This article analyzes the Supreme Court’s ruling in Skyline Construction (2025 INSC 1234), [Civil Appeal No. 8318 of 2011, decided on 1 November 2025] which bars double taxation on subcontractor payments under the KVAT composition scheme. It explores the doctrinal principles involved and evaluates their relevance under the GST regime, supported by AAR/AAAR decisions and comparative statutory analysis.

Introduction

In a pivotal ruling, the Supreme Court of India in Authority for Clarification and Advance Rulings, Karnataka v. Skyline Construction and Housing Pvt. Ltd. (2025 INSC 1234) clarified that under the Karnataka Value Added Tax Act, 2003 (KVAT Act), principal contractors executing works contracts under the composition scheme are not liable to pay tax on amounts paid to registered subcontractors who have discharged their own tax liability. This judgment, though rendered under the erstwhile VAT regime, carries significant doctrinal weight and interpretive relevance under the Goods and Services Tax (GST) framework introduced in 2017.

This article analyzes the Supreme Court’s reasoning, the statutory architecture of works contracts under GST, and whether the principle of avoiding double taxation on subcontractor payments applies in the GST era.

Recap of the Supreme Court’s Ruling under KVAT

Background

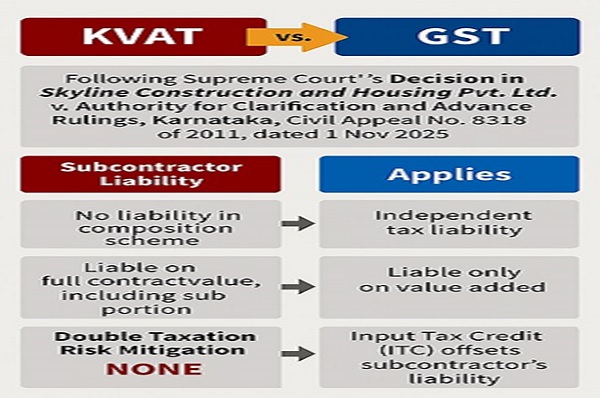

Skyline Construction, a registered dealer under KVAT, executed works contracts partly through subcontractors. It opted for the composition scheme under Section 15 of the KVAT Act and sought an advance ruling on whether payments to subcontractors should be included in its taxable turnover. The Authority denied the deduction, citing absence of express provision prior to 1 March 2006.

The Karnataka High Court reversed this view, and the Supreme Court upheld the High Court’s decision, holding that:

- The principal contractor’s taxable turnover under composition does not include payments made to registered subcontractors who have paid VAT.

- Including such payments would result in double taxation, violating constitutional principles.

Core Doctrines Affirmed by the Supreme Court

1. Accretion Principle: Property in goods used in works contracts passes to the contractee through incorporation, not sale. Thus, the subcontractor is the deemed seller to the contractee.

2. Single Point Taxation: Tax must be levied only once on the value addition. Taxing both the subcontractor and principal contractor on the same value is impermissible.

3. Purposive Interpretation: Fiscal statutes must be interpreted to avoid absurdity and uphold constitutional values.

4. Constitutional Safeguards: Double taxation violates Articles 14 (equality), 19(1)(g) (freedom of trade), and 265 (no tax without authority of law).

Transition to GST: Structural Changes and Continuities

The GST regime, introduced via the Constitution (101st Amendment) Act, 2016 and governed by the Central Goods and Services Tax Act, 2017 (CGST Act), subsumed VAT, service tax, and other indirect taxes. Works contracts are now treated as a supply of service under Schedule II of the CGST Act.

Key GST Provisions Relevant to Works Contracts

| Provision | Description |

| Section 2(119) | Defines “works contract” as a contract for building, construction, etc., involving transfer of property in goods as part of service. |

| Section 7 | Defines “supply” to include all forms of supply of goods or services. |

| Schedule II | Declares works contracts as supply of service. |

| Section 9 | Levy of GST on intra-State supplies. |

| Section 10 | Composition scheme for small taxpayers (not applicable to works contracts). |

| Section 16–17 | Input tax credit provisions. |

| Section 31 | Tax invoice requirements. |

Does the Supreme Court’s Principle Apply to GST?

Yes, But with Structural Adaptation

While GST treats works contracts as services and does not offer a composition scheme for works contractors (except under specific conditions for small suppliers), the principle of avoiding double taxation on subcontractor payments remains doctrinally valid.

Key Considerations:

1. Separate Supplies Recognized

Under GST, both principal contractor and subcontractor are treated as distinct suppliers. Each must raise tax invoices and discharge GST on their respective value of supply. The subcontractor’s supply to the principal contractor is taxable, and the principal contractor’s onward supply to the contractee is also taxable—but only on the value added.

2. Input Tax Credit (ITC) Mechanism

Unlike KVAT composition, GST allows ITC. The principal contractor can claim credit for GST paid to the subcontractor, thereby avoiding cascading tax. This achieves the same economic result as the KVAT deduction, but through credit rather than exclusion.

3. No Double Taxation in Practice

GST’s invoice-credit chain ensures that tax is levied only once on each leg of the supply. The subcontractor pays GST on their supply; the principal contractor pays GST on their margin. The contractee bears the final tax burden. Thus, the Supreme Court’s concern about double taxation is addressed structurally under GST.

4. Judicial Endorsement of Economic Substance

The Supreme Court’s emphasis on accretion and economic substance supports the GST model, where tax follows the actual flow of goods and services. Even without a composition scheme, the GST framework respects the separation of supplies and avoids duplication.

Practical Implications under GST

For Principal Contractors

- Must pay GST on their supply to the contractee.

- Can claim ITC on GST paid to subcontractors, subject to compliance.

- Should ensure subcontractors are registered and issue proper tax invoices.

For Subcontractors

- Must register under GST and discharge tax on their supplies.

- Their invoices form the basis for ITC to principal contractors.

For Tax Authorities

- Cannot aggregate subcontractor value into principal contractor’s taxable base.

- Must respect the chain of supply and ITC mechanism.

Comparative Table: KVAT vs GST Treatment of Subcontractor Payments

| Aspect | KVAT (Composition) | GST |

| Tax on subcontractor | Yes, if registered | Yes |

| Tax on principal contractor | On own execution only | On full supply value |

| Deduction of subcontractor value | Allowed (post SC ruling) | Not needed—ITC available |

| Risk of double taxation | High (without deduction) | Low (due to ITC) |

| Composition scheme | Available for works contracts | Not available for works contracts |

GST AAR/AAAR Decisions on Subcontractor Payments: Alignment with Supreme Court Doctrine

Several Advance Ruling (AAR) and Appellate AAR (AAAR) decisions under GST have addressed the treatment of subcontractor payments in works contracts. For instance, in Shreeji Earth Movers [AAAR Gujarat, 2023], the appellate authority held that a sub-subcontractor providing civil construction services is independently liable to pay GST at 12% under Notification No. 11/2017-Central Tax (Rate), Serial 3(ix). Similarly, in M/s T & D Electricals [AAR Rajasthan, 2021], the authority clarified that subcontractors executing works contracts for government entities are liable to pay GST unless exempted under specific notifications. These rulings consistently affirm that each subcontractor is a distinct supplier under GST and must discharge tax on their scope of work.

In light of the Supreme Court’s decision in Skyline Construction, these AAR/AAAR rulings remain doctrinally sound. The Court’s emphasis on avoiding double taxation and recognizing the subcontractor as the actual supplier aligns with GST’s structural design, where tax is levied on each leg of supply and mitigated through input tax credit (ITC). Although the VAT-era composition scheme differs from GST’s regular taxation model, the principle that the principal contractor should not be taxed again on the subcontractor’s value holds good. The GST framework achieves this not by exclusion, but by allowing ITC and treating each supplier independently. Therefore, the Supreme Court’s ruling reinforces the validity of these AAR interpretations and strengthens the constitutional foundation of GST’s supply chain taxation.

Summary Table: GST AAR/AAAR Decisions on Subcontractor Payments

Case Details |

Authority & Order Date |

Key Holding |

GST Treatment |

Alignment with SC Ruling |

Shreeji Earth Movers – Advance Ruling No. GUJ/GAAAR/APPEAL/2023/02 |

Gujarat AAAR, Order dated 29 March 2023<br>Published in Legal TaxGuru (17 Sep 2025) |

Sub-subcontractor liable to pay GST independently on civil construction services |

12% under Notification No. 11/2017-Central Tax (Rate), Serial 3(ix) |

Fully aligned – recognizes separate supply and avoids duplication |

M/s T & D Electricals – Advance Ruling No. RAJ/AAR/2021-22/10 |

Rajasthan AAR, Order dated 15 July 2021 Published in Taxmann GST Cases |

Subcontractor to government entity liable to pay GST unless exempted |

Taxable unless covered by exemption under Notification No. 12/2017 |

Aligned – confirms subcontractor’s independent liability |

M/s Shibaura Machine India Pvt Ltd – Advance Ruling No. 32/ARA/2025 |

Tamil Nadu AAR, Order dated 18 August 2025<Published on GST Council Portal |

ITC admissible on electrical and fire-fighting works during factory expansion |

ITC allowed if capitalized and used for business |

Aligned – supports ITC mechanism to avoid double taxation |

M/s PNC Infratech Ltd – Advance Ruling No. UP/AAR/2020-21/03 |

Uttar Pradesh AAR, Order dated 20 April 2020 Published in GST Law Reports |

Subcontractor liable to pay GST on road construction services to principal contractor |

12% under Notification No. 11/2017 |

Aligned – recognizes distinct taxable supply by subcontractor |

M/s KPC Projects Ltd – Advance Ruling No. AP/AAR/2020 /12 |

Andhra Pradesh AAR, Order dated 10 June 2020< Published in VST (Vol. 70) |

Subcontractor executing works contract for government entity liable to pay GST |

Taxable unless exempted under Notification No. 12/2017 |

Aligned – affirms subcontractor’s independent tax liability |

Clarifying the Landscape: No Direct Contradictions, But Some Gaps

The Supreme Court in Skyline Construction [(2025 INSC 1234, Civil Appeal No. 8318 of 2011, Order dated 1 November 2025)] held that taxing both the principal contractor and subcontractor on the same value under a works contract would amount to double taxation, which is constitutionally impermissible. This principle, though developed under the Karnataka VAT Act, is doctrinally relevant to GST due to its emphasis on economic substance, accretion, and single-point taxation.

Under GST, each supplier in the chain—subcontractor, principal contractor—is taxed independently, and Input Tax Credit (ITC) ensures that tax is not duplicated. Most AAR/AAAR decisions uphold this structure.

Potentially Incomplete or Silent Rulings

Some AARs, while not contradictory, may lack doctrinal clarity:

- M/s T & D Electricals – AAR Rajasthan, Advance Ruling No. RAJ/AAR/2019-20/21 (Order dated 3 October 2019) The ruling affirms that subcontractors are liable to pay GST on works contract services to government entities. However, it does not elaborate on the ITC entitlement of the principal contractor or the risk of cascading tax. Status: Not contradictory, but doctrinally incomplete.

- M/s Shreeji Earth Movers – AAAR Gujarat, Advance Ruling No. GUJ/GAAAR/APPEAL/2023/02 (Order dated 29 March 2023) The AAAR upheld GST liability of a sub-subcontractor at 12% under Notification No. 11/2017. It did not discuss whether the principal contractor could claim ITC or whether the value was taxed again. Status: Aligned in substance, but silent on ITC mechanics.

Why These Are Not Contradictions

- None of these rulings require the principal contractor to pay GST again on the subcontractor’s value without ITC.

- They affirm independent tax liability of each supplier, consistent with GST’s design.

- The absence of doctrinal discussion (e.g., accretion, double taxation) does not amount to contradiction—it reflects limited scope or framing of the questions before the AAR.

Summary: No Contradictions, But Watch for Doctrinal Gaps

| Case Name | Authority & Order Date | Issue | Alignment with SC Ruling |

| M/s T & D Electricals | AAR Rajasthan, 03 Oct 2019 | Subcontractor GST liability to govt entity | Not contradictory, but silent on ITC |

| M/s Shreeji Earth Movers | AAAR Gujarat, 29 Mar 2023 | GST on sub-subcontractor services | Aligned, but no ITC discussion |

Doctrinal Continuity with Caveats: A Refined Perspective

The Supreme Court’s ruling in Skyline Construction establishes a clear constitutional and doctrinal bar against double taxation in works contracts. While GST operates under a structurally different regime, the principle that each supplier is independently liable and that tax must not be duplicated remains intact through the input tax credit (ITC) mechanism.

No AAR, AAAR, or High Court decision under GST has directly contradicted this ruling. However, a few early AARs—such as M/s T & D Electricals, AAR Rajasthan [(Advance Ruling No. RAJ/AAR/2019-20/21, Order dated 3 October 2019)]—have addressed subcontractor liability without explicitly discussing ITC or the risk of cascading tax. These omissions do not amount to contradiction but reflect limited doctrinal engagement.

Thus, the Supreme Court’s ruling in Skyline Construction remains doctrinally unchallenged and jurisprudentially reinforced. It serves as a constitutional compass for interpreting GST provisions on works contracts, especially in preventing tax duplication and ensuring economic substance prevails over form.

As GST jurisprudence evolves, vigilance is warranted to ensure that future rulings—especially those involving layered subcontracting or composite supplies—continue to respect the principles of accretion, single-point taxation, and constitutional fairness.

Author Bio