GOVERNMENT OF KARNATAKA

DEPARTMENT OF COMMERCIAL TAXES

No. KGST/DC/EG/CR-01/19-20

Office of the Commissioner of

Commercial Taxes (Karnataka),

1st floor, VTK-1, Kalidasa Road,

Gandhinagar, Bengaluru,

Dated: 31.10.2019.

COMMISSIONER OF COMMERCIAL TAXES

CIRCULAR NO: 27/2019-2020

Sub: – User Acceptance Testing of New Returns Offline Tool and online version of Form GST ANX-1 and Form GST ANX-2.

To simplify the process and procedure of filing of return across various categories of taxpayers, the GST Council in its 31st meeting has decided that a New Return System under GST would be introduced for taxpayers. The important salient features of new returns are as under:

a) Form GST RET-1 (Normal Monthly) – Those taxpayers whose aggregate turnover in the preceding financial year was above Rs.5 crores will have to file monthly return in FORM GST RET-1, this needs to be filed based on FORM GST ANX-1 and FORM GST ANX-2.

b) Form GST RET-1 (Normal Quarterly) – Taxpayers whose aggregate turnover in the preceding financial year was up to Rs.5 crores can file this return based on FORM GST ANX-1 and FORM GST ANX-2. This return needs to be filed quarterly. Tax has to be paid on monthly basis through FORM GST PMT-08.

c) FORM GST RET-2 (SAHAJ Quarterly) -Taxpayers whose aggregate turnover in the preceding financial year was up to Rs.5 crores and have supplies only to consumers and unregistered persons (B2C supplies) can file this return based on FORM GST ANX-1 and FORM GST ANX-2 on quarterly basis, but pay tax on monthly basis through FORM GST PMT-08.

Taxpayers opting to file SAHAJ can declare outward supply under B2C category and inward supplies attracting reverse charge only. E-commerce operators are ineligible to file SAHAJ.

d) FORM GST RET-3 (SUGAM Quarterly)- Taxpayers whose aggregate turnover in the preceding financial year was up to Rs.5 crores and have made supplies to consumers and un-registered persons (B2C) and to registered persons (B2B) can file this return based on FORM GST ANX — 1 and FORM GST ANX — 2 on quarterly basis, but pay tax on monthly basis through FORM GST PMT-08.

Taxpayers opting to file SUGAM can declare outward supply under B2C and B2B category and inward supplies attracting reverse charge only. E-commerce operators are ineligible to file SUGAM.

e) All Returns are essentially prepared on the basis of two forms namely GST ANX-1 and GST ANX-2.

2. GST ANX-1 (Annexure of Supplies) is for reporting details of all outward supplies, inward supplies liable to reverse charge, and import of goods and services etc. Invoice-wise details may be furnished (except for B2C supplies) on a real-time basis as and when the invoices are issued by the supplier and the recipient can view them and take action on real time basis. Inward supplies attracting reverse charge will be reported only by the recipient. Option is available to include details omitted in the previous tax period.

a) Edit/Amendment of uploaded documents FORM GST- ANX-1: The amendment of details of earlier tax period can be made in FORM GST ANX-1A before the due date of filing of September return following the end of the financial year or the actual date of furnishing relevant annual return, whichever is earlier.

b) Editing of documents can be done only by supplier. Editing by supplier is allowed only if recipient has not accepted such supply. If already accepted, unless ‘reset/unlock’ by recipient details cannot be edited by supplier.

c) Recipient filing monthly returns can accept details uploaded by supplier till 10th of following month. Recipient filing Quarterly returns can accept details uploaded by supplier till 10th of the month succeeding the quarter for which the return is being filed.

d) Documents rejected by the recipient shall be conveyed to the supplier only after filing of the return by the recipient. Supplier may edit the rejected documents before filing any subsequent return. However, credit will be made available to recipient through the next FORM GST ANX-2 for the recipient. The tax liability for such edited documents will be accounted for in the same tax period.

3. GST ANX-2 (Annexure of Inward Supplies): Details of documents uploaded by the corresponding supplier(s) will be auto populated in FORM GST ANX-2 and recipient(s) can take action on the auto populated documents to — accept, reject or to keep pending on continuous basis after 10th of the following month on which it was uploaded by supplier. Accepted documents would not be available for amendment at the corresponding supplier’s end. Supplier may edit rejected documents before filing subsequent return. However, credit will be available to recipient through next FORM GST ANX-2. The tax liability will be accounted for in the same tax period.

a) Returns not filed for consecutive two months by the supplier- Indication in FORM GST ANX-2 to the recipient that credit shall not be available. However, uploaded invoices will be visible but recipient can not avail ITC on such invoices. Recipient to reject or keep such invoices pending till the supplier files return.

b) Recipient to reject or keep such invoices pending till the supplier files return.

c) However uploaded invoices will be visible but recipient cannot avail ITC on such invoices.

4. Option to file NIL return through SMS will be provided.

5. Harmonized System of Nomenclature (HSN) code will be needed in order to submit details at invoice level.

6. Inward supplies which are liable to RCM have to be declared in FORM GST ANX-1 at the GSTIN level, by the recipient of supplies.

7. Matching tool is available which will help the taxpayer to match their Input Tax Credit based on their FORM GST ANX – 2 and purchase register.

8. The new return system is proposed to be put into place from April 2020. The prototype system of new GST return will be for taxpayers and other stakeholder to familiarize themselves with the ANX-1, ANX-2 and the matching tool.

9. The implementation plan of new returns based on ANX 1 and ANX-2 will be announced shortly.

10. The GSTN has released an interactive web-based trial version of the New Returns (Trial) Offline Tool of Form GST ANX-1, Form GST ANX-2 (with Matching Tool built in it) and a template for Purchase Register to be used to import data from purchase register for matching. The purpose behind release of GST New Return Offline Tool on trial basis is to enable familiarization of stakeholders with tool’s functionalities and to get their feedback/suggestions to improve the tool further, before its actual deployment.

11. GSTN has also provided online version of GST ANX-1 and GST ANX-2 on its portal. This prototype will also allow a taxpayer or user to experience various functionalities by navigating across different sections, upload of invoices, matching of invoices received through ANX-2 with invoices of his books of accounts etc. The documents containing the features of all types of new returns may be obtained from “Download” of the portal: gst.gov.in.

12. The issues and problems being encountered at the time of testing of ANX-I and ANX -2 can be shared as feedback or suggestions with the GSTN by filling in the template(a special sheet that has been provided in GST portal) and mailing the same to NewReturn@gstn.org.in marking a copy to concerned LGSTO/SGSTO.

13. In this background, the GSTN has provided a List of Taxpayers [Supplier (Seller) and Recipient (Buyer)] of all the LGSTOs, who have made supplies to or bought from multiple tax payers during the previous year. The said list will be shared with the concerned DGSTO and who shall further share the list to the concerned LGSTO/SGSTO.

14. The LGSTOs/SGSTOs shall initiate the filing of ANX-1 by supplier and download the ANX-2 by the Recipient, match the invoices, upload the ANX-2. The LGSTOs/SGSTOs should personally supervise the functions of such selected taxpayers and assist them and handhold at all stages. The experience, issues encountered, steps to be taken to simplify the process, if required, suggestions, feedback, positive criticism including appreciations shall be recorded and submitted to the Additional Commissioner of Commercial Taxes (e-Governance) by mail: gst@ka.gov.in

15. This testing will not affect the regular data uploaded by the tax payers and it will be only a dummy data and it will be deleted by the GSTN later on.

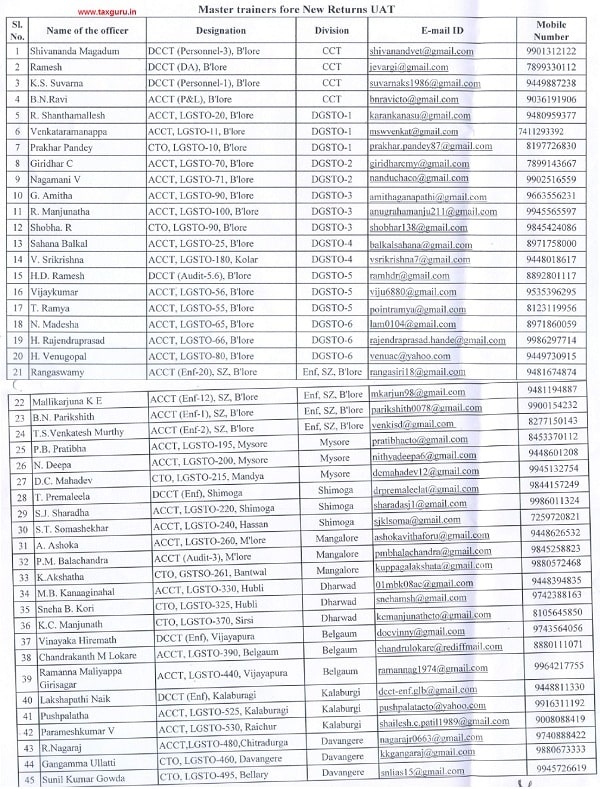

16. A training on features and functionalities of New Returns (Trial) Offline Tool of Form GST ANX-1 and Form GST ANX-2 will be imparted to 45 Master Trainers and three Master trainers will be the Nodal officers for each division to assist the LGSTO/SGSTO and the tax payers. All the master trainer details will be hosted on the web https://gst.kar.nic.in.

17. One day training is being scheduled shortly to all the LGSTOs and SGSTOs on features of GSTPro and New Returns (Trial) Offline Tool of Form GST ANX-1 and FORM GST ANX-2. The date, time and venue will be intimated separately.

18. The Joint Commissioner of Commercial Taxes of respective DGSTO shall supervise through the nodal officers the progress of User Acceptance Testing carried out by the taxpayers and assisted by the LGSTOs. If any assistance required with regard to understanding of the process, procedure etc. the Deputy Commissioner of Commercial Taxes (e-Governance) — e-mail: dcctgov-bng@ka.gov.in may be contacted.

19. This exercise shall begin forthwith, and shall be completed by December 31st, 2019.

20. Further timelines and schedule of activities will be intimated either through letter or mail from this office as and when warranted.

(M S SRIKAR)

Commissioner of Commercial Taxes (Karnataka), Bengaluru

Commissioner or Commercial Taxes Karnataka, Bangalore,

To,

All the officers of the department.

Master trainers fore New Returns UAT