ Petition Due to Availability of Alternative Remedy

Goods and Services Tax

Goods and Services Tax

GST RegistrationCancellation Quashed Due to Grounds Beyond SCN: Bombay HC

Goods and Services Tax

Goods and Services Tax

GST Registration Cancellation Quashed Due to Vague SCN & Lack of Reasons: Bombay HC

Income Tax

Income Tax

Interest Income Linked to Project Development Activities is Not Taxable: ITAT Delhi

Corporate Law

Corporate Law

Calcutta HC Quashed Property Tax Demand Due to Invalid Retrospective Validation Clause

Custom Duty

Custom Duty

Rubber Mixture Classifiable Under 40028090 Due to Absence of Prohibited Additives: CAAR Mumbai

Custom Duty

Custom Duty

Plant Extract Classifiable as Medicament Due to Therapeutic Use & Processing: CAAR Mumbai

SEBI

SEBI

SEBI Highlights Investor Protection Need Amid Rising Retail Participation

Goods and Services Tax

Goods and Services Tax

Do You Really Need GST Registration? Common Mistakes Businesses Must Avoid

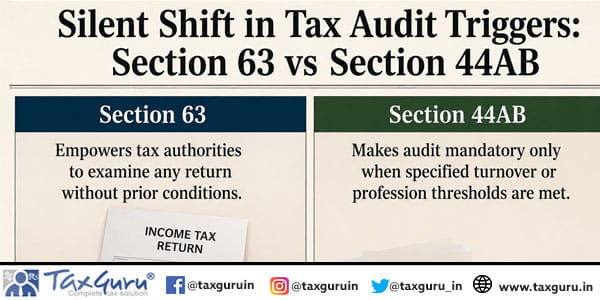

Income Tax

Income Tax