Income Tax Department

Ministry of Finance, Government of India

DTAA & FTC

Double Taxation Avoidance Agreement (DTAA) & Foreign Tax Credit (FTC)

Double Taxation Avoidance Agreement (DTAA) & Foreign Tax Credit (FTC)

Introduction

The Double Taxation Avoidance Agreement (DTAA) is an agreement between India and other countries to avoid double taxation, ensure the exchange of tax-related information, and facilitate tax recovery.

Scope of DTAA

Under Section 90, India can enter into agreements with other countries to:

1. Provide relief from double taxation of income taxed in both countries.

2. Promote trade and investment by aligning tax laws.

3. Prevent tax evasion and misuse of treaty benefits.

4. Facilitate tax recovery and information exchange.

5. Section 90A allows agreements with specified associations for similar purposes.

Applicability of Beneficial Provisions

If the provisions of the DTAA are more beneficial than those in the Income-tax Act, the DTAA provisions will apply. However, provisions under the General Anti-Avoidance Rule (GAAR) will override beneficial DTAA provisions.

Understanding Terms in DTAA

- Terms defined in the DTAA take precedence.

- Undefined terms derive their meaning from the Income-tax Act or relevant government notifications.

Claiming DTAA Benefits

To claim relief under DTAA, a non-resident must:

1. Furnish Tax Residency Certificate (TRC) obtained from his home country.

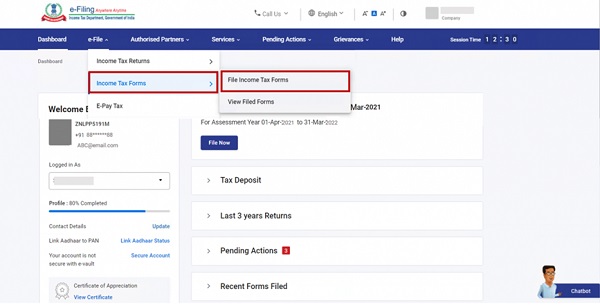

2. File Form 10Felectronically.

3. Maintain supporting documents for claims.

To claim relief under DTAA in a foreign country, a resident can make an application in Form No. 10FA electronically to the assessing officer to obtain a Tax Residency Certificate. The tax residency certificate to a resident person is provided in Form No. 10FB.

Foreign Tax Credit (FTC)

Foreign Tax Credit (FTC)

What Is FTC?

FTC allows a resident person to claim credit for taxes paid abroad on income also taxed in India.

Key Points on FTC

1. Year of Credit: FTC is allowed in the year the foreign income is taxed in India.

2. Amount of Credit: FTC is limited to the lower of Indian tax payable or foreign tax paid.

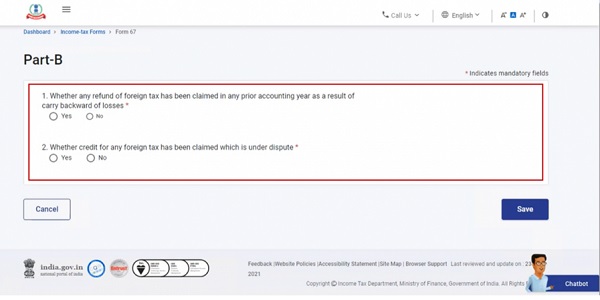

3. Disputed Taxes: FTC is not allowed for disputed foreign taxes until the dispute is resolved.

4. Conversion to INR: Foreign tax is converted to INR using specified rates.

Documents Required for FTC

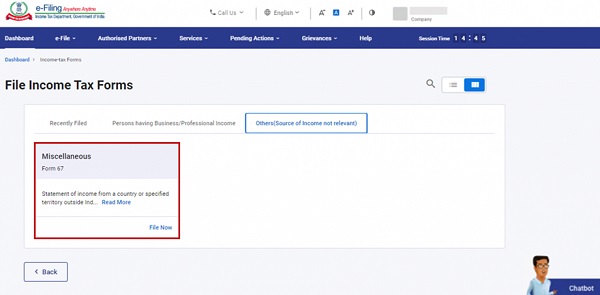

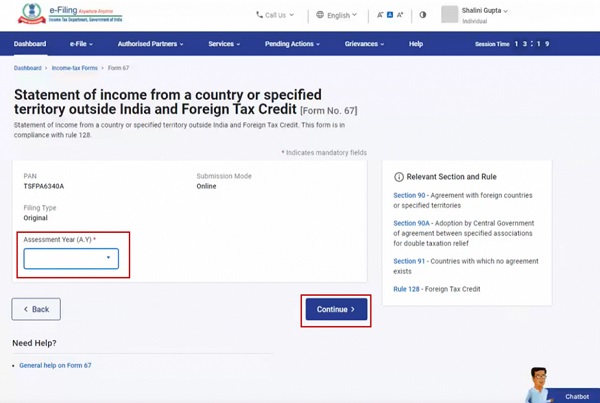

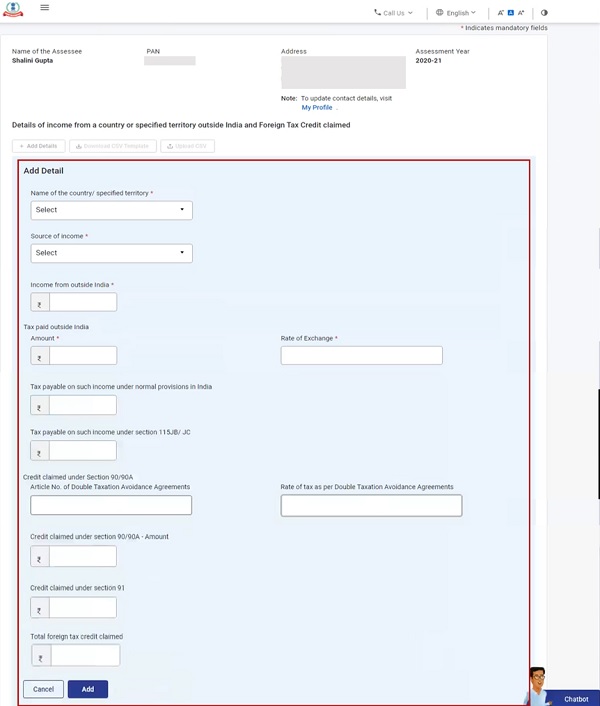

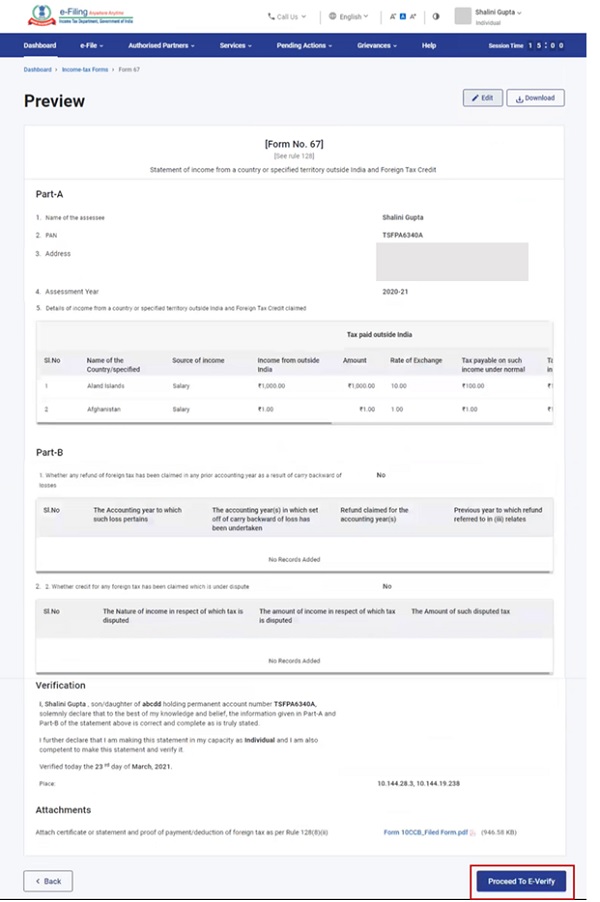

1. Statement of income and tax in Form 67.

2. Certificate from the foreign tax authority or payer detailing income and tax paid.

3. Proof of tax payment or deduction.

Deadlines for Document Submission

- Original or belated return: End of the assessment year.

- Updated return: Before filing the updated return.

Unilateral Relief

Unilateral Relief

If no DTAA exists with a foreign country, relief for taxes paid abroad is allowed if:

1. The taxpayer is an Indian resident.

2. The income is earned and taxed abroad.

3. Tax is paid in the foreign country.

Relief is a deduction based on the lower tax rate between the two countries.

*********

Income-tax Rules, 1962

Rule – 21AB

Certificate for claiming relief under an agreement referred to in sections 90 and 90A.

21AB. (1) Subject to the provisions of sub-rule (2), for the purposes of sub-section (5) of section 90 and sub-section (5) of section 90A, the following information shall be provided by an assessee in Form No. 10F, namely:—

(i) Status (individual, company, firm, etc.) of the assessee;

(ii) Nationality (in case of an individual) or country or specified territory of incorporation or registration (in case of others);

(iii) Assessee’s tax identification number in the country or specified territory of residence and in case there is no such number, then, a unique number on the basis of which the person is identified by the Government of the country or the specified territory of which the assessee claims to be a resident;

(iv) Period for which the residential status, as mentioned in the certificate referred to in sub-section (4) of section 90 or sub-section (4) of section 90A, is applicable; and

(v) Address of the assessee in the country or specified territory outside India, during the period for which the certificate, as mentioned in (iv) above, is applicable.

(2) The assessee may not be required to provide the information or any part thereof referred to in sub-rule (1) if the information or the part thereof, as the case may be, is contained in the certificate referred to in sub-section (4) of section 90 or sub-section (4) of section 90A.

(2A) The assessee shall keep and maintain such documents as are necessary to substantiate the information provided under sub-rule (1) and an income-tax authority may require the assessee to provide the said documents in relation to a claim by the said assessee of any relief under an agreement referred to in sub-section (1) of section 90 or sub-section (1) of section 90A, as the case may be.

(3) An assessee, being a resident in India, shall, for obtaining a certificate of residence for the purposes of an agreement referred to in section 90 and section 90A, make an application in Form No. 10FA to the Assessing Officer.

(4) The Assessing Officer on receipt of an application referred to in sub-rule (3) and being satisfied in this behalf, shall issue a certificate of residence in respect of the assessee in Form No. 10FB.

Rule – 128

57[Foreign Tax Credit.

128. (1) An assessee, being a resident shall be allowed a credit for the amount of any foreign tax paid by him in a country or specified territory outside India, by way of deduction or otherwise, in the year in which the income corresponding to such tax has been offered to tax or assessed to tax in India, in the manner and to the extent as specified in this rule:

Provided that in a case where income on which foreign tax has been paid or deducted, is offered to tax in more than one year, credit of foreign tax shall be allowed across those years in the same proportion in which the income is offered to tax or assessed to tax in India.

(2) The foreign tax referred to in sub-rule (1) shall mean,—

(a) in respect of a country or specified territory outside India with which India has entered into an agreement for the relief or avoidance of double taxation of income in terms of section 90 or section 90A, the tax covered under the said agreement;

(b) in respect of any other country or specified territory outside India, the tax payable under the law in force in that country or specified territory in the nature of income-tax referred to in clause (iv) of the Explanation to section 91.

(3) The credit under sub-rule (1) shall be available against the amount of tax, surcharge and cess payable under the Act but not in respect of any sum payable by way of interest, fee or penalty.

(4) No credit under sub-rule (1) shall be available in respect of any amount of foreign tax or part thereof which is disputed in any manner by the assessee:

Provided that the credit of such disputed tax shall be allowed for the year in which such income is offered to tax or assessed to tax in India if the assessee within six months from the end of the month in which the dispute is finally settled, furnishes evidence of settlement of dispute and an evidence to the effect that the liability for payment of such foreign tax has been discharged by him and furnishes an undertaking that no refund in respect of such amount has directly or indirectly been claimed or shall be claimed.

(5) The credit of foreign tax shall be the aggregate of the amounts of credit computed separately for each source of income arising from a particular country or specified territory outside India and shall be given effect to in the following manner:—

(i) the credit shall be the lower of the tax payable under the Act on such income and the foreign tax paid on such income:

Provided that where the foreign tax paid exceeds the amount of tax payable in accordance with the provisions of the agreement for relief or avoidance of double taxation, such excess shall be ignored for the purposes of this clause;

(ii) the credit shall be determined by conversion of the currency of payment of foreign tax at the telegraphic transfer buying rate on the last day of the month immediately preceding the month in which such tax has been paid or deducted.

(6) In a case where any tax is payable under the provisions of section 115JB or section 115JC, the credit of foreign tax shall be allowed against such tax in the same manner as is allowable against any tax payable under the provisions of the Act other than the provisions of the said sections (hereafter referred to as the “normal provisions”).

(7) Where the amount of foreign tax credit available against the tax payable under the provisions of section 115JB or section 115JC exceeds the amount of tax credit available against the normal provisions, then while computing the amount of credit under section 115JAA or section 115JD in respect of the taxes paid under section 115JB or section 115JC, as the case may be, such excess shall be ignored.

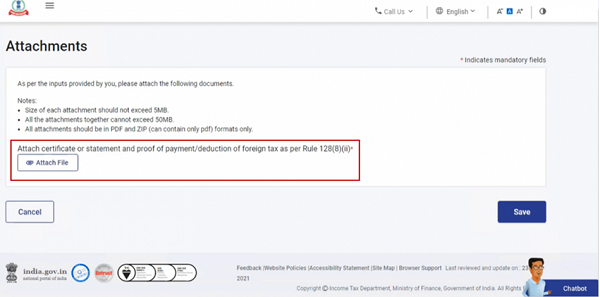

(8) Credit of any foreign tax shall be allowed on furnishing the following documents by the assessee, namely:—

(i) a statement of income from the country or specified territory outside India offered for tax for the previous year and of foreign tax deducted or paid on such income in Form No. 67 and verified in the manner specified therein;

(ii) certificate or statement specifying the nature of income and the amount of tax deducted therefrom or paid by the assessee,—

(a) from the tax authority of the country or specified territory outside India; or

(b) from the person responsible for deduction of such tax; or

(c) signed by the assessee:

Provided that the statement furnished by the assessee in clause (c) shall be valid if it is accompanied by,—

(A) an acknowledgement of online payment or bank counter foil or challan for payment of tax where the payment has been made by the assessee;

(B) proof of deduction where the tax has been deducted.

58[(9) The statement in Form No. 67 referred to in clause (i) of sub-rule (8) and the certificate or the statement referred to in clause (ii) of sub-rule (8) shall be furnished on or before the end of the assessment year relevant to the previous year in which the income referred to in sub-rule (1) has been offered to tax or assessed to tax in India and the return for such assessment year has been furnished within the time specified under sub-section (1) or sub-section (4) of section 139:

Provided that where the return has been furnished under sub-section (8A) of section 139, the statement in Form No. 67 referred to in clause (i) of sub-rule (8) and the certificate or the statement referred to in clause (ii) of sub-rule (8) to the extent it relates to the income included in the updated return, shall be furnished on or before the date on which such return is furnished.]

(10) Form No. 67 shall also be furnished in a case where the carry backward of loss of the current year results in refund of foreign tax for which credit has been claimed in any earlier previous year or years.

Explanation.—For the purposes of this rule “telegraphic transfer buying rate” shall have the same meaning as assigned to it in Explanation to rule 26.]

Notes:

57.Inserted by the IT (Eighteenth Amdt.) Rules, 2016, w.e.f. 1-4-2017.

58.Substituted by the IT (Twenty-seventh Amdt.) Rules, 2022, w.e.f. 1-4-2022.

********

Income Tax Forms

Form No. : 1

1[Appendix IV

FORM NO. 1

[See rule 11UE (1)]

Undertaking under sub-rule (1) of rule 11UE of the Income-tax Rules, 1962

To,

Principal Commissioner/Commission

………………….. ………………………. ……………………

Sir/Madam,

I …………………………………….. (name in block letters) son/daughter of …………………………………………. designation ………………………………….. and nationality …………………………………. and related passport number………………………………….. (hereinafter referred to as “signatory”) having Permanent Account Number/Aadhaar Number (see Note 1) …………………………………………………………………. on behalf of ………………………………………… (name of the declarant) having Permanent Account Number/Aadhaar number/Tax Deduction Account Number (see Note 2) ……………………………………….. and being duly authorised and competent to represent the declarant in this regard pursuant to Board Resolution and legal authorisation (see Note 3), as the case may be ,hereby declare as follows:

a. That specified orders have been passed or made in respect of income accruing or arising through or from the transfer of an asset or a capital asset situate in India in consequence of the transfer of a share or interest in a company or entity registered or incorporated outside India made before the 28th day of May, 2012 and particulars of such specified orders are provided in Part A of the Annexure.

b. The declarant has (strike off the options that are not applicable),

i. not filed any appeal or application or petition or proceeding before any Income-tax authority or Authority for Advance Rulings constituted under section 245-O of the Act or the Board for Advance Rulings constituted under section 245-OB or Income-tax Settlement Commission constituted under section 245B or the Interim Board for Settlement constituted under section 245AA or any tribunal or court against the relevant orders, and hereby undertakes that it shall not file any appeal, application, petition or proceeding in future against the relevant order or orders. Particulars of such relevant order or orders are provided in Part B of the Annexure;

ii. filed one or more appeals or applications or petitions or proceeding before any Income-tax authority or Authority for Advance Rulings constituted under section 245-O of the Act or the Board for Advance Rulings under section 245-OB or Income-tax Settlement Commission constituted under section 245B or the Interim Board for Settlement constituted under section 245AA or any tribunal or court against the relevant orders and has irrevocably withdrawn, on a with prejudice basis, all such appeals or applications or petitions or proceeding and evidence thereof is furnished herewith and hereby undertakes that it shall not file any appeal, application, petition or proceeding in future against the relevant order or orders. Particulars of such appeals or applications or petitions or proceeding filed and irrevocably withdrawn with prejudice by the declarant, are provided in Part C of the Annexure;

iii. filed one or more appeals or applications or petitions or proceeding before any Income-tax authority or Authority for Advance Rulings constituted under section 245-O of the Act or the Board for Advance Rulings under section 245-OB or Income-tax Settlement Commission constituted under section 245B or the Interim Board for Settlement constituted under section 245AA or any tribunal or court against the relevant order or orders and all the appeals or applications or petitions or proceeding filed by the declarant have been disposed of and no further appeal or application or petition or proceeding has been filed by the declarant and evidence thereof is furnished herewith and hereby undertake that it shall not file any appeal, application, petition or proceeding in future against the relevant order or orders. Particulars of such appeals or applications or petitions or proceeding filed and disposed of, are provided in Part C of the Annexure;

iv. filed appeals or applications or petitions or proceeding before any Income-tax authority or Authority for Advance Rulings constituted under section 245-O of the Act or the Board for Advance Rulings under section 245-OB or Income-tax Settlement Commission constituted under section 245B or the Interim Board for Settlement constituted under section 245AA or any tribunal or court against the relevant orders and one or more of such appeals or applications or petitions or proceeding are pending as on the date of this undertaking and hereby undertakes to irrevocably withdraw, terminate and discontinue any and all such appeals or applications or petitions or proceeding that are pending as on the date of signing this undertaking, on a with prejudice basis, in accordance with clause (e) below. The declarant further undertakes that it shall not file any such appeal, application, petition or proceeding in future against the relevant order or orders. Particulars of such pending appeals or applications or petitions or proceeding filed by the declarant and their status as on the date of this undertaking, are provided in Part D of the Annexure;

c. The declarant has (strike off the options that are not applicable),

i. not initiated any proceeding for arbitration, conciliation or mediation, and no notice has been given thereof under any law for the time being in force or under any agreement entered into by India with any other country or territory outside India, whether for protection of investment or otherwise against the relevant orders, and hereby undertakes that it shall not initiate any such arbitration, conciliation or mediation in future. Particulars of such relevant order or orders are provided in Part B of the Annexure;

ii. initiated proceeding for arbitration, conciliation or mediation, or notices thereof has been given, under any law for the time being in force or under any agreement entered into by India with any other country or territory outside India, whether for protection of investment or otherwise against the relevant order or orders and has irrevocably, on a with prejudice basis, withdrawn any such proceeding for arbitration, conciliation or mediation, and notices given thereof and evidence thereof is furnished herewith. The declarant hereby undertakes that it shall not reopen in future any such proceeding or initiate or file any such arbitration, conciliation or mediation in future arising out of or in connection with the relevant order or orders. Particulars of such proceeding for arbitration, conciliation or mediation and notices given thereof, initiated and irrevocably withdrawn with prejudice by the declarant, are provided in Part E of the Annexure;

iii. initiated proceeding for arbitration, conciliation or mediation, or notices thereof has been given, under any law for the time being in force or under any agreement entered into by India with any other country or territory outside India, whether for protection of investment or otherwise against the relevant order or orders and all the arbitration, conciliation or mediation filed by the declarant have been disposed of and no further proceeding has been initiated by the declarant and evidence thereof is furnished herewith. The declarant hereby undertakes that it shall not reopen in future any such proceeding or initiate or file any such arbitration, conciliation or mediation in future arising out of or in connection with the relevant order or orders. Particulars of such proceeding for arbitration, conciliation or mediation and notices given thereof, initiated and disposed of, are provided in Part E of the Annexure;

iv. initiated proceeding for arbitration, conciliation or mediation, or notices thereof has been given, under any law for the time being in force or under any agreement entered into by India with any other country or territory outside India, whether for protection of investment or otherwise against the relevant order or orders and one or more of such proceeding or notices are pending on the date of undertaking and hereby undertakes to irrevocably withdraw, terminate and discontinue any and all such proceeding or notices for arbitration, conciliation or mediation that are pending as on the date of signing this undertaking, on a with prejudice basis, in accordance with clause (e) below. Particulars of such pending proceeding and notices filed by the declarant are provided in Part F of the Annexure. The declarant hereby further undertakes that it shall not initiate any such arbitration, conciliation or mediation in future arising out of or in connection with the relevant order or orders;

v. received or got any awards, orders, judgments or any other reliefs issued in favour of the declarant, arising out of or in any way relating to the imposition of tax, interest and penalty based on the relevant order or orders, under any agreement entered into by India with any other country or territory outside India, whether for protection of investment or otherwise and hereby undertakes to irrevocably waive any right to seek or pursue any claim or costs or declaratory relief in relation to or arising out of such awards, orders or judgments or any other relief that may have been ordered, issued or passed against India and any Indian affiliate, whether it is in proceeding initiated by the declarant or by India and any Indian affiliate. The declarant also undertakes to irrevocably waive any right to seek or pursue any claim for costs or relief in respect of any proceeding initiated by the Republic of India to set aside such award, order or judgment or any other relief issued in favour of the declarant. The declarant hereby undertakes that it shall not initiate or file any such arbitration, conciliation or mediation in future. Particulars of such awards, orders, judgment or any other relief are provided in Part G of the Annexure;

.d. The declarant has (strike off the options that are not applicable),

i. not initiated any proceeding to enforce or pursue attachments in connection with any awards, orders, judgments, any other relief that may have been ordered, issued or passed by any tribunal or court or other judicial, quasi-judicial or administrative authority in relation to the said arbitration, conciliation or mediation proceeding in favour of the declarant as referred in clause (c) of this undertaking either against the Republic of India and any Indian affiliate, and hereby undertakes that it shall not initiate any such proceeding in future. Particulars of such award, order or judgment are provided in Part B of the Annexure;

ii. initiated proceeding to enforce or pursue attachments in connection with any awards, orders, judgments or any other relief that may have been ordered, issued or passed by any tribunal or court or other judicial, quasi-judicial or administrative authority in relation to the said arbitration, conciliation or mediation proceeding in favour of the declarant, as referred to in clause (c) of this undertaking against the Republic of India and any Indian affiliate. The declarant has irrevocably and with prejudice withdrawn or discontinued any such proceeding and hereby undertakes that it shall not reopen any such proceeding in future or file or initiate fresh proceeding to enforce or pursue attachments and evidence thereof is furnished herewith. Particulars of such proceeding, initiated and withdrawn or discontinued by the declarant, are provided in Part H of the Annexure;

iii. initiated proceeding to enforce or pursue attachments in connection with any awards, orders, judgments or any other relief that may have been ordered, issued or passed by any tribunal or court or other judicial, quasi-judicial or administrative authority in relation to the said arbitration, conciliation or mediation proceeding in favour of the declarant, as referred to in clause (c) of this undertaking against the Republic of India and any Indian affiliate. All such proceeding filed by the declarant have been disposed of and no further proceeding has been filed by the declarant and evidence is herewith furnished and hereby undertakes that it shall not reopen any such proceeding in future or file or initiate fresh proceeding to enforce or pursue attachments. Particulars of such proceeding, initiated and disposed of, are provided in Part H of the Annexure;

iv. initiated proceeding to enforce or pursue attachments in connection with any awards, orders, judgments, or any other relief that may have been ordered, issued or passed by any tribunal or court or other judicial, quasi-judicial or administrative authority in relation to the said arbitration, conciliation or mediation proceeding in favour of the declarant as referred to in clause (c) of this undertaking, either against the Republic of India and any Indian affiliate and one or more of such proceeding are pending on the date of undertaking and, the declarant has obtained one or more orders from any court or other authority which remain outstanding against India and any Indian Affiliate. The declarant hereby undertakes that it shall not file in future any such proceeding to enforce or pursue attachments regarding any awards, orders, judgments, or any other relief that may have been ordered , issued or passed by any tribunal or court or other judicial, quasi-judicial or administrative authority in relation to the said arbitration, conciliation or mediation proceeding in favour of the declarant as referenced in clause (c) of this undertaking or to enforce the orders from any court or other authority which remain outstanding against Republic of India and any Indian Affiliate. The declarant further undertakes to fully cooperate with the Republic of India or any Indian affiliate which is subject to such outstanding order, in order to set-aside or otherwise nullify any such outstanding order, and irrevocably and with prejudice waives any rights or remedies arising from such outstanding order. Particulars of such proceeding are provided in Part I of the Annexure. The declarant also undertakes to irrevocably withdraw, terminate and discontinue with prejudice any and all such proceeding to enforce or pursue attachments in accordance with clause (e).

e. The declarant hereby undertakes as follows:

i. to irrevocably and with prejudice withdraw, discontinue, terminate and take all necessary steps to irrevocably and with prejudice close the pending proceeding referred in sub-clause (iv) of clause (b), sub-clause (iv) of clause (c), sub-clause (v) of clause (c) and sub-clause (iv) of clause (d) of this undertaking, as well as any other pending proceeding against India or Indian affiliates relating to the relevant order or orders and not referenced in clauses (b), (c) and (d) above, and not to pursue in any way and by any means in future the pending proceeding as referenced in clauses (b), (c), and (d) above, and any other pending proceeding relating to the relevant order or orders not referred in the above clauses and any other fresh proceeding relating to the relevant order or orders. In so acting, declarant shall act in accordance with this undertaking and in full cooperation with the Republic of India;

ii. to irrevocably terminate, release, discharge, and forever irrevocably waive any right, whether direct or indirect, and any claims, demands, liens, actions, suits, causes of action, obligations, controversies, debts, costs, attorneys’ fees, court’s fees, expenses, damages, judgments, orders, declaratory reliefs and liabilities of whatever kind or nature at law, in equity, or otherwise, whether now known or unknown previously (or in future discovered), suspected or unsuspected, and whether or not concealed or hidden, which have existed or may have existed, or do exist or which hereafter can, shall or may exist , in relation to any award, order, judgment, or any other relief as referred in clauses (b), (c) and (d) of this undertaking, against the Republic of India and all Indian affiliates, ordered, issued or passed in connection with the relevant order or orders, whether it is in proceeding initiated by the declarant or by Republic of India and any Indian Affiliate. The declarant further undertakes to fully cooperate with the Republic of India or any Indian affiliate which is subject to any outstanding order referenced in clause (d), in order to set-aside or otherwise nullify any such outstanding order, and irrevocably and with prejudice waives any rights or remedies arising from such outstanding order. For the avoidance of doubt, the declarant’s irrevocable waiver includes irrevocable waiver of any right provided by any existing ex parte, provisional, or other kind of court order permitting enforcement or attachment against the Republic of India and any Indian affiliate, in furtherance of any award, order judgment, or any other relief that may have been ordered or issued or passed by any arbitral tribunal as referred in clauses (b), (c) and (d) above. For further avoidance of doubt, the declarant also undertakes to irrevocably waive any right to seek or pursue any claim for costs in respect of any proceeding initiated by Republic of India and any Indian affiliate to set aside such award, order or judgement ordered, issued or passed in favour of the declarant. Such irrevocable waiver includes, but is not limited to, any right under any relevant ex parte order;

iii. to irrevocably waive any right to seek or pursue any claim for costs in respect of any proceeding initiated by the Republic of India to set aside such award, order or judgment, or any other relief issued in favour of the declarant.

f. The declarant specifically represents that all Parts of the Annexure as described in this undertaking are full and complete to the best of its knowledge.

g. The declarant hereby undertakes to irrevocably terminate, release, discharge and forever irrevocably waive any right, whether direct or indirect, and any remedies, claims, demands, liens, actions, suits, causes of action, obligations, controversies, debts, costs, attorneys’ fees, court’s fees, expenses, damages, judgments, orders, compensation, and liabilities of whatever kind or nature at law, in equity, or otherwise, whether now known or unknown, suspected or unsuspected, and whether or not concealed or hidden, which have existed or may have existed, or do exist or which hereafter can, shall or may exist, based on pursuit of any remedy or any and all claims, demands, damages, judgments, awards, costs, expenses, compensation or liabilities of any kind (whether asserted or unasserted) in relation to any facts, events, or omissions occurring from the beginning of time to the date of this undertaking and thereafter in future in relation to taxation of said income or relevant order or orders, or any related award, judgment or court order, which may otherwise be available to the declarant under any law for the time being in force, in equity, under any statute or under any agreement entered into by Republic of India with any country or territory outside Republic of India, whether for protection of investment or otherwise , whether it is in proceeding initiated by the declarant or by Republic of India and any Indian affiliate. For the avoidance of doubt, the declarant’s above waiver includes an irrevocable waiver of any claim against India and any Indian Affiliate to costs incurred or interest accrued in relation to the relevant order or orders, or any related ongoing or completed litigation, arbitration, conciliation or mediation. Moreover, for the avoidance of any doubt, the declarant hereby undertakes (for itself and on behalf of all related parties) to forgo any reliance on any right under any award, judgment, or court order pertaining to the relevant order or orders or under the relevant order or orders.

h. The declarant further represents that as of the date of this undertaking, it has not transferred any of its claims under any award, judgment, or court order pertaining to the relevant order or orders or under the relevant order or orders, or granted any rights, to third parties, and further undertakes to not transfer any of its claims to third parties after entering this undertaking. Where any such claim or right is transferred, the declarant confirms that it has provided the particulars of all the interested parties in Part L, and the undertakings from each of such interested parties is attached with this undertaking in accordance with Part M of the Annexure.

i. In the event that, notwithstanding the foregoing, any person asserts, brings, files or maintains any claim against the Republic of India or Indian affiliates (hereinafter collectively referred to as “releases”) at any time on or after the date of furnishing this undertaking, the declarant shall indemnify, defend and hold harmless such releases from and against any and all costs, expenses (including attorney’s fees and court’s fees), interest, damages, and liabilities of any nature arising out of or in any way relating to the assertion or, bringing, filing or maintaining of such claim. The declarant specifically represents that, to the best of its knowledge, after—

i. the execution of this undertaking;

ii. the execution of any separate related undertaking by any other party in connection with the relevant order or orders; and

iii. irrevocable withdrawal of all pending proceeding as outlined in this undertaking, no other claim regarding the said relevant order or orders referenced above, or any related award, judgment, or court order, shall remain outstanding against the Republic of India or any Indian affiliates. To avoid any doubt, the declarant’s indemnity of releases under this clause shall include any claim brought by any third party alleging that it has obtained the declarant’s claims under an award, judgment or court order or the relevant order or orders. An indemnity bond to this effect is attached in Part N of the undertaking.

j. For the removal of any doubt, the declarant fully assumes the risk through the indemnity in clause (i) of any omission or mistake with respect to securing releases against any related claim by any person. If the declarant fails to obtain any release from such person, the declarant warrants that it will indemnify the Republic of India or any Indian affiliates from any defense costs, court costs, and damages. An indemnity bond to the effect of clauses (i) and (j) is annexed to the undertaking.

k. The declarant further undertakes to refrain from facilitating, procuring, encouraging or otherwise assisting any person (including but not limited to any related party or interested party) from bringing any proceeding or claims of any kind referred to in the above clauses, or any proceeding or claim of any kind related to any relevant order or orders referred to above (whether in respect of tax, interest or penalty). The declarant shall notify by a public notice or press release, at any time before furnishing intimation in Form No. 3 where this Form is required to be furnished under rule 11UF and before furnishing this undertaking in other cases, that by signing this undertaking any claims arising out of or relating to the relevant order or orders or any related award, judgment or court order, no longer subsist. Such public notice or press release shall include, among other things, confirmation that,—

i. the declarant (and its related parties) forever irrevocably forgo any reliance on any right and provisions under any award, judgment or court order pertaining to the relevant order or orders or under the relevant order or orders;

ii. the declarant has provided this undertaking, which includes a complete release of the Republic of India and any Indian Affiliates with respect to any award, judgment or court order pertaining to the relevant order or orders or under the relevant order or orders, and with respect to any claim pertaining to the relevant order or orders;

iii. the undertaking also includes an indemnity against any claims brought against the Republic of India or any India affiliate, including by related parties or interested parties, contrary to the release; and

iv. the declarant confirms it will treat any such award, judgment or court order as null and void and without legal effect to the same extent as if it had been set aside by a competent court and will not take any action or initiate any proceeding or bring any claim based on that.

l. The declarant confirms that the undertakings given herein are intended to be enforceable by the Republic of India, including so as to secure the irrevocable waiver, withdrawal or discontinuance (as appropriate) of all the proceeding and claims referred to in any of the clauses of this undertaking.

m. The declarant represents and warrants that:

i. it has full legal power and authority to execute and deliver this undertaking (including but not limited to the issuance of the indemnity described in clauses (i) and (j)under applicable law;

ii. the execution, delivery and performance of this undertaking (including but not limited to the issuance of the indemnity described in clauses (i) and (j) has been duly authorised by all necessary corporate action, including but not limited to any board resolution or similar authorisation under applicable law (see Note 3);

iii. this undertaking constitutes the legal, valid and binding obligation of the declarant, enforceable against the declarant in accordance with its terms;

iv. such authorisations described in the above sub-clauses (i), (ii) and (iii) are effective under applicable law, and to this end, letters from local counsel in the relevant jurisdictions are attached to this undertaking which confirm the legality of such authorisations under applicable law.

n. The declarant confirms that by submitting the present undertaking, it fulfills the conditions specified in the Explanation below the sixth proviso to Explanation 5 to clause (i) of sub-section (1) of section 9.

o. The details of the bank account in which the refund may be credited are provided in Part J of the Annexure.

p. The details of all the interested parties are provided in Part K and Part L of the Annexure. The undertaking in Part M of the Annexure by each of such persons is attached with this undertaking. The declarant represents and warrants that:

i. all such undertakings have been executed and delivered by the person who has full legal power and authority to execute and deliver such undertakings;

ii. the execution, delivery and performance of this undertaking has been duly authorised by all necessary corporate action; and

iii. this undertaking constitutes the legal, valid and binding obligation of the declarant, enforceable against such person in accordance with its terms. Such separate, related undertakings may take the same form as this undertaking.

q. The declarant is or is not covered under sub-rule (6) of rule 11UF and in case if the declarant is not covered under said sub-rule all the conditions provided under sub-rule (2) of rule 11UE have been fulfilled.

r. This undertaking is governed by relevant Indian law and any dispute with respect to this undertaking shall be subject to Indian laws and be decided in accordance with the procedures specified in the Act under the exclusive jurisdiction of the relevant income-tax authorities, tribunals or courts in Republic of India, as the case may be, which are empowered to decide disputes under the Act.

I also confirm that I am aware of all the consequences and implications of this undertaking.

Place:…………………………………

Signature:………………………………….

Date: …………………………………………………………………………………………………………………………….

Attachments

1. The Board Resolution or legal authorisation, as the case may be, as referred to in clause (m) of the undertaking

2. An indemnity bond to the effect of clause (i) and clause (j) of the undertaking attached in Part N of the undertaking.

3. Copy of the public notice referred to in clause (k) of the undertaking, where Form No. 3 is not required to be furnished under sub-rule (6) of rule 11UF.

4. Attachments as required in different parts of the Annexure to this undertaking.

Notes

1. This information is required to be furnished where the Permanent Account Number or Aadhaar Number of the signatory is available.

2. Company Identification Number and Taxpayer Identification Number are to be provided where Permanent Account Number or Aadhaar Number or Tax Deduction Account Number of the declarant are not available.

3. The Board Resolution or legal authorisation, as referred to in clause (m) of the undertaking shall, among other things:

a. record the signatory’s power and authority to give the undertaking on behalf of the declarant; and

b. record the declarant’s power and authority to indemnify defend and hold harmless the Republic of India and the Indian affiliates in accordance with clause (i) of the undertaking.

VERIFICATION

Verified that the contents of this undertaking are true to the best of my knowledge and belief. No part of the undertaking is false and nothing has been concealed or misstated therein.

Verified at________________ place_______________ on this the_________ day________________ of ______ month_______________ , year .

Place: ……………………

Date:……………………..

Signature…………………………

Annexure

Part A– Particulars of the relevant order or orders:

| Sl. No. | Assessment Year or Financial year | Income-tax Authority passing the order | Details of the order under consideration |

Taxes or penalty determined |

Interest | Total demand |

Relief, provided in any appeal proceeding , if any |

Demand recovered from the declarant |

Pending demand or refund due as on date | Details of the attachments made by any Income-tax Authority | |

| Section and sub-section of the Income-tax Act, 1961 |

Date of order | ||||||||||

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | (12) |

Part B– Particulars of the relevant order or orders covered by sub-clause (i) of clauses (b), (c) and (d) of the undertaking:

| Sl. No. | Sl. No. in Part A where the relevant order is mentioned | No appeal or application or petition or proceeding before any Income-tax authority or Authority for Advance Rulings constituted under section 245-O of the Act or the Board for Advance Rulings under section 245-OB or Income-tax Settlement Commission constituted under section 245B or the Interim Board for Settlement constituted under section 245AA or any tribunal or court has been filed(refer clause (b)(i) of the undertaking). |

No proceeding has been initiated for arbitration, conciliation or mediation, and no notice has been given thereof under any law for the time being in force or under any agreement entered into by India with any other country or territory outside India, whether for protection of investment or otherwise (refer clause (c)(i) of the undertaking). |

No proceeding initiated to enforce or pursue attachments in connection with any award, order or judgment, any other relief that may have been ordered or issued or passed by any tribunal or court or other judicial or administrative authority in relation to the said arbitration, conciliation or mediation proceeding in favour of the declarant against the Republic of India and Indian affiliates (refer clause (d)(i) of the undertaking). |

| (1) | (2) | (3) | (4) | (5) |

| Applicable or Not applicable | Applicable or Not applicable | Applicable or Not applicable |

Part C: Particulars of the appeals or applications or petitions or proceeding under sub-clauses (ii) and (iii) of clause (b) of the undertaking:

| Sl. No. | Sl. No. in Part A where the relevant order is mentioned | Nature of appeals or applications or petitions or proceeding | Income-tax authority or Authority for Advance Rulings constituted under section 245-O of the Act or the Board for Advance Rulings under section 245-OB or Income-tax Settlement Commission constituted under section 245B or the Interim Board for Settlement constituted under section 245AA or any tribunal or court before whom such appeals or applications or petitions or proceeding has been filed |

Date of filing the appeals or applications or petitions or proceeding | Date of disposing of or withdrawal such appeals or applications or petitions or proceeding (Please attach a copy of order by the Income-tax authority or Authority for Advance Rulings constituted under section 245-O of the Act or the Board for Advance Rulings under section 245-OB or Income-tax Settlement Commission constituted under section 245B or the Interim Board for Settlement constituted under section 245AA or any tribunal or court accepting the withdrawal or disposing of) |

| (1) | (2) | (3) | (4) | (5) | (6) |

Part D – Particulars of the appeals or applications or petitions or proceeding under sub-clause (iv) of clauses (b) of the undertaking:

| Sl. No. | Sl. No. in Part A where the relevant order is mentioned | Nature of appeals or applications or petitions or proceeding | Income-tax authority or Authority for Advance Rulings constituted under section 245-O of the Act or the Board for Advance Rulings under section 245-OB or Income-tax Settlement Commission constituted under section 245B or the Interim Board for Settlement constituted under section 245AA or any tribunal or court before whom such appeals or applications or petitions or proceeding has been filed | Date of filing the appeals or applications or petitions or proceeding |

| (1) | (2) | (3) | (4) | (5) |

Part E – Particulars of the proceeding for arbitration, conciliation or mediation, or notices under sub-clause (ii) and (iii) of clause (c) of the undertaking:

Sr. No. |

Sl. No in Part A where the

|

Nature of proceeding for arbitration,

|

Particulars (including the name of the country) where such proceeding for

|

Date of initiating the proceeding for arbitration, conciliation or

|

Name of the agreement entered into

|

Status of the proceeding for arbitration,

|

Date of disposing of or withdrawal of such proceeding

|

(1) |

(2) |

(3) |

(4) |

(5) |

(6) |

(7) |

(8) |

Part F – Particulars of the proceeding for arbitration, conciliation or mediation, or notices under sub-clause (iv) of clause (c) of the undertaking:

| Sl. No. | Sl. No in Part A where the relevant order is mentioned | Nature of proceeding for arbitration, conciliation or mediation, or notices thereof with case number or Notice given | Particulars (including the name of the country where such proceeding for arbitration, conciliation or mediation are pending or notices thereof have been issued) | Date of initiating the proceeding for arbitration, conciliation or mediation/issue of notice | Name of the agreement entered into by India under which proceeding for arbitration, conciliation or mediation are pending | Status of the proceeding for arbitration, conciliation or mediation |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) |

Part G – Particulars of the award, order or judgment or any other relief under sub-clause (v) of clause (c) of the undertaking:

| Sl. No. | Sl. No. in Part A where the relevant order is mentioned |

Nature of such award, order or judgment or any other relief |

Particulars (including the name of the country) where proceeding related to such award, order, judgment or any other relief were held |

Date of such award, order, judgment or any other relief along with reference number |

Status of the award, order, judgment or any other relief |

| (1) | (2) | (3) | (4) | (5) | (6) |

Part H – Particulars of the proceeding to enforce any award, order or judgment or any other relief under sub-clauses (ii) and (iii) of clause (d) of the undertaking:

Sl. No. |

Sl. No. in Part A where the relevant order is mentioned |

Nature of proceeding to enforce such award, order or judgment or any other relief |

Particulars (including the name of the country where such proceeding to enforce any award, order or judgment or any other relief are taking place) |

Date of filing proceeding to enforce any award, order or judgment or any other relief |

Nature of such award, order or judgment or any other relief (Attach copy thereof) |

Status of the proceeding to enforce such award, order or judgment or any other relief |

Date of disposing of or withdrawal of proceeding to enforce such award, order or judgment or any other relief (Please attach a copy of evidence of such disposing of/withdrawal, including order of the Court or other judicial authority) |

(1) |

(2) |

(3) |

(4) |

(5) |

(6) |

(7) |

(8) |

Part I – Particulars of the proceeding to enforce any award, order or judgment or any other relief under sub-clause (iv) of clause (d) of the undertaking:

| Sl. No. | Sl. No in Part A where the relevant order is mentioned | Nature of proceeding to enforce such award, order or judgment or any other relief | Particulars (including the name of the country where such proceeding to enforce any award, order or judgment or any other relief are taking place) | Date of filing proceeding to enforce any award, order or judgment or any other relief | Nature of such award, order or judgment or any other relief (Attach copy thereof) | Status of the proceeding to enforce such award, order or judgment or any other relief |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) |

Part J – Details of bank account in Republic of India to which the refund is to be remitted

| Sl. No. | Bank Name and Address | Account Number and other required details for remittance |

| (1) | (2) | (3) |

Part K– Details of all the companies or entities in the entire chain of holding of the declarant till the ultimate holding company or entity of the declarant:

| Sl. No. |

Name of holding company |

Percentage of the ownership by such holding company in the declarant as on the date of undertaking |

If the ownership in the declarant is not held directly by such holding company, the chain of ownership with the names of all the companies in the chain of ownership |

| (1) | (2) | (3) | (4) |

Part L- Details of all the interested parties other than the interested parties covered under Part K

| Sl. No. |

Name of such persons whose interest may be affected directly or indirectly by this undertaking | Nature of interest of such person | Amount of interest of such person (Rs), if available |

| (1) | (2) | (3) | (4) |

PART M Undertaking by person(s) declared in Part K and Part L of the Undertaking

To,

Principal Commissioner/Commissioner

……………….. ……………………… ………….

Sir/Madam,

I………………….. (name in block letters) son/daughter of…………………………………………….. designation ……………….. .and nationality …………………………. .and related passport number……………………………… (hereinafter referred to as “signatory”) having Permanent Account Number/Aadhaar Number (see Note 1) ………………………………. on behalf of …………………………………. . (name of the interested party) having Permanent Account Number/Aadhaar number/Tax Deduction Account Number (see Note 2) …………………………………………. . and being duly authorised and competent to represent the interested party in this regard pursuant to Board Resolution and legal authorisation (see Note 3), as the case may be , hereby declare as follows:

(a) The particulars of specified orders that have been passed or made in respect of income accruing or arising through or from the transfer of an asset or a capital asset situate in India in consequence of the transfer of a share or interest in a company or entity registered or incorporated outside Republic of India made before the 28th day of May, 2012 in the case of declarant and the nature of interest of the interested party in such specified orders are provided in Part MA of the Annexure.

(b) The interested party has (strike off options that are not applicable):

i. not filed any appeal or application or petition or proceeding before any Income-tax authority or Authority for Advance Rulings constituted under section 245-O of the Act or the Board for Advance Rulings under section 245-OB or Income-tax Settlement Commission constituted under section 245B or the Interim Board for Settlement constituted under section 245AA or any tribunal or court against the relevant order or orders, and hereby undertakes that it shall not file any appeal, application, petition or proceeding in future against the relevant order or orders. Particulars of such relevant order or orders are provided in Part MB of the Annexure;

ii. filed one or more appeals or applications or petitions or proceeding before any Income-tax authority or Authority for Advance Rulings constituted under section 245-O of the Act or the Board for Advance Rulings under section 245-OB or Income-tax Settlement Commission constituted under section 245B or the Interim Board for Settlement constituted under section 245AA or any tribunal or court against the relevant order or orders and has irrevocably, on a with prejudice basis, withdrawn all such appeals or applications or petitions or proceeding or such appeals or applications or petitions or proceeding have been disposed at any time before the date of filing Form No. 1, and hereby undertake that it shall not file any appeal, application, petition or proceeding in future against the relevant order or orders. Particulars of such appeals or applications or petitions or proceeding filed and irrevocably withdrawn with prejudice by the interested party, are provided in Part MC of the Annexure.

iii. filed one or more appeals or applications or petitions or proceeding before any Income-tax authority or Authority for Advance Rulings constituted under section 245-O of the Act or the Board for Advance Rulings under section 245-OB or Income-tax Settlement Commission constituted under section 245B or the Interim Board for Settlement constituted under section 245AA or any tribunal or court against the relevant order or orders and all the appeals or applications or petitions or proceeding filed by the interested party have been disposed of and no further appeal or application or petition or proceeding has been filed by the interested party and evidence thereof is furnished herewith and hereby undertake that it shall not file any appeal, application, petition or proceeding in future against the relevant order or orders. Particulars of such appeals or applications or petitions or proceeding filed and disposed of, are provided in Part MC of the Annexure.

iv. filed appeals or applications or petitions or proceeding before any Income-tax authority or Authority for Advance Rulings constituted under section 245-O of the Act or the Board for Advance Rulings under section 245-OB or Income-tax Settlement Commission constituted under section 245B or the Interim Board for Settlement constituted under section 245AA or any tribunal or court against the relevant order or orders and one or more of such appeals or applications or petitions or proceeding are pending as on the date of this undertaking and hereby undertakes to irrevocably withdraw, terminate and discontinue any and all such appeals or applications or petitions or proceeding that are pending as on the date of signing this undertaking, on a with prejudice basis, in accordance with clause (e) below. The interested party further undertakes that it shall not file any such appeal, application, petition or proceeding in future against the relevant order or orders. Particulars of such pending appeals or applications or petitions or proceeding filed by the interested party and their status as on the date of this undertaking, are provided in Part D of the Annexure. Particulars of any appeals or applications or petitions or proceeding as described in this clause (b) which are not covered by the sub-clauses (i) and (ii) are also provided in Part MD of the Annexure.

(c) The interested party has (strike off options that are not applicable):

i. not initiated any proceeding for arbitration, conciliation or mediation, and no notice has been given thereof under any law for the time being in force or under any agreement entered into by Republic of India with any other country or territory outside India, whether for protection of investment or otherwise against the relevant order or orders, and hereby undertakes that it shall not initiate any such arbitration, conciliation or mediation in future. Particulars of such relevant order or orders are provided in Part MB of the Annexure;

ii. initiated proceeding for arbitration, conciliation or mediation, or notices thereof has been given, under any law for the time being in force or under any agreement entered into by India with any other country or territory outside India, whether for protection of investment or otherwise against the relevant order or orders and has irrevocably, on a with prejudice basis, withdrawn any such proceeding for arbitration, conciliation or mediation, and notices given thereof. The interested party hereby undertakes that it shall not reopen in future any such proceeding or initiate or file any such arbitration, conciliation or mediation in future arising out of or in connection with the relevant order or orders. Particulars of such proceeding for arbitration, conciliation or mediation and notices given thereof, initiated and irrevocably withdrawn with prejudice by the interested party, are provided in Part ME of the Annexure.

iii. initiated proceeding for arbitration, conciliation or mediation, or notices thereof has been given, under any law for the time being in force or under any agreement entered into by Republic of India with any other country or territory outside India, whether for protection of investment or otherwise against the relevant order or orders and all the arbitration, conciliation or mediation filed by the interested party have been disposed of and no further proceeding has been initiated by the interested party and evidence thereof is furnished herewith. The interested party hereby undertakes that it shall not reopen in future any such proceeding or initiate or file any such arbitration, conciliation or mediation in future arising out of or in connection with the relevant order or orders. Particulars of such proceeding for arbitration, conciliation or mediation and notices given thereof, initiated and disposed of, are provided in Part ME of the Annexure.

iv. has initiated proceeding for arbitration, conciliation or mediation, or notices thereof has been given, under any law for the time being in force or under any agreement entered into by Republic of India with any other country or territory outside Republic of India, whether for protection of investment or otherwise against the relevant order or orders and one or more of such proceeding or notices are pending on the date of undertaking and hereby undertakes to irrevocably withdraw, terminate and discontinue any and all such proceeding or notices for arbitration, conciliation or mediation that are pending as on the date of signing this undertaking, on a with prejudice basis, in accordance with clause (e). Particulars of such pending proceeding and notices filed by the interested party are provided in Part F of the Annexure. The interested party hereby further undertakes that it shall not initiate any such arbitration, conciliation or mediation in future arising out of or in connection with the relevant order or orders. Particulars of any proceeding for arbitration, conciliation or mediation, or notices thereof, which are not covered by the sub-clause (i) and sub- clause (ii), are also provided in Part MF of the Annexure.

v. received or got any awards, orders, judgements or any other reliefs issued in favour of the interested party, arising out of or in any way relating to the imposition of tax, interest and penalty based on the relevant order or orders, under any agreement entered into by India with any other country or territory outside India, whether for protection of investment or otherwise and hereby undertakes to irrevocably waive any right to seek or pursue any claim or costs or declaratory relief in relation to or arising out of such awards, orders or judgments or any other relief that may have been ordered, issued or passed against India and any Indian affiliate, whether it is in proceeding initiated by the interested party or by India and any Indian affiliate. The interested party also undertakes to irrevocably waive any right to seek or pursue any claim for costs in respect of any proceeding initiated by the Republic to set aside such award, order or judgment issued in favour of the interested party. The interested party hereby undertakes that it shall not initiate or file any such arbitration, conciliation or mediation in future. Particulars of such awards, orders, judgment or any other relief are provided in Part MG of the Annexure.

(d) The interested party has (strike off options that are not applicable):

i. not initiated any proceeding to enforce or pursue attachments in connection with any awards, orders, judgments, or any other relief that may have been ordered, issued or passed by any tribunal or court or other judicial, quasi-judicial or administrative authority in relation to the said arbitration, conciliation or mediation proceeding in favour of the interested party as referred in clause (c) of this undertaking either against the Republic of India and any Indian affiliate, and hereby undertakes that it shall not initiate any such proceeding in future. Particulars of such award, order or judgment are provided in Part MB of the Annexure.

ii. initiated proceeding to enforce or pursue attachments in connection with any awards, orders, judgements or any other relief that may have been ordered, issued or passed by any tribunal or court or other judicial, quasi-judicial or administrative authority in relation to the said arbitration, conciliation or mediation proceeding in favour of the interested party, as referred to in clause (c) of this undertaking against the Republic of India and any Indian affiliate. The interested party has irrevocably and with prejudice withdrawn or discontinued any such proceeding and hereby undertakes that it shall not reopen any such proceeding in future or file fresh proceeding to enforce or pursue attachments. Particulars of such proceeding, initiated and withdrawn or discontinued by the interested party, are provided in Part MH of the Annexure.

iii. initiated proceeding to enforce or pursue attachments in connection with any awards, orders, judgements or any other relief that may have been ordered, issued or passed by any tribunal or court or other judicial, quasi-judicial or administrative authority in relation to the said arbitration, conciliation or mediation proceeding in favour of the interested party, as referred to in clause (c) of this undertaking against the Republic of India and any Indian affiliate. All such proceeding filed by the interested party have been disposed of and no further proceeding has been filed by the interested party and evidence is herewith furnished and hereby undertakes that it shall not reopen any such proceeding in future or file or initiate fresh proceeding to enforce or pursue attachments. Particulars of such proceeding, initiated and disposed of, are provided in Part MH of the Annexure.

iv. initiated proceeding to enforce or pursue attachments in respect of any awards, orders, judgments, or any other relief that may have been ordered, issued or passed by any tribunal or court or other judicial, quasi-judicial or administrative authority in relation to the said arbitration, conciliation or mediation proceeding in favour of the interested party as referred to in clause (c) of this undertaking, either against the Republic of India and any Indian affiliate and one or more of such proceeding are pending on the date of undertaking and, interested party has obtained one or more orders from any court or other authority which remain outstanding against India and any Indian affiliate. The interested party hereby undertakes that it shall not file in future any such proceeding to enforce or pursue attachments regarding any awards, orders, judgments, or any other relief that may have been ordered , issued or passed by any tribunal or court or other judicial, quasi-judicial or administrative authority in relation to the said arbitration, conciliation or mediation proceeding in favour of the interested party as referenced in clause (c) of this undertaking or to enforce the orders from any court or other authority which remain outstanding against India and any Indian affiliate. The interested party further undertakes to fully cooperate with the Republic of India or any Indian affiliate which is subject to such outstanding order, in order to set-aside or otherwise nullify any such outstanding order, and irrevocably and with prejudice waives any rights or remedies arising from such outstanding order. Particulars of such proceeding, are provided in Part MI of the Annexure. Particulars of any such proceeding, to enforce or pursue attachments in connection with any awards, orders, judgments, or any other relief, which are not covered by the sub-clauses (i) and (ii), are also provided in Part MI of the Annexure. The interested party also undertakes to irrevocably withdraw, terminate and discontinue with prejudice any and all such proceeding to enforce or pursue attachments in accordance with clause (e) below.

(e) The interested party hereby undertakes as follows: –

i. to irrevocably and with prejudice withdraw, discontinue, terminate and take all necessary steps to irrevocably and with prejudice close the pending proceeding referred in sub-clause (iv) of clause (b), sub-clause (iv) of clause (c), sub-clause (v) of clause (c) and sub-clause (iv) of clause (d) of this undertaking, as well as any other pending proceeding against Republic of India or Indian affiliates relating to the relevant order or orders and not referenced in clauses (b), (c) and (d) above, and not to pursue in any way and by any means in future the pending proceeding as referenced in clauses (b), (c) and (d) and any other pending proceeding relating to the relevant order or orders not referred in the above clauses and any other fresh proceeding relating to the relevant order or orders. In so acting, interested party shall act in accordance with this undertaking and in full cooperation with the Republic of India.

ii. to irrevocably terminate, release, discharge, and forever irrevocably waive any right, whether direct or indirect, and any claims, demands, liens, actions, suits, causes of action, obligations, controversies, debts, costs, attorneys’ fees, court’s fees, expenses, damages, judgments, orders, declaratory reliefs, and liabilities of whatever kind or nature at law, in equity, or otherwise, whether now known or unknown previously (or in future discovered), suspected or unsuspected, and whether or not concealed or hidden, which have existed or may have existed, or do exist or which hereafter can, shall or may exist , in relation to any award, order, judgment, or any other relief as referred in clauses (b), (c) and (d) of this undertaking, against the Republic of India and all Indian affiliates, ordered, issued or passed in connection with the relevant order or orders, whether it is in proceeding initiated by the interested party or by India and any Indian affiliate. For the avoidance of doubt, the interested party’s irrevocable waiver includes irrevocable waiver of any right provided by any existing ex parte, provisional, or other kind of court order permitting enforcement or attachment against the Republic of India and any Indian affiliate, in furtherance of any award, order, judgment, or any other relief that may have been ordered or issued or passed by any arbitral tribunal as referred in clauses (b), (c) and (d). The interested party further undertakes to fully cooperate with the Republic of India or any Indian affiliate which is subject to any outstanding order referenced in clause (d), in order to set aside or otherwise nullify any such outstanding order, and irrevocably and with prejudice waives any rights or remedies arising from such outstanding order. For further avoidance of doubt, the interested party also undertakes to irrevocably waive any right to seek or pursue any claim for costs in respect of any proceeding initiated by Republic of India and any Indian Affiliate to set aside such award, order or judgment ordered, issued or passed in favour of the interested party. Such irrevocable waiver includes, but is not limited to, any right under any relevant ex parte order.

iii. to irrevocably waive any right to seek or pursue any claim for costs in respect of any proceeding initiated by the Republic of India to set aside such award, order or judgment, or any other relief issued in favour of the interested party.

(f) The interested party specifically represents that all Parts of the Annexure as described in this undertaking are full and complete to the best of its knowledge.

(g) The interested party hereby undertakes to irrevocably terminate, release, discharge, and forever irrevocably waive any right, whether direct or indirect, and any remedies, claims, demands, liens, actions, suits, causes of action, obligations, controversies, debts, costs, attorneys’ fees, court’s fees, expenses, damages, judgments, orders, compensation and liabilities of whatever kind or nature at law, in equity, or otherwise, whether now known or unknown, suspected or unsuspected, and whether or not concealed or hidden, which have existed or may have existed, or do exist or which hereafter can, shall or may exist, based on pursuit of any remedy or any and all claims, demands, damages, judgments, awards, costs, expenses, compensation or liabilities of any kind (whether asserted or unasserted) in relation to any facts, events, or omissions occurring from the beginning of time to the date of this undertaking and thereafter in future in relation to taxation of said income or relevant order or orders, or any related award, judgment or court order, which may otherwise be available to the interested party under any law for the time being in force, in equity, under any statute or under any agreement entered into by India with any country or territory outside India, whether for protection of investment or otherwise , whether it is in proceeding initiated by the interested party or by India and any Indian affiliate. For the avoidance of doubt, the interested party’s above waiver includes an irrevocable waiver of any claim against India and any Indian affiliate to costs incurred or interest accrued in relation to the relevant order or orders, or any related ongoing or completed litigation, arbitration, conciliation or mediation. Moreover, for the avoidance of any doubt, the interested party hereby undertakes to forgo any reliance on any right under any award, judgment, or court order pertaining to the relevant order or orders or under the relevant order or orders.

(h) The interested party further represents that as of the date of this undertaking, it has not transferred any of its claims under any award, judgment, or court order pertaining to the relevant order or orders or under the relevant order or orders, or granted any rights, to third parties, and further undertakes to not transfer any of its claims to third parties after entering this undertaking.

(i) In the event that, notwithstanding the foregoing, any person asserts, brings , files or maintains any claim against the Republic of India or Indian affiliates (hereinafter collectively referred to as “releasees”)at any time on or after the date of furnishing this undertaking, the interested party shall indemnify, defend and hold harmless such releasee from and against any and all costs, expenses (including attorneys’ fees and court’s fees), interest, damages, and liabilities of any nature arising out of or in any way relating to the assertion or, bringing, filing or maintaining of such claim. The interested party specifically represents that, to the best of its knowledge, after

i. the execution of this undertaking;

ii. the execution of any separate related undertaking by any other party in connection with the relevant order or orders; and

iii. irrevocable withdrawal of all pending proceeding as outlined in this undertaking.

no other claim regarding the said relevant order or orders referenced above, or any related award, judgment, or court order, shall remain outstanding against the Republic of India or any Indian affiliate. To avoid any doubt, the interested party’s indemnity of releasees shall include any claim brought by any third party alleging that it has obtained the interested party’s claims under an award, judgment or court order or the relevant order or orders. An indemnity bond to this effect is attached in Part N of the undertaking.

(j) For the avoidance of any doubt, the interested party fully assumes the risk through the indemnity in clause (i) of any omission or mistake with respect to securing releases against any related claim by any person. If the interested party fails to obtain any release from such person, the interested party warrants that it will indemnify the Republic of India or any Indian affiliates from any defense costs, court costs, and damages. An indemnity bond to the effect of clauses (i) and (j) is annexed to the undertaking.

(k) The interested party further undertakes to refrain from facilitating, procuring, encouraging or otherwise assisting any party (including but not limited to any related party) from bringing any proceeding or claims of any kind referred to in the above clauses, or any proceeding or claim of any kind related to any relevant order or orders referred to above (whether in respect of tax, interest or penalty). The interested party shall notify by a public notice or press release, at any time before furnishing intimation in Form No. 3 where Form No. 3 is required to be furnished under rule 11UF and before furnishing this undertaking in other cases, that by signing this undertaking any claims arising out of or relating to the relevant order or orders or any related award, judgment or court order, no longer subsist. Such public notice shall include, among other things, confirmation that,-

i. the interested party forever irrevocably forgoes any reliance on any right and provisions under any award, judgment, or court order pertaining to the relevant order or orders or under the relevant order or orders;

ii. the interested party has provided this undertaking, which includes a complete release of the Republic of India and any Indian Affiliate with respect to any award, judgment, or court order pertaining to the relevant order or orders or under the relevant order or orders, and with respect to any claim pertaining to the relevant order or orders;

iii. the undertaking also includes an indemnity against any claims brought against the Republic of India or any India affiliate contrary to the release; and

iv. the interested party confirms it will treat any such award, judgment, or court order as null and void and without legal effect to the same extent as if it had been set aside by a competent court and will not take any action or initiate any proceeding or bring any claim based on that.

(l) The interested party confirms that the undertakings given herein are intended to be enforceable by the Republic of India, including so as to secure the irrevocable waiver, withdrawal or discontinuance (as appropriate) of all the proceeding and claims referred to in any of the clauses of this undertaking.

(m) The interested party represents and warrants that:

i. it has full legal power and authority to execute and deliver this undertaking (including but not limited to the issuance of the indemnity described in clauses (i) and (j) under applicable law;

ii. the execution, delivery and performance of this undertaking (including but not limited to the issuance of the indemnity described in clauses (i) and (j) has been duly authorised by all necessary corporate action, including but not limited to any board resolution or similar authorisation under applicable law (see Note 3);

iii. this undertaking constitutes the legal, valid and binding obligation of the interested party, enforceable against the interested party in accordance with its terms;

iv. such authorisations described in the above sub-clauses (i), (ii) and (iii) are effective under applicable law, and to this end, letters from local counsel in the relevant jurisdictions are attached to this undertaking which confirm the legality of such authorisations under applicable law; and

(n) This undertaking is governed by relevant Indian law and any dispute with respect to this undertaking shall be subject to Indian laws and be decided in accordance with the procedures specified in the Act under the exclusive jurisdiction of the relevant Income-tax authorities, tribunals or courts in India, as the case may be, which are empowered to decide disputes under the Act.

I also confirm that, I am aware of all the consequences and implications of this undertaking.

Place: ……………….. .

Date: ……………………….. .

Signature………………………………………….

Attachments

1. The Board Resolution and legal authorisation, as referred to in clause (m) of Part M.

2. An indemnity bond to the effect of clauses (i) and (j) of Part M in Part N of the undertaking in Form No. 1;

3. Copy of the public notice referred to in clause (k) of Part M, where Form No. 3 is not required to be furnished under sub-rule (6) of rule 11UF.

4. Attachments as required in different parts of the Annexure to Part M of this undertaking

Notes:

1. This information is required to be furnished where the Permanent Account Number or Aadhaar Number of the signatory is available.

2. Company Identification Number and Taxpayer Identification Number are to be provided where Permanent Account Number/Aadhaar Number or Tax Deduction Account Number of the interested party are not available.

3. The Board Resolution or legal authorisation, as referred to in clause (m) of the undertaking shall, among other things:

a. record the Signatory’s power and authority to give the undertaking on behalf of the interested party; and

b. record the interested party’s power and authority to indemnify defend and hold harmless the Republic of India and the Indian affiliates in accordance with clause (i) of the undertaking.

VERIFICATION

Verified that the contents of this undertaking are true to the best of my knowledge and belief. No part of the undertaking is false and nothing has been concealed or misstated therein.

Verified at ___________place_________ on this the ___day ____of ___month ______ ,_year ________ .

Place: ……………..

Date: ……………….

Signature…………….

Annexure

Part MA– Particulars of the relevant order or orders:

| Sl. No. |

Assessment Year or Financial year | Income-tax Authority passing the order |

Details of the order under consideration | Nature of interest of the interested party | |