Background

Ind AS 40 deals with recognition, disclosure and measurement of Investment Property. As per this standard Investment Property should be disclosed as a separate line item on the face of the balance sheet and cannot be clubbed as part of Property, Plant and Equipment.

Scope of Ind AS 40

Ind AS 40 does not deal with:

- Biological assets related to agricultural activity;

- Mineral rights and mineral reserves such as oil, natural gas and other similar non-regenerative resources.

Definitions

The following are not investment property, when they are held for:

i. Production or supply of goods or services or for administrative purposes; or

ii. Sale in ordinary course of business

Owner-occupied property is property held for use in the production or supply of goods or services or for administrative purposes.

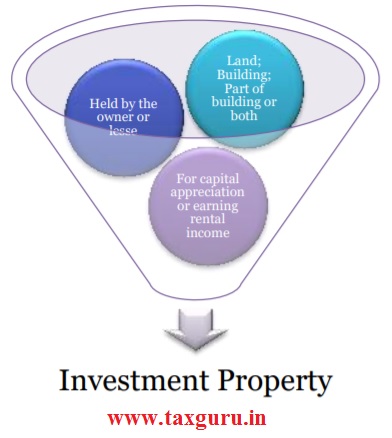

Examples of Investment Property

i. Land held for long-term capital appreciation rather than for short term sale in the ordinary course of business.

ii. Land held for a currently undetermined future use. (If an entity has not determined that it will use the land as owner-occupied property or for short-term sale in the ordinary course of business, the land is regarded as held for capital appreciation.)

iii. A building owned by the entity (or held by the entity under a finance lease) and leased out under one or more operating leases.

iv. A building that is vacant but is held to be leased out under one or more operating leases.

v. Property that is being constructed or developed for future use as investment property.

Following are examples of items that are not investment property:

i. Property intended for sale in the ordinary course of business or in the process of construction or development for such sale.

ii. Owner-occupied property, including property held for future use as owner-occupied property, property held for future development and subsequent use as owner-occupied property, property occupied by employees (whether or not the employees pay rent at market rates) and owner-occupied property awaiting disposal.

iii. Property that is leased to another entity under a finance lease.

Recognition & Measurement

An asset shall be recognised in the books of accounts when it satisfies following two conditions:

i. Probable future economic benefits inflows to the entity; and

ii. Cost should be measured reliably.

Initial Recognition

Owned Investment Property should be measured at its Cost. Following shall form part of the cost:

Purchase Price – XX

(+) No refundable taxes, property transfer taxes – XX

(+) Professional fees – XX

(+) Brokerage & commission – XX

(+) Borrowing cost – XX

(+) Decommissioning or restoration cost (Present value) – XX

(+) Any other directly attributable cost XX

Cost of Investment Property to be capitalised – XXX

An entity should measure the investment property using cost model as per Ind AS 16. This standard prohibits recognising the investment property using fair value model although standard requires all entities to measure the fair value of investment property only for the purpose of disclosure.

As per Ind AS 16 – Cost Model

Cost XX

(-) Accumulated depreciation – XX

(-) Accumulated impaired loss – XX

Net carrying amount – XXX

Transfer/Reclassification

The entities intension on usage of the property may change due to many reasons, i.e. it may use the property for its own use or it may decide to sell the property in ordinary course of its business or start renting a property which was being used in the business, etc.

Note:

i. Any reclassification shall only be made when there is a change in use. Mere change in the management’s intension does not qualify to provide evidence of a change in use.

ii. Transfer/reclassification does not change the carrying amount of the property for measurement or disclosure purpose.

Disposal

An investment property shall be derecognised on disposal or when the investment property is permanently withdrawn from use and no future economic benefits are expected from its disposal.

Disclosure

i. Its accounting policy for measurement of investment property.

ii. When classification is difficult, the criteria it uses to distinguish investment property from owner occupied property and from property held for sale in the ordinary course of business.

iii. The extent to which the fair value of investment property (as measured or disclosed in the financial statements) is based on a valuation by an independent valuer, if there has been no such valuation, that fact shall be disclosed.

iv. The amounts recognised in profit or loss for:

- Rental income from investment property;

- Direct operating expenses (including repairs and maintenance) arising from investment property that generated rental income during the period; and

- Direct operating expenses (including repairs and maintenance) arising from investment property that did not generate rental income during the period.

v. The existence and amounts of restrictions on the realisability of investment property or the remittance of income and proceeds of disposal.

vi. Contractual obligations to purchase, construct or develop investment property or for repairs, maintenance or enhancements.

Author Bio

Thanks to illustrate the tedious subject in a very interesting way.