ITC REVERSAL FOR NON-PAYMENT OF TAX BY SUPPLIER AND RE-AVAILMENT THEREOF – RULE 37A OF CGST RULES (NEWLY INSERTED)

CBIC vide its Notification No 26/2022 – Central Tax dt 26-12-2022 introduced a new rule i.e. Rule 37A regarding reversal of input tax credit in case of non-payment of tax by the supplier and re-availment thereof.

Thus, now buyer need be more cautious about the performance of supplier since non-filling of return by its supplier will affect its credit.

A. Background:

Finance Act, 2022 proposed amendments in following section of Input Tax Credit (ITC):

- Section 16 (2) (C): It states that buyers can claim ITC for a supply if the tax charged on its invoice has been deposited with the government by the supplier / vendor, either in cash or by utilising ITC (Subject to Provisions of Section 41)

- Section 41 (2): It states that the recipient of credit must reverse such ITC claimed if the supplier has not deposited taxes. The proviso allows the buyer to re-avail or re-claim such reversed ITC later when the supplier pays tax.

Such amendments were later made effective from 1st October, 2022 vide Notification No. 18/2022 – Central Tax dated 28.09.2022

However, there was no corresponding rule in the CGST rule in order to govern the procedure of reversal and reclaim of ITC pursuant to Section 41.

Now, CBIC for the purpose of implementation of provision contained in section 41(2) inserted a new Rule called Rule 37A in CGST Rules vide Notification No 26/2022 – Central Tax dt 26-12-2022.

Quote:

[Rule 37A. Reversal of input tax credit in the case of non-payment of tax by the supplier and re-availment thereo.-

Where input tax credit has been availed by a registered person in the return in FORM GSTR-3B for a tax period in respect of such invoice or debit note, the details of which have been furnished by the supplier in the statement of outward supplies in FORM GSTR-1 or using the invoice furnishing facility, but the return in FORM GSTR-3B for the tax period corresponding to the said statement of outward supplies has not been furnished by such supplier till the 30th day of September following the end of financial year in which the input tax credit in respect of such invoice or debit note has been availed, the said amount of input tax credit shall be reversed by the said registered person, while furnishing a return in FORM GSTR-3B on or before the 30th day of November following the end of such financial year:

Provided that where the said amount of input tax credit is not reversed by the registered person in a return in FORM GSTR-3B on or before the 30th day of November following the end of such financial year during which such input tax credit has been availed, such amount shall be payable by the said person along with interest thereon under section 50.

Provided further that where the said supplier subsequently furnishes the return in FORM GSTR-3B for the said tax period, the said registered person may re-avail the amount of such credit in the return in FORM GSTR-3B for a tax period thereafter.]

B. Date of Applicability of Rule 37A:

The effective date of applicability of Section 41 is w.e.f 01-10-2022. Though its corresponding rule i.e. Rule 37A got notified on 26-12-2022, Rule 37A would still be applicable from 01-10-2022 onwards.

C. Contents of Rule 37A:

1. Supplier has duly furnished the details of invoice/debit note in its GSTR-1 and Buyer has claimed the ITC of such invoices/ debit notes based upon the its GSTR-2B (auto populated based upon GSTR-1 filed by Supplier)

2. Supplier has not furnished the GSTR-3B for the period corresponding to such invoice/ debit note till 30th September following the end of financial year in which the ITC is availed by buyer.

3. Buyer need to reverse the ITC while filling its GSTR-3B on or before 30th November following the end of FY in which such ITC is Availed.

4. If buyer not able to reverse within 30th November, ITC amount need to be paid along with interest.

5. Buyer can re-avail/ reclaim the ITC when the supplier file GSTR-3B for the said tax period.

Summary: Rule 37A is applicable if for a particular Invoice/Debit Note, Supplier has duly filed GSTR-1 (along with details of such invoice/debit note) but not its GSTR-3B for that period. Also, Buyer has availed credit based upon its GSTR-2B (auto populated from such GSTR-1 filed by the Supplier). In such case, consequently

| SL | Heading | Reversal of Credit (Required or Not) |

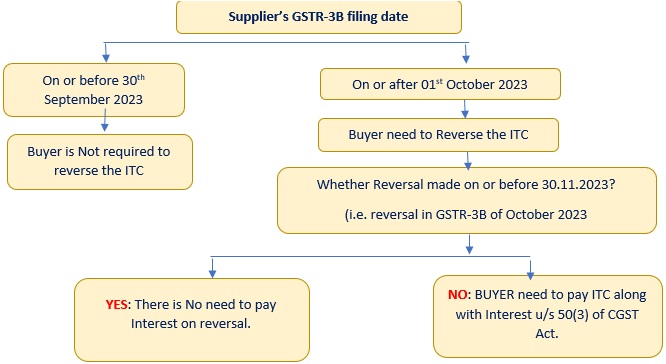

| 1. | If Supplier files the said GSTR-3B on or before 30Th September following the end of FY in which the ITC was availed by the buyer | Buyer is not required to Reverse the Credit availed by it |

| 2. | If Supplier do not file the said GSTR-3B on or before 30Th September following the end of FY in which the ITC was availed by the buyer |

Buyer is required to Reverse the Credit availed by it –in its GSTR-3B filed on or before 30th November (i.e. GSTR-3B of October Month). If Not done within 30th November, then ITC amount need to be paid along with interest. However, Buyer can re-avail the ITC when the said GSTR-3B is filed by Supplier |

For e.g: If during FY 2022-23 (i.e. on or after 01-10-2022), Supplier issued Invoices / debit note, filed its GSTR-1 and Buyer also availed the ITC in FY 2022-23, then following scenario would follow:

Example:

M/s Buyer Ltd received an Invoice dated 01/01/2023 for Rs 118 (Base price Rs 100+ GST@ 18%) against service from M/s Supplier ltd. M/s Supplier Ltd has filled the GSTR- 1 of January 2023 with in due date and as a consequence, the invoice got reflected in GSTR-2B of M/s Buyer Ltd. Based upon its GSTR-2B, M/s Buyer Ltd availed the ITC while filling its GSTR-3B of January 2023. However, M/s Supplier Ltd did not file its GSTR-3B for January 2023. What will be the course of action for M/s Buyer Ltd under following circumstances?

Case-1: M/s Supplier Ltd filed its January 2023 GSTR-3B on 20-09-2023.

Case-2; M/s Supplier Ltd filed its January 2023 GSTR-3B on 20-11-2023.

Case-3: M/s Supplier Ltd filed its January 2023 GSTR-3B on 31-01-2024.

Case-1: Since M/s Supplier Ltd has filed the GSTR-3B prior to 30th September 2023 i.e. 30th September following the end of FY in which ITC has been availed by the Buyer (FY 22-23), M/s Buyer Ltd is not required to reverse the ITC.

Case-2: Since the GSTR-3B has been filled after 30th September 2023, M/s Buyer Limited need to Reverse the ITC by 30th November 2023 i.e. ITC to be reversed while filling GSTR-3B of October 2023 without making payment of Tax and interest. The same ITC can be re avail while filling GSTR-3B of November 2023 as the supplier has filled GSTR-3B in November 2023.

Case-3: Since M/s Supplier Ltd not filled GSTR-3B as on 30th September 2023, M/s Buyer Ltd need to reverse the ITC in GSTR-3B of October, 2023 failing of which it will attract payment of ITC amount along with interest. Say for example, if M/s Buyer Ltd came to know on or after 01.12.2023 by way of self-assessment or by way of investigation by dept that the ITC has not been reversed by 30.11.2023 by it, then Buyer Ltd need to pay the ITC along with interest U/s 50(3) of the CGST Act for the period 01.12.2023 to 31.01.2024. Again M/s Buyer Ltd is eligible for re availment of such ITC while filling GSTR-3B of January 2024 since M/s Supplier Ltd has filled the GSTR-3B in January 2024.

D. Rate of Interest for Reversal of ITC:

Rule 37A prescribe for payment of interest u/s 50 of CGST Act on reversal of ITC.

As per amended provision of Section 5 {vide N/no 09/2022(CT) dt 05.07.2022}

Quote:

Section 5(3): Where the input tax credit has been wrongly availed and utilised, the registered person shall pay interest on such input tax credit wrongly availed and utilised, at such rate not exceeding twenty-four per cent. as may be notified by the Government, on the recommendations of the Council, and the interest shall be calculated, in such manner as may be prescribed]

Important Point:

1. Currently, Interest @ 18% per annum will be applicable where ITC has been availed and utilised.

2. If ITC has been availed but not utilised, the interest need not to be paid by the buyer/recipient.

E. Reclaiming of ITC reversed under Rule 37A

As per the proviso to the rule the buyer is eligible for reclaiming of ITC when the supplier filed its GSTR-3B for corresponding period of tax invoice / debit note.

Important Point:

1. Method of re-availment along with Disclosure in GSTR-3B by Buyer.

I. If Buyer Reverse the ITC prior to 30th November and subsequently supplier file GSTR-3B:

-

- Under this circumstances buyer need to Reverse the ITC in Table 4(B)(2) of GSTR-3B

- After filling of GSTR-3B by supplier, the buyer can re-avail the same in Table 4(A)(5) but the same need to be additionally disclosed in Table 4(D)(1) of GSTR-3B.

II. If Buyer did not reverse the ITC prior to 30th November and subsequently supplier file GSTR-3B:

-

- Since the buyer not reverse the ITC prior to 30th November, the only recourse available is to pay the ITC along with Interest. No need to reverse the same in table 4(B).

- When Supplier files its GSTR-3B, then Buyer can directly re-avail the same in GSTR-4(A)(5). No need to disclose in Table 4(D)(1) since the same was not reversed in Table 4(B)(2).

GSTR-3B : Table-4

2. The time limit for availing of ITC as per Section 16(4) will not be applicable on reclaiming of ITC. Meaning thereby no time limit is available for reclaiming of ITC. It can be claim at any time when supplier files the GSTR-3B.

F. Important Point for Applicability of Rule 37A:

1. Since the date of applicability of section 41 is from 01-10-2022, the new rule may be applicable in respect of those ITC which are availed on or after 01-10-2022. Meaning thereby, ITC availed in GSTR-3B of September 2022 (due date of filling 20-10-2022) and onwards need to be considered for applicability of new rule 37A.

2. The rule specifically mentioned about filling of GSTR-3B not for payment of tax in respect of such particular tax invoice. Therefore, only filling of GSTR-3B will suffice the purpose of Rule 37A. No need to go for intricacies of GSTR-3B.

3. Rule 37A specify the condition of only ITC availed, therefore in the case where ITC availed but not utilised by the buyer and not reversed with in 30th November, payment of ITC along with interest may not be applicable as there is not reduction of outward tax liability by buyer by utilising the ITC. The matter however may be litigated by the dept.

G. Procedural Aspect:

1. Maintain record of all ITC Availed on or after 01-10-2022 (for FY 2022-23) and check the GSTR-3B filling status of supplier from the GSTIN portal.

2. The GSTR-3B for the month pertaining to the Invoice (whose ITC has been availed by the buyer) should be filled by the supplier. Meaning thereby if ITC of Tax Invoice dated 01-12-2022 is availed by buyer, then the supplier needs to file GSTR-3B for December 2022.

3. If any supplier has not filled GSTR-3B for the period pertaining to tax invoice, keep a track of such supplier.

4. If the supplier has not filled the return by 30th September, 2023 then ITC need to be reversed by the buyer in its GSTR-3B for the month of October 2023 (filed on or before 30.11.2023).

5. Failing to do ITC reversal with in 30th November 2023, buyer would be required to pay ITC amount along with payment of Tax and interest u/s 50.

6. ITC can be reclaimed by the Buyer when supplier will file GSTR-3B.

Author Bio

Is there any way to check all the defaulting supplier in a single click or we need to verify all the supplier’s return filing status one by one.