Background

♣ Section 134(5) of the Companies Act, 2013 requires board of directors of every company to state in its Directors’ Responsibility Statement that they have prepared the annual accounts on a going concern.

♣ Also, Ind AS 1 – Presentation of Financial Statements and AS 1 – Disclosure of Accounting Policies requires the management to assess the entities ability to continue as a going concern.

♣ Given the economic uncertainties due to Covid-19 and business disruption for entities in almost all sectors, there is likely to be an increase in events and circumstances which may cast a significant doubt on the entitles ability to continue as a going concern.

Recent Development

The International Accounting and Auditing Standards Board (IAASB) and The Institute of Chartered Accountants of India (ICAI) have issued guidance on going concern assessment amid COVID-19 for companies and considerations for an auditor while evaluating the management’s assessment.

The guidance note issued by ICAI focuses on the following matters:

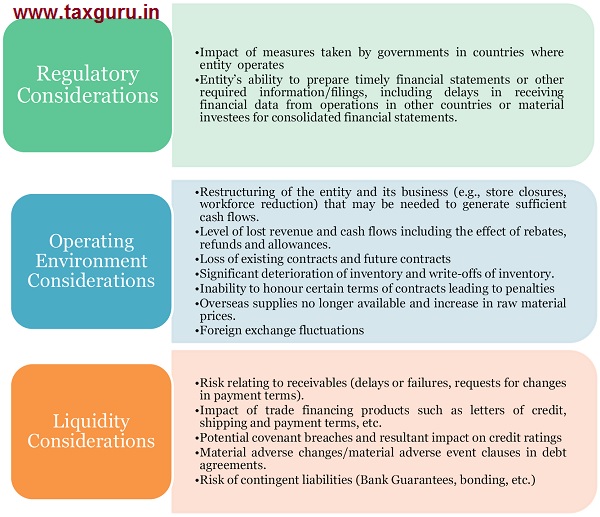

Some of the important considerations highlighted by the ICAI guidance are as follows:

- Assess what impact the current events have on an entity’s operations and forecasted cash flows.

- Consider the existing and anticipated effects of the COVID-19 on the assumptions.

- Assess specific matters relating to COVID-19. Few examples are highlighted below:

Key Points

- The auditor should consider the following mitigating factors:

- Capital expenditure reductions;

- Reduction in dividends;

- Suspension of non-performance based bonuses;

- Deferral of payments of principal and interest;

- Working capital reduction, taxation payment holidays or deferrals or COVID-19 driven government funding.

- In assessing the entities ability to continue as a going concern, the management shall consider for at least but not limited to 12 months from the end of reporting period.

- In case after the reporting period, management determines that it intends to liquidate the entity or cease trading, or that it has no realistic alternative but to do so, the financial statements may require a fundamental change in the basis of accounting (e.g., to liquidation basis of accounting), rather than an adjustment to the amounts recognised within the original basis of accounting.

Additional audit procedures when events or conditions are identified

- Analysing and discussing cash flow, profit and other relevant forecasts with management.

- Analysing and discussing the entity’s latest available interim financial statements.

- Reading the terms of debentures and loan agreements and determining whether any have been

- Inquiring of the entity’s legal counsel regarding the existence of litigation and claims.

- Confirming the existence, legality and enforceability of arrangements to provide or maintain financial support with related and third parties.

- Evaluating the entity’s plans to deal with unfilled customer orders.

- Performing audit procedures regarding subsequent events to identify those that either mitigate or otherwise affect the entity’s ability to continue as a going concern.

- Confirming the existence, terms and adequacy of borrowing facilities.

Good writing.