NFRA’s investigations inter-alia revealed that the MACEL’s Auditor for the FY 2019-20 failed to meet the relevant requirements of the Standards on Auditing (‘SA’ hereafter) in a number of significant aspects and demonstrated a serious lack of competence. The EP failed to exercise professional judgement & skepticism during audit of fraudulent borrowings of Rs. 4,438.37 crore from Banks & Related Parties and its use for fraudulent diversion of Rs. 4,176.67 crore to personal accounts of promoters, their relatives, entities controlled by them and other Related Parties. The EP failed to exercise professional skepticism during audit of Related Party Transactions involving an accounting fraud orchestrated by issue of cheques at the end of FY 2018-19 without adequate bank balance or bank credit limit, with the ulterior motive to conceal huge amount of Related Party balances. These cheques were cleared in the subsequent year i.e., FY 2019-20 by evergreening of loans through structured circular transactions of funds among Coffee Day Group Companies. The EP failed to exercise professional skepticism during the audit of inappropriate recognition of finance cost of Rs 40.47 crores for the borrowings that were not used for any business purpose ofMACEL. The EP failed to perform sufficient and appropriate audit procedure during audit of Cash Flow Statement, which had material misstatement of Rs 1,938.87 crores. The EP failed to evaluate corporate guarantees issued by MACEL and creation of charges on its assets to facilitate borrowings of Rs 130 crores taken by the wife ofV.G. Siddhartha (chairman of CDEL, the listed company of the coffee Day group) and one other related party. Thus, despite material and pervasive misstatement of Rs 10,724.38 crores in the Financial Statements of MACEL, the EP did not report these misstatements.

5 The EP did not report that Internal Financial Control over Financial Reporting was absent, despite pre-signed blank cheques being used by V.G. Siddhartha (‘VGS’ hereafter), who was neither a shareholder nor a director nor an employee ofMACEL, for diversion of funds to other group entities. Besides these, the EP violated a number of Standards on Auditing and Accounting Standards.

6 The EP contended that she became aware of the possible financial mismanagement only after learning about the death of VGS (in July 2019) and the contents of the letter he left behind. Consequent to that she had issued Disclaimer of Opinion indicating non recoverability of advances made by MACEL. The Standards on Auditing do not absolve an Auditor from the responsibility of reporting other misstatements once a disclaimer on a particular aspect is given. It was found that the EP had failed in her statutory duty and had tried to hide behind one disclaimer of opinion, which itself was incomplete as she did not cover all aspects of infraction of the Laws and the Standards.

7 Based on investigation and proceedings under section 132 (4) of the Companies Act and after giving her opportunity to present her case, NFRA has found the EP – CA Lavitha Shetty, guilty of professional misconduct and imposes through this Order the following monetary penalties and sanctions that will take effect after a period of 30 days from issuance of this Order:

a) Imposition of a monetary penalty of Rs Ten Lakhs;

b) Debarment for a period of Ten years from being appointed as an auditor or internal auditor or from undertaking any audit in respect of financial statements or internal audit of the functions and activities of any company or body corporate. The first five years out of the ten years debarment ordered, would run concurrently with the period of debarment ordered vide NFRA order dated 13.04.2023 in the case of CA Lavitha Shetty.

Government of India

National Financial Reporting Authority

*****

7th Floor, Hindustan Times House,

Kasturba Gandhi Marg, New Delhi

Order No. NF-23/14/2022 Dated: 25.04.2023

In the matter of CA Lavitha Shetty under Section 132(4) of the Companies Act 2013

1 This Order disposes of the Show Cause Notice (‘SCN’ hereafter) number- NF-23/14/2022 dated 10th November 2022, issued to CA Lavitha Shetty, proprietor of M/s Lavitha & Associates (ICAI Firm registration no. 011882S), Chikkamagaluru, who is a member of the Institute of Chartered Accountants of India (‘ICAI’ hereafter) and was the Engagement Partner (‘EP’ or ‘Auditor’ hereafter) for the statutory audit of Mysore Amalgamated Coffee Estates Limited, (‘MACEL’ or ‘the company’ hereafter) Chikkamagaluru, for the Financial Year (‘FY’ hereafter) 2019-20.

2 This Order is divided into the following sections:

A. Executive Summary.

B. Introduction & Background.

C. Major lapses in audit of fraudulent borrowings, diversion of funds, evergreening of loans and related matters.

D. Other non-compliances with Laws and Standards.

E. Omissions and commissions by the Audit Firm.

F. Articles of Charges of Professional Misconduct by the Auditor.

G. Penalty & Sanctions.

A. EXECUTIVE SUMMARY

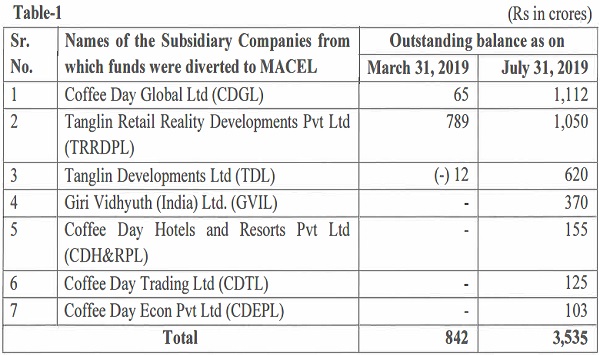

3 Pursuant to Securities and Exchange Board of India (‘SEBI’ hereafter) sharing in April 2022 its investigation regarding diversion of Rs 3,535 crores from seven subsidiary companies of Coffee Day Enterprises Limited (‘CDEL’ hereafter), a listed company, to Mysore Amalgamated Coffee Estate Limited (‘MACEL’ or ‘the company’ hereafter), an entity owned and controlled by the promoters ofCDEL, NFRA initiated investigations under Section 132(4) of the Companies Act 2013 (‘the Act’ hereafter).

4 NFRA’s investigations inter-alia revealed that the MACEL’s Auditor for the FY 2019-20 failed to meet the relevant requirements of the Standards on Auditing (‘SA’ hereafter) in a number of significant aspects and demonstrated a serious lack of competence. The EP failed to exercise professional judgement & skepticism during audit of fraudulent borrowings of Rs. 4,438.37 crore from Banks & Related Parties and its use for fraudulent diversion of Rs. 4,176.67 crore to personal accounts of promoters, their relatives, entities controlled by them and other Related Parties. The EP failed to exercise professional skepticism during audit of Related Party Transactions involving an accounting fraud orchestrated by issue of cheques at the end of FY 2018-19 without adequate bank balance or bank credit limit, with the ulterior motive to conceal huge amount of Related Party balances. These cheques were cleared in the subsequent year i.e., FY 2019-20 by evergreening of loans through structured circular transactions of funds among Coffee Day Group Companies. The EP failed to exercise professional skepticism during the audit of inappropriate recognition of finance cost of Rs 40.47 crores for the borrowings that were not used for any business purpose of MACEL. The EP failed to perform sufficient and appropriate audit procedure during audit of Cash Flow Statement, which had material misstatement of Rs 1,938.87 crores. The EP failed to evaluate corporate guarantees issued by MACEL and creation of charges on its assets to facilitate borrowings of Rs 130 crores taken by the wife ofV.G. Siddhartha (chairman of CDEL, the listed company of the coffee Day group) and one other related party. Thus, despite material and pervasive misstatement of Rs 10,724.38 crores in the Financial Statements of MACEL, the EP did not report these misstatements.

5 The EP did not report that Internal Financial Control over Financial Reporting was absent, despite pre-signed blank cheques being used by V.G. Siddhartha (‘VGS’ hereafter), who was neither a shareholder nor a director nor an employee ofMACEL, for diversion of funds to other group entities. Besides these, the EP violated a number of Standards on Auditing and Accounting Standards.

6 The EP contended that she became aware of the possible financial mismanagement only after learning about the death of VGS (in July 2019) and the contents of the letter he left behind. Consequent to that she had issued Disclaimer of Opinion indicating non recoverability of advances made by MACEL. The Standards on Auditing do not absolve an Auditor from the responsibility of reporting other misstatements once a disclaimer on a particular aspect is given. It was found that the EP had failed in her statutory duty and had tried to hide behind one disclaimer of opinion, which itself was incomplete as she did not cover all aspects of infraction of the Laws and the Standards.

7 Based on investigation and proceedings under section 132 (4) of the Companies Act and after giving her opportunity to present her case, NFRA has found the EP – CA Lavitha Shetty, guilty of professional misconduct and imposes through this Order the following monetary penalties and sanctions that will take effect after a period of 30 days from issuance of this Order:

a) Imposition of a monetary penalty of Rs Ten Lakhs;

b) Debarment for a period of Ten years from being appointed as an auditor or internal auditor or from undertaking any audit in respect of financial statements or internal audit of the functions and activities of any company or body corporate. The first five years out of the ten years debarment ordered, would run concurrently with the period of debarment ordered vide NFRA order dated 13.04.2023 in the case of CA Lavitha Shetty.

B. INTRODUCTION & BACKGROUND

8 The National Financial Reporting Authority is a statutory authority set up u/s 132 of the Companies Act 2013 (‘Act’ hereafter) to monitor implementation and enforce compliance of the auditing and accounting standards and to oversee the quality of service of the professions associated with ensuring compliance with such standards. NFRA has the powers of a civil court and is empowered u/s 132 ( 4) of the Act to investigate into professional and other misconducts of auditors of the prescribed classes of companies1 and impose penalty for proven professional or other misconduct of the individual members or firms of Chartered Accountants.

9 The Statutory Auditors, individuals and firms of Chartered Accountants, are appointed by the members of companies as per the provisions of section 139 of the Act. The Statutory Auditors, including the Engagement Partners and the Engagement Team that conduct the Audit are bound by the duties and responsibilities prescribed in the Act, the Rules made thereunder, the Standards on Auditing (‘SA’ hereafter), including the Standards on Quality Control (‘SQC’ hereafter) and the Code of Ethics, the violation of which constitutes professional misconduct, and is punishable with penalty prescribed u/s 132 (4) (c) of the Act.

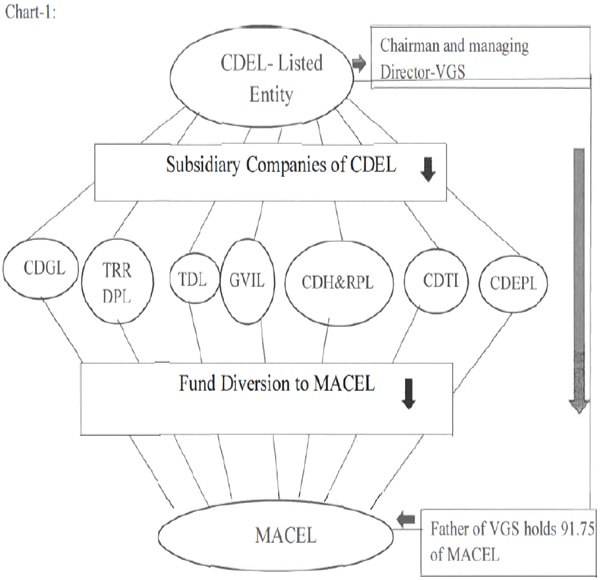

10 On receipt of information from SEBI vide letters dated 01.04.2022 & 29.04.2022 sharing its investigation regarding diversion of funds worth Rs 3,535 crores (as on 31-07-2019) from seven subsidiary companies of Coffee Day Enterprises Limited, a listed company, to Mysore Amalgamated Coffee Estate Limited, an entity owned and controlled by the promoters of CDEL, NFRA started investigation into the role of the statutory auditor under section 132 (4) of the Companies Act 2013.

11 Late V. G. Siddhartha was Chairman & Managing Director of CDEL till 29.07.2019. VGS and his family reportedly owned around 10,000 acres of coffee estates through various entities owned by VGS and operated and managed by MACEL. Out of total acreages of coffee estates owned by the group, MACEL owned 578 acres of coffee plantations and 91.75% shares of MACEL were held by Late S.V. Gangaiah Hegde, the father ofVGS.

12 As per the investigations made by SEBI, the outstanding balance payable by MACEL to subsidiary companies of CDEL was Rs 842 crores as on 31 March 2019, which had increased to Rs 3,535 crores on 31 July 2019, detailed as under in Table 1- 1 Rule 3 of The NFRA Rules 2018.

13 The linkage of the entities described in above Table is depicted in the chart given below: Chart-1:

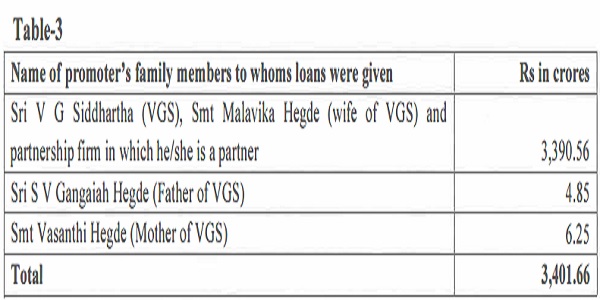

14 As per the Financial Statement of MACEL, funds were further transferred from MACEL to the personal accounts of VGS, his relatives and entities controlled by him and/or his family members, whose outstanding balances receivable by MACEL were Rs 3,401.66 crores as on 31-03-2020. On examination of Financial Statement of MACEL, it transpired that MACEL did not have any business transaction with 6 of the 7 subsidiary companies of CDEL except CDGL; and that MACEL was used as a conduit to fraudulently transfer funds from the subsidiary companies of CDEL to the personal accounts of VGS, his relatives and entities controlled by him and/or his family members, as loans and advances that were never returned to MACEL/CDEL.

14 As per the Financial Statement of MACEL, funds were further transferred from MACEL to the personal accounts of VGS, his relatives and entities controlled by him and/or his family members, whose outstanding balances receivable by MACEL were Rs 3,401.66 crores as on 31-03-2020. On examination of Financial Statement of MACEL, it transpired that MACEL did not have any business transaction with 6 of the 7 subsidiary companies of CDEL except CDGL; and that MACEL was used as a conduit to fraudulently transfer funds from the subsidiary companies of CDEL to the personal accounts of VGS, his relatives and entities controlled by him and/or his family members, as loans and advances that were never returned to MACEL/CDEL.

15 The modus operandi of the alleged diversion of funds discovered during SEBI investigation was that “VGS used to ask the Authorised Signatories to sign bunch of cheques which was kept in his possession and used them as and when required”. Such pre- signed blank cheques of bank accounts of various Coffee Day Group companies were used for the diversion of funds.

16 M/s Lavitha & Associates is a proprietary firm registered with ICAI carrying on the profession of chartered accountancy from Chikkamagaluru city in the state of Karnataka. The Audit Firm was statutory auditor of MACEL for FY 2019-20 and 2018-19 and Ms Lavitha Shetty was Engagement Partner (`EP’ hereafter) for this audit engagement. The Firm was also statutory auditor of Coffee Day Hotels & Resorts Private Limited (CDH&RPL) for FY 2019-20 and Rs 155 crores was diverted from CDH&RPL to MACEL during FY 2019-20. NFRA vide its order dated 13.04.2023 has held Ms Lavitha Shetty guilty of professional misconduct for the audit of MACEL for the FY 2018-19.

17 This Order deals with the role of the Auditor ofMACEL, which was owned by father ofVGS (the then Chairman & Managing Director of CDEL). MACEL is engaged in agricultural activities in the state of Karnataka, India. MACEL had around 578 acres of Coffee plantations besides some plantations of Paper, Areca etc. It has office at Chikkamgaluru, a district headquarters in Kamataka.

18 Rule 3 of The National Financial Reporting Authority Rules 2018 (‘NFRA Rules 2018’ hereafter) lists out the classes of companies and body corporates governed by NFRA. This includes unlisted Public Companies having paid-up capital of not less than rupees five hundred crores or having annual turnover of not less than rupees one thousand crores or having, in aggregate, outstanding loans, debentures and deposits of not less than rupees five hundred crores as on the 31st March of the immediately preceding financial year. MACEL is an unlisted Public Company having borrowings of Rs 4,112.47 crores as on 31-03-2019, therefore, it falls under the jurisdiction of NFRA for the FY 2019-20 and and its financial statements are to be prepared in accordance with Accounting Standards and the relevant Laws.

19 NFRA called from the statutory auditor the Audit File for the audit of Financial Statements (‘FS’ hereafter) of MACEL for Financial Year 2019-20 to examine the role of the auditor and for investigation under section 132(4)(b)(i) of the Act. Based on an examination of the Audit File and other materials on record, NFRA issued a Show Cause Notice (‘SCN’ hereafter) on 10.11.2022 asking the Statutory Auditor (EP) to show cause by 10.12.2022 why penal provisions of section 132(4)(c) of the Companies Act 2013 should not be invoked for professional misconduct of:

a) Failure to disclose a material fact known to the EP which is not disclosed in a financial statement, but disclosure of which is necessary in making such financial statement where the Statutory Auditor is concerned with that financial statement in a professional capacity.

b) Failure to report a material misstatement known to the EP to appear in a financial statement with which the Statutory Auditor are concerned in a professional capacity.

c) Failure to exercise due diligence and being grossly negligent in the conduct of professional duties.

d) Failure to obtain sufficient information which is necessary for expression of an opinion or its exceptions are sufficiently material to negate the expression of an opinion, and

e) Failure to invite attention to material departure from the generally accepted procedures of audit applicable to the circumstances.

20 After availing extension of time, the EP vide letter dated 03.01.2023 submitted reply to SCN.

21 The SCN also gave an opportunity of personal hearing to the EP, which she did not avail. Accordingly, this Order is based on examination of the facts of the matter, charges in the SCN, written replies of the EP and other materials available on record.

C. MAJOR LAPSES – FAILURE IN AUDIT RELATING TO FRAUDULENT DIVERSION OF FUNDS AND RELATED MATTERS

Examination of General submission by the EP

22 The EP has stated in preliminary submission that she had issued a ‘Disclaimer of Opinion’ in accordance with SA 705, Modifications to the Opinion in the Independent Auditor’s Report. While inviting attention to para 9 of this SA, which states ‘A disclaimer of audit opinion is issued when an auditor is unable to obtain sufficient appropriate audit evidence, to form the basis of an audit

opinion, and at the same time believes that the possible effects on the financial statements of undetected misstatements, if any, could be both material and pervasive’, she replied that the Audit Report issued by her had unequivocally communicated that the Financial Statements of MACEL for FY 2019-20, attested by her, contained possible material and pervasive misstatements, but specifics of which were not possible to be determined for absence of audit evidences and hence a disclaimer of opinion was given. While drawing attention to para A 7 of SA 230, Audit Documentation, which provides that it is neither necessary nor practical to document every matter considered, or professional judgement made, in an audit, she argued that where an auditor has issued a disclaimer of audit opinion, no further audit documentation is necessary to prove whether the Auditor had undertaken due process to arrive at her view.

23 The EP further replied that in the ‘Basis of disclaimer of opinion’ section of the Independent Auditor’s Report, she had drawn attention to note no-19 of the Financial Statements that sufficient appropriate audit evidence could not be obtained to enable her taking a view over the recoverability of the advances worth Rs 3401.66 crores from Late V G Siddhartha, his associated entities and relatives. She argued that once an auditor concludes after assessing the possibility of Risk of Material Misstatement (‘RoMM’ hereafter) with respect to a significantly material line items in the Financial Statements, then there is no need for the Auditor to carry out any further examination of any of the other line items in the same Financial Statements, because such an examination is inconsequential, and the audit opinion would always remain a ‘disclaimer of audit opinion’ in all circumstances. She further replied that when the audit opinion issued was an ‘expression of inability to issue an audit opinion’, the Auditor is not accountable for any other elements in the Financial Statements, whether present or missing.

24 We have considered this submission. As per para 27 of SA 705, the Auditor is required to report all matters having material effect on the financial statements as it states that “Even if the auditor has expressed an adverse opinion or disclaimed an opinion on the financial statements, the auditor shall describe in the basis for opinion section the reasons for any other matters of which the auditor is aware that would have required a modification to the opinion, and the effects thereof’. Its explanatory material at para A24 further explain this matter as “An adverse opinion or a disclaimer of opinion relating to a specific matter described within the Basis for Opinion section does not justify the omission of a description of other identified matters that would have otherwise required a modification of the auditor’s opinion. In such cases, the disclosure of such other matters of which the auditor is aware may be relevant to users of the financial statements”. 2 Thus it is very clear that in case an auditor gives disclaimer of opinion for one matter, it does not mean that the auditor will be free of responsibilities for other unreported material deficiencies/ misstatements in the financial statements. It is important that the Auditors report all material misstatements so that the impact of all misstatements on the financial statements is known and the users of financial statements are not under the misleading impression that the financial statements carry only the reported misstatements. Therefore, we cannot accept this submission of the EP.

C. Failure in understanding the nature of business of MACEL resulting in lapses in audit of diversion of funds

25 The EP was charged3 with failure to obtain an understanding of the nature of MACEL, including its operations, its ownership and governance structures, the types of investment the entity was making and how it was financed, in order to understand the classes of transactions and account balances. She was also charged with failure to exercise Professional Judgment and Professional Skepticism in planning and performing audit of Financial Statements as required by SA 2004• Had the EP obtained an understanding of MACEL, exercised Professional Judgment & Professional Skepticism, and performed sufficient appropriate audit procedure, she would have detected and reported material and pervasive misstatements in the financial statements worth Rs 4,176.67 crores on Assets side of the Balance Sheet and Rs 4438.37 crores on the Liability side of the Balance Sheet. These misstatements were a result of fraudulent borrowing mainly from related parties, which were used for fraudulent lending to promoters, their family members and entities owned/controlled by them.

26 The SCN noted that MACEL received funds from seven subsidiary companies of CDEL despite the fact that it did not have any business relationship with six of these seven subsidiary companies except CDGL, the sole buyer of coffee beans produced by MACEL. As per the Financial Statements of MACEL, its borrowings of Rs 4,479.79 crores constituted 99.94% of total liabilities of Rs 4,482.40 crores, while 99.01 % of its total assets of Rs 4,218.09 crores were the loans & advances given worth Rs 4,176.67 crores. While MACEL had meagre Revenue from Operations of Rs 3.27 crores & Other Income of Rs 0.15 crores only, its Finance cost was Rs 40.4 7 crores which constituted 91.89% of the total cost of Rs 44.04 crores. The loss incurred by MACEL during the year was Rs 40.62 crores and MACEL had a negative Net worth of Rs 264.32 crores. All the above stated borrowings (except bank borrowings of Rs 160.02 crores) and lending ofMACEL were interest free, payable on demand and not supported by any contract/agreement.

27 The Financial Statements, according to the SCN, indicated that the majority of the related party borrowings was froni subsidiary companies of CDEL (Table 2) and was further diverted to the personal accounts of the Promoters, their family members and entities controlled by them (Table 3).

|

Loans from subsidiary companies of CDEL (Related Parties) taken by MACEL |

||

| Sr No | Name of company from whom loans were taken | Total outstanding as on 31.03.2020 |

| 1 | Tanglin Retail Realty Development Pvt Ltd | 1,050.31 |

| 2 | Coffee Day Global Ltd | 1,084.01 |

| 3 | Tanglin Development Ltd | 607.54 |

| 4 | Coffee Day Trading Ltd | 125.00 |

| 5 | Day Hotels & Resorts Pvt Ltd | 136.96 |

| 6 | Giri Vidhyut (India) Ltd | 370.00 |

| 7 | Coffee Day Econ Pvt Ltd | 103.20 |

| Total | 3,477.02 | |

28 According to the SCN, it can be observed from Tables-2 and 3 above that the loans & advances taken by MACEL were not for the business activities of the company but for onward lending to the related parties. Out of the total assets of Rs 4,218.09 crores, only Rs 41.42 crores appeared to have been used for business activity and remaining Rs 4,176.67 crores (99.01 %) was diverted as Loans & advances, resulting in material and pervasive misstatement on the Assets side of the Balance Sheet5. Similarly, out of the total Liabilities of Rs 4,482.40 crores, borrowings were Rs 4,479.79 crores (99.94%). Keeping in view that the assets of only Rs 41.42 crores appeared to have been used for business activity, the rest of the borrowings of Rs 4,438.37 crores (Rs 4,479.79 crore Rs 41.42 crore ), i.e., 99 .07% of total borrowings were used for diversion of funds, resulting in material and pervasive misstatement on the Liability side of the Balance Sheet. There was no business rationale in such borrowing and lending transactions and MACEL was used mainly to create an intermediate layer with the ulterior motive to mislead stakeholders and regulators while fraudulently diverting funds to personal accounts of promoters, their relatives and entities controlled by them.

29 The SCN noted that SA 200 requires an auditor to exercise professional judgement and skepticism while planning and performing audit. Para 5 of SA 315 requires an Auditor to perform risk assessment procedures to identify and assess Risk of Material Misstatements (‘RoMM’ hereafter). As per para 5 of SA 330, the Auditor was required to respond to the assessed RoMM. SA 240 prescribes an Auditor’s responsibilities relating to fraud in audit of Financial Statements. Para 10 of SA 240 provides that the objectives of an auditor are to identify and assess the RoMM in the Financial Statements due to fraud, obtain audit evidence and respond to identified or suspected risk. Para 12 of SA 240 requires the auditor to maintain professional skepticism recognizing the possibility of existence of material misstatement due to fraud. Para 32(c) of SA 240 requires the auditor to evaluate the business rationale ( or lack thereof) of the significant transactions that are outside the normal course of business or otherwise appear unusual and evaluate whether such transactions may have been entered into to engage in fraudulent financial reporting or to conceal misappropriation of funds. While the financials of MACEL indicated that it had abnormally high amounts of transactions in loans and advances and balances with Related Parties, which was outside the normal course of business of the company and presented strong indicators that MACEL was being used by the promoters for diversion of funds from subsidiary companies of CDEL to promoters, their family members and entities controlled by them, there was no evidence to indicate that the EP had performed the basic audit procedure to understand the nature of business of MAC EL, and to identify and respond to RoMM due to fraudulent diversion of funds. The SCN charged that the EP failed to comply with SA 200, SA 240, SA 315 & SA 330.

30 The SCN noted that the Director of MACEL admitted on 30.05.2019 (letter available in the Audit File of 2018-19) that funds were received from group entities for development and maintenance of coffee plantations, which were payable on demand but no agreements had been signed. She also admitted that loans and advance given to group entities were payable on demand, that no agreements were signed and that the account of the group was being maintained as a running account. These admissions together with the financial information in Table-3 were strong indicators of fraudulent diversion of funds. Had the EP applied professional judgment and skepticism to the admitted facts that no agreements were signed for the financial arrangements involving substantial funds, huge loans were payable on demand and that the group accounts were maintained as running accounts, she could have found the material misstatements and fraud. Therefore, the EP was charged with failure to exercise due diligence in evaluating the said Management letter during audit of the Financial Statements for FY 2019-20.

31 The SCN stated that the EP’s lack of due diligence was also a violation of Section 143 (12) of the Act under which she had the Statutory duty to report an offence of fraud to the Central Government. However, she reported6 that no material fraud by or on the company had been noticed or reported during the course of audit. It was also a violation of the Companies (Auditors Report) Order 2016 (‘CARO’ hereafter), as she ignored the strong indicators of fraud including the receipt and disbursal of loans and advances without any business rationale, complete absence of internal control and violation of the provisions of the Act.

32 As per the Audit File for FY 2018-19, MACEL, in its extraordinary general meeting held on 13.02.2019, had passed two special resolutions authorizing the Board of Directors to borrow up to Rs 6,000 crores under section 180(1)(c) of the Act and to make investment and grant loans up to Rs 6,000 crores under section 186 of the Act. As per section 179 of the Act, while the Board of Directors has powers to borrow funds and grant loans, there is no evidence in the Audit File that the Board of Directors had approved any resolution for borrowing and giving funds as loans and advances, as required under section 179(3) of the Act. The EP was accordingly charged for not verifying whether MACEL had complied with provisions of section 179(3) of the Act.

33 Diverting funds fraudulently to personal accounts of VGS, his relatives and entities controlled by him and/or his family members is covered in section 420 of the Indian Penal Code 7, which is a predicate offence for money laundering under section 3 of the Prevention of Money Laundering Act 2002 (PMLA)8. As the EP did not report this violation in the Independent Auditor’s Report and also did not consider its impact on the Financial Statements while making audit conclusions she was charged with violating SA 250 – ‘Consideration of Laws and Regulations in an Audit of Financial Statements’.

Reply of the EP

34 While denying the charge, the EP has replied that she had issued a ‘disclaimer of opinion’, which is evidence that she had exercised professional judgement and professional skepticism. Accordingly, there was no noncompliance with SA 200. She further replied that during the audit of FY 2018-19, she had no occasion to suspect that anything was amiss in the functioning of MACEL because the management actions were professional and under the control and overall supervision of the shareholders. Therefore, she issued an unmodified audit report with an Emphasis of Matter paragraph over ‘going concern assumption’. However, during FY 2019-20, VGS passed away leaving behind a note that he had not disclosed many facts about the financial mess of the group to anyone including the Auditors. According to the EP, based on that information, she changed her view during FY 2019-20 and issued a disclaimer of audit opinion. She also stated that the borrowings and advances made as appearing in financial statements of FY 2019-20 were the effect of the carried over numbers of FY 2018-19 and that ‘Additional transactions on FY 2019-20 were collateral and rotational effects’.

35 In respect of compliance with SA 200 and SA 315, the EP replied that advancing of huge amounts to related parties and consequent outstanding balances as reflected in the Financial Statements did not pose any risk of material misstatement as these were the effect of actual transactions. The EP replied that she obtained a fair knowledge of the entity, its environment, financial reporting system and internal controls during the Audits of earlier years. She claimed to have performed risk assessment procedure as recorded at page 157-158 of the Audit File forming part of annexure to SCN and that her assessment of internal finance control policy was available on page 181-182 of the Audit File forming part of annexure to SCN. She further replied that the transactions happened during FY 2018-19, and were not outside the normal course of business as she did not suspect the explanation given by management that promoters were looking after about 10000 acres of coffee estates and the advances in question were in furtherance of their coffee business. She stated that the money received from the subsidiary companies of CDEL, and advances granted to accounts of promoters were to achieve this objective. However, during FY 2019-20, from the note of VGS, she realized that the explanations given about the objective of the advances were perhaps not true. Suspecting doubt in recoverability of advances and absence of proper audit evidence, she gave a disclaimer of opinion, which was evidence of her compliance with SA 200, SA 315 and SA 330.

36 While not disputing the facts given in Tables 2 and 3 regarding borrowings and advances made to Related Parties, the EP replied that she would not be able to agree or disagree with the narratives used in SCN that funds were diverted to personal accounts of promoters because such findings can emerge only from an investigation and are not capable of being detected within the scope of work of a Statutory Auditor.

37 While responding to the charge relating to failure to verify whether borrowings & lending were approved by the Board of Directors in accordance with section 179(3) of the Act, she replied that there is no reporting obligation on an Auditor under section 179(3) and section 180 of the Act and also stated that:

“Kindly appreciate that the financial statements that are duly approved by the Board of Directors of the company is the evidence that all the transactions in it including the loans and advances both as assets and liabilities have the stamp of approval of the Board of Directors”.

38 Responding to the charge relating to noncompliance with SA 240, the EP replied that borrowings and lending were for furtherance of business interest of MACEL and were not outside the normal course of business, thus they do not constitute fraud and misappropriation of funds There was no error or omission in the presentation of transactions in the Financial Statements. The EP further replied that the cash flow management was under the control of VGS. One can criticize it as poor corporate governance but does not make a case of fraudulent acts. The EP further stated that the absence of agreements for advances given, does not make out a case of transactions given with fraudulent intentions. MACEL was in a liquidity trap and recovery of advances made was doubtful, therefore she had given disclaimer of opinion.

39 Responding to the charge relating to noncompliance with section 143(12) of the Act, the EP replied that no investigating agency has termed these transactions as fraudulent and she had no doubt about the sincerity of purpose of the Management of CDEL. There was no misappropriation of assets, no falsification of accounts and no concealment of any transactions in the Financial Statements, therefore she did not suspect any fraud or misappropriation of funds and it was a false allegation that the EP knew that funds were being diverted to personal accounts of promoters. She further stated that an Auditor is not skilled to detect fraud; and that VGS, holding 91 % shares, carried out the transactions, and hence the issue was not about absence of internal control.

40 Responding to the charge relating to violation of PMLA, the EP replied that she had no knowledge that these transactions were fraudulent diversion of funds; and that there were no findings by any authority that such transactions fell within the definition of section 420 ofIPC or section 3 of PMLA.

Analysis of reply

41 We observe that MACEL’s revenue from operations was Rs 3.27 crores in 2019-20, it had tangible assets of Rs 41.42 crores and negative net worth of Rs 264.32 crores. It did not have any expansion plan. From these numbers it would be evident to any prudent person that a company like MACEL did not need huge borrowings of 4,479.79 crores and lending of Rs 4,176.67 crores for its business. The EP has confessed that during the Audit for FY 2018-19 she had completely relied upon the explanations given by the Management that huge amounts of borrowings from related parties and lending to related parties were for furtherance of coffee business of associated entities. MACEL was not a financial institution, therefore routing of such huge amounts through it cannot be termed to be in the ordinary course of business ofMACEL, as it did not have any business relationship with such associated entities from which it received and to which it lent money. Therefore, before relying on the management explanation, the EP was required to evaluate the business purpose behind such huge borrowing and lending transactions ofMACEL with related parties. But this was not done.

42 On compliance with Section 179(3) of the Act, we find that the section empowers the Board of Directors (Board) to exercise powers relating to borrowing and lending of money, by means of resolutions passed in meetings of the Board. Mandatory provision of passing a resolution at meetings of the Board shows the importance of these transactions in the operations of a company. The obvious purpose of making such a provision, is to ensure that no unauthorized borrowings and lending is entered into by the management. In this case the EGM authorised the Board to take decisions on borrowings and lendings up to a monetary limit. This empowered the Board to pass resolutions for transactions within the set limit. But the Board passed no resolution authorising the said transactions, thus rendering the transactions in question as unauthorised. Further, section 179(3) of the Act is independent of section 134( 1) of the Act which inter alia provides that financial statements shall be approved by the Board of Directors. The reply of the EP that the approval of financial statements by the Board of Directors (done under section 134(1) of the Act) is evidence that all the transactions in it have the stamp of approval of the Board of Directors, is astonishing. This shows a total lack of understanding of what an ‘authorisation of transaction’ by the Board means. Such a flawed understanding by the EP, who is entrusted to check adherence to Standards and the Laws, is alarming and disconcerting. It appears that the EP has furnished this absurd reply to cover up her deficiency during performance of Audit of MACEL.

43 It is an undisputed fact that all the loans and advances were without any written Contract/ Agreement and were repayable on demand. There is no material on record to show whether any Security was obtained before giving such huge amounts of loans/advances. Despite knowing these adverse indicators, the EP did not evaluate the business rationale of these huge transactions with related parties. Needless to say, every Auditor should be aware that Related Party Transactions have a high potential of misuse/misstatement, as is also reflected in the special provisions in law to monitor and regulate them.

44 Based on above analysis, we find that funds were fraudulently borrowed from subsidiary companies of CDEL with the ulterior motive to fraudulently divert such funds to the personal accounts of promoters, their family members and entities owned/controlled by them.

45 The Audit work papers quoted by the EP have been perused. On verification of page 157 of the Audit File forming part of annexure to SCN, we see that it is a statement prepared by MACEL containing some basic details about the company like nature of business and operational heads of the company. Page 158 is a statement prepared by MACEL regarding assessment ofrisk in the area of sales, purchase, estate works and bank accounts. These documents do not contain any details about any risk assessment procedure performed by the EP. Page 181 and 182 are the Internal Financial Control Policy prepared by MACEL containing high level general information about separation of duties, authorization & approval, custodial & security arrangement and review & reconciliation. No specific information about these areas is mentioned. The EP has not evaluated these documents. Therefore, the contention of the EP of having performed risk assessment procedure is factually incorrect. Further, the EP’s statement that she changed her view about the company and issued the disclaimer of opinion on learning about the financial mess in the group after the unfortunate death of VGS, is an admission that prior to the death of VGS, she relied on the explanation of the management and did not perform any audit procedure to identify, assess and respond to Ro MM due to fraud. Surprisingly, even after knowing about financial mess in the company, she did not report this fraudulent diversion of funds in the ‘Basis of disclaimer of opinion’ section of her Independent Auditor’s Report. With reference to her reply that diversion of funds can emerge only from an investigation and is not capable of being detected by a statutory auditor, as detailed and analyzed above, we find that the diversion of funds was evident from the Financial Statements and other information accessible to the EP. Accordingly, we find that the EP did not comply with SA 200, SA 240, SA 315 and SA 330.

46 In respect of noncompliance with section 143(12) of the Act relating to non- reporting of fraud to the Central government, the reply of the EP that no agency had termed the said transactions as fraudulent, is misplaced. The findings of an Auditor are not dependent on findings of any other agency and should be the outcome of the Auditor’s professional skepticism which was totally lacking in this case. The EP failed to detect the fraud that was apparent and failed to report it to the Government oflndia thus violating section 143(12) of the Act. The EP has also violated CARO, as she reported that no fraud was noticed during the course of audit.

47 In respect of the EP’s reply regarding violation of PMLA, that as per her knowledge, these transactions were not fraudulent and there is no finding by any authority that such transactions fall within the definition of section 420 of IPC or section 3 of PMLA, we note that the fraudulent diversion of funds was apparent from the Bank Statements and from the Financial Statements itself, and was in the knowledge of the EP. After the death ofVGS (in July 2019) the fraud was clearly in the know of the EP, but she chose to remain silent. Diversion of funds to personal accounts of promoters, their relatives and entities owned/controlled by them is clear proof of cheating and dishonesty, and thus falls under section 420 ofIPC and section 3 of PMLA. We find that the EP has failed to report this violation in the audit report, thus violating SA 250.

48 The Auditor should know, amongst other things, that gaining an understanding of the business purpose of such transactions and examination of the agreements, contracts, and other transactionrelated documents is primary to any audit. There is no audit evidence to support a valid understanding of the business and the business purpose for huge borrowing and lending transactions. Even when there were circumstances warranting increased scrutiny and facts strongly suggesting fraud, magnified after the death of V GS, the EP failed to perform any additional auditing procedures. This indicates that the EP did not exercise the necessary professional skepticism to determine whether these transactions posed a risk of material misstatement due to fraud.

49 In view of above analysis, we find that this charge is proved that the EP has violated section 143(12) of the Act, CARO, SA 200, SA 240, SA 250, SA 315, SA 330 and failed to report violation of section 179(3) of the Act by MACEL.

50 We note that PCAOB9, the US regulator, in a similar matter of diversion of funds to a related party, observed that “The transactions between one of the Issuer’s wholly-owned Chinese subsidiaries (“Subsidiary”) and a Chinese purchasing agent (“Agent”) involved the Subsidiary’s transfers of loan proceeds to the Agent as prepayments to buy equipment and materials that the Agent never delivered. The loans were obtained from Chinese lenders for the purpose of making these purchases. While the Agent returned a portion of the prepayments some in unusual same-day, round-trip transfers it did not return most of them”…. “By failing to adequately respond to the known fraud risks, Marcum ‘s engagement team breached its duty to perform the Audits with the due professional care and professional skepticism required by PCAOB standards. The team also failed to adequately understand the business rationale (or the lack thereof) for the significant unusual transactions and failed to obtain sufficient appropriate audit evidence to support Marcum ‘s opinion on the Issuer’s financial statements”. For this misconduct, PCAOB censured Marcum LLP (“Marcum”); imposed a civil money penalty of $250,000, prohibiting Marcum, for a period of three years from issuing an audit report for an issuer client with substantially all of its operations in the People’s Republic of China; and requiring Marcum to undertake a review of its quality control policies and procedures regarding initial acceptance of, and audits performed for, certain issuer clients.

C2. Failure to detect evergreening of loans through structuring circular transactions of funds

51 The EP was charged with failure to perform risk assessment procedures to identify and assess Risk of Material Misstatements due to fraud and failure to exercise professional skepticism while performing audit of related party transactions. Evergreening of loans through structured circular transactions of funds, was evident on analysis of cheques issued and received by MACEL in FY 2018-19 but debited and credited in FY 2019-20. Banks-wise details are given in subsequent paras.

Karnataka Bank

52 On 30.03.2019 MACEL issued six cheques for total amount of Rs 105.00 crores favoring CDGL. On 04.04.2019 the account received Rs 22.70 crores from MACEL’s own bank ale in Yes Bank. This was followed by a series of circular transactions, on the same day, between MACEL and CDGL, starting with MACEL paying Rs 20 crores to CDGL, followed by CDGL paying the same amount to MACEL and so on for clearance of the above referred six cheques issued on 30.3.2019.

53 On 10.04.2019, MACEL received Rs 90 crores from CDGL which again started a series of payments on the same day in a circular manner for clearance of four cheques of total amount of Rs 350 crores issued to TDL on 31.03.2019 & eight cheques of total amount of Rs 650 crores issued to TRRDPL on 30.03.2019. For example, Rs 90 crores received from CDGL was paid by.. MACEL to TDL, which then paid Rs 90 crores to GVIL, which then paid Rs 90 crores to MACEL, which then paid Rs 50 crores to GVIL, which then paid Rs 50 crores. to MACEL, which then paid Rs 90 crores to TDL, which then paid Rs 90 crores to GVIL, which then paid Rs 90 crores to MACEL, which then paid Rs 90 crores to TDL, which then paid Rs 90 crores to GVIL, which then paid Rs 90 to MACEL, which then paid Rs 90 crores to TRRDPL, thereafter Rs 90 crores was paid by TDL to MACEL, which then paid Rs 80 crores to TDL, and so on …..

54 On 10.05.2019 MACEL got Rs 10 crores from its own bank ale with Corporation bank, which again started a series of sham circular payments on the same day for clearance of five cheques of total amount of Rs 50 crores issued to GVIL on 30.03.2019. For example, Rs 10 crores was paid by MACEL to GVIL, which then paid Rs 10 crores to MACEL, which then paid Rs 10 crores to GVIL and so on….. Further, in the bank statement there are 35 entries on date 10.05.2019, each for Rs 10 crores, for payment to GVIL as well as receipt from GVIL in a circular manner.

Corporation Bank

55 MACEL issued five cheques of Rs 25 crores each (total Rs 125 crores) in FY 2018-19 to CDTL, which were cleared on 10.04.2019 through a series of sham transactions in a circular manner with the credit balance of Rs 25.07 crores only by rotating funds between MACEL and CDTL in five circular transactions of Rs 25 crores each.

56 On 26.04.2019, MACEL received Rs 20 crores from CDGL which started a series of sham payments on the same day for clearance of six cheques totaling Rs 131.20 crores by circulating the funds amongst MACEL, Gonibedu Coffee Estates Pvt Ltd (‘Gonibedu’ hereafter) and Kumargode Estates Ltd (‘Kumargode’ hereafter). Gonibedu and Kumargode are related parties ofMACEL.

57 On 03.05.2019, with the credit balance of Rs 40.11 crores only, 10 cheques totaling Rs 333.88 crores (which were issued on 31-03-2019) were cleared through similar transactions in a circular manner by rotating funds among MACEL, TDL, TRRDPL and Gonibedu.

58 On 18.05.2019, MACEL paid Rs 50 crores to TRRDPL starting a series of sham transactions as thereafter TRRDPL paid Rs 50 crores to MACEL, which then paid Rs 50 crores to TRRDPL, which then paid Rs 50 crores to MACEL, which then paid Rs 40.99 crores to TRRDPL, which then paid Rs 40.99 crores to MACEL. In the Bank Reconciliation Statements (BRS), these cheques were shown as received but not credited in bank as on 31.03.2019.

Induslnd Bank

59 On 02.04.2019, MACEL received Rs 32 crores from CDGL through six RTGS transactions, which was then used to clear on the same day, one by one in circular manner, the five cheques of total amount of Rs 25 crores issued on 30.03.2019. For example, CDGL paid Rs 7 crores to MACEL, which then paid Rs 6.70 crores to CDGL, which then paid Rs 6 crores to MACEL, which then paid Rs 5 crores to CDGL and so on ..

Yes Bank

60 On 04.04.2019, MACEL received credit of Rs 30 crores from related parties including CDGL, thereafter, this fund was used on the same day for clearance of three cheques of total amount of Rs 65.50 crores issued to CDGL on 30.03.2019. These bank transactions were done one by one in a circular manner by circulating funds between MACEL and CDGL in smaller amounts on the same day. After completing these transactions, Rs 22. 70 crores was transferred to bank account with Karnataka Bank referred to above.

61 The SCN noted that the clearance of a large quantum of loans through structured circulation of smaller amounts of funds had resulted in evergreening of loans within the group, which was an indicator of the severe financial crisis in MACEL and fraudulent intentions of MACEL to misstate the Financial Statements. One of the important substantive audit procedures, the SCN noted, is to examine the Bank Statements and the evergreening of loans mentioned above showed that the EP did not exercise due diligence while performing audit of Bank Statements.

62 The unusual feature of evergreening of loans through structured circular transactions of funds was an indication of suspected fraudulent intentions of the MACEL. The SCN noted that there is no evidence in the Audit File that the EP had performed any procedure to identify and respond to RoMM in light of this evergreening of loans despite the fact that it was evident from the bank statements of MACEL. She also did not ask any question to Those Charged With Governance (TCWG) and Management about these unusual transactions. Accordingly, the EP was charged for not having performed the audit with professional judgement and professional skepticism and thus not complying with SA 200, SA 240 and SA 315.

63 As per section 143(1) of the Act, the Auditor is also required to inquire whether transactions are represented merely by book entries and are prejudicial to the interest of the company. As explained above, transactions related to evergreening of loans were mere book entries without adequate funds available with any company, done with the ulterior motive to misstate the financial statements. The EP did not report these fictitious accounting entries and thus violated section 143(1) of the Act.

Reply of the EP

64 The EP has denied this charge stating that these transactions were a desperate attempt of Management in FY 2019-20 to honor the cheques issued in FY 2018-19, as planned funds did not come therefore management arranged funds from Associates. The transactions did not achieve any wrongful purpose. She further mentioned that the method of fund management adopted by MACEL did not form any basis to allege professional misconduct against her. While drawing attention to para 10 to 15 of SA 700 ‘Forming an Opinion and Reporting on Financial Statements’, the EP contended that there is no mandatory responsibility on the Auditor to examine the manner in which funds were managed by the company to clear the cheques issued. This is not within the scope of statutory auditor in normal course of audit unless there is a reason to suspect fraudulent intent, which she did not find.

65 While drawing attention to para 5 and 13 of SA 240 ‘Auditor’s responsibility relating to Fraud in an Audit of Financial Statements’, relating to inherent limitation of an audit and context of professional skepticism, the EP contended that there was no reason to believe wrongful intentions on the part of the management as they gained nothing through circular transactions and rotation of funds and these did not constitute material misstatements. The EP further contended that disclaimer of opinion was issued on Internal Financial Control System, which naturally included these circular transactions.

66 While drawing attention to definition of ‘Material Misstatements’, the EP contended that she has to examine the elements in the Financial Statements for the accuracy of amounts, correctness of time of recognition, completeness of transactions, classification in appropriate group and presentation & disclosures as per financial reporting framework. This was achieved through a detailed process of verification, validation, examination, discussion and inspections. However, it is not possible to record the whole process in audit working paper and also not required to be recorded as per SA 230-‘ Audit Documentation’. The EP further stated that documents of risk assessment procedures performed are available at page 24, 180 and 181 of the Audit File forming part of annexure to SCN and the process of examination by her did not result in identification of risk of any material misstatement.

67 Regarding bank statements, the EP contended that she had verified books of accounts with bank statements to ascertain that bank transactions were duly recorded in the books of accounts, and final position of assets and liabilities was correctly presented in the balance sheet. She stated that there is no error in accounting, hence no misstatements and that raising of money from associate entities to clear off cheques already issued was not illegal and such transactions were not qualified to be reported as fraudulent transactions as per SA 240.

68 The EP further contended that the Standards of Auditing are not reference material to decide on charges of professional misconduct against an Auditor; on the contrary these are for guidance to an Auditor to act professionally. There is no provision in law to hold an Auditor guilty of professional misconduct because the Auditor has erred in her judgement in application of provisions in SA 240 or SA 200.

69 In respect of the charge relating to violation of section 143(1) of the Act, the EP contended that these were actual bank transactions represented by cash flows, accordingly there was neither any material misstatements nor any effect prejudicial to interest of the company.

Analysis of reply

70 Having considered the reply, we note that the fact of evergreening of loans evident from banks statements has not been refuted by the EP. Her line of defense is that ‘planned funds’ did not come hence funds were arranged from Associates. There is no record in the Financial Statements and the Audit File about any ‘Planned Funds’ as contended by the EP. We note that circular transactions did not result in net cash flow ( either inflow or outflow) to MACEL. Cheques were issued, received and recorded in books of accounts in FY 2018-19. Subsequently, in FY 2019-20, these cheques were cleared though circulation of funds among group companies and the incremental accounting impact of such circulation of funds was recorded in books of accounts in FY 2019-20. We find that this resulted in misstatements in financial statements of both the year i.e., FY 2018-19 and FY 2019-20. Since there was no ‘Planned Funds’ for clearance of those cheques, it can be reasonably inferred that it was a preplanned scheme of promoters to misstate financial————— statements to deceive

stakeholders.

71 In respect of the contention of the EP that she is not responsible to examine the manner of fund management by MACEL, we find that preplanned scheme of promoters to misstate financial statements through circulation/ rotation of funds could be easily detected from the bank statements had the EP shown the slightest alertness during the course of Audit, particularly when she was aware of the financial mess committed by VGS. Therefore, the examination of fund management was well within the scope of the EP.

72 The definition of ‘Misstatement’ given in SA 200 inter alia describes that ‘Misstatement can arise from error or fraud’. As already discussed, evergreening of loans through circulation of funds was done to fraudulently misstate financial statements. We find that the arguments of the EP that rotation of funds did not result in any misstatement in the Financial Statements, shows complete lack of professional skepticism in the EP. While the fraud was apparent earlier, it got established after the financial mess was unveiled post the death of VGS in the first half of the financial year. Despite this, the warranted audit procedures were not performed.

73 Further, we have already examined that the contention of the EP of having performed risk assessment procedure is factually incorrect. With respect to the contention of the EP that all bank transactions were correctly recorded in the books of account and that there is no accounting error, we find that she has not been charged for the same in the SCN. The EP’s contention that SAs are not reference material for deciding misconduct of an Auditor, is erroneous as the Auditor is duty bound to comply with SAs in terms of section 143(9) and section143(10) of the Act10.

74 Regarding violation of section 143(1) of the Act in respect of circulation of funds, we notice that circulation of funds was done by MACEL intentionally to misstate the Financial Statements and it did not result in any net cash flow and remained book entries only, resulting in fictitious accounting entries as per section 143(1) of the Act. Accordingly, this charge is proved that the EP violated SA 200, SA 240, SA 315 and section 143(1) of the Act.

C.3 Lapses in audit of inappropriate recognition of Finance Cost of Rs 40.47 crores

75 The EP was charged with failure to perform risk assessment procedure & analytical procedure and failure to exercise professional skepticism in respect of inappropriate recognition of finance cost of Rs 40.46 crores as corresponding borrowings were not used for business activity of MACEL. The EP was also charged with violation of section 143(2) and 143(3)(e) of the Act,. as finance cost was

an extraordinary expense but shown as ordinary finance cost resulting in violation of Division I of Schedule III of the Act and Accounting Standards (‘ AS’ hereafter) 5, Net profit or loss for the period, prior period items and changes in accounting policies.

76 The SCN noted that MACEL had recognized finance cost of Rs 40.46 crores in FY 2019-20, which was 91.89% of total expenses of Rs 44.04 crores. Total bank borrowings of the company were Rs 160.02 crores on 31.03.2020 and Rs 272.32 crores on 31-03-2019. Examination of the Financial Statements shows that the borrowed money was not used for the business activity of the company, but diverted to related parties. Out of the total assets of Rs 4,218.09 crores, approx. 99% (Rs 4,176.67 crores) was given as loans & advances, leaving assets of only Rs 41.42 crores to be used for business activities ofMACEL. Though the finance cost of borrowed fund was recognized, the interest income on loans and advances given to promoters and other related parties was not recovered, resulting in material and pervasive misstatement in the Profit and Loss Statement by a large proportion of finance cost.

77 As per SA 315, the EP was required to perform risk assessment procedures to provide a basis for the identification and assessment ofRoMM in respect of finance cost. Para 6 of SA 520 required the EP to design and perform analytical procedures near the end of the audit that would have assisted her in forming an overall conclusion whether the Financial Statements are consistent with her understanding of MACEL. As a prudent Auditor, she was required to critically analyze the finance cost & bank borrowings with the assets used for business activity ofMACEL. Analysis in previous para and application of Professional Skepticism as provided in SA 200 should have aroused suspicion in her mind. As per para 32( c) of SA 240, she was required to evaluate whether there is any fraud in recognition of finance cost, being unusual in nature. Examination of the Audit File, according to the SCN, shows that she did not perform any audit procedure and also did not ask any question to TCWG and Management, and thus violated SA 200, SA 240, SA 315 and SA 520.

78 Further, as per para 4.2 of AS 5 ‘Net Profit or Loss for the Period, Prior Period Items and Prior Period Items and changes in accounting policies’, Extraordinary items are income or expenses that arise from events or transactions that are clearly distinct from the ordinary activities of the enterprise and, therefore, are not expected to recur frequently or regularly. Finance cost was not for ordinary activity of MACEL, hence was required to be treated as extraordinary item. As per Division I of Schedule III of the Act and para 8 of AS 5, extraordinary items should be disclosed in the statement of profit and loss as a part of net profit or loss for the period. The nature and amount of each extraordinary item should be separately disclosed in the statement of profit and loss in a manner that its impact on current profit or loss can be perceived. Accordingly, MACEL was required to disclose the finance cost as extraordinary expense in the statement of profit and loss in the manner described ,above. Examination of the Financial Statement shows that MACEL did not disclose finance cost as extraordinary expense but as ordinary finance cost, thus violated Division I of Schedule III of the Act and AS 5. Section 143(3)(e) of the Act requires an auditor to state in the Auditor’s Report whether the Financial Statements comply with the accounting standards. The SCN charged that the EP has violated section 143(2) & 143(3)(e) of the Act as she reported in the Audit Report that the Financial Statements comply with the Accounting Standards specified under section 133 of the Act, read with Rule 7 of the Companies (Accounts) Rules, 2014 ..

Reply of the EP

79 While denying the charge the EP stated that interest expenses incurred were neither in violation of any law nor inconsistent with accounting principles in force. MACEL paid interest on borrowed amount whereas there was no contractual obligation to pay interest by the entities to whom loans/advances were given by MACEL. In respect of not charging interest on the loans/advances given by MACEL, the EP contended that there was no authority with the EP to dispute the Management action relating to charging of interest or not. She contended that interest expense was incurred by MACEL and duly reflected in the Profit and Loss Statement, hence cannot constitute a misstatement. The EP stated that proper disclosure about advances given to persons covered under section 189 of the Act has been given in CARO report, to discharge her responsibility as per section 143(1)(a) of the Act.

80 The EP has contended that based on the information and evidence collected by her, she was not in a position to form a view that there was any fraud in recognition of interest. She replied that reference to para 32(c) of SA 240 is misplaced. According to her, para 31 & 32 of SA 240 are in the context of overriding controls by management to perpetuate fraud… In MACEL, there was no override of controls. Management of MACEL were no other than shareholders, hence she could not see it as a fraud. The EP further contended that she had given disclaimer of opinion and disclosed the interest free nature of advances made, therefore she had no other obligation in this regard.

81 While drawing attention to para 9 and 10 of AS 5, the EP contended that going by the spirit of principles in AS 5, proposition ofNFRA that finance cost was an extra-ordinary item is denied and there was no violation of AS 5 and Schedule III of the Act. She further replied that it is incorrect to say that she had reported that financial statements comply with Accounting Standards specified under section 133 of the Act, whereas in the Audit Report she had expressed her inability to comment whether the financial statements complied with Accounting Standards specified under section 133 of the Act.

Analysis of reply

82 MACEL is a small company having Revenue from Operation of Rs 3.27 crores only. Its total business assets are Rs 41.42 crores only in the form of Tangible assets, Inventories, Cash and Cash equivalent and Other Current Assets. Compared to this, its Balance Sheet size of Rs 4218.09 crores is disproportionately large, mainly on account of Rs 4176.67 crores loans given to related parties, with whom MACEL did not have any business relations. The loans given to the related parties were without any business rationale and clearly beyond the normal course of business.

83 MACEL’s total borrowings were Rs 4479.79 crores, of which a major part was from related parties. Since the assets used for the business activities of MACEL were only Rs 41.42 crores, it is evident that the remaining borrowings of Rs 4438.37 crores (Rs 4479.79 crores – Rs 41.42 crores) were diverted to related parties. Therefore, the diversion of funds was clearly visible from the Balance Sheet signed by the EP.

84 MACEL recognised huge interest expenses of Rs 40.47 crores, whereas interest income of Rs 0.15 crores only was recognised in its Profit and Loss Statement signed by the EP. A combined reading of the Balance Sheet and the Profit & Loss Statement clearly shows that the proceeds of interestbearing loans were diverted to related parties at no or nominal interest. Therefore, it is clear that Related Party Transactions were not at ‘Arm’s Length’. Further, this resulted in recognition of loss of Rs 40.62 crores in the Profit & Loss Statement for FY 2019-20. Had the interest been recovered from the related parties, which used these funds, the loss of MACEL would have been minuscule. A similar trend is visible in FY 2017-18 and FY 2018-19. This practice has eroded the entire net worth of the company, which was a negative Rs 264.32 crores on 31.03.2020.

85 The EP has replied that interest expense was incurred and duly accounted for. She could not give any reply why such interest expense should be ultimately borne by MACEL, when the borrowed money was not used by MACEL and passed on to other related entities. The EP failed to question why the interest on such borrowed money should become expenses of MACEL, unless the corresponding interest income on advances made to related parties is also recognised as interest income of MACEL. In that context, we find that interest expense of Rs 40.47 crores has resulted in misstatement in the Profit and Loss Statement of MACEL.

86 Diversion ofinterest-bearing loan proceeds to promoters/their entity without any interest was a proof of fraudulent intention of promoters to recognize loss in the Profit and Loss Statement of MACEL and therefore it was an unusual transaction. The EP was duty bound as per SA 240 to evaluate such an unusual transaction, which she failed to do. Further, disclosure given in CARO report relating to interest free nature of advances made, does not absolve the EP of her responsibility to report misstatement in Profit and Loss Statement, which is required to be reported in the Independent Auditor’s Report as per SA 700. Section 143 of the Act prescribes powers and duties of Auditors. Subsection (l)(a) of the said section provides that an auditor has right to inquire “whether loans and advances made by the company on the basis of security have been properly secured and whether the terms on which they have been made are prejudicial to the interest of the company or its members”. The EP has reported at para (iii) of CARO report that “The company has not granted any loan, secured or unsecured to companies, firms, Limited Liability Partnerships or any other parties covered in the register maintained under section 189 of the Companies Act, 2013. However, the company has granted advances to various companies and other parties covered in the register maintained under section 189 of the companies Act 2013. According to the information and explanation provided to us, these advances are interest free and with no fixed repayment tenure and are repayable on demand”. It is clear from above that the EP did not disclose whether such loans (termed as advances) were secured or not. Despite being fully aware of their existence, she failed to evaluate whether such loans were prejudicial to the interest of the company or its members. Therefore, her claim of having discharged her responsibility under section 143(1)(a) of the Act, is factually incorrect.

87 With respect to the management override of controls, the EP has argued that there was no override of control as the Management of MAC EL were no other than shareholders. themselves. It is obvious that involvement of shareholders in the day-to-day management of MACEL was a proof of override of controls. In this case VGS, Chairman of CDEL (a listed company) transferred huge funds from subsidiary companies ofCDEL to MACEL and further from MACEL to his own personal accounts, his family members’ personal accounts and to other entities owned by them, by using pre-signed blank cheques. This is a classic example of override of controls and the reply shows that the EP has poor understanding of the meaning of’ Override of Controls”.

88 Para 9 of AS 5 states “Virtually all items of income and expense included in the determination of net profit or loss for the period arise in the course of the ordinary activities of the enterprise. Therefore, only on rare occasions does an event or transaction give rise to an extraordinary item”. Further, para 10 of AS 5 provides that the nature of transaction determines whether a transaction is distinct from ordinary activity of the enterprise. In this case, the interest expense did not arise in the course of ordinary activity of MACEL but due to the borrowings not meant for MACEL’s business but to siphon off funds by the promoters using MACEL as a conduit; therefore this is a rare occasion and such interest expense was to be classified as extraordinary expense.

89 Division I of Schedule III of the Act prescribes the format of the Profit and Loss Statement, which has been followed by MACEL, and includes a line item ‘Extraordinary Items’. MACEL has shown NIL amount against this line item. Interest cost incurred by MACEL on Borrowings from Related Parties which were not meant for the ordinary business activities of MACEL is no doubt an extraordinary item within the meaning of para 9 of AS 5. However, by not classifying interest cost of Rs 40.4 7 crores as extraordinary item in the Profit and Loss Statement, MAC EL violated Division I of Schedule III of the Act and AS 5, and the EP failed to report this.

90 With reference to the response of the EP regarding disclaimer on compliance with accounting standards specified under section 133 of the Act, we have perused the audit report and find that she had expressed her inability to comment whether the financial statements complied with accounting standards specified under section 133 of the Act. This reply is partially correct. However, we perused this disclaimer at para (d)……… of the Audit Report which states “We are unable to comment whether the aforesaid financial statements comply with the accounting standards specified under section 13 3 of the Act, read with rule 7 of the Companies (Accounts) Rules, 2014 because of the significance of the matters described in Basis for Disclaimer of Opinion section above”. As can be seen from the wording of the disclaimer of opinion, it is only related to compliance with ASs in respect of subject matter of disclaimer of opinion i.e., recoverability of Loans to Related Parties. It does not relate to non-compliance with ASs in respect of other areas such as the instant case of failure to classify the interest cost incurred on extraordinary borrowings, as the extraordinary expense. Thus MACEL did not comply with AS 5 and the EP failed to identify and report this material misstatement. In view of above analysis, we find that the EP has violated section 143(2) and 143(3)(e) of the Act.

C.4 Lapses in audit relating to misstatement of Rs 1938.87 crores in the Cash Flow Statement

91 The EP was charged with failure to report material misstatement of Rs 1938.87 crores in Cash Flow Statement resulting in violation of section 143(2) & 143(3)(e) of the Act. According to the SCN, MACEL failed to comply with AS 3 ‘Cash Flow Statements’, which provides that short term borrowings are to be disclosed as Cash Flow from Financing Activities. However, MACEL has recognized decrease in short term borrowings of Rs 1,877.56 crores as negative Cash Flow from Operating Activities resulting in understatement of Cash Flow from Operating Activities and overstatement of Cash Flow from Financing Activities by Rs 1,877.56 crores. Further, as per AS-3, loans and advances made to third parties are to be disclosed as Cash Flow from Investing activity ( other than advances and loans made by financial enterprise). MACEL did not consider itself a financial enterprise. However, MACEL has disclosed decrease in short term loans & advances made (assets) of Rs 61.31 crores as Cash Flow from Operating Activity resulting in overstatement of Cash Flow from Operating Activity and understatement of Cash Flow from Investing activity by Rs 61.31 crores.

Reply of the EP

92 The EP has partially admitted the charge relating to wrong presentation of Cash Flow from shortterm borrowing in Cash Flow from Operating Activities. According to her, out of Rs 1,877.56 crores, Rs 109.03 crores represented repayment of bank borrowings and deserved to be included under ‘Cash Flow from Financing Activities’, while the remaining amount represented changes to operating assets/liabilities like advances received and advances given, and was therefore correctly classified under ‘Cash Flow from Operating Activities’. The EP further stated that the admitted mistake may be pardoned as an inadvertent presentation error because it is not material.

93 Regarding the charge relating to loans/advances made to third parties, the EP denied the charge stating that advances were given for furtherance of their business objectives associated with several coffee estates managed by the associate entities and so these advances related to operations. She contended that they were not loans. The EP stated that the term ‘advance’ and ‘loan’ are interchangeably used in AS 3, which is misleading and accepted that loans given would certainly be ‘Cash Flow from Investments’. She further contended that there is always room for following an alternate accounting policy by virtue of the provisions in para 12 to 17 of AS 1 – ‘Disclosure of Accounting Policies’ and section 129(5) of the Act. The EP finally stated that according to the substance of the advance transactions, it was proper to present them as Cash Flow from Operating Activities.

Analysis of reply

94 Para 3 & 4 of AS 3 describe the importance of Cash Flow Information as “A cash flow statement, when used in conjunction with the other financial statements, provides information that enables users to evaluate the changes in net assets of an enterprise, its financial structure (including its liquidity and solvency) and its ability to affect the amounts and timing of cash flows in order to adapt to changing circumstances and opportunities. Cash flow information is useful in assessing the ability of the enterprise to generate cash and cash equivalents and enables users to develop models to assess and compare the present value of the future cash flows of different enterprises. It also enhances the comparability of the reporting of operating performance by different enterprises because it eliminates the effects of using different accounting treatments for the same transactions and events. Historical cash flow information is often used as an indicator of the amount, timing and certainty of future cash flows. It is also useful in checking the accuracy of past assessments of future cash flows and in examining the relationship between profitability and net cash flow and the impact of changing prices”.

95 Para 8 of AS 3 provides that the cash flow statement should report cash flows during the period classified by operating, investing and financing activities, which are defined as under:

a) Operating activities are the principal revenue-producing activities of the enterprise and other activities that are not investing or financing activities.

b) Investing activities are the acquisition and disposal of long-term assets and other investments not included in cash equivalents.

c) Financing activities are activities that result in changes in the size and composition of the owners’ capital (including preference share capital in the case of a company) and borrowings of the enterprise.

96 Therefore, the importance of Cash Flow information and its classification are clearly prescribed in AS 3, which were to be complied by MACEL. In her response, the EP has admitted wrong presentation of cash flow from short-term borrowing of Rs 109.03 crores in ‘Cash Flow from Operating Activities’ in place of ‘Cash Flow from Financing Activities’. Accounting and analysis of Cash Flow is an important aspect of Auditing.