The Chartered Accountants Association, Surat (CAAS), submitted a representation to the Chief Electrical Inspector and Collector of Electricity Duty, Gujarat, objecting to the insistence on Chartered Accountant certificates being issued strictly in departmental formats for Electricity Duty Exemption claims. CAAS contended that while authorities are entitled to prescribe the information required for processing applications, they cannot compel Chartered Accountants to omit professional disclosures mandated by the Institute of Chartered Accountants of India (ICAI). The representation emphasized that ICAI’s Guidance Note on Reports or Certificates for Special Purposes (Revised 2016) requires practitioners to disclose the basis of certification, scope of work, records examined, limitations, responsibilities, and restrictions on use. According to CAAS, rejection of certificates solely because they contain such safeguards prioritizes form over substance, creates ethical dilemmas for professionals, delays applicants’ claims, and undermines compliance with professional standards. The Association sought immediate clarification permitting ICAI-compliant certificates that contain all information required by the Department.

Chartered Accountants Association, Surat

Ref: CAAS/Representations/2026-27/02 Dated: Date: 07-06-2026

To,

The Chief Electrical Inspector & Collector of Electricity Duty,

Office of the Chief Electrical Inspector,

Block No. 18, 6th Floor, Udyog Bhavan,

Sector 11, Gandhinagar, Gujarat – 382011.

Email: [email protected]

Copy by email: [email protected]

Subject: Objection to insistence upon rigid “prescribed format” CA certificates for Electricity Duty Exemption matters — demand to immediately permit ICAI-compliant certificates with essential safeguards

Respected Sir,

We write this representation on behalf of the Chartered Accountants Association, Surat (CAAS) regarding the continuing insistence by your office and/or the online processing mechanism on submission of Chartered Accountant certificates strictly in a prescribed format, even where the certificate submitted by the applicant contains all relevant information required for processing claims under Electricity Duty Exemption and related incentive schemes, along with additional professional disclosures mandated by the Institute of Chartered Accountants of India (ICA!).

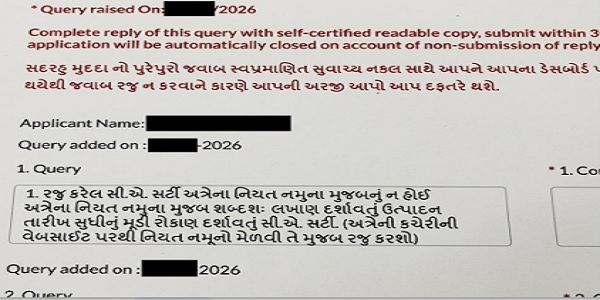

CAAS has recently come across documentary evidence indicating that an applicant seeking benefits under the Electricity Duty framework was issued a query requiring submission of a Chartered Accountant’s certificate strictly in the prescribed format and objecting to the certificate already furnished on the ground that it was not in the prescribed format. The query specifically required the applicant to submit a certificate in the prescribed format showing capital investment up to the date of commencement of production and indicated that the prescribed format available through the Department must be followed.

A redacted copy of the relevant query is enclosed for ready reference as per Para 2. The identity of the applicant has been removed as the issue raised herein is not applicant-specific but concerns a larger systemic practice affecting Chartered Accountants and applicants seeking Electricity Duty Exemption and related benefits across the State.

The contents of the query provide direct evidence that certificates are being scrutinized not merely for the information contained therein, but also for conformity with a rigid departmental format. This raises serious concerns because such insistence conflicts with the professional obligations imposed upon Chartered Accountants under the framework prescribed by the Institute of Chartered Accountants of India (ICAI).

1. The Department may prescribe information requirements, but cannot compel professional non-compliance

CAAS fully recognizes and respects the statutory and administrative authority of your office to call for, verify, and evaluate information that is relevant for determining eligibility under Electricity Duty Exemption schemes and other benefits administered by the Department. We appreciate that the Department must ensure that fiscal incentives and exemptions are granted only to eligible industrial units and that it is therefore entitled to seek details relating to capital investment, commencement of commercial production, installed capacity, expansion projects, machinery acquisition, electricity consumption, and any other factual matter necessary for proper scrutiny of an application.

We also acknowledge that, for the sake of administrative efficiency and uniformity, government departments often prescribe formats, checklists, annexures, and data tables to ensure that applications are processed in a consistent manner. CAAS has no objection whatsoever to the Department specifying the information that must be furnished by applicants or certified by professionals. Indeed, a clearly defined information requirement helps both applicants and certifying professionals understand the expectations of the authority and facilitates timely processing of Electricity Duty Exemption and related claims.

However, there is a critical distinction between:

1. prescribing the information required by the Department, and

2. prescribing or enforcing a reporting format that prevents a Chartered

Accountant from complying with ICAI-mandated professional requirements.

The former is entirely legitimate. The latter is not.

This distinction is not merely technical or semantic. It goes to the very heart of professional accountability and regulatory compliance. A government authority is fully entitled to specify what information it requires for decision-making purposes. However, the manner in which a Chartered Accountant expresses professional conclusions, qualifications, limitations, responsibilities, and the basis of certification is governed by the professional framework established by the Institute of Chartered Accountants of India (ICAI), which is the statutory regulator of the profession under the Chartered Accountants Act, 1949.

A Chartered Accountant’s certificate submitted in support of an Electricity Duty Exemption or subsidy claim is not a clerical formality or a mechanical endorsement. It is a professional document carrying legal, ethical, disciplinary, and reputational consequences. The issuance of such a certificate requires the practitioner to exercise professional judgment, perform appropriate verification procedures, evaluate the sufficiency of available records, and communicate the outcome in a manner that is fair, transparent, and consistent with applicable professional standards.

Accordingly, such a certificate must disclose, wherever applicable:

- the basis of certification;

- records and documents examined;

- scope of verification;

- limitations of procedures performed;

- management responsibilities;

- practitioner responsibilities;

- criteria applied; and

- restrictions on use.

These disclosures serve an important purpose. They inform the user of the certificate about the extent of work performed, the nature of reliance placed on records and representations, the boundaries of the practitioner’s responsibility, and the context in which the certificate should be interpreted. Without such disclosures, there is a risk that the certificate may be misunderstood as providing a level of assurance that was neither intended nor professionally permissible.

These are not optional additions inserted at the discretion of the practitioner. They are integral components of responsible professional reporting and are rooted in the guidance, ethical requirements, and assurance principles prescribed by ICA!. Their inclusion protects not only the Chartered Accountant but also the Department, the applicant, and any other stakeholder who may rely upon the certificate while evaluating eligibility for Electricity Duty Exemption or related incentives.

When a certificate is objected to merely because it contains such professional safeguards and therefore does not mirror a bare departmental format, the issue ceases to be procedural and becomes one of professional compliance. In such circumstances, the objection is no longer directed at the information furnished to the Department; rather, it effectively penalizes the Chartered Accountant for adhering to professional requirements. This creates an untenable situation in which a practitioner is expected to choose between satisfying a departmental preference for a simplified format and complying with the standards and ethical obligations imposed by the profession’s statutory regulator.

It is precisely this conflict that CAAS seeks to address. The Department’s legitimate requirement for information can and should coexist with the Chartered Accountant’s obligation to issue a professionally compliant certificate. There is no inconsistency between the two. The Department may prescribe the information that must be certified for Electricity Duty Exemption purposes, but the professional must remain free to include the disclosures, qualifications, explanations, and safeguards necessary to ensure that the certificate complies with ICAI requirements and accurately reflects the nature and extent of the work performed.

2. ICAI’s Guidance Note governs CA certificates — not departmental convenience

The issuance of certificates by Chartered Accountants is governed by ICAI’s Guidance Note on Reports or Certificates for Special Purposes (Revised 2016), issued by the Institute of Chartered Accountants of India under the framework of the Chartered Accountants Act, 1949. The procedures, disclosures, and safeguards prescribed therein are not optional drafting preferences but form part of the professional standards and ethical obligations that govern Chartered Accountants while issuing certificates, including certificates submitted for Electricity Duty Exemption and subsidy claims.

The Guidance Note requires that certificates issued by Chartered Accountants appropriately address matters such as:

- title and addressee;

- identification of subject matter;

- applicable criteria;

- scope of work performed;

- responsibilities of management and practitioner;

- inherent limitations;

- restriction on use;

- compliance with professional requirements; and

- appropriately worded conclusion.

These requirements are intended to ensure transparency, accountability, clarity regarding the nature of work performed, and proper understanding by the user of the certificate regarding the extent and limitations of the certification. They protect not only the Chartered Accountant but also the applicant, the Department, and all other stakeholders who may rely upon the certificate while determining eligibility under Electricity Duty Exemption schemes.

A certificate that omits such disclosures may create ambiguity regarding the basis of certification, the procedures performed, the extent of verification undertaken, and the level of assurance intended to be conveyed. Such omissions can expose both the user and the issuer to misunderstanding and may result in inappropriate reliance being placed upon the certificate.

More importantly, a Chartered Accountant who disregards the requirements of the Guidance Note and issues certificates without following the prescribed professional procedures may expose himself or herself to disciplinary consequences under the Chartered Accountants Act, 1949. Failure to exercise due diligence, failure to comply with accepted professional standards, or issuance of certificates without incorporating essential professional safeguards may, depending upon the facts and circumstances, amount to professional misconduct. Accordingly, compliance with the Guidance Note is not merely advisable—it is a mandatory professional obligation.

In these circumstances, it cannot be the intention of any Government Department or statutory authority to compel a regulated professional to act in a manner that may place him or her in breach of professional standards or expose the professional to disciplinary proceedings. While the Department is fully entitled to prescribe the information required for processing Electricity Duty Exemption applications, it should not insist upon a format that effectively requires omission of disclosures and safeguards mandated by the Chartered Accountant’s professional regulator.

Accordingly, a Chartered Accountant cannot be expected to abandon professional safeguards merely because a departmental format does not expressly provide space for them. On the contrary, permitting such safeguards strengthens the reliability, transparency, and defensibility of the certification process and serves the interests of both the Department and the public at large.

3. Documentary evidence indicates rigidity in acceptance of certificates

The above redacted screenshot demonstrates that the concern raised by CAAS is not hypothetical. The query raised is as follows:

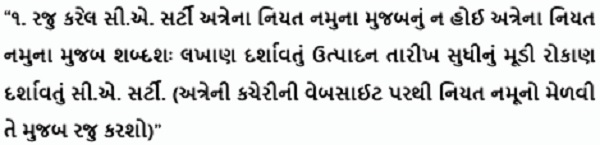

This literally translates to:

“Since the submitted C.A. Certificate is not as per the prescribed format of this office, submit a C.A. Certificate showing the capital investment up to the date of production, containing the exact word-for-word text as per the prescribed format of this office. (Kindly obtain the prescribed format from this office’s website and submit accordingly)”

While the screenshot pertains to a particular applicant and has been enclosed only as an illustrative example, it is important to clarify that this is not an isolated incident. CAAS has observed a recurring pattern across numerous applications processed under Electricity Duty Exemption related industrial incentive schemes, where applicants are asked to resubmit Chartered Accountant certificates solely because they do not conform to a rigid prescribed format, notwithstanding that the certificates contain the relevant information required by the Department.

The query reflected in the enclosed screenshot does not appear to challenge the correctness of the figures certified, nor does it identify any factual deficiency, inconsistency, or inadequacy in the information furnished. Instead, the objection is directed toward the format of the certificate itself and requires submission of a certificate in the prescribed format. This distinction is important.

If the Department requires additional information, clarification, supporting documents, reconciliation statements, or further verification of facts relevant to an Electricity Duty Exemption claim, such requests are understandable and fall within its legitimate administrative powers. CAAS fully supports the right of the Department to seek any information necessary for proper scrutiny of claims and protection of public revenue.

However, where the objection is solely that the certificate is not in the prescribed format despite containing the required information, it reflects a rigid and mechanical approach that prioritizes form over substance. Such insistence effectively discourages Chartered Accountants from incorporating professional safeguards mandated by ICAI, including disclosures relating to scope of work, basis of certification, reliance on records and representations, limitations of verification, and restriction on use.

The concern therefore extends beyond the individual case reflected in the enclosed screenshot. The screenshot merely evidences a broader administrative practice that appears to be prevalent in many cases brought to the attention of CAAS. The repeated insistence on strict adherence to departmental formats, without accommodating essential professional reporting requirements, creates systemic difficulties for Chartered Accountants and applicants alike and increases the risk of non-compliant certifications being issued under procedural pressure.

4. A State authority cannot override standards prescribed by a statutory regulator

ICAI is a statutory body established under the Chartered Accountants Act, 1949, enacted by Parliament to regulate the profession of Chartered Accountancy in India. The Institute is entrusted with the responsibility of maintaining professional standards, prescribing ethical requirements, regulating the conduct of its members, and safeguarding public confidence in professional certifications and attest functions performed by Chartered Accountants.

Its ethical framework, guidance notes, standards, and professional pronouncements govern the conduct of Chartered Accountants throughout India. These requirements are not merely advisory in nature, nor are they optional recommendations that may be disregarded whenever a client, consultant, or government authority prefers a different approach. They form an integral part of the professional obligations applicable to every member of the Institute and are intended to ensure consistency, transparency, accountability, and reliability in professional reporting.

When a Chartered Accountant issues a certificate in support of an Electricity Duty Exemption claim, he or she is required to comply with the applicable professional framework prescribed by ICA!. Such compliance includes, among other things, clearly identifying the subject matter being certified, describing the basis of certification, specifying the records and information examined, disclosing any limitations or assumptions, defining the scope of work performed, and ensuring that the certificate is not capable of being misunderstood or relied upon beyond its intended purpose.

Accordingly, professional requirements cannot be displaced, diluted, or overridden by:

- departmental formats;

- portal-generated instructions;

- administrative checklists;

- internal processing practices;

- informal expectations communicated during scrutiny; or

- any procedural requirement framed solely for administrative convenience. While administrative authorities are fully entitled to prescribe the information, particulars, data points, and supporting documents necessary for processing Electricity Duty Exemption applications, such authority does not extend to directing a Chartered Accountant to omit professional disclosures or abandon safeguards mandated by ICA!.

Put simply:

The Department may prescribe what information is required for Electricity Duty Exemption purposes. It cannot prescribe professional non-compliance as the price of acceptance.

5. Addition of professional safeguards does not dilute the certificate

CAAS respectfully submits that incorporating appropriate professional disclosures enhances the reliability, transparency, and credibility of a certificate rather than diminishing its value.

For instance, when a Chartered Accountant specifies:

- the documents and records reviewed;

- the nature and extent of verification carried out;

- reliance placed on books of account and management representations;

- limitations inherent in the procedures performed;

- restrictions on the use of the certificate; and

- the specific purpose for which the certificate is issued,

such disclosures do not affect, alter, or modify the certified figures in any manner. They merely explain the basis on which the certification has been issued and the scope within which it should be interpreted.

The amount of capital investment remains unchanged.

The date of commencement of commercial production remains unchanged.

The underlying factual particulars remain unchanged.

The Department’s authority to examine and determine eligibility for Electricity Duty

Exemption remains unchanged.

The only result is that the certificate is supported by appropriate professional safeguards, provides greater clarity regarding the work performed by the Chartered Accountant, and is better equipped to withstand legal, regulatory, and disciplinary scrutiny.

Permitting such disclosures causes no disadvantage to the Department. On the contrary, they promote transparency, reduce the possibility of misunderstanding, eliminate uncertainty regarding the scope of certification, and clearly define the extent to which the certificate may be relied upon.

6. Existing practice is creating unnecessary conflict

The insistence upon strict adherence to a departmental format is creating avoidable difficulties for applicants and professionals alike.

In practice, applicants seeking Electricity Duty Exemption or related benefits are often informed that unless the certificate is furnished exactly in the prescribed format, the application may be queried, delayed, returned for clarification, or kept pending until a revised certificate is submitted. Even where the certificate contains all the information required by the Department, objections are sometimes raised merely because the Chartered Accountant has included additional paragraphs relating to scope of verification, reliance on records, management responsibility, limitations of the certification, or restriction on use.

This creates a practical problem for applicants. They may have already invested substantial time and resources in preparing their application and obtaining professional certification. When a certificate is rejected solely because it contains professionally required disclosures, the applicant is forced to approach the Chartered Accountant again, seek revisions, and resubmit documents, resulting in unnecessary delay and uncertainty in obtaining Electricity Duty benefits.

At the same time, this situation places pressure on Chartered Accountants to remove professional safeguards and issue certificates in a form that may not fully comply with ICAI guidance.

As a result:

- applicants face delays and repeated compliance requirements;

- professionals face ethical and regulatory dilemmas;

- consultants and practitioners encounter unnecessary disputes regarding the acceptable form of certification;

- departmental officers are required to raise and process avoidable queries despite having received the relevant information; and

- administrative resources are consumed in correspondence and resubmissions that do not materially assist the verification process.

The difficulty is not that the Department seeks information; rather, it arises when the format is treated as mandatory to the exclusion of professionally necessary disclosures. If the required information is available and properly certified, the addition of !CAI-compliant safeguard paragraphs should not become a ground for objection.

No applicant should be compelled to choose between timely processing of an Electricity Duty Exemption claim and professional compliance. No Chartered Accountant should be compelled to choose between satisfying a departmental format and complying with professional standards.

7. Demand for immediate corrective clarification

In light of the above, CAAS demands your office to issue a clarification stating that:

1. Chartered Accountants may submit certificates in ICAI-compliant formats even where the Department has prescribed a specimen format or data table;

2. certificates shall not be rejected merely because they contain professional disclosures relating to scope, limitations, responsibilities, basis of verification, or restriction on use;

3. the prescribed format shall be treated as specifying the information required by the Department and not as prohibiting additional professional disclosures;

4. officers and portal administrators shall not raise objections solely because a certificate contains additional ICAI-compliant reporting elements;

5. where necessary, the prescribed information may be incorporated within or annexed to a detailed professional certificate; and

6. pending Electricity Duty Exemption applications shall not be delayed merely because the certificate is not confined to the exact wording of the departmental format, provided the required information has been duly certified.

8. Volunteering for consultation and development of a compliant format

CAAS remains willing to assist your office in developing a standard format that

simultaneously satisfies:

- the Department’s information requirements for Electricity Duty Exemption and related schemes;

- administrative processing needs; and

- ICAI’s professional reporting requirements.

Such a collaborative approach would eliminate recurring disputes and provide clarity to applicants, officers, and professionals alike. Until such a format is finalized, certificates containing the required departmental information together with ICAI-mandated safeguards should be accepted without objection.

9. Escalation to Ethical Standards Board of ICAI

A copy of this representation is being forwarded to the Chairperson, Ethical Standards Board of ICAI for consideration and appropriate guidance.

CAAS has already brought to the attention of members of the ICAI leadership the increasing number of situations across various government departments, authorities, boards, corporations, and regulatory agencies where Chartered Accountants are required to issue certificates in rigid prescribed formats that do not adequately accommodate professional reporting requirements mandated by ICAI.

Such conflicts create uncertainty not only for professionals but also for applicants, government authorities, and users of the certificates. They expose practitioners to potential disciplinary risks, create avoidable disputes during processing of Electricity Duty Exemption applications, and undermine the consistency and reliability of professional certifications. In these circumstances, institutional intervention may become necessary if professionals continue to face pressure—whether direct or indirect—to issue certificates that compromise accepted standards of reporting or omit disclosures considered essential under ICAI guidance.

The purpose of this representation is not to challenge the authority of your office or dilute any eligibility requirement, but to demand that Chartered Accountants be permitted to issue !CAI-compliant certificates containing the disclosures and safeguards mandated by their professional regulator. A timely action on above demands shall be highly appreciated.

Regards,

For Chartered Accountants Association, Surat.

Enclosure: Extracts from /G4/ Guidance Note on Reports or Certificates for Special Purposes (Revised 2016) to be downloaded from https://resource.cdnicai.org/43452aasb-an-rcsp.pdf

Copy To

1. Honible Chief Minister of Gujarat

Chief Minister’s Office, 3rd Floor, Swarnim Sankul-1, New Sachivalaya, Sector 10, Gandhinagar,

Gujarat – 382010. (Email: [email protected])

2. Principal Secretary (Energy & Petrochemicals Department)

Government of Gujarat, Block No. 5, 5th Floor, New Sachivalaya, Sector 10, Gandhinagar,

Gujarat – 382010. (Email: [email protected])

3. Joint Secretary (NCE, Budget) (Energy & Petrochemicals Department)

Government of Gujarat, Block No. 5, 5th Floor, New Sachivalaya, Sector 10, Gandhinagar,

Gujarat – 382010. (Email: [email protected])

4. The Chairperson (Ethical Standards Board)

The Institute of Chartered Accountants of India (ICAI), ICAI Bhawan, A-29, Sector 62, Noida,

Uttar Pradesh – 201309. (Email: [email protected])

5. The President (The Institute of Chartered Accountants of India)

ICAI Bhawan, Indraprastha Marg, New Delhi – 110002. (Email: [email protected])