This article wishes to bring to the notice of the concerned authorities a major inconsistency that exist between the provisions of section 44 AB and the Audit Report Utility available in the Income Tax E filing website.

When an Individual or a partnership firm with a turnover not exceeding 1 crore reports a profit of less than 8% of the gross turnover ( 6 % in case the payments are received by account payee cheques or a draft or by way of electronic clearing system), then that person should get their accounts audited by a Chartered Accountant under section 44AB till Assessment Year 2016-17.

But from Assessment Year 2017-18, those persons who have opted to declare the income on presumptive basis under section 44AD in any one of the previous years and have not opted to do so for the 5 subsequent years alone are required to get their accounts audited under section 44AB; as per the amended clause 4 of section 44AD. The minimum deemed profit percentage condition has been done away with effect from 01-04-2017.

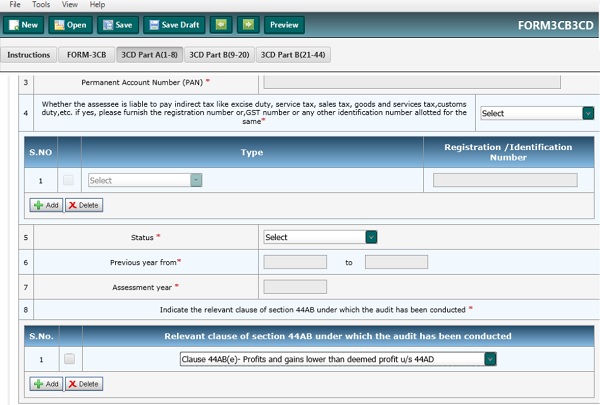

The Chartered Accountant after conducting the tax audit has to submit a statement of particulars in Form 3CD along with his Audit Report in Form 3 CB. In Form 3 CD he has to indicate under which clause of section 44AB the audit was conducted by choosing from a drop-down menu. That menu has 8 options and the seventh one reads “44 AB (e) Profits and gains lower than deemed profit u/s 44 AD”. Nowhere in that menu can one find – “When provisions of section 44 AD (4) are applicable”.

So there is an inconsistency between the provisions of the law and Audit Report utility available in the Income Tax Department’s E filing website. And this has been the case for the past three years.

Therefore it is high time that the department takes notice of this inconsistency and make suitable modifications in the Audit Report utility by removing the option “44AB (e) Profits and gains lower than deemed profit u/s 44AD” and replacing with the following option“44AB (e) When provisions of section 44AD(4) are applicable”.

Apart from doing this modification, CBDT should issue a clarification in this regard to make it amply clear that no tax audit is required when the turnover is less that 1 crore and the profit is less than those prescribed under section 44 AD for those tax payers who have been maintaining accounts on a regular basis and had never opted for presumptive taxation under section 44 AD in any of the assessment years.

It is not inconsistent in my opinion. May be ambiguous and will have to be more clear. However, the same drop down menu is not given in winman and it gives only 5 options.