Family settlements occupy a unique space at the intersection of personal law, property rights, and taxation. Though not codified under the Income-tax Act, 1961, they have been judicially recognized as legitimate instruments for resolving intra-family disputes and realigning ownership without triggering tax liability. This article introduces the foundational concepts, doctrinal scope, and legal character of family settlements, especially under Hindu law, and clarifies that such arrangements are not confined to Hindu Undivided Families (HUFs). It also explores the evolution of judicial interpretation, the role of equity and conscience, and the practical necessity of registration—particularly where immovable property is involved.

This is the first in a series of articles that will examine family settlements under key legal and tax topics. Each instalment will build on statutory analysis, case law synthesis, and professional practice considerations to offer a comprehensive understanding of this important but often misunderstood domain.

Page Contents

- A. Introduction

- B. Meaning and Scope of “Family” under Hindu Law

- C. Historical Evolution of Family Settlements in Indian Law

- D. Judicial Interpretation: Kale v. Deputy Director of Consolidation

- E. Role of Equity and Conscience in Judicial Recognition

- F. Family Settlement Not Confined to HUFs Alone

- CIT v. Ashwani Chopra (2007) 209 CTR 297 (P&H); [2007] Taxmann 456 (P&H)

- Rahisuddin v. Fatima & Others

- Author’s View: Family Settlements Apply Universally — Beyond Hindu Law

- Special Relevance to Mohammedan Families

- Supporting Case Laws for Oral Family Settlements Among Muslims

- Supreme Court of India, 2024 INSC 1006, decided on 19 December 2024

- Legal Basis for Family Settlements Among Christians

- Indian Succession Act, 1925

- Key Judicial Recognition

- Practical Relevance

- G. Nature of Family Settlement: Compromise, Arrangement, or Declaration?

- H. Oral vs Written Settlements: Legal Validity and Registration

- I. Why is registration practically essential, where immovable property is involved?

- J. Oral Settlements: Advisable to Record and Register

- K. Practical Necessity: Visibility in Encumbrance Certificate (EC) What is an EC?

- L. Credibility with Buyers and Lending Banks

- M. Risks of Non-Registration

- N. Drafting Checklist for Practitioners

- O. Common Pitfalls and How Courts Have Addressed Them

- P. Relevance under Income-Tax Law (To Be Covered Separately)

- Q. Conclusion

A. Introduction

In the intersection of personal law and taxation, the concept of a “family settlement” emerges as a pragmatic and legally recognized tool for resolving intra-family disputes and realigning property rights. Though not defined under the Income-tax Act, 1961, family settlements have been judicially upheld as non-transfer arrangements, thereby enjoying tax neutrality under certain conditions. This article explores the meaning, scope, and legal character of family settlements, especially under Hindu law, and examines their relevance under income-tax law. It also clarifies that such settlements are not confined to Hindu Undivided Families (HUFs) alone, but extend to broader familial arrangements.

B. Meaning and Scope of “Family” under Hindu Law

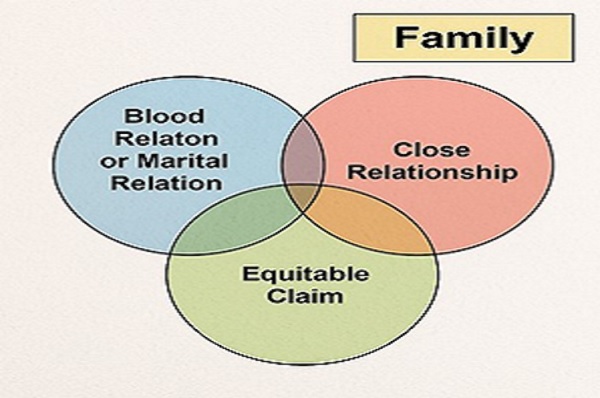

The term “family” in the context of family settlements is interpreted liberally under Hindu law and judicial precedent. It is not restricted to the definition of a Hindu Undivided Family under tax law, nor to coparceners under Hindu succession.

Mulla on Hindu Law

Mulla observes:

“The word ‘family’ in the context of family arrangements is not to be interpreted in a narrow or technical sense. It includes not only persons who have a claim to share in the property but also those who have a possible claim or even a moral claim.”

This includes:

- Coparceners and female members of a joint Hindu family

- Widowed daughters, illegitimate children, and estranged members

- Collaterals and descendants with moral or equitable claims

Raghavachariar’s Hindu Law

Raghavachariar reinforces that the essence of a family settlement lies in mutuality and bona fides, not in the strict enforceability of legal claims. The arrangement may include even those who are not strictly entitled under succession law, provided the objective is to resolve disputes and maintain family peace.

C. Historical Evolution of Family Settlements in Indian Law

Family settlements (also called family arrangements) have evolved from informal, oral understandings within joint families to legally recognized instruments of dispute resolution. In classical Hindu law, Mitakshara and Dayabhaga schools acknowledged intra-family arrangements to preserve harmony and avoid litigation. These arrangements were often undocumented and based on trust.

Post-independence, courts began formalizing the doctrine. In Kale v. Deputy Director of Consolidation, AIR 1976 SC 807; (1976) 105 ITR 134 (SC), the Supreme Court laid down the modern framework, recognizing oral settlements and emphasizing that even moral claims could justify inclusion in a family arrangement.

Over time, the judiciary has expanded the scope to include:

- Non-coparceners and female members

- Collaterals and descendants

- Persons with disputed or moral claims

This evolution reflects a shift from rigid entitlement-based structures to equitable, conscience-driven resolutions.

D. Judicial Interpretation: Kale v. Deputy Director of Consolidation

In the landmark case of Kale & Others v. Deputy Director of Consolidation, AIR 1976 SC 807; (1976) 3 SCC 119; (1976) 105 ITR 134 (SC), the Supreme Court laid down the foundational principles governing family settlements:

“The term ‘family’ for the purpose of a family arrangement is not to be interpreted in a narrow or technical sense. It includes not only persons who have a claim to share in the property but also those who have a possible claim or even a moral claim.”

The judgment emphasized that family arrangements are governed by equity and good conscience, and their validity depends on bona fides, voluntary consent, and absence of fraud. The Court also clarified that such arrangements are not transfers in the legal sense, but rather mutual adjustments of rights.

E. Role of Equity and Conscience in Judicial Recognition

Indian courts have consistently prioritized equity and conscience over technicalities when evaluating family settlements. The doctrine is rooted in the principle that preserving family harmony and avoiding litigation is a legitimate legal objective.

In S. Shanmugam Pillai v. K. Shanmugam Pillai, AIR 1972 SC 2069; (1973) 87 ITR 619 (SC), the Supreme Court held:

“Even if one of the parties to the arrangement has no title, but under the arrangement the other party relinquishes all his claims or titles in favour of such a person and acknowledges him to be the sole owner, then the antecedent title must be assumed and the arrangement will be upheld.”

Similarly, in Roshan Singh v. Zile Singh, AIR 1988 SC 881, the Court emphasized substance over form, validating a family arrangement among collaterals despite procedural irregularities.

These decisions underscore that judicial recognition of family settlements is guided by conscience, fairness, and the intent to resolve disputes, not by rigid statutory definitions.

F. Family Settlement Not Confined to HUFs Alone

A critical doctrinal point is that family settlements are not limited to Hindu Undivided Families (HUFs). Courts have consistently held that the concept of a family arrangement applies to any group of persons connected by blood, marriage, or close relationship, provided the arrangement is genuine and intended to resolve disputes.

CIT v. Ashwani Chopra (2007) 209 CTR 297 (P&H); [2007] Taxmann 456 (P&H)

“A family settlement is not confined to members of a Hindu Undivided Family. It can be entered into by persons who are relatives and have a pre-existing right or even a semblance of a claim in the property. The term ‘family’ must be understood in a broad sense to include persons connected by blood or close relationship.”

This decision affirms that:

- Brothers, sisters, cousins, and female members can be parties to a family settlement.

- Tax neutrality does not depend on HUF status.

- The Income-tax Department cannot narrowly interpret “family” to deny the legitimacy of a genuine arrangement.

Dr. Suraj Munjal v. Mr. Chandan Munjal & Others, (Delhi HC) CS(OS) No. 682/2017, decided on 30 January 2018

In this case, the Court recognized that a family settlement could be valid even among persons who were not part of a Hindu Undivided Family. The dispute involved self-acquired and ancestral properties, and the Court upheld the arrangement based on mutual consent and the intent to resolve disputes. Key takeaway: The existence of a HUF is not a prerequisite for a valid family settlement under general civil law

Rahisuddin v. Fatima & Others

Principal District & Sessions Judge, North-East, Karkardooma Courts, Delhi, Civil Suit No. 1/24 decided on 19 October 2020

- Parties were Muslims. The dispute involved partition and ownership claims over immovable property.

- The Court examined the validity of a family arrangement and emphasized that under Mohammedan law, oral family arrangements are valid if acted upon.

- The Court also considered the Transfer of Property Act and Mohammedan law principles, affirming that family arrangements are enforceable even without formal registration, provided they are genuine and voluntary.

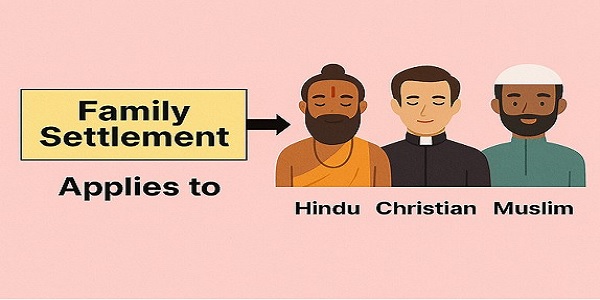

Author’s View: Family Settlements Apply Universally — Beyond Hindu Law

It must be stated in unequivocal terms that the concept of family settlement is not confined to Hindus or Hindu Undivided Families (HUFs). The doctrine of family arrangement is rooted in equity, kinship, and the intent to resolve disputes, and it applies to all families—regardless of caste, religion, or creed.

Courts across jurisdictions have consistently upheld family settlements among Muslims, Christians, Parsis, and other communities, provided the arrangement is genuine, voluntary, and aimed at preserving family harmony. The term “family” in this context is interpreted liberally, encompassing persons connected by blood, marriage, or close relationship.

Special Relevance to Mohammedan Families

In Mohammedan law, the need for family settlements is particularly acute due to several doctrinal constraints:

- Restrictions on gifts: A Muslim cannot make a gift of future property or conditional gifts. Oral gifts require delivery of possession, and written instruments may be challenged if not properly executed.

- Complex inheritance rules: Succession under Muslim law is governed by fixed shares, leaving little room for testamentary discretion. The testator can only bequeath up to one-third of the estate to non-heirs.

- Limitations on wills: Any will that infringes on the Quranic shares is void unless consented to by all heirs after the testator’s death.

These constraints often lead to disputes among heirs, especially in urban families with mixed assets and business interests. In such cases, family settlements serve as a vital tool to:

- Clarify ownership and possession

- Avoid litigation

- Realign rights based on mutual consent

- Preserve family relationships

Courts have recognized that even in Muslim families, oral settlements followed by conduct or memoranda are valid, provided they are not opposed to public policy or used as tax avoidance devices.

Supporting Case Laws for Oral Family Settlements Among Muslims

1. Rafiq v. Razia Sultan

[Delhi District Court, RCA No. 43/11, decided on 26 May 2014]

- The parties were Muslims, and the dispute involved ownership and possession of immovable property.

- The Court upheld the validity of an oral family arrangement, noting that it had been acted upon and was supported by conduct.

- The judge emphasized that registration is not mandatory if the arrangement is oral and does not itself create rights in immovable property.

- Key takeaway: Oral arrangements among Muslim family members are valid if followed by possession and mutual recognition. 🔗 Read full judgment

2. Rahisuddin v. Fatima & Others (supra)

Delhi District Court, Civil Suit No. 1/24, decided on 19 October 2020

- The Court recognized that oral family arrangements among Muslim heirs are valid under Mohammedan law, especially when they are followed by conduct and possession.

- The judgment emphasized that such arrangements are enforceable unless they violate public policy or statutory restrictions.

- Key takeaway: Oral settlements are valid if they reflect genuine intent and are not used to circumvent inheritance laws. 🔗 Read full judgment

3. Mansoor Saheb v. Salima 2024 INSC 1006

Supreme Court of India, 2024 INSC 1006, decided on 19 December 2024

- The Court clarified that under Mohammedan law, a Muslim cannot partition property among heirs during their lifetime, but oral gifts and settlements are valid if accompanied by delivery of possession.

- The judgment reinforced that documentation is advisable, but oral arrangements are not invalid per se.

- Key takeaway: Oral family settlements must comply with hiba (gift) requirements and cannot override fixed shares unless consented to post-death.

Legal Basis for Family Settlements Among Christians

Indian Succession Act, 1925

Christian families are governed by this Act for inheritance and succession. While it prescribes rules for intestate and testamentary succession, it does not prohibit family arrangements. In fact, courts have consistently held that mutual settlements among family members—even outside the statutory framework—are valid if they are:

- Bona fide

- Voluntary

- Intended to resolve disputes

- Not opposed to public policy

Key Judicial Recognition

Pharez John Abraham v. Arul Jothi Sivasubramaniam & Others (2020) 13 SCC 711

Supreme Court of India, decided on 2 July 2019

- The case involved a Christian family dispute over inheritance and the rights of adopted children.

- The Court addressed whether a family settlement without a registered deed could be valid.

- It emphasized that family arrangements are enforceable if they are acted upon and not intended to defeat statutory rights.

- Key takeaway: Even in Christian families, courts recognize oral or informal settlements when they reflect genuine intent and are supported by conduct.

Practical Relevance

Christian families often face:

- Disputes over self-acquired vs ancestral property

- Challenges in testamentary succession

- Multiple heirs with overlapping claims

In such cases, family settlements offer a flexible and equitable solution, especially when:

- Wills are contested

- Property is jointly held

- Heirs wish to avoid litigation

G. Nature of Family Settlement: Compromise, Arrangement, or Declaration?

A family settlement may take various forms:

- Compromise: Resolving an existing dispute (e.g., over succession or partition)

- Arrangement: Preventing future disputes by clarifying rights

- Declaration: Acknowledging existing rights without transferring new ones

The key is that the settlement must be:

- Bona fide

- Voluntary

- Intended to resolve or prevent disputes

It is not a device to transfer property under the guise of a settlement. Courts look at substance over form, and the presence of consideration is not essential.

H. Oral vs Written Settlements: Legal Validity and Registration

Oral Settlements

Oral family settlements are valid under Indian law if they are bona fide, acted upon, and intended to resolve disputes.

Key Case Laws:

- Kale v. Deputy Director of Consolidation, AIR 1976 SC 807; (1976) 105 ITR 134 (SC)

- Shanmugam Pillai v. K. Shanmugam Pillai, AIR 1972 SC 2069; (1973) 87 ITR 619 (SC)

- CIT v. A.L. Ramanathan, (2000) 245 ITR 494 (Mad); (2000) 159 CTR (Mad) 255

Written Settlements: Deed vs Memorandum

1. Family Settlement Deed

A formal written document that creates or extinguishes rights in immovable property must be registered under Section 17(1)(b) of the Registration Act, 1908.

Key Case Laws:

- Thamma Venkata Subbamma v. Thamma Rattamma, AIR 1987 SC 1775

- Roshan Singh v. Zile Singh, AIR 1988 SC 881

- Khushi Ram v. Nawal Singh, SCC OnLine SC 159 (2021)

2. Memorandum of Family Settlement

A memorandum that merely records a past oral settlement does not require registration.

Key Case Laws:

- Kale v. Deputy Director of Consolidation, AIR 1976 SC 807

- Ravinder Kaur Grewal v. Manjit Kaur, MANU/SC/0570/2020

- Darshan Singh v. Mann Singh, RSA-1512-1989 (P&H HC, 2024)

I. Why is registration practically essential, where immovable property is involved?

Statutory Framework: Registration Act, 1908

Under Section 17(1)(b) of the Registration Act, 1908, any document that creates, declares, assigns, limits, or extinguishes rights in immovable property of value exceeding ₹100 must be compulsorily registered. This includes:

- Family settlement deeds

- Partition deeds

- Relinquishment deeds

- Gift deeds

Failure to register such documents renders them inadmissible in evidence under Section 49 of the Act, except for collateral purposes. Thus, even a valid family settlement deed affecting immovable property cannot be relied upon in court unless registered.

Judicial Doctrine: Substance Over Form

The Supreme Court in Thamma Venkata Subbamma v. Thamma Rattamma, AIR 1987 SC 1775, held that:

“Where a document purports to extinguish rights in immovable property, it must be registered. Otherwise, it cannot be used to establish title.”

Even if the parties call it a “memorandum,” courts examine the substance of the document. If it creates or alters rights, registration becomes mandatory.

J. Oral Settlements: Advisable to Record and Register

While oral family settlements are legally valid if bona fide and acted upon, it is strongly advisable to draw up a Memorandum of Family Settlement (MoFS) and get it registered. This serves multiple purposes:

- Provides documentary evidence of the oral arrangement

- Prevents future disputes or repudiation

- Enables legal enforceability and admissibility

- Facilitates mutation and revenue records update

- Ensures visibility in public records

Even if the MoFS merely records a past oral settlement, registration adds credibility and legal weight.

K. Practical Necessity: Visibility in Encumbrance Certificate (EC) What is an EC?

An Encumbrance Certificate is a public record maintained by the Sub-Registrar’s office that reflects all registered transactions affecting a property. It is used to verify:

- Ownership history

- Existing mortgages or liens

- Transfers, gifts, or settlements

Why registration matters

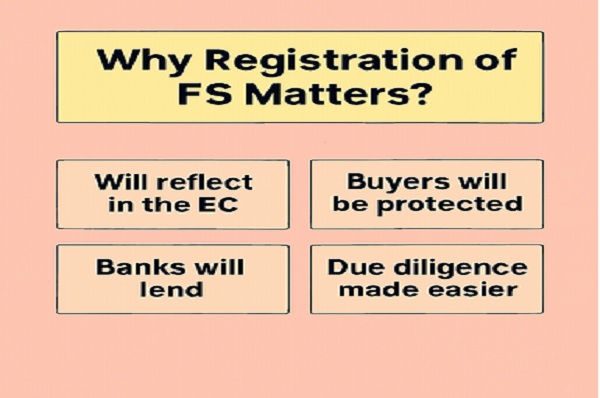

Only registered documents appear in the EC. If a family settlement deed is not registered:

- It will not reflect in the EC

- Prospective buyers will see no record of the arrangement

- Lending institutions will treat the property as legally ambiguous

- Title due diligence will fail

Thus, registration ensures public notice, traceability, and marketable title.

L. Credibility with Buyers and Lending Banks

For Buyers

Buyers rely on registered documents to confirm:

- Clear title

- Absence of disputes

- Validity of ownership claims

An unregistered family settlement—even if legally valid—creates uncertainty. Buyers may demand indemnities or refuse to proceed.

For Banks and Financial Institutions

Banks require:

- Registered title documents

- EC reflecting ownership

- No pending litigation or unregistered claims

Without registration, banks may:

- Refuse to sanction loans

- Demand additional collateral

- Impose higher interest rates due to title risk

Thus, registration instills confidence and facilitates financial transactions.

Recognition under Hindu Succession (Amendment) Act, 2005

The Hindu Succession (Amendment) Act, 2005 granted daughters equal coparcenary rights. Post-amendment:

- Daughters are co-owners by birth

- Any relinquishment or settlement involving their rights must be documented and registered

Courts have held that oral relinquishment by daughters is insufficient. Only registered deeds are recognized for extinguishing their rights.

Key case: Vineeta Sharma v. Rakesh Sharma, (2020) 9 SCC 1 The Supreme Court emphasized that registered documents are essential to prove voluntary relinquishment or settlement of coparcenary rights.

M. Risks of Non-Registration

- Title disputes due to lack of public record

- Inadmissibility in court proceedings

- Rejection by banks and buyers

- Exposure to tax scrutiny if treated as transfer or gift

- Invalidation of relinquishment under HSA post-2005

Summary: Why Registration Is Practically Essential

| Reason | Explanation |

| Legal enforceability | Unregistered deeds are inadmissible in court |

| Visibility in EC | Only registered documents appear in Encumbrance Certificate |

| Credibility | Buyers and banks rely on registered records |

| Compliance with HSA | Post-2005, only registered deeds extinguish daughters’ rights |

| Tax clarity | Registered deeds help establish non-transfer character |

| Protection against future claims | Registration creates public notice and estoppel |

Detailed Discussion: Thamma Venkata Subbamma v. Thamma Rattamma, AIR 1987 SC 1775

In the context of registration discussion on above case law will be apt.

Background

In this case, the dispute arose over a document styled as a “family arrangement” that purported to divide immovable property among family members. The document was not registered, and one party sought to rely on it to assert ownership rights.

The central question before the Supreme Court was:

Does a family arrangement that creates or extinguishes rights in immovable property require registration under Section 17(1)(b) of the Registration Act, 1908?

Supreme Court’s Ruling

The Court held that:

“If the document itself is the source of the title and purports to extinguish or create rights in immovable property, it must be registered. If it is only a record of a past oral arrangement, it may be treated as a memorandum and does not require registration.”

This distinction is doctrinally critical.

- Memorandum of oral settlement → No registration required

- Instrument that creates or alters rights → Registration mandatory

Key Doctrinal Takeaways

- Substance over nomenclature: Merely calling a document a “memorandum” does not exempt it from registration. Courts examine the legal effect of the document.

- Creation or extinguishment of rights: If the document is the source of title, it must be registered.

- Admissibility in evidence: An unregistered document affecting immovable property is inadmissible in court, except for collateral purposes.

Application to Family Settlements

This case is frequently cited in disputes where:

- A family settlement deed is unregistered

- One party claims title based on the deed

- The other party challenges its admissibility

If the deed is unregistered and not merely a record of a past oral arrangement, courts will refuse to admit it in evidence, thereby undermining the entire settlement.

Practical Implications

Title Security

- Without registration, the deed will not appear in the Encumbrance Certificate (EC).

- Buyers and banks will not recognize the arrangement.

- Future disputes may arise from heirs or third parties.

Financial Transactions

- Lending institutions require registered documents for mortgage and loan processing.

- Unregistered deeds create title risk, leading to rejection or higher collateral demands.

Succession and Daughters’ Rights

Post the Hindu Succession (Amendment) Act, 2005, daughters are coparceners by birth. Any relinquishment of their rights must be:

- Voluntary

- Documented

- Registered

Courts have refused to recognize oral relinquishment by daughters unless supported by a registered deed.

Summary: Why Thamma Venkata Subbamma Is Central to Registration Doctrine

| Principle | Explanation |

| Source of title | If the document creates rights, registration is mandatory |

| Memorandum exception | Only records of past oral settlements are exempt |

| Admissibility | Unregistered deeds are inadmissible in court |

| Title clarity | Registration ensures visibility in EC and public records |

| Legal certainty | Protects against future claims and litigation |

N. Drafting Checklist for Practitioners

To ensure legal validity and tax neutrality, practitioners should consider:

- Clearly identify all parties and their relationship

- Describe the nature of claims and disputes resolved

- Specify whether the arrangement is oral, written, or a memorandum

- Attach asset schedules and ownership declarations

- Include disclaimers on tax treatment and non-transfer intent

- Register the document if it creates or extinguishes rights in immovable property

- Ensure signatures and witnesses are properly recorded

- Avoid language that implies sale, gift, or relinquishment for consideration

O. Common Pitfalls and How Courts Have Addressed Them

Failure to register deeds involving immovable property If a family settlement deed creates or extinguishes rights in immovable property, it must be registered under Section 17(1)(b) of the Registration Act, 1908. Courts have invalidated such documents when unregistered, unless they are mere memoranda of past oral arrangements. Key case: Thamma Venkata Subbamma v. Thamma Rattamma, AIR 1987 SC 1775, discussed supra, in detail.

Unequal division challenged as a gift or transfer Where one party receives a disproportionately larger share, the department may argue that the arrangement is a taxable gift or transfer. Courts have upheld such arrangements if they are bona fide and aimed at resolving disputes. Key case: CIT v. Ashwani Chopra, (2007) 209 CTR 297 (P&H)

Lack of documentation for oral settlements While oral settlements are valid, failure to document or act upon them can lead to disputes or denial of tax benefits. Courts require corroborative evidence such as possession, conduct, or subsequent memoranda. Key case: Kale v. Deputy Director of Consolidation, AIR 1976 SC 807

Misuse of family settlement to avoid tax If the arrangement is a façade to transfer assets and avoid tax, courts apply the doctrine of substance over form and may invoke anti-avoidance principles. Key case: McDowell & Co. Ltd. v. CTO, (1985) 154 ITR 148 (SC)

P. Relevance under Income-Tax Law (To Be Covered Separately)

The tax implications of family settlements are doctrinally rich and merit a separate article. Key topics to be addressed include:

- Whether a family settlement constitutes a “transfer” under section 2(47)

- Capital gains implications under section 45

- Taxability under section 56(2) for recipients

- Ownership attribution and clubbing provisions

- Judicial safeguards against tax avoidance (McDowell doctrine)

These will be covered in the next article: “Family Settlement: Not a Transfer Under Income-Tax Law – Doctrinal and Judicial Analysis.”

Q. Conclusion

Family settlements represent a confluence of personal law, equity, and tax jurisprudence. Their recognition by courts as non-transfer arrangements makes them invaluable in succession planning and dispute resolution. Crucially, they are not confined to HUFs, and can be entered into by any group of relatives with a genuine intent to resolve disputes.

Judicial doctrine emphasizes:

- Substance over form

- Equity over entitlement

- Peace over litigation

Practitioners must ensure that settlements are properly documented, registered when required, and structured to reflect genuine intent. With careful drafting and doctrinal awareness, family settlements can serve as powerful instruments of harmony—both legally and fiscally.

It is advisable to get the family settlement registered, from the practical point of view, where immovable property is involved.

Author Bio