ITR Utility Glitch in Capital Gain Reporting Problem with Negative Values in Quarterly Breakup

Introduction

While filing Income Tax Returns (ITR) for AY 2025-26, many taxpayers are encountering an unusual technical glitch in the capital gains reporting schedule. The utility does not allow entry of negative values in the quarterly breakup under Schedule CG → Table F (Information about accrual/receipt of capital gain).

This issue creates difficulties for taxpayers who may have incurred short-term or long-term capital losses in certain quarters, but overall, the full-year computation results in a net capital gain. Since the utility enforces only positive entries, it causes mismatches with Schedule BFLA and prevents return filing unless manual adjustments are made.

What is Table F Used For? (Understanding 234C Impact)

The quarterly breakup of capital gains in Table F is not for computing taxable income, but mainly for calculating interest under section 234C of the Income-tax Act.

- Section 234C requires taxpayers to pay advance tax on capital gains in the quarter in which they arise.

- Table F enables the system to apportion capital gains across quarters and calculate any shortfall in advance tax payment.

- However, since the utility disallows negative values, it cannot capture scenarios where losses in some quarters offset profits in others.

The Glitch: Why Negative Quarterly Values Are Rejected

When reporting capital gains, the system requires a quarterly breakup in the table “F. Information about accrual/receipt of capital gain”.

The problem:

- If a quarter shows a loss, the system rejects the entry (since only positive values are allowed).

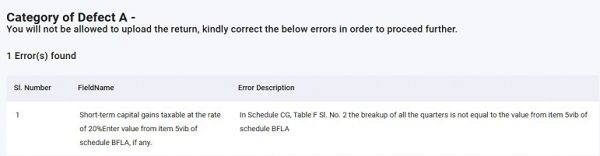

- At the time of validation, the portal throws an error stating that the quarterly breakup does not tally with the annual figure in Schedule BFLA.

This error arises only when:

- There is a loss in one or more quarters,

- But the annual computation still results in a net profit.

If the entire year results in a net capital loss, the system accepts entries with “0” in all columns without error.

Legal vs Technical: Why the Glitch Contradicts the Law

The Income-tax Act, 1961 clearly recognizes capital losses and permits them to be set off or carried forward.

- The Income-tax Act imposes imposes no restriction on reporting negative values in quarterly capital gain details.

- The restriction arises purely from the design of the ITR utility.

- The table was built to capture positive gains for 234C computation, but in practice, losses should also be factored in to give a true quarterly picture.

This makes the restriction a system error, not a legal bar.

Workaround: How to Adjust Negative Capital Gains in Table F

Until the e-filing utility is corrected, taxpayers can adopt the following workaround to ensure smooth filing:

1.Enter “0” for quarters with negative values (since system does not accept –ve entries).

2. Adjust the positive values in the nearby quarter(s) where losses occurred. This ensures that:

– All quarterly entries remain positive.

– The sum of quarterly figures equals the actual annual gain.

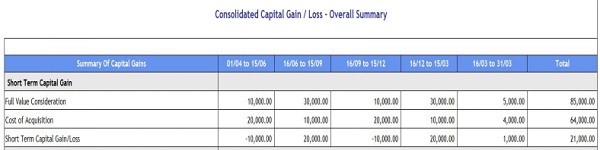

Example Adjustment:

- Q1: –₹10,000 (loss)

- Q2: +₹20,000 (profit)

- Q3: –₹10,000 (loss)

- Q4: +₹20,000 (profit)

- Q5: +₹1,000 (profit)

- Total = +₹21,000

Adjustment for ITR utility input:

- Q1: Enter “0” instead of –10,000; reduce Q2 profit from 20,000 → 10,000.

- Q3: Enter “0” instead of –10,000; reduce Q4 profit from 20,000 → 10,000.

- Q5 remains 1,000.

- Now, quarterly breakup shows all positive entries, and the total still matches 21,000.

3. Ensure the annual figure in Schedule CG matches the computation in Schedule BFLA.

4. Prepare a working note of the actual quarter-wise breakup (with negatives).

5. Retain broker contract notes and capital gain statements as evidence.

6. Report the issue with screenshots to the Income Tax e-filing grievance portal.

Conclusion

The problem is essentially a technical design flaw in the ITR utility. Table F is meant for 234C interest computation, but its current restriction against negative values distorts reporting and creates mismatches.

Taxpayers must adopt practical adjustments to ensure:

- Annual totals remain correct,

- Returns can be filed without errors, and

- Proper documentation is maintained for any future scrutiny.

Until the system is upgraded, taxpayers should carefully manage quarterly adjustments and raise grievances with the Income Tax Department to highlight the issue.

*****

Disclaimer

This article is based on practical experiences observed during AY 2025-26 ITR filings. It reflects the author’s personal interpretation and does not constitute legal or professional advice. Taxpayers are advised to consult a qualified tax professional for specific guidance.

Author Bio

fully agreed..

glitch is there..

perfect reply…

while there is Short term and Long term loss, the system wrongly takes the total of the two under Long term loss in. Schedule CFL, to the disadvantage of the tax payer and in contradiction of the relevant provisions.