When Being Late Costs You More Than Stress: Real Cases of Penalties for Late ITR/TDS Filing

Filing an income-tax return on time is one of those boring-but-critical tasks that can save you money and a lot of hassle. In India the law doesn’t just charge interest on unpaid tax; it also levies statutory fees and sometimes heavy penalties on late returns. This report summarizes how the rules work and presents real examples — from statutory caps to a rare case where the individual faced-and then contested-a six-figure penalty.

The Baseline Rules: Fees under Section 234F and Interest under 234A/B/C

The most visible rule for most taxpayers is Section 234F (the “late-filing fee”). For recent assessment years, a late return attracts a penalty of a maximum of Rs. 5,000 for taxpayer whose total income above Rs. 5 lakh-small taxpayers face a Rs. 1,000 cap. In addition to that, there’s interest under Sections 234A/B/C-usually 1% per month on outstanding tax and operational effects such as inability to carry forward certain losses if the return is belated.

TDS/TCS Statements — A Different Beast (Section 271H)

If you’re responsible for deducting tax (as an employer or business), missing the TDS statement deadlines can trigger much harsher penalties. Section 271H sets a minimum penalty of Rs. 10,000 (extendable up to Rs. 1,00,000), besides a late fee of Rs. 200 per day. Organisations missing payroll TDS filings often bear costs significantly higher than the usual ones Rs. 5,000 ITR cap.

Real-World Enforcement

The Income Tax Department has become active in pursuing non-compliance — not just for late filing but also for fictitious claims and incorrect deductions. Government press Releases from 2025 highlighted coordinated action against fraudulent intermediaries and preparers. Such enforcement commonly results in penalties or reassessment actions.

A Named Case: Rs. 1.46 Lakh Penalty on an Individual

A Business Today report, in July 2025, highlighted one conspicuous case wherein a salaried taxpayer faced a proposed penalty of about Rs. 1.46 lakh for alleged bogus deductions and under-reporting. The taxpayer appealed the assessment and succeeded on appeal. This illustrates how penalties can swell far beyond the normal late-filing fees.

What Courts Have Said About Late Fees

Section 234F has been tested in courts. For example, the Madras High Court has upheld its validity, confirming its status as a valid compliance fee and not as an unconstitutional penalty. Courts continue to refine the boundaries of relief and discretion for the evaluation of officers.

Quick Practical Lessons

1. Don’t assume small penalties are harmless; overtime, the unpaid interest and other fees add up quickly.

2. TDS compliance pertains to the employers and businesses; penalties under Section 271H begin from high.

3. If you get a penalty notice, appeal straight away – many appeals are upheld.

4. Responsibly use the belated return window by paying the late fee and interest to remain.

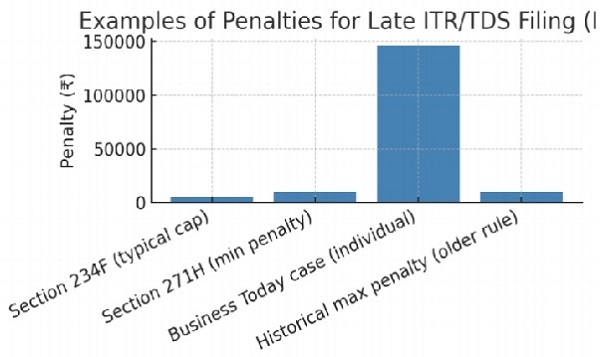

Chart Summary: Real Penalty Examples

The chart below compares the standard Section 234F cap Rs. 5,000 and the Section 271H Minimum punishment Rs. 10,000, actual reported case Rs. ~1.46 lakh, and historical maximum penalty mention Rs. 10,000. While statutory caps are modest, real-life penalties related understatement or the TDS failure is huge.

Conclusion

For most taxpayers, filing on time remains the simplest solution to avoid unnecessary expenses. For organisations, building automated reminders and internal review systems helps ensure compliance. If you receive a notice, act quickly and seek expert help — many cases have shown that appeals and representations can succeed. Penalties are designed to enforce discipline, not to punish honest mistakes, but once triggered, they can become expensive lessons.