Important Amendment for Goods Transport Agency ( GTA) under Reverse charge Mechanism( RCM) & Forward Charge

As per recommendation of 47th GST Council Meeting, Govt. has issued various notifications on 13/07/2022. As per the new Notifications certain Options has been provided to Goods Transport Agencies (GTA) to charge GST under Forward charge and there are certain changes in Reverse charge Mechanism( RCM) U/s 9(3) of CGST Act 2017.

The summary of changes is as follows

Relevant Notification :

1. Notification No :- 03/2022-Central Tax(Rate) Dt 13/07/2022 ( Amendment to N No 11/2017 Central Tax(Rate) dt 28/06/2017) – Forward Charge [U/s 9(1)]

2. Notification No :- 05/2022-Central Tax(Rate) Dt 13/07/2022 ( Amendment to N No 13/2017 Central Tax(Rate) dt 28/06/2017) – Reverse Charge [u/s 9(3)]

Analysis :

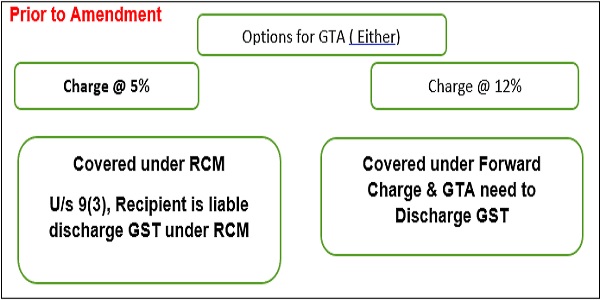

Prior to this amendment, GTA has only 2 options i.e.

1. GTA may charge GST @ 5% without ITC, in such case the specified recipient are liable to discharge the GST under Reverse charge Mechanism (RCM) as per section 9(3) notified under N No 13/2017 Central Tax(Rate) dt 28/06/2017

Or

2. GTA may charge GST @ 12% with ITC as per N No 11/2017 Central Tax(Rate) dt 28/06/2017. In such case GTA has to discharge the GST under Forward charge.

Amendment under Forward Charge Section 9(1) of CGST Act 2017

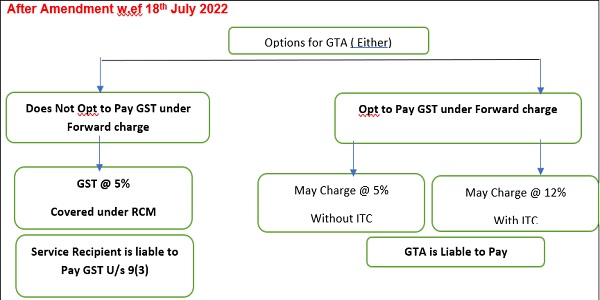

Now Govt has amended the original N No 11/2017 Central Tax(Rate) dt 28/06/2017 by way of issuing Notification no 03/2022 dt 13/07/2022(Central Tax Rate). Under the new notification Govt has provided an option to GTA to charge GST @ 5% under Forward charge in addition to existing rate @ 12%.

Meaning thereby, in the beginning of each Financial Year the GTA has to choose the option either to charge GST under Forward charge @ 5% with out ITC or to Charge @ 12 % with ITC.

Such Option for a Financial Year need to apply by 15th of March of Preceding FY . i.e. For FY 2023-24 the GTA need to apply the option by 15th March,2023.

However, Dept has provide an opportunity to claim the Option for FY 2022-23 also. The GTA wants to opt for charging GST @5% or 12% under Forward charge for FY 2022-23 should apply the option on or before 16th August 2022.

Such Option shall be exercised by making a declaration provided in Annexure-V to the notification no 03/2022. ( see below)

Amendment under Reverse Charge Mechanism- Section 9(3) of CGST Act 2017:

Now Govt has amended the original N No 13/2017 Central Tax(Rate) dt 28/06/2017 by way of issuing new Notification No :- 05/2022-Central Tax(Rate) Dt 13/07/2022

As per the Notification, Now the Specified Service recipient need to discharge GST under RCM if the same Service provided by GTA who had not opt for forward charge payment of GST as provided under Notification no 03/2022 dt 13/07/2022(Central Tax Rate)

Meaning thereby, If the service recipient Received a Tax Invoice from the GTA containing the declaration(Mentioned in Notification No :- 05/2022-Central Tax(Rate) Dt 13/07/2022) that the GTA has opted for Payment of Tax under Forward charge, then the service recipient is not required to pay tax under RCM .

In the absence of such Tax Invoice and Declaration as per Annexure-III of the Notification No :- 05/2022-Central Tax(Rate) Dt 13/07/2022 , the specified service recipient is liable to discharge GST Under RCM.

Declaration by GTA Under Notification No :- 05/2022-Central Tax(Rate) Dt 13/07/2022 in Tax Invoice

“ I/we have taken registration under the CGST Act, 2017 and have exercised the option to pay tax on services of GTA in relation to transport of goods supplied by us during the Financial Year _____ under forward charge.”

New Declaration by GTA Under Notification no : 14/2022 dt 05-07-2022( Central tax)

As per the notification sl no 4 of the Notification :

Quote :

In the said rules, in rule 46, after clause (r), the following clause shall be inserted, namely: – ̳

(s) a declaration as below, that invoice is not required to be issued in the manner specified under sub-rule (4) of rule 48, in all cases where an invoice is issued, other than in the manner so specified under the said sub-rule (4) of rule 48, by the taxpayer having aggregate turnover in any preceding financial year from 2017-18 onwards more than the aggregate turnover as notified under the said sub-rule (4) of rule 48

I/We hereby declare that though our aggregate turnover in any preceding financial year from 2017-18 onwards is more than the aggregate turnover notified under sub-rule (4) of rule 48, we are not required to prepare an invoice in terms of the provisions of the said sub-rule.

Unquote :

Analysis : A declaration as above, is required to be made on invoice issued by registered person whose aggregate turnover exceeds Rs 20 Crores but who is exempt from issuance of e-invoice such as

- insurer or

- banking company or financial institution, including NBFC

- Goods Transport Agency (GTA),

- supplier of taxable service is supplying passenger transportation service and

- registered person supplying services by way of admission to exhibition of cinematograph films in multiplex screens:

In view of the above, in case where GTA whose Turnover in any preceding FY from 2017-18 onwards exceeds Rs 20 cr and it is specifically outside the purview of the generation of e-invoice need to mention the above declaration in his Tax Invoice.

Summary of Important Points:

1. W. e. f 18th July 2022, GTA has been provided with an option to choose either to charge GST @ 5% without ITC or @ 12% GST with ITC Under Forward charge ( Earlier only 12% forward Charge is Available)

2. If Such option has not bee exercised, and GTA wants to issue invoice @ 5% such service will be covered under RCM U/s 9(3) of CGST Act.

3. Such Option for a Financial Year need to apply by 15th of March of Preceding FY.

4. The GTA wants to opt for charging GST @5% or 12% under Forward charge for FY 2022-23 should apply the option on or before 16th August 2022.

5. The GTA Issuing Tax Invoice under Forward charge need to furnish a declaration in the Tax invoice ( as per Notification No :- 05/2022-Central Tax(Rate) Dt 13/07/2022 ) as follows

I/we have taken registration under the CGST Act, 2017 and have exercised the option to pay tax on services of GTA in relation to transport of goods supplied by us during the Financial Year _____ under forward charge.

6. The Recipient of Service while making payment need to ensure that, if Tax invoice has been issued by the GTA does not charge GST under Forward charge and no declaration has been furnished for opting of tax under Forward charge, GST under RCM need to be discharged by the recipient.

7. If GTA’s Turnover in any preceding FY from 2017-18 onwards exceeds Rs 20 cr. Then GTA needs to furnish the following declaration in Tax Invoice as per Nno 14/2022 dt 05-07-2022

I/We hereby declare that though our aggregate turnover in any preceding financial year from 2017-18 onwards is more than the aggregate turnover notified under sub-rule (4) of rule 48, we are not required to prepare an invoice in terms of the provisions of the said sub-rule.

A comparative view of amendment

Prior to Amendment: N. No 11/2017

| Sl no | Chapter, Section or Heading | Description of Service | Rate (per cent.) | Condition |

| 9 | Heading 9965 (Goods transport services) | [(iii) Services of goods transport agency (GTA) in relation to transportation of goods (including used household goods for personal use). Explanation.- “goods transport agency” means any person who provides service in relation to transport of goods by road and issues consignment note, by whatever name called. | 2.5 | Provided that credit of input tax charged on goods and services used in supplying the service has not been taken [Please refer to Explanation no. (iv)] |

| or | ||||

| 6 | Provided that the goods transport agency opting to pay central tax @ 6% under this entry shall, thenceforth, be liable to pay central tax @6% on all the services of GTA supplied by it.]57 | |||

After Amendment vide Notification no 03/2022 dt 13/07/2022(Central Tax Rate)

| Sl. no | Chapter, Section or Heading | Description of Service | Rate (per cent.) | Condition |

| 9 | Heading 9965 (Goods transport services) | (iii) Services of Goods Transport Agency (GTA) in relation to transportation of goods (including used house hold goods for personal use) supplied by a GTA where,-.

(a) GTA does not exercise the option to itself pay GST on the services supplied by it |

2.5 | Provided that credit of input tax charged on goods and services used in supplying the service has not been taken [Please refer to Explanation no. (iv)] |

| (b) GTA exercises the option to itself pay GST on services supplied by it. | 2.5

Or

6 |

(1) In respect of supplies on which GTA pays tax at the rate of 2.5%, GTA shall not take credit of input tax charged on goods and services used in supplying the service.[Please refer to Explanation no. (iv)]

(2) The option by GTA to itself pay GST on the services supplied by it during a Financial Year shall be exercised by making a declaration in Annexure V on or before the 15th March of the preceding Financial Year: Provided that the option for the Financial Year 2022-2023 shall be exercised on or before the16th August, 2022 Provided further that invoice for supply of the service charging Central tax at the rates as applicable to clause(b) maybe issued during the period from the 18th July,2022 to 16th August, 2022 before exercising the option for the financial year 2022-2023 but in such a case the supplier shall exercise the option to pay GST on its supplies on or beforethe16thAugust,2022.” |

“Annexure V

FORM

Form for exercising the option by a Goods Transport Agency (GTA) for payment of GST on the GTA services supplied by him under forward charge before the commencement of any financial year to be submitted before the jurisdictional GST Authority

Reference No.-

Date: –

1. I/We______________ (name of Person), authorised representative of M/s……………………. have taken registration/have applied for registration and do hereby undertake to pay GST on the GTA services in relation to transportation of goods supplied by us during the financial …………..under forward charge in accordance with section 9(1) of the CGST Act, 2017 and to comply with all the provisions of the CGST Act, 2017 as they apply to a person liable for paying the tax in relation to supply of any goods or services or both.

2. I understand that this option once exercised shall not be allowed to be changed within a period of one year from the date of exercising the option and will remain valid till the end of the financial year for which it is exercised.

Legal Name: –

GSTIN: –

PAN No.

Signature of Authorised representative:

Name of Authorised Signatory:

Full Address of GTA

Changes in Reverse Charge Mechanism ( RCM)

Prior to Amendment : N No 13/2017 Central Tax(Rate) dt 28/06/2017– Reverse Charge Mechanism ( RCM)

| Sl no | Category of Supply of Services | Supplier of service | Recipient of Service |

| (1) | (2) | (3) | (4) |

| (i) | Supply of Services by a goods transport agency (GTA), [who has not paid central tax at the rate of 6%,]1 in respect of transportation of goods by road to-

(a) any factory registered under or governed by the Factories Act, 1948(63 of 1948); or

(b) any society registered under the Societies Registration Act, 1860 (21 of 1860) or under any other law for the time being in force in any part of India; or (c) any co-operative society established by or under any law; or (d) any person registered under the Central Goods and Services Tax Act or the Integrated Goods and Services Tax Act or the State Goods and Services Tax Act or the Union Territory Goods and Services Tax Act; or (e) any body corporate established, by or under any law; or f) any partnership firm whether registered or not under any law including association of persons; or ( g) any casual taxable person. [Provided that nothing contained in this entry shall apply to services provided by a goods transport agency, by way of transport of goods in a goods carriage by road, to, – (a) a Department or Establishment of the Central Government or State Government or Union territory; or (b) local authority; or (c) Governmental agencies, which has taken registration under the Central Goods and Services Tax Act, 2017 (12 of 2017) only for the purpose of deducting tax under section 51 and not for making a taxable supply of goods or services.]2 |

Goods Transport Agency (GTA) | (a) Any factory registered under or governed by the Factories Act, 1948(63 of 1948); or

(b) any society registered under the Societies Registration Act, 1860 (21 of 1860) or under any other law for the time being in force in any part of India; or (c) any co-operative society established by or under any law; or (d) any person registered under the Central Goods and Services Tax Act or the Integrated Goods and Services Tax Act or the State Goods and Services Tax Act or the Union Territory Goods and Services Tax Act; or (e) any body corporate established, by or under any law; or (f) any partnership firm whether registered or not under any law including association of persons; or (g) any casual taxable person; located in the taxable territory. |

After Amendment: vide N no 05/2022 dt 13/7/2022

| Sl no | Category of Supply of Services | Supplier of service | Recipient of Service |

| (1) | (2) | (3) | (4) |

| Supply of Services by a goods transport agency (GTA), [who has not paid central tax at the rate of 6%,] in respect of transportation of goods by road to-

(a) any factory registered under or governed by the Factories Act, 1948(63 of 1948); or (b) any society registered under the Societies Registration Act, 1860 (21 of 1860) or under any other law for the time being in force in any part of India; or (c) any co-operative society established by or under any law; or (d) any person registered under the Central Goods and Services Tax Act or the Integrated Goods and Services Tax Act or the State Goods and Services Tax Act or the Union Territory Goods and Services Tax Act; or (e) any body corporate established, by or under any law; or f) any partnership firm whether registered or not under any law including association of persons; or (g) any casual taxable person. [Provided that nothing contained in this entry shall apply to services provided by a goods transport agency, by way of transport of goods in a goods carriage by road, to, – (a) a Department or Establishment of the Central Government or State Government or Union territory; or (b) local authority; or (c) Governmental agencies, which has taken registration under the Central Goods and Services Tax Act, 2017 (12 of 2017) only for the purpose of deducting tax under section 51 and not for making a taxable supply of goods or services.]2 “Provided further that nothing contained in this entry shall apply where, – i. the supplier has taken registration under the CGST Act, 2017 and exercised the option to pay tax on the services of GTA in relation to transport of goods supplied by him under forward charge; and ii. the supplier has issued a tax invoice to the recipient charging Central Tax at the applicable rates and has made a declaration as prescribed in Annexure III on such invoice issued by him.”; |

Goods Transport Agency (GTA) | (a) Any factory registered under or governed by the Factories Act, 1948(63 of 1948); or

(b) any society registered under the Societies Registration Act, 1860 (21 of 1860) or under any other law for the time being in force in any part of India; or (c) any co-operative society established by or under any law; or (d) any person registered under the Central Goods and Services Tax Act or the Integrated Goods and Services Tax Act or the State Goods and Services Tax Act or the Union Territory Goods and Services Tax Act; or (e) any body corporate established, by or under any law; or (f) any partnership firm whether registered or not under any law including association of persons; or (g) any casual taxable person; located in the taxable territory. |

“Annexure III

Declaration

I/we have taken registration under the CGST Act, 2017 and have exercised the option to pay tax on services of GTA in relation to transport of goods supplied by us during the Financial Year _____ under forward charge.”

Author Bio

sir a transport agency register in mp and Opt GST FORWARD Sch and charged 12 Percent .they want to open a branch in karantaka and want to adopt Rcm Scheme it is possible

Nice articles. Please send articles to this ID:

Chaitra @loadshare.net

Can a gst having two seperate registrations in one state, opt for forward charge under one GSTIN and reverse charge under another GSTIN?

If GTA has charged 5% GST (2.5*2) is it necessary for the recipient to pay GST under RCM or NOT required to pay if GTA charged 5% (WITHOUT ITC)

If GTA has opted RCM option and transfer good for an unregistered person then who liable to pay GST

If the transportation service is received by a NON-GTA, whether it will be chargeable for RCM?

Please guide.

how to opt in for Forward charge in GST portal

Whether RCM exemption where freight is ₹ 1500 / ₹ 750 stands withdrawan?

Now for GTA who doesn’t charge GST in invoice

RCM applicable from ₹ 1?

Please guide

Yes the exemption provided earlier to GTA vide notification no 12/2017 (sl21) got deleted vide notification no 04/2022 from 18/07/22. Therefore w.e.f 18/07/2022 gst provision would apply Even for Rs 1