Renting residential properties for corporate guest houses, director accommodations, or employee relocation is a standard practice across corporate India. However, managing the tax compliance surrounding these transactions often leaves corporate finance teams scratching their heads. Specifically, determining the exact Tax Deduction at Source (TDS) rate causes significant confusion. Should your business deduct tax at 2% or 10%?

Getting the TDS on residential rent paid by companies wrong can result in costly interest penalties, disallowance of business expenses, and compliance notices from the Income Tax Department.

Under Section 194-I of the Income Tax Act, rent payments are subject to varying slabs depending on what exactly is being leased. In this comprehensive guide, we will break down the crucial difference between 2% and 10% TDS on rent, clarify when each rate applies to corporate entities, and help you keep your company’s financial records perfectly compliant for the current financial year.

The Core Framework: Section 194-I and Corporate Rent Payments

For any corporate entity in India, making a rental payment to a resident individual or business triggers mandatory tax compliance under Section 194-I. Unlike individual tenants who operate under different thresholds and rules, companies must follow strict corporate rules.

The Basic Rule: Every corporate entity paying rent to a resident person is required to deduct tax at source if the total rental amount paid or payable during the financial year exceeds ₹6,00,000 (Rupees Six Lakhs) per landlord.

This threshold applies per landlord, meaning if a company rents three different apartments from three different owners for ₹1,00,000 each per annum, Section 194-I is not triggered because no single landlord receives more than ₹6.0 lakhs. However, if the threshold is crossed, the company must identify the correct asset classification to apply either the 2% or 10% tax rate.

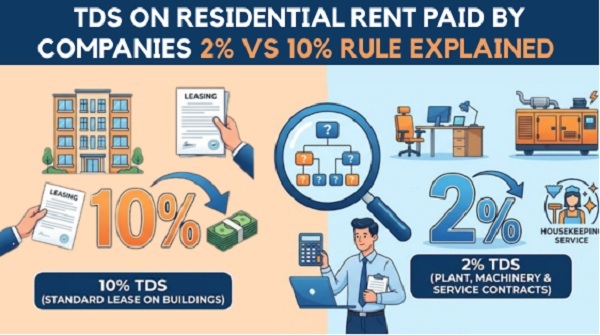

The 10% Rule Explained: Pure Rental of Land and Buildings

When a corporate entity leases a residential apartment, flat, or bungalow purely for accommodation purposes, the transaction falls under the legal definition of renting a “building”.

According to Section 194-I(b) of the Income Tax Act, the mandatory Section 194I TDS rate for the use of any land, building (including factory buildings), furniture, or fittings is fixed at 10%.

Common Corporate Scenarios Attracting 10% TDS:

- Employee Accommodation: A company rents a residential flat directly from a landlord to provide rent-free accommodation to its Managing Director or senior executives.

- Corporate Guest Houses: A business leases an entire residential property to maintain it as a corporate guest house for visiting clients or employees.

- Long-Term Lease Contracts: Regular monthly rental payouts for physical office buildings or residential spaces used for residential-cum-commercial purposes.

If your agreement is a simple, straightforward lease for the physical property, your finance team must deduct a flat 10% from the monthly or advance rent payment before transferring the balance to the landlord.

The 2% Angle: Plant, Machinery, or Service Agreements

If the baseline rate for buildings is 10%, where does the 2% rate come from? The confusion around TDS on residential rent paid by companies usually stems from two distinct legal provisions within tax regulations:

1. Section 194-I(a) – Renting of Plant, Machinery, or Equipment (New Section 393(1) of Income Tax Act, 2025)

The Income Tax Act specifies that if a company pays rent for the use of any plant, machinery, or equipment, the Section 194I TDS rate drops to 2%. In a residential context, this becomes relevant when dealing with a composite lease agreement.

If a company rents a luxury serviced apartment and the lease explicitly breaks down the cost structure—allocating specific sums for the bare building and a separate amount for the high-end machinery, backup generators, central air conditioning plants, or security equipment—the equipment portion attracts only 2% TDS, while the building portion attracts 10%.

2. The Service Contract Loophole (Section 194C) (New Section 393(1) of Income Tax Act, 2025)

Many companies utilize modern co-living spaces or service apartments where the contract isn’t a pure lease of property. Instead, it is a composite agreement for stay, maintenance, catering, and housekeeping.

If the agreement is legally drafted as a contract for providing services rather than a tenancy agreement for a building, it may fall under Section 194C (Contracts). The TDS rate for corporate payments under Section 194C is 2%.

Critical Compliance Steps for Corporate Tenants

Applying the correct rate for TDS on rent paid by corporate entities is only half the battle. Your finance team must follow a systematic workflow on the TRACES portal to ensure complete compliance:

- Verify the Landlord’s PAN: Always collect a valid PAN card from the landlord before processing the first payment. If the landlord fails to provide a PAN, the TDS rate automatically jumps to a punishing 20%, regardless of whether the 2% or 10% rule originally applied.

- Observe the Timeline: The tax deducted during the month must be deposited with the Central Government by the 7th day of the following month (except for March deductions, which can be deposited up to April 30th).

- File Quarterly Returns: Companies must report these deductions by filing Form 26Q every quarter. Failure to file or late filing attracts a fee of ₹200 per day under Section 234E.

- Issue Form 16A: After filing your quarterly returns, download the TDS certificates (Form 16A) from the official TRACES portal and provide them to your landlord so they can claim credit in their income tax returns.