Karan Khatri

INTRODUCTION

Background

Section-145(2) of Income tax Act, 1961 empowers Central Government to issue Income Computation and Disclosure Standards (ICDS).

Key Features of ICDS

- Effective Date of ICDS is 01stApril, 2015 AY: 2016-17 onwards.

- ICDS applicable to all assesses Corporate & Non Corporate Assesses.

- To be followed by all the assesses following Mercantile System of Accounting.

- ICDS is only for computation of income under the head :

- Profit and gains of business or profession

- Income from other sources

- Entity need not maintain Books of accounts for ICDS.

- ICDS is meant for Normal computation of income and not for Minimum Alternate Tax (MAT) Calculation.

- No Net Worth or Turnover Criteria Prescribed for applicability.

- In the case of conflict between the provisions of the Income‐tax Act, 1961 and ICDS: The provisions of the“I.T Act shall prevail”.

Transitional Provisions

All contract or transactions existing on the 1st day of April, 2015 or entered into on or after the 1st day of April, 2015 shall be dealt with in accordance with the provisions of this standard.

ICDS I –DISCLOSURE OF ACCOUNTING POLICIES

- There are certain differencesin disclosures of AS – 1 as notified by ICAI and ICDS -1, which are as under:

- Marked to market loss or an expected loss shall not be recognized unless permitted by any other ICDSas against in AS – 1.

- The concept of “Prudence” and “Materiality” is not recognized for the purpose of computation of incomeas against AS – 1.

- The similaritiesin disclosure of AS- 1 and ICDS – 1 are as follows :

- The treatment and presentation of transactions and events shall be governed by their “substance” and not merely by the legal form.

- If the fundamental accounting assumption of Going Concern, Consistency and Accrual are not followed, the fact shall be disclosed.

Changes in Accounting Policies

1. All significant accounting policies adopted by the assesse shall be disclosed.

2. Accounting policy can be changed for any “reasonable cause”.

3. Any change in an accounting policy which has material effect: Shall be disclosed along with amount by which such item is affected.

4. If such amount is not ascertainable wholly or in part:The fact shall be indicated.

5. If no material effect in current year, but likely to have material effect in subsequent year: Disclosure to be given in the year when the changes are made.

ICDS II – VALUATION OF INVENTORIES

Scope

1. This Income Computation and Disclosure Standard shall be applied for valuation of inventories, except :

- Work‐in‐progress arising under ‘construction contract’, which is dealt by ICDS III;

- Shares, debentures and other financial instruments held as stock‐in‐trade

which are dealt with by the ICDS VIII;

- Producers’ inventories of livestock, agriculture and forest products, mineral oils, ores and gases to the extent that they are measured at net realisable value;

- Machinery spares, which can be used only in connection with a tangible fixed asset and their use is expected to be irregular.

Definitions

The following terms are used in this Income Computation and Disclosure Standard with the meanings specified:

1. “Inventories” are assets which include:

- FINISHED GOODS held for sale in the ordinary course of business;

- WORK IN PROGRESS for such sale;

- CONSUMABLES to be used in the production process or in the rendering of

2. Net Realisable value

Measurement

Measurement

Inventories shall be valued at cost, or net realisable value, whichever is lower.

Cost of Inventories

Costs of Purchase

Costs of Purchase

The costs of purchase shall consist of purchase price

INCLUDING:

- Duties and taxes,

- Freight inwards and

- Other Expenditure directly attributable to the acquisition &

EXCLUDING:

- Trade discounts,

- Rebates and

- Other similar items.

Costs Of Services

The costs of services in the case of a service provider shall consist of

Labour Cost, +

Other costs of personnel directly engaged in providing the service

and attributable overheads.

Costs Of Conversion

It is cost which is incurred in converting materials into finished goods

IT INCLUDES:

1. costs directly related to the units of production

2. and a systematic allocation of fixed and variable production overheads

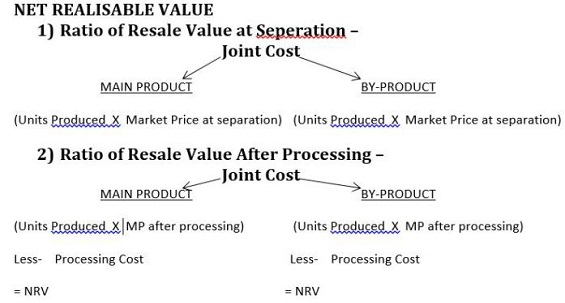

Any By‐products, scrap or waste material which are immaterial,shall be measured at NRV and this value shall be deducted from the cost of the main product.

Other Costs

INCLUDES: cost of inventories only to the extent that they are incurred in bringing the inventories to their present location and condition

EXCLUDES: Interest Cost specified in the ICDS IX.

Exclusions Of The Cost Of Inventories

Following cost to be EXCLUDED and recognised as expenses of the period:

- Abnormal amounts of wasted materials, labour, or other production costs;

- Storage costs, unless those costs are necessary in the production process prior to a further production stage;

- Administrative overheads that do not contribute to bringing the inventories to their present location and condition;

- Selling costs.

Cost Formulae

First‐in First‐out Method (FIFO)

Weighted Average Method (WEIGHTED AVG)

Retail Method

Disclosure & Change of Method of Valuation of Inventory

1. The method of valuation of inventories once adopted by a person in any previous year shall not be changed without reasonable cause.

2. Disclosure

- Accounting policies

- Cost formula used

- Total carrying amount

- Classification appropriate to a person.

ICDS III – CONSTRUCTION CONTRACT

Introductions

Construction contract means contact negotiated for construction of :

- An asset or Combination of assets

- Which are interrelated or interdependent in their design, technology and function

- Or their ultimate purpose or use.

Retention – amount which are not paid until the satisfaction of conditions specified in the contract for the payment of such amounts or until defects have been rectified.

Types of Contract

- Fixed Price

- Cost Plus

- Combination of Both

Combining & Segmentation of Contract

This ICDS is applicable to each construction Contract except:

- If it is necessary to break the contract and apply component wise.

- If interrelated then can Combine various contracts.

Contract Revenue

1. Contract revenue shall be recognized when there is reasonable certainty of its ultimate collection.

2. Contract revenue shall comprise of:

- Initial amount of revenue agreed(including retention) and

- Variations in contact work, claims and incentive payments:

- To the extent that it will result in revenue

- Capable of being reliably measured.

3. If income is written off as uncollectable, the same is recognized as

Contract Cost

Cost shall include:

- Related directly to contract

- Activity related to contract

- Other costs chargeable under the terms of the contract.

- Allocated borrowing cost

Recognition of Contract Revenue and Expenses

1. To be recognized by reference to the stage of completion of the contract.

2. Should be recognized under Percentage of Completion Method (POCM).

3. Mandatory to recognize profit/loss on POCM basis beyond 25%.

- /-Less than 25% – Extent to the cost incurred.

- Beyond 25% – POCM

4. Retention money to be included as part of contract revenue.

Disclosure

- The amount of contract revenue

- Method used to determine the stage of completion of contract.

If contract is in progress:

- Amount of cost and recognized profits

- Amount of advances received

- Amount of retentions.

ICDS IV – REVENUE RECOGNITION

- This ICDS deals with revenue from

- The sale of goods;

- The rendering of services;

- Interest, royalties or dividends.

- For a transaction undertaken on or before the 31stMarch, 2015 but not completed shall be recognized as per ICDS.

- While considering gross turnover or sales for the purpose of determining whether the assessee is liable for tax audit u/s 44AB or u/s like 44AD, the same will have to be computed as per ICDS.

Sale of Goods-

1. Revenue is recognized when

Property in goods or all significant risks and rewards of ownership are transferred to the buyer

And

There is reasonable certainty of its ultimate collection.

2. Where the ability to assess the ultimate collection with reasonable certainty is lacking revenue recognition shall be postponed to the extent of uncertainty involved.

Sale of Services-

- Revenue/Profit/Loss from service transactions shall be recognized by the percentage completion method only.

- Under this method, revenue from service transactions is matched with the service transactions costs incurred in reaching the stage of completion, resulting in determination of revenue, expenses and profit, which can be attributed to the proportion of work completed.

- Stage of Completion will be determined through:

- Cost incurred in proportion to total estimated costs for rendering the service.

- Survey of work performed.

- Completion of physical proportion of the work.

- If the service contract is in its early stages and the outcome cannot be reliably estimated, revenue is recognized only to the extent of costs incurred. However early stage cannot extend beyond 25% of the stage of completion.

Interest, royalties or dividends-

| Particulars of Income | Basis for recognition |

| Interest | Time basis |

| Royalties | Terms of agreement or any other systematic basis |

| Dividends | Provisions of Income tax Act |

| Discount or premium on debt securities | Time basis |

Disclosures required-

- Total amount of claim raised for escalation of price and export incentives but not recognized as revenue along with nature of uncertainty about such claims.

- Revenue from service transactions recognized.

- The methods used to determine the stage of completion.

- For service transactions in progress at the end of previous year:

- Costs incurred and profits recognized till the end of previous year

- Advances received

- Retentions made.

ICDS V – TANGIBILE FIXED ASSETS

This Income Computation and Disclosure Standard deals with the treatment of Tangible Fixed Assets.

The ICD would apply to assets acquired or construction of which commenced before 31st March, 2015 but not completed till date.

Identification of tangible fixed asset

1. Tangible fixed asset is an asset held for the purpose of producing or providing services and is not held for sale in normal course of business.

2. Stand by equipment and servicing equipment are to be capitalized.

3. Machinery

- Spares shall be charged to the revenue as and when consumed

- When such spares can be used only in connection with an item of tangible fixed asset and their use is expected to be irregular, they shall be capitalized.

Actual Cost – Components

The actual cost of tangible fixed asset shall include –

- Purchase price

- Import duties & Other Taxes

- Any directly attributable expenditure made on asset for making it ready to use.

The asset is subject to changes on account of its acquisition or construction on account of –

1. Price adjustment, changes in duties or

Exchange fluctuations as specified in ICDS.

The expenditure incurred on startup and commissioning of the project, including the expenditure incurred on test runs and experimental production, shall be capitalized. The expenditure incurred after the plant has begun commercial production, that is, production intended for sale or captive consumption, shall be treated as revenue expenditure.

In case of self-generated asset also, the same principles as stated above to arrive at actual cost of the asset.

Any expenditure that increases the benefits derived from the asset are the included in calculation of actual cost of the asset.

Non-Monetary Consideration

When a fixed asset is acquired in exchange for another asset or in exchange of securities, the actual cost shall be thefair value of asset so acquired.

Valuation of asset in Special Cases

- Assets held jointly with others, the value of actual cost, depreciation and written down value is grouped together with similar fully owned assets.

- Details of such jointly held assets have to be indicated separately in assets register.

Also, if assets are purchased for consolidated price, the consideration is to be apportioned on a fair basis to various assets.

Tangible Assets Register

Where a person owns tangible fixed assets jointly with others, the proportion in the

Actual cost, accumulated depreciation and written down value is grouped together with similar fully owned tangible fixed assets. Details of such jointly owned tangible fixed assets shall be indicated separately in the tangible fixed assets register.

Where several assets are purchased for a consolidated price, the consideration shall be apportioned to the various assets on a fair basis.

Disclosures

Following disclosures are to be made in respect of tangible fixed assets, which are as under –

- Description of asset or block of assets.

- Rate of depreciation.

- Actual cost or written down value , as the case may be:

- Additions or deductions during the year with proper details.

- Depreciation allowable.

- Written down value at end of year.

ICDS VI – EFFECT OF CHANGE IN FOREIGN EXCHANGE RATES

Scope

- Treatment of transactions in foreign currencies.

- Translating the financial statements of foreign operations.

- Treatment of foreign currency transactions in the nature of forward exchange contracts.

Applicability

All foreign currency transactions undertaken on or after 1st day of April,2015 shall be recognised in accordance with the provisions of this standard.

Recognition of Transaction

(Subject to the provisions of Sec.43A or Rule 115 of the IT Act,1961)

1. Initial Recognition

- A Foreign currency shall be recorded in the reporting currency, by applying the exchange rate at the “date of the transaction”.

- An average rate for the week or month that approximates the actual rate at the date of the transaction may be used, for all transactions in each foreign currency occurring during that period.

2. Year End Balances

- Monetary Items

Foreign currency monetary items shall be converted into reporting currency by applying the “closing rate” and exchange difference arising out of settlement shall be recognised as income or expense of that year.

- Non-Monetary Items

Non-monetary items in foreign currency shall be converted into reporting currency by using the exchange rate at the “date of the transaction” and the exchange difference shall not be recognised as income or expense.

Presentation in Financial Statements

3. Integral Foreign Operations

The financial statements will be translated on the basis of the Recognition principles mentioned above.

4. Non- Integral Foreign Operations

The financial statements will be translated as below:

- Assets and liabilities both monetary and non-monetary- “At closing rates.”

- Incomes and Expenses- Rate on the date of transaction

- Exchange differences as : income or expense in that year.

(Note: When there is a change in the classification of Foreign Operation the new translation procedures should be applied from the date of change in classification.)

Forward Exchange Contracts

The premium or discount arising at the inception of a forward exchange contract shall be amortised over the life of the contract and any exchange difference shall be recognised as income or expense in that period subject to some conditions of recognition of forward contracts.

Inference

The ICDS will open up a new area of intellectual and professional challenge, a requirement for technology upgradation for business systems and room for significant litigation in the tax area.

ICDS VIII – TANGIBLE FIXED ASSETS

Definition

ICD standard VIII deals with securities held as stock-in-trade.

But does not deal the following (excludes):

- Bases for recognition of interest and dividends on securities

- Securities held by a person engaged in the business of insurance

- Securities held by mutual funds, venture capital funds, banks and public financial institution

Terms

- “Fair Value”:-

Means amount for which an asset could be exchanged between a knowledgeable, willing buyer and a knowledgeable, willing seller in an Arm’s length transaction.

- “Securities”:-

Shares, scrip’s, stocks, bonds, debentures, debenture stock or other marketable securities of a like nature in or of any incorporated company or other body corporate, other than Derivatives.

Measurement of Securities

Acquisition by means of Actual Purchase:

Recognized at actual purchase cost.

Actual cost includes purchase price and acquisition charges such as brokerage, fees, tax, duty or cess.

Acquisition by means of Exchange of other securities:

Recognized at fair value or the fair value of the securities issued, whichever is lower.

Acquisition by means of Exchange of another Asset:

Recognized at actual cost of Asset exchanged.

Where unpaid interest has accrued before the acquisition of an interest-bearing security and is included in the price paid for the security, the subsequent receipt of interest is allocated between pre-acquisition and post-acquisition periods; the pre-acquisition portion of the interest is deducted from the actual cost.

At the end of any previous year, securities held as stock-in-trade shall be valued at actual cost initially recognized or net realizable value at the end of that previous year, whichever is lower.

The comparison of actual cost initially recognized and net realizable value shall be done category wise and not for each individual security.

For this purpose, securities shall be classified into the following categories:

(a) Shares

(b) Debt securities;

(c) Convertible securities; and

(d) Any other securities other than above.

The value of securities held as stock-in-trade of a business as at the beginning of the previous year shall be:

- Nil, if the business is commenced during the previous year; and

(b) The value of the securities of the business as on the close of the immediately preceding previous year, in any other case.

In case of securities not listed on a recognized stock exchange; or listed but not quoted on a recognized stock exchange with regularity from time to time, shall be valued at actual cost initially recognized.

Illustration:-

Comparison at Category Level v/s Individual Security Level

| Security | Cost | NRV | As per GAAP(Lower of Cost or NRV at Security Level) | As per ICDS(Lower of Cost or NRV at Category Level) |

| A | 100 | 20 | 20 | NA |

| B | 100 | 100 | 100 | NA |

| C | 100 | 400 | 100 | NA |

| Total | 300 | 520 | 220 | 300 |

Impact:-

As per GAAP while Computing Income for Taxation Rs.220/- shall be taxed in the hands of Assesse, while as per ICDS Rs.300/- shall be taxed.

This could be limiting factor where carrying back/drawing back of past losses that needs to be set off.

ICDS IX – BORROWING COST

Scope:

- This Income Computation & Disclosure Standard deals with treatment of borrowing costs.

- This Income Computation & Disclosure Standard does not deal with the actual or imputed cost of owners’ equity and preference share capital.

Definitions:

Borrowing Costs are interest and other costs incurred by a person in connection with the borrowing of funds and include:

1. Commitment charges on borrowings;

2. Amortised amount of discounts or premiums relating to borrowings;

- Amortised amounts of ancillary costs incurred in connection with the arrangement of borrowings;

1. Finance charges in respect of assets acquired under finance leases or under other similar arrangements.

Qualifying Asset means:

1. Tangible assetslike land, building, machinery, plant or furniture;

2. Intangible assetslike know-how, patents, copyrights, trademarks, licenses, franchises, or any other business or commercial rights of similar nature;

- Inventories that require a period of twelve months or more to bring them to a saleable condition.

Recognition:

Borrowing costs that are directly attributable to the acquisition, construction or production of a qualifying assetshall be capitalized as part of the cost of that asset.

Borrowing cost other than for capitalization shall be recognized in accordance with the provisions of the Act.

Borrowing costs eligible for capitalization:

1. If the funds are borrowed specifically for the purpose of acquisition of a qualifying asset, the amount of borrowing costs to be capitalizedon that asset shall be the actual borrowing costs incurred during the period on the funds so borrowed.

2. For generally borrowed funds, the amount of capitalization shall be computed as follows: A*B/C

Where:

A = General borrowing costs incurred

B = Avg. costs of qualifying asset appearing in the balance sheet

C = Avg. of the amount of total assets as appearing in the balance sheet

Commencement of Capitalization:

The capitalization of borrowing costs shall commence:

- In case of specific borrowings, from the date on which the funds were borrowed;

- In case of general borrowings, from the date on which funds were utilized.

Cessation of Capitalization:

The capitalization of borrowing costs in other cases and when the construction of a qualifying asset is completed in parts and a completed part is capable of being used while construction continues for the other parts, capitalization shall cease:

- In case of assets tangible or intangible(as per definition of qualifying asset), when such asset is first put to use;

- In case of inventory(as per definition of qualifying asset), when all activities necessary to prepare such asset for its intended sale are complete.

Disclosures required:

- Accounting policy adopted for borrowing costs.

- Amount of borrowing costs capitalized during the previous year.

ICDS X – PROVISIONS, CONTINGENT LIABILITIES AND CONTINGENT ASSETS

Scope

This ICDS deals with contingent Liability and Assets but,

Excludes:

- Resulting from financial instruments;

- Resulting from executory contracts;

- Arising in insurance businessfrom contracts with policyholders; and

- Covered by another ICDS.

Provisions excludes :-

- Doubtful debts

- Depreciation

- Impairment of Assets

Definition

- “Provision” is a liability which can be measured only by using a substantial degree of estimation.

- “Contingent liability” “Contingent asset”

Is Possible Obligation Is Possible Asset

“that arises from past events and the existence of which will be confirmed only by the occurrence or non- occurrence of one or more uncertain future events”

Recognition

Provision

1. A provision can be recognized when :-

- There is present obligation

- It is reasonably certain that an outflow of resources will be required

- A reliable estimate can be made of the amount

2. No provision shall be recognised for costs that need to be incurred to operate in the future.

3. Only obligations arising from the past events existing independently of a person’s future actions(i.e future conduct of its business) shall be recognised as provisions

4. Where details of a proposed new law have yet to be finalised, an obligation arisesonly when the legislation is enacted.

- A person shall not recognise a Contingent Liability.

- A person shall not recognise a Contingent Asset.

Measurement

♠ Best Estimate

Best Estimate of Provisions & Contingent Liability is “Expenditure required to settle a present obligation”

Best Estimate of Contingent Assets “value of economic benefit arising”

These estimates are measured at the end of the previous year. The amount and related income shall not be discounted to its present value.

♠ Reimbursement

Where some or all of the expenditure required to settle a provision is expected to be reimbursed by another party, the reimbursement shall be recognised when it is reasonably certain that reimbursement will be received if only the person settles the present obligations.

Review

Provisions shall be reviewed at the end of each previous year and adjusted to reflect the current best estimate.

Disclosure

♠ For each class of provision

1. brief description of the nature of the obligation;

2. the carrying amount(CA) at the beginning and end of the previous year;

3. additional provisions made during the previous year, including increases to existing provisions;

4. amounts used, that is incurred and charged against the provision, during the previous year;

5. unused amounts reversed during the previous year; and

6. the amount of any expected reimbursement, stating the amount of any asset that has been recognised for that expected reimbursement.

♠ For each class of asset & related income recognised

♠ For each class of asset & related income recognised

- a brief description of the nature of the asset and related income;

- the carrying amount of asset at the beginning and end of the previous year;

- additional amount of asset and related income recognised during the year, including increases to assets and related income already recognised; and

- amount of asset and related income reversed during the previous year.

(We have not covered ICDS VII – Government Grants)

Special Thanks to CA Virag Shah , CA Jigar Jain, Aasna Shah,Vinil Malde, Rainy Sanghvi, Karan Khatri, Veear Parekh, Nikita Baid, Khushbu Parekh and Kunal Shah who helped us in preparing this article

Dear Sir

Thanks very well presentation

sir

this is really good work

Dear sir,it is very well explained lucid presentation.Thank you very much for elaborate discussion.if you don’t please mail it to ID.

Very well compiled and explained

Very good compilation indeed.Pl continue such good work and share knowledge

SIR,

EXCELLENT INFORMATION FOR SMALL INDIVIDUAL ASSESSES IT WILL BE VERY DIFFICULT TO FOLLOW.SPECIALLY IN CASE OF CIVIL CONTRACTORS VALUATION OF CLOSING STOCK AND WORK IN PROGRESS IS CHALLENGING TO THE PROFESSIONALS.