The Pension Fund Regulatory and Development Authority (PFRDA) has released a Consultation Paper proposing a dual valuation framework (using both ‘accrual’ and ‘fair market’ methods) for long-dated Government Securities held within the National Pension System (NPS) and Atal Pension Yojana (APY) schemes. This proposal, detailed in the paper dated October 17, 2025, aims to improve governance and protect subscriber interests by offering a more stable and simplified depiction of pension wealth during the long accumulation phase. The primary objective is to reduce the impact of short-term interest rate volatility on the scheme’s Net Asset Value (NAV), as these fluctuations are immaterial for long-term investors. By insulating a portion of the long-dated, less liquid government securities from daily ‘mark-to-market’ swings, the PFRDA intends to better align pension fund investments with long-term capital formation, supporting productive, long-gestation infrastructure projects. Stakeholders, including subscribers, pension funds, and the public, are invited to submit their feedback on the proposed framework by November 30, 2025.

Ministry of Finance

PFRDA releases Consultation Paper to Align Valuation Guidelines with Core Objectives of Long-Only Pension Funds investing in Government Securities and calculation of Net Asset Value (NAV)

Consultation Paper Proposes Dual Valuation Framework to Enhance Transparency and Stability in NPS and APY Schemes PFRDA invites Stakeholder Feedback on Consultation Paper; Comments Open till November 30, 2025

Posted On: 21 OCT 2025 7:20PM by PIB Delhi

The Pension Fund Regulatory and Development Authority (PFRDA) has released a comprehensive Consultation Paper titled “Alignment of Valuation Guidelines with the core objectives of Long-only Funds when investing in Government Securities and calculation of Net Asset Value (NAV)”.The framework proposed is part of PFRDA’s ongoing commitment towards improving governance, protecting subscriber interests and contributing for India’s broader financial and infrastructural growth.

The Consultation Paper, dated October 17, 2025, proposes adoption of dual valuation framework (‘accrual’ and ‘fair market’) for long dated Government Securities held in NPS/APY to achieve three key purposes:

1. Depict stable and simplified pension wealth accumulation to subscribers during the accumulation phase.

2. Reduce the impact of short-term interest rate volatility on scheme NAV, since such fluctuations do not materially affect subscribers during the accumulation phase.

3. Align pension fund investments with long-term capital formation, boosting stakeholder confidence by funding productive, long-gestation infrastructure assets.

Overall, the framework aims to present pension wealth accumulations more clearly to subscribers while ensuring long-term financial stability and economic relevance.

Invitation for Stakeholder Comments

The consultation paper is available on PFRDA website under the tab Research andPublication. (https://pfrda.org.in/en/web/pfrda/consultation-papers). PFRDA is seeking feedback on the proposal from all stakeholders, including NPS participants, prospective subscribers, pension funds, industry experts, academia and the general public.

The Authority encourages thorough review and constructive inputs on the proposals to ensure the successful development and implementation of the schemes regulated by PFRDA.

Stakeholders are requested to submit their comments, inputs and feedback on aforesaid the consultation paper latest by 30th November 2025.

*****

Pension Fund Regulatory and Development Authority

CONSULTATION PAPER

Alignment of Valuation Guidelines with the core objectives of Long-only Funds when investing in Government Securities and calculation of Net Asset Value (NAV)

This consultation paper attempts to explore adoption of dual valuation methodology for Government Securities held in NPS/APY schemes managed by the Pension Funds.

1. OBJECTIVE

The purpose of applying dual valuation framework (partly accrual basis and fair market value) within the scheme portfolio comprising of Government Securities are threefold:-

i. depict to subscribers of a Defined Contribution Pension Plan like NPS, a simple and stabilised accumulations of pension wealth during their contribution phase or working years.

ii. minimise the impact of short-term volatility of interest rate on scheme NAV. Such cyclical phenomenon disturbs the market valuation of debt papers including long-dated Government Securities while the resultant notional gains or loss on investments is immaterial to subscribers during the accumulation phase (pension wealth).

iii. better align the role of Pension Funds in converting long term savings into productive long gestation capital formation and thereby enhance stakeholders’ confidence.

2. BACKGROUND

National Pension System (NPS) is a Defined Contribution (DC) pension plan wherein the investment risks are fully borne by subscribers. Pension Fund managing the investments or schemes on behalf of NPS Trust, acts as a pass-through entity. Pension Fund are required to invest the contributions made by subscribers in those asset classes (i.e instruments permitted by PFRDA) as chosen by the subscriber. Upon completion of the accumulation phase, the pension wealth or outstanding corpus is utilised by subscriber to receive periodic payouts through a variety of mechanisms permitted by PFRDA.

Currently, the investments held under NPS are ‘mark to market’ and the pension funds are mandated to declare scheme NAVs at the close of each working day. In this scenario, the investment returns to subscribers are thus directly linked to the market conditions of each day and the performance of pension fund (in managing the scheme portfolios) gets adjudged for each day instead of a holistic evaluation of performance during the entire accumulation phase of the subscriber.

Typically defined contribution pension plans, have a long accumulation phase spanning between 20 to 40 years and the method of valuing the investments plays a crucial role in depicting the pension wealth to a subscriber.

From a subscriber’s perspective, fair valuation of investments is crucial at the point of exercising withdrawals or subscriber receiving payments from the scheme because at this point the exact quantum of accumulated pension wealth gets determined for being paid to the subscriber. In contrast, during accumulation phase, notional gain or loss of accumulated pension wealth due to short-term volatility of interest rates may not be of much relevance to a subscriber.

3. CHALLENGES

Presently, the accounting and valuation guidelines issued by PFRDA prescribes fair valuation (mark-to-market) for all securities (equity, corporate bond, government securities) held in the scheme portfolios under NPS/APY. This valuation norm is applied uniformly across all debt securities (corporate or government) regardless of their maturity profiles or the schemes/asset class in which these debt securities are held. The challenges faced are:

(i) Long-dated debt securities constitute a substantial portion of the scheme portfolios (Central Government, State Government, Corporate CG, NPS Lite, Asset Class ‘C’, Asset Class ‘G’), which are more sensitive to interest rate fluctuations. A snapshot of NPS/APY scheme holdings in Government Securities (inclusive of State Development Loans and Govt. Guaranteed Bonds) out of the total AUM of Rs 15,49,611.97 crore as on 29.08.2025, is depicted hereunder:

| Asset Class | < 1 yr | 1 yr to 5 yr | 5yr to 10yr | 10yr to 15 yr | 15yr & above | Total |

| Govt. Securities | 842 | 35,155 | 1,57,608 | 1,11,337 | 2,80,053 | 5,84,996 |

| State Dev. Loans | 1,179 | 36,491 | 92,032 | 49,067 | 24,493 | 2,03,262 |

| Govt. Guaranteed | – | 2,620 | 10,504 | – | – | 13,124 |

| TREPS | 306 | – | – | – | – | 306 |

| Total | 2,328 | 74,266 | 2,60,143 | 1,60,405 | 3,04,546 | 8,01,737 |

| % of total | 0.29% | 9.26% | 32.45% | 20.01% | 37.99% | 100.00% |

Of the total NPS/APY AUM of Rs 15,49,611.97, Government Securities (inclusive of State Development Loans and Govt. Guaranteed Bonds) constitute 51.74%. It can be observed that debt investments having a residual maturity of 10 years and above comprises of 59.15% of the total Government Securities holdings in NPS/APY.

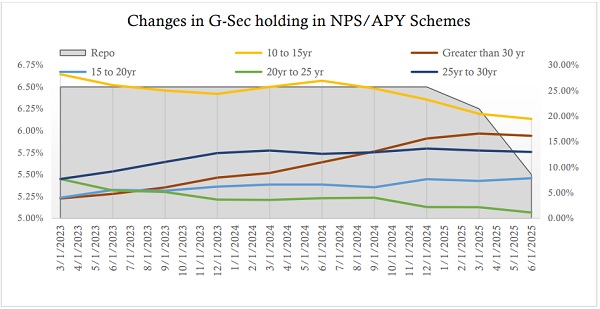

A graphical representation of Government Securities held in NPS/APY schemes by Pension Funds under various maturity buckets during the period 01.03.2023 to 01.06.2025 is depicted below:

As can be observed from the above graph, allocation towards long dated Government Securities (residual maturity of greater than 30 years) have increased from a low of 3.89% in March 2023 to 16.59% in March 2025.

(ii) Long-dated debt securities are relatively less liquid compared to debt securities with shorter-duration. The prevalence of lower market liquidity can be attributed towards limited market participants for long-dated securities (typically banks, insurance and pension funds) and higher interest rate risk associated with long-dated securities. These factors collectively constrain secondary market activity and hampers efficient trading by investors. The securities trading data analysed from CCIL website for the period 01-03-2025 to 29-08-2025 and the break-up of the average face value traded for each month is depicted hereunder:

| Month | Mar-25 | Apr-25 | May-25 | Jun-25 | Jul-25 | Aug-25 |

| Less than 1 year | 12.97% | 7.53% | 7.69% | 9.22% | 9.68% | 8.13% |

| 1 to 5 years | 14.69% | 12.96% | 17.11% | 13.12% | 13.30% | 11.84% |

| 5 to 10 years | 49.02% | 60.95% | 59.83% | 61.72% | 58.17% | 61.29% |

| 10 to 15 years | 11.72% | 10.89% | 6.71% | 6.97% | 7.37% | 8.47% |

| 15 to 20 years | 1.18% | 0.86% | 1.07% | 0.72% | 1.31% | 0.69% |

| 20 to 25 years | 1.95% | 0.30% | 0.73% | 0.63% | 0.84% | 0.31% |

| 25 to 30 years | 3.49% | 2.51% | 2.77% | 3.92% | 4.28% | 3.99% |

| 30 to 35 years | 0.31% | 0.08% | 0.16% | 0.12% | 0.27% | 0.61% |

| 35 to 40 years | 3.77% | 2.75% | 2.73% | 2.76% | 3.95% | 3.42% |

| 40 to 45 years | 0.07% | 0.39% | 0.04% | 0.08% | 0.02% | 0.07% |

| 45 to 50 years | 0.83% | 0.80% | 1.14% | 0.76% | 0.81% | 1.18% |

| Grand Total | 100.00% | 100.00% | 100.00% | 100.00% | 100.00% | 100.00% |

It can be observed from the above table that securities with residual maturity of 5 to 10 years are the most liquid instruments. Nearly 80% of trades have occurred in the 010 years maturity bucket and nearly 90% of trades have occurred in 0-15 years maturity bucket for the period under consideration. Trades beyond 30 years maturity bucket account for only about 5% in any given month.

iii. Though long-dated debt securities offer higher yields compared to shorter duration papers, short-term interest rate movements with mark-to-market valuation results in investment gain or loss (purely notional in nature) and these fluctuations does not reflect the intent of holding such long-dated securities (with higher yields) in the scheme portfolio till maturity but gives an impression that it will be sold immediately.

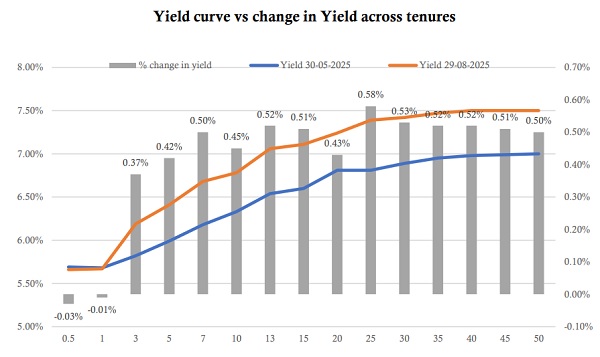

iv. The effects of short-term volatility in interest rates are ultimately passed on to subscribers through scheme NAVs, leading to unjust depiction of their pension wealth during the accumulation phase, which may undermine the system. The movement of yield curve across various maturities during the past 04 months (May-August 2025) is depicted in the chart below:

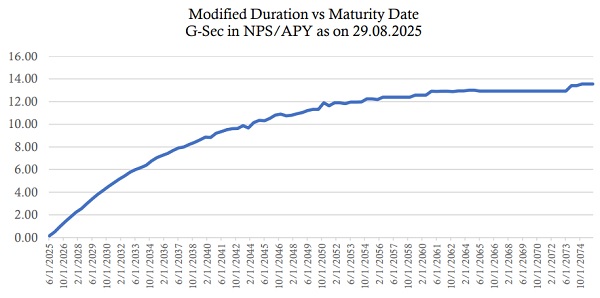

v. Though long-dated securities carry significant duration risk, it is observed that the interest rate risk starts flattening beyond the 30-year residual maturity. Considering the relationship that price of debt securities is inversely proportional to interest rates and using modified duration to measure debt securities price sensitivity for a given change in interest rates with modified duration of 12, on a 1% rise in interest rates, the price of the debt security will decrease by about 12% (ignoring for convexity), the following chart depicts the Modified Duration vs Maturity Date of Government Securities of NPS/APY Schemes as on 28.09.2025.

As can be observed from the above chart, the modified duration of securities starts flattening to about 12 years when the residual maturity crosses 30 years. Thus, it may be interpreted that the interest rate risk starts flattening beyond the 30-year residual maturity and beyond this point while the absolute duration risk remains high for high maturity securities, holding an incremental unit of maturity adds limitedly to the potential upside from a decrease in interest rates.

It is envisaged that the challenges narrated above may get resolved by shifting a part of the Government Securities holding into HTM category viz. the illiquid long-dated debt securities. This model may deliver dual benefit of insulating the scheme NAVs from market price fluctuations of debt securities due to short-term volatility of interest rates and provide greater flexibility to pension funds to actively manage the most liquid debt securities (take benefit of interest rate movements) and maintain overall portfolio liquidity.

Moreover, in an emerging economy like India, the requirements of funds for infrastructure development are immense considering the fact that infrastructure projects are in the nature of long-term, large-scale and capital-intensive viz. roads, ports, railways, airports, power plants, digital connectivity, etc. Infrastructure development necessitates significant upfront investments coupled with realisation of returns after long gestation periods (after completion of project). Thus, infrastructure development demands long-term capital (investments) which can be locked in for 10-30 years and any interruptions of capital inflows during the gestation period would delay or derail the project, lead to costs escalations and inefficient delivery of economic benefits to the citizens. The sources of long-term funds for financing infrastructure are government borrowings or institutional investors like insurance companies, pension funds or sovereign wealth funds. In other words, NPS/APY investments in Government Securities indirectly supports economic growth, job creation, improved public services which lays the foundation for transition from a developing to a developed nation.

4. FRAMEWORK PROPOSED

To overcome the above noted challenges and with an objective to minimise the effects of short-term volatility of interest rates in scheme NAVs alongwith depiction of simplified investment returns to subscribers during the accumulation phase, this consultation paper proposes a dual valuation approach for the securities held in scheme portfolios of NPS/APY viz. Long-dated Government Securities (residual maturity, above xx years or modified duration, above xx years) valued on ‘accrual basis’ and remaining as mark-to-market.

Drawing a parallel from the banking industry, Categorisation of all Government Securities held in the scheme portfolios of NPS/APY is proposed to be undertaken as under:

| Category – Govt. Securities | Valuation Method | Purpose |

| Held-to-Maturity (HTM) | Accrual or Amortisation | minimise short-term interest rate volatility effects on scheme NAV |

| Available-for-Sale (AFS) | Mark-to-Market | continue reflection of fair value |

The features and benefits of both the valuation methodologies are briefly outlined below:

i. With ‘accrual basis’ of valuation or HTM;

− the coupon or interest income on securities gets recognised or accrued as receivable on a daily basis till its receipt. The discount/premium over face value of securities will get amortised over time.

− the aforesaid accounting approach insulates the daily price fluctuations of the securities due to interest rate movements and facilitates valuation of securities at a stable and consistent rate over time, free from interest rate volatility.

− with elimination of short-term notional gain/loss due to interest rate movements, the depiction of subscriber’s pension wealth during accumulation phase gets smoothened out and easy to comprehend.

− pension fund may scale down active debt portfolio management due to shift in their investment focus (deploying subscriber contributions in higher yielding securities as interest rate movement does not impact the scheme portfolio performances).

ii. With fair or ‘mark to market’ valuation;

− the coupon or interest income on securities gets recognised or accrued as receivable on a daily basis till its receipt. The securities get valued at the price, as if, it will be liquidated in the market.

− the value of securities reflects current market conditions and ensures transparency.

− it depicts to subscriber the actual value of pension wealth if liquidated under current market conditions even though the subscriber may withdraw the pension wealth at a future date after completion of the accumulation phase.

− with investment risks being fully borne by subscribers, ‘mark to market’ valuations imply pension funds are primarily a pass-through entity and this facilitates easier risk management and liquidity management of the scheme portfolio.

5. ANALYSIS

Though both the valuation methodology has its own merits and drawbacks depending on the scheme design (open/close ended, contributions, lock-in/vesting period, withdrawals, guarantee of returns, liabilities of fund manager, etc.), the relevant features of NPS are summarised below:

− accumulation period for subscriber’s stretches between 20-40 years.

− contributions are invested by pension funds (in permitted asset classes) as per the choices exercised by subscribers and the investment risks are fully borne by subscriber.

− withdrawals of contributions are restricted, with partial withdrawal of pension wealth is permitted only after 5 years upto 25% of their own contributions and complete withdrawals permitted after subscriber attains 60 years of age or at superannuation.

− subscribers have flexibility to change the pension fund (once in a year) and change the asset allocation (once in a quarter) during the accumulation phase.

− pension funds have the responsibility to actively manage the scheme portfolio and undertake investments only in those securities permitted by PFRDA.

− scheme NAVs are declared by the pension funds for each working day and evaluation of pension fund performance is based on returns generated for the scheme.

− Government Securities are permitted for investments exclusively in Asset Class ‘G’ and upto 65% of scheme portfolio in Central Government scheme, State Government scheme, Corporate CG scheme, NPS Lite scheme and Atal Pension Yojana (APY).

A comparison of valuing Government Securities on ‘accrual basis’ and as ‘mark-to-market’, is envisioned below: –

| Parameter | Accrual | Mark-to-Market |

| Investment Objective | buy and hold the security till maturity | buy and sell the security before

maturity |

| Change in value of security due to interest rate movement | notional pension wealth is not impacted | notional pension wealth is impacted due to inverse relationship between interest rate & price of debt security |

| Impact on scheme NAV | stabilised movement | linked to volatility of interest rate |

| Reflection of pension wealth | economic performance | current market conditions |

| Transfer of value while executing withdrawal/switch | may not reflect the actual value paid from scheme | actual realisable value is paid from scheme |

| Industry Practices | Insurance (except ULIP), Banks (partly), EPFO (except equity), DB pensions | mutual funds, Banks (partly), NPS |

| Accounting Standards | based on regulatory guidelines as IndAS is not applicable for Trusts | |

From the above, inference can be drawn that:-

i. valuation on ‘accrual basis’ is preferable when scheme liabilities are pre-determined, subscriber has limited investment choices, withdrawals by subscriber is not on demand anytime and are payable on a known future date.

ii. valuation on ‘mark-to-market’ is best suited when scheme offers withdrawal facility to subscriber at any point of time or when inflows and outflows are un-defined.

6. PROPOSAL CONSULTATIONS

Considering the structure/features of NPS, this consultation paper seeks to elicit views/comments from the public and stakeholders on the proposal of valuing a portion of the Government Securities (G-Sec) portfolio in the NPS/APY schemes on ‘accrual basis’ on the underlying framework: –

– optimum portion or percentage of G-Sec portfolio that may be valued on ‘accrual basis’ viz. 10% – 60%, such that the difference in scheme NAVs is minimal between the scheme portfolios valued entirely on ‘mark-to-market’ and the proposed valuation method.

– criteria (to be laid down) for segregating the G-Sec portfolio into two broad categories (HTM and AFS) viz. based on residual maturity or modified duration of each security. and for movement of individual securities between these 02 categories.

– restrictions (to be imposed) for curtailing fund outflows (due to subscriber choices and switching) from the scheme wherein dual valuation methodology is adopted for G-Sec holdings in the scheme portfolio viz. partly ‘accrual basis’ and partly ‘mark-to-market’.

– periodicity (to be specified) at which comparison should be undertaken for valuing the scheme portfolio with 02 different valuation methodologies. If difference in NAVs are observed, the acceptable tolerance limits for maximum difference in scheme NAVs between the scheme portfolios valued entirely on ‘mark-to-market’ and the proposed valuation methodology. In case of differences in scheme NAVs is beyond the acceptable tolerance limits, the remedial measures to be undertaken (viz. recasting unit allocation)

– disclosures (to be mandated) on computation of scheme NAVs with dual valuation methodology for Government Securities holdings in the scheme portfolios for ensuring regulatory, operational and accounting integrity of the system.

8. CONCLUSIONS

It is envisaged that the above proposed framework (dual valuation) balances prudence and realism that reflects the economic purpose of the investments and simultaneously would depict stable accumulation of pension wealth in a simplified manner to subscribers.

9. COMMENTS FROM STAKEHOLDERS

Comments/views are solicited on this consultation paper from stakeholders and the general public which may be submitted latest by 30th November 2025 in softcopy or hardcopy to:-

E-mail: sup-pf@pfrda.org.in

OR

To,

Chief General Manager – Supervision Fund Management

Pension Fund Regulatory and Development Authority (PFRDA),

Tower E, 5th Floor, World Trade Centre, Nauroji Nagar, New Delhi – 110029

Friday, 17 October 2025

ANNEXURE

As on 31st July 2025 – Types of Securities held in NPS /APY Schemes

| Asset Type | Amount | % AUM |

| Central Government Securities | 598317 | 38% |

| State Government Securities | 204751 | 13% |

| Government Guaranteed Bonds | 11305 | 1% |

| Bonds issued by PSU-PFI | 190276 | 12% |

| Bonds issued by Banks | 77377 | 5% |

| Basel III Additional Tier I Bonds | 9635 | 1% |

| Bonds issued by NBFC | 45270 | 3% |

| Bonds issued by corporate entities | 20353 | 1% |

| Bonds issued by Insurance company | 4520 | 0% |

| Bonds issued by IFC | 73 | 0% |

| Pass Through Certificates | 803 | 0% |

| Municipal Bond | 79 | 0% |

| Infrastructure Debt Fund | 2749 | 0% |

| Bharat Bond ETF | 2312 | 0% |

| InVIT (bonds) | 605 | 0% |

| REIT (bonds) | 957 | 0% |

| REIT (units) | 341 | 0% |

| InVIT (units) | 1504 | 0% |

| Equity | 331972 | 21% |

| Mutual Fund | 23405 | 2% |

| Fixed Deposit | 300 | 0% |

| Current Assets | 28048 | 2% |

| Total | 1554950 |

As on 31st July 2025 – Details of holdings under SCHEME ‘G’ Tier-I

| Parameters / Pension Fund | Axis | Birla | DSP | HDFC | ICICI | Kotak | LIC | SBI | Tata | UTI |

| Central Govt | 3339 | 1388 | 1398 | 33846 | 12404 | 1846 | 5839 | 19647 | 1027 | 2855 |

| State Govt | 538 | 379 | 146 | 7776 | 2257 | 328 | 1397 | 2892 | 280 | 622 |

| Govt. Guaranteed | 3 | 10 | 0 | 950 | 905 | 57 | 75 | 976 | 15 | 26 |

| Mutual Fund | 164 | 130 | 99 | 414 | 316 | 34 | 55 | 854 | 36 | 18 |

| Current Assets | 69 | 33 | 14 | 424 | 141 | 38 | 127 | 469 | 24 | 69 |

| NCD – PSU-PFI | 0 | 0 | 0 | 50 | 267 | 0 | 48 | 0 | 0 | 51 |

| Total AUM | 4113 | 1940 | 1657 | 43460 | 16289 | 2303 | 7542 | 24837 | 1383 | 3641 |

–

| WA. Residual Maturity (yrs) | 20.98 | 17.61 | 23.46 | 27.34 | 24.16 | 26.93 | 21.10 | 21.45 | 26.60 | 17.98 |

| WA. Modified Duration (yrs) | 9.14 | 8.28 | 9.58 | 10.63 | 9.66 | 10.58 | 9.34 | 9.08 | 10.11 | 8.48 |

| WA. Coupon Rate (%) | 6.80 | 6.20 | 6.64 | 6.22 | 6.27 | 6.54 | 7.01 | 6.09 | 6.80 | 6.62 |

| WA. Current YTM (%) | 6.56 | 6.31 | 6.51 | 6.94 | 6.85 | 6.92 | 6.68 | 6.47 | 6.77 | 6.60 |