1. In India, it is common for grandparents to show their love and blessings by giving cash gifts to their grandchildren, whether on birthdays, festivals, or special occasions. While these gestures hold cultural and emotional significance, they may also draw scrutiny from the Income Tax Department. A recent case before the PUNE ITAT (Income Tax Appellate Authority) highlights the importance of proper documentation in such matters.

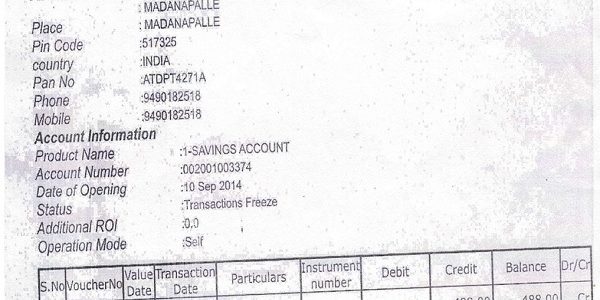

2. Case Background: Vikram’s grandmother gifted him Rs. 10 lakhs in cash on 17.10.2016, which he deposited into his bank account. A gift deed on Rs. 100 stamp paper, bearing her thumb impression, was prepared but not notarised or witnessed. His grandmother passed away in February 2017.

Vikram filed his Income Tax Return (ITR) for Assessment Year (AY) 2017-18, reporting an income of Rs 3 lakh. During scrutiny, the tax officer noted a cash deposit of Rs. 14.50 lakhs during the demonetization period. Vikram explained that this included his cash savings, withdrawals, other income, and the Rs. 10 lakh gift. The officer rejected his explanation and added the entire Rs. 14.50 lakhs as unexplained income under section 69A.

On appeal, the CIT(A) removed Rs. 4.50 lakhs but upheld the addition of Rs. 10 lakhs. Vikram then appealed to the ITAT.

3. ITAT Pune’s Observation – ITA No. 950/PUN/2025, dated August 26, 2025: The key observations made by ITAT Pune are as follows:

(a) The gift deed lacked notarization and witnesses and only carried the grandmother’s thumb impression.

(b) No evidence was produced to prove her financial capacity to gift Rs. 10 lakhs.

(c) The Tribunal held that the gift could not be treated as genuine.

(d) However, considering Vikram’s cash balance, withdrawals, and other income, the availability of Rs. 5 lakhs was accepted.

4. Ruling: ITAT Pune upheld the disallowance of Rs 10 lakhs as unexplained but granted partial relief by deleting the addition of Rs 5 lakhs, sustaining only Rs 5 lakhs as unexplained cash.

5. Key Takeaways:

Burden of Proof: The taxpayer must prove the authenticity of any cash gift or deposit.

Gift Deed Alone Is Not Sufficient: The donor’s financial capacity must be verified through income tax returns, bank statements, or proof of savings.

Maintain Records. Properly documented cash balances and income strengthen the taxpayer’s cash position.

6. Conclusion: While it is true that gifts received from relatives as defined under the Income Tax Act are not taxable, the definition specifically includes lineal ascendants or descendants, which covers grandparents. Therefore, any gift from a grandparent to an individual should not be taxed. However, in practice, such gifts must be supported with proper documentation and proof of the donor’s financial capacity; otherwise, they may be subject to scrutiny. Affection may be tax-free, but proof is not optional.

Disclaimer: This article is for educational use only.

The author can be reached at caanitabhadra@gmail.com