The document sets out comprehensive, practice-driven suggestions to improve the Ease of Doing Business under GST, focusing on registration, returns, reverse charge, audits, refunds, ITC, e-way bills, dispute resolution, and social relief measures. It highlights how discretionary powers, portal limitations, and form-design mismatches create compliance burdens, cash-flow blockages, and avoidable litigation despite clear statutory intent. Key concerns include subjective GST registration queries, duplication in multi-state registrations, flawed annual return reconciliations, ITC mismatches arising from form logic, rigid reverse charge rules, excessive penalties for minor procedural lapses, fragmented audits, delayed refunds, and systemic gaps in dispute resolution and notice service. The suggestions emphasise standardisation, PAN-based automation, form redesign, portal safeguards, and clearer legal guidance to align procedures with substantive law. The overall thrust is to replace discretion with systems, reduce duplication, protect bona fide taxpayers, and ensure that GST operates as a neutral, technology-driven tax regime rather than a source of procedural friction.

The Institute of Chartered Accountants of India

Suggestions on Enhancing Ease of Doing Business

INTRODUCTION

ICAI is a statutory body established by an Act of Parliament, viz. The Chartered Accountants Act, 1949, for regulating and developing the profession of Chartered Accountancy in the country. The ICAI is the largest professional body of Chartered Accountants in the world, with a strong tradition of service to the Indian economy in public interest.

The GST & Indirect Taxes Committee of the ICAI plays a vital role in supporting the Government’s GST initiatives through policy advisory, capacity-building programmes and knowledge dissemination. The Committee extended unwavering support to the Government during the rollout of GST by providing inputs on GST law and procedures and by undertaking extensive awareness and training initiatives.

The Committee is pleased to present its considered suggestions on issues impacting the ‘Ease of Doing Business’. These suggestions are aimed at strengthening the GST framework, enhancing the ‘Ease of Doing Business,’ and providing practical solutions to the persistent challenges faced by trade and industry.

In case any further clarification or data is considered necessary, the Committee shall be pleased to furnish the same. The contact details are:

| Name and Designation | Contact Details | |

| Mobile/Tel. No. | Email Id | |

| CA. Rajendra Kumar P

Chairman GST & Indirect Taxes Committee |

9444017087 | rk@icai.in |

| CA. Umesh Sharma

Vice –Chairman GST & Indirect Taxes Committee |

9822079900 | fcaumeshsharma@gmail.com |

| CA. Smita Mishra

Secretary GST & Indirect Taxes Committee |

9205559863

0120-3045954 |

gst@icai.in; smita@icai.in

|

SUGGESTIONS ON ENHANCING EASE OF DOING

BUSINESS

A. REGISTRATION

1. Standardization of Document Verification and Rejection Protocols Issue

Despite the issuance of Instruction No. 03/2025-GST dated 17.04.2025, which explicitly directs officers to adhere to the standard document list, field formations continue to raise queries and demand documents (e.g., Landlord’s PAN, signature verification). The root cause lies in the subjective language of proviso to Rule 9(1) of the CGST Rules, 2017, which empowers the proper officer to mandate physical verification and additional scrutiny in cases where they “deem fit” and Rule 9(3) of the CGST Rules, 2017, which empowers the Proper Officer to issue a deficiency notice based on their “satisfaction” regarding the completeness of the application. This “deem fit” and “satisfaction” clause is sometimes interpreted as an open-ended power to demand any additional document, effectively nullifying the intent of the CBIC’s instructions. This statutory discretion effectively overrides administrative instructions, enabling officers to raise subjective queries and demand unspecified documents—such as the landlord’s personal tax details or signature verification under the guise of “satisfaction”. Consequently, applications are rejected without speaking orders or on irrelevant grounds, such as the operation of business from residential premises, thereby defeating the objective of Ease of Doing Business.

Suggestions

To eliminate this ambiguity, the relevant provisions (specifically Rule 9) be amended as under:

- The discretionary “satisfaction” clause may be removed.

- The wordings “the Government may by the notification specify an exhaustive list of documents for registration under the said rule” may be added under the said the rule.

- Any additional information or queries raised by officers be restricted to a structured, pre-approved framework, aligned with the Rules, the registration form, and instructions/ circulars.

- GSTN portal be modified to limit the officer’s query mechanism as follows:

ii. Standardized Drop-Down Menus: Officers should only be able to select from a pre-defined list of standard query types (e.g., “clarification on address proof”, “business activity mismatch”, “ownership proof of premises”).

iii. Limited Free Text: A restricted text box should be provided for brief, case-specific remarks, preventing long-form, arbitrary demands.

In light of the discrepancies observed in field practices, we propose the following Standardized Illustrative Checklist of Documents, based on the principles of Instruction No. 03/2025-GST, which officers should adhere to for the grant of registration:

Table 1: Illustrative List of Documents

| Scenario | Standard Documents | Remarks ! Restrictions ! Legal Basis |

| A. PROOF OF PRINCIPAL!ADDITIONAL PLACE OF BUSINESS | ||

| 1. Own

Premises |

Upload Any One:

|

Restriction: No additional documents shall be demanded. |

| 2. Rented

Premises (Registered Agreement) |

|

Restriction: Identity proof or signature proof of the Lessor shall NOT be sought. |

| 3. Rented

Premises (Unregistered Agreement) |

|

Remark: Identity proof is mandatory only in this specific case. |

| 4. Rented Premises

(Utility Bill in Tenant’s Name) |

|

Remark: Identity proof of Lessor is mandatory only in this specific case. |

| 5. Consent (Spouse, Relative, etc.)

Shared (For example in Fulfilment Centers / Cold storage / Godowns owned by others / Co-working places) |

|

Restriction: No “No

Objection” Affidavit |

| 6. No Rent Agreement |

|

|

| 7. Special Economic Zone |

|

|

| 8. Premises is owned by Parents who are not alive | a. Ownership Proof where name change did not happen

b. Legal Heir Certificate c. Electricity Bill / Water Bill/ Property Tax |

Restriction: No other document shall be demanded. |

| Note: | ||

|

||

| B. PROOF OF CONSTITUTION OF BUSINESS | ||

| 1. Partnership Firms | · Partnership Deed (whether registered or not). |

Restriction: Do NOT ask for Udhyam/MSME, Shops &

Establishments Certificate, |

| 2. Society,

Trust, Club, Govt, AOP, BOI |

· Registration Certificate OR

· Proof of Constitution. |

|

| C. STRATEGIC REQUIREMENTS & LEGAL SAFEGUARDS | ||

| 1. Bank Account Proof |

|

Restriction: Officers should not demand financial history or 6-month statements. |

| 2.

Authorization Proof |

· Board Resolution (Companies); OR

· Letter of Authorization |

Mandatory: Must explicitly

authorize signatory for |

| 3.Presumptive Queries | Prohibition on queries regarding business viability/zoning. | Legal Basis: Para 7 of Instruction 03/2025-GST prohibits queries on business logic or address suitability. |

| D. NEGATIVE LIST (EXPLICITLY EXCLUDED) | ||

| Documents Officer MUST NOT Ask For

|

|

Basis: Instruction No. 03/2025-GST explicitly excludes these to curb discretionary practices.

|

Justification

Merely issuing instructions has proven insufficient as they are often disregarded at the field level. System should be put in place where senior officers review the instances of defiance of instructions and strict administrative action should be initiated against erring officers with a view to ensure that the “Ease of Doing Business” is not compromised by individual interpretation.

2. PAN-Based Pre-auto population of Data in Multi-State Registrations Issue

Currently, when a taxpayer already registered under GST in one State applies for a subsequent registration in another State or Union Territory or within the same State / UT, the GST portal mandates the manual re-entry of all entity-level details. Despite this master data— Legal Name, Constitution of Business, and details of Directors or Partners—already existing in the system against the same PAN, the portal lacks the functionality to retrieve it. This redundancy forces taxpayers to duplicate efforts for every new registration (within or outside the State / UT), increasing the compliance burden and the risk of data entry errors.

Suggestion

The functionality on GST portal be enhanced to auto-fetch and pre-populate all common PAN-based information from the existing GSTINs associated with the applicant. The registration workflow should be streamlined to require the applicant to furnish only new registration specific information, such as the Principal Place of Business, Bank Account details, and Additional Places of Business along with the facility to edit the fetched information.

Justification

Implementing a PAN-linked data retrieval system aligns with the “Digital India” objective of minimizing repetitive compliance. It would significantly reduce the time required for multi-state registrations and ensure data consistency across the taxpayer’s GST registrations.

3. Issues in Integrated Registration via MCA Portal

Issue

Currently, the integrated registration mechanism provided through the Ministry of Corporate Affairs (MCA) portal (via SPICe+ and AGILE-PRO-S forms) suffers from significant systemic opacity. While the facility allows for GST registration to be applied concurrently with the incorporation of Companies and LLPs, there is a distinct lack of visibility and defined timelines for the processing of these applications once data is transmitted to the GST Network. Unlike other statutory registrations such as PAN and TAN which are generated seamlessly, GST applications often face transmission delays or data mismatches without a transparent status tracking mechanism, leaving newly incorporated entities in a state of uncertainty.

Suggestion

The GST registration process for newly incorporated entities be upgraded to a robust, fully automated Single-Window Facility. Just as PAN, TAN, EPFO, and ESIC registrations are processed concurrently and seamlessly with incorporation, the GST registration workflow must be aligned to ensure immediate validation and TRN generation. The system should be enhanced to provide real-time status updates back to the MCA portal to ensure applicants can track the progress of their application.

Justification

Achieving a true single-window clearance is pivotal for the Government’s Ease of Doing Business initiative. Harmonizing GST registration timelines with company incorporation will ensure that newly formed entities can commence business operations immediately, thereby eliminating the compliance lag that currently exists between the date of incorporation and the effective date of tax registration.

5. Single Biometric Verification for Multi-State Registrations Issue

Currently, the protocol for biometric Aadhaar authentication and document verification operates in silos across different States and Union Territories.

Consequently, even when an applicant has successfully completed the rigorous biometric verification process for a registration in one jurisdiction, the system mandates a de novo (fresh) verification for subsequent applications in other States linked to the same PAN. This results in the system repeatedly flagging the same applicant for verification, compelling them to undertake repetitive compliance procedures and incur avoidable travel costs for physical verification at designated centers. Such redundancy directly contradicts the Government’s objective of procedural simplification and digital integration.

Suggestion

Biometric verification be treated as a PAN-level validation rather than a State-specific requirement. Once an applicant has successfully completed biometric authentication for one GSTIN, this status should be legally and technically accepted PAN-India for all subsequent registrations associated with that PAN.

Justification

Adopting a ‘One PAN, One Verification’ approach will significantly reduce the compliance burden for businesses expanding their operations within same State / across States. It ensures that the robust identity checks are respected globally within the system without subjecting compliant taxpayers to duplicative processes, thereby enhancing the Ease of Doing Business.

5. Procedural Guidelines for GST Registration of Minors

Issue

The current GST framework lacks explicit guidance regarding the eligibility and procedure for granting registration to minors. This ambiguity causes significant compliance hurdles, particularly in cases involving the transfer of business via inheritance (succession) or the formation of family-run enterprises and startups where a minor is a beneficiary. Due to the absence of a defined standard operating procedure (SOP) concerning the legal capacity of minors and the role of guardians, field officers often raise objections or reject such applications, creating a legislative vacuum for legitimate business successions.

Suggestion

The CBIC may issue a comprehensive clarificatory circular and simultaneously update the GST portal workflow to specify:

i. The eligibility criteria and legal capacity for minors to obtain registration through a legal guardian.

ii. The specific procedural mechanism for obtaining such registration, including the linking of the Minor’s PAN with the Guardian’s details.

iii. A validation protocol for e-signing and document verification, explicitly authorizing the legal guardian to undertake compliance on behalf of the minor.

Justification

Clarifying the registration protocol for minors is essential to ensure seamless business continuity, especially in cases of death of a proprietor where the successor is a minor. A defined mechanism will eliminate discretionary rejections at the field level and align GST processes with general laws governing guardianship and succession.

6. GST Registration Hurdles for New Units

Issue

When a taxpayer intends to establish a manufacturing or business unit in a different state from their principal place of business, they encounter significant procedural hurdles in obtaining a new GST registration in the other state. The primary challenge arises because:

The physical unit does not yet exist (it is still in the planning or construction phase) and does not have technically qualified manpower in the said state. However, the taxpayer incurs substantial capital expenditure (plant & machinery) before the unit becomes operational.

Legally, such taxpayer is required to compulsorily obtain registration in the other State in terms of section 24 which entitles him to claim Input Tax Credit (ITC) on such capital goods and services under CGST Act. However, field officers sometimes reject or delay registration applications of such units because the ‘physical unit’ is still under construction and does not meet the strict definition of a “Place of Business” under Section 2(85) of the CGST Act (which implies a fully functional setup). This prevents the taxpayer from claiming ITC, leading to severe cash flow blockages, compliance delays, and deterrence to inter-State investment.

The new units also face the same challenge while applying for voluntary registration for the first time. They are also not able to claim ITC of eligible capital goods installed/set up in the pre-operation stage leading to cash flow blockages which can be a genuine concern for new businesses.

Suggestions

For Existing Taxpayers: Registration should be granted immediately by leveraging their compliance history in their home state. The system should allow them to apply for the new State’s registration linked to their existing GSTIN.

It is suggested that a scheme of ‘Single-Window Registration via Resident State (Centralized Provisional Registration)’ be implemented for existing taxpayers.

Allow the taxpayer to apply for a provisional GST registration for the new state through their existing registration in the resident state – since the jurisdictional office is well aware of the business need and requirement of the taxpayer.

This could be facilitated via the GST Portal’s single-window interface, where:

- The taxpayer declares the intended location of the new unit (with supporting documents like land deeds, MoU with state government, or project approval).

- A unique provisional GSTIN is issued for the new state, linked to the principal GSTIN.

- ITC on capital expenditures is automatically routed to the provisional GSTIN, with deemed place of supply as the new state.

- Transition Mechanism: Once the unit is physically established (e.g., issuance of occupancy certificate), the provisional registration converts to a regular registration with minimal additional compliance.

For First-Time Registrants (New Businesses): Registration should be granted on a provisional basis relying on valid documentary evidence of project initiation (e.g., Land Deeds, Sanctioned Project Loans, Regulatory Approvals, or Industrial Licenses) without insisting on immediate physical verification of a ‘ready-to-operate’ unit.

Safeguard: Physical verification can be mandated at a later stage (e.g., after 6 months or upon commencement of commercial production) to verify the final setup.

Justification

This proposal is grounded in the statutory right provided under the CGST Act, which entitles taxpayers to claim Input Tax Credit on capital goods used for business. Denying registration during the setup phase effectively nullifies this legal right. Ultimately, this measure promotes the Ease of Doing Business by removing significant bottlenecks on inter-State investments and ensuring that vital working capital is not unnecessarily blocked in taxes during the critical project phase.

7. Procedural Irregularity in Granting Voluntary Registration instead of Temporary Registration for Unregistered Persons

Issue

During the Assessment proceedings against unregistered persons (e.g., under Section 63, Section 74, or Section 122(1A) of CGST Act, 2017), Proper Officers sometimes grant Voluntary Registration (under Section 25(3) of CGST Act) instead of creating a Suo Motu Temporary Registration (under Rule 16A). This creates two significant legal and technical anomalies:

1. Loss of Jurisdiction: By granting Voluntary Registration, the noticee get converted into a ‘Registered Person.’ This undermines the legal basis for passing an assessment order under Section 63, which is explicitly reserved for the Assessment of Unregistered Persons.

2. Appellate Deadlock: Without a specific Temporary ID generated in the State where the offence occurred (Host State), the adjudication order is not properly linked on the portal. Consequently, the taxpayer cannot file an online appeal (Form GST APL-01) in the Host State. They are forced to file manual appeals, often in their Home State, which are subsequently rejected for lack of jurisdiction, leaving the taxpayer without a valid appellate remedy.

Suggestion

It is recommended that an Instruction be issued mandating Proper Officers to generate a suo moto Temporary ID (as per Rule 16A of CGST Rules) for all adjudication proceedings involving unregistered persons. The use of Voluntary Registration for enforcement purposes should be prohibited to preserve the distinction between a compliance-seeking applicant and an enforcement-led assessment.

Justification

Granting Temporary Registration ensures that the noticee retains the status required for assessment under Section 63 while providing a digital identity for the demand. This enables the system to host the order electronically in the correct jurisdiction, allowing the taxpayer to exercise their statutory right to file an online appeal in the Host State, thereby eliminating the need for manual filings and jurisdictional disputes.

B. RETURNS – [Forms GSTR 9 & 9C]

8. Segregation of Forward Charge and Reverse Charge (RCM) Liabilities in Table 4N of GSTR-9

Table Reference: GSTR-9-Table 4N (Supplies and advances on which tax to be paid)

| N | Supply and advance on which tax is to be paid (H+M) above |

Issue

The current format of Table 4N aggregates forward charge and reverse charge liabilities, creating a misalignment with the separate disclosures required in Form GSTR-3B. This lack of segregation hinders accurate reconciliation and often creates artificial mismatches during departmental scrutiny.

Suggestion

Introduce separate reporting fields/columns within Table 4N to distinctly capture:

1. Tax payable under forward charge, and

2. Tax payable under reverse charge (RCM).

This will ensure consistency with GSTR-3B and GSTR-9 disclosures, improve traceability of liabilities, and enhance the accuracy of annual return reconciliation.

9. Exempted Supplies Reporting in GSTR-9

Table Reference: GSTR-9-Table 5D (Details of Exempted supplies made during the financial year)

Issue

Table 5D of Form GSTR-9 currently captures all ‘Exempted’ supplies in a single consolidated figure. However, under Rule 42 and 43 of the CGST Rules, not all exempt supplies attract the reversal of common Input Tax Credit (ITC). Specifically, supplies such as interest income (services by way of extending deposits, loans, or advances), No Supply, etc. are explicitly excluded from the value of exempt supply for the purpose of reversal calculations. The current consolidated reporting in Table 5D fails to distinguish between ‘Exempt supplies attracting reversal’ and ‘Exempt supplies NOT attracting reversal’. This structural limitation leads to automated notices where the department assumes the entire turnover in Table 5D as liable for ITC reversal, forcing taxpayers into unnecessary litigation to explain the exclusion of interest income and such other supplies which are not regarded as exempt supplies for the purposes of Rule 42 / 43.

Suggestion

Table 5D be divided into two parts as under:

| Table 5D | Exempted |

| Table 5D1 | Exempted Supplies for which reversal of common ITC is not required |

Justification

This bifurcation will facilitate the precise identification of supplies relevant for reversal computations thereby avoiding overstatement of exempt turnover.

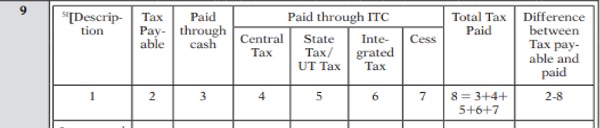

10. Concerns with Tax Payment Comparison in GSTR-9 (Table 9)

Table Reference: GSTR-9-Table 4N (Supplies and advances on which tax to be paid)

| N | Supply and advance on which tax is to be paid (H+M) above |

Table Reference: GSTR-9-Table 9 (Details of tax paid as declared in returns filed during the financial year)

Table Reference: GSTR-9-Table 10 & 11 (Particulars of the transactions for the financial year declared in returns of the next financial year till the specified period)

Issue

A new column has been added (vide Notification No. 13/2025-CT) in Table 9 of GSTR-9 to compare “tax payable” with “tax paid”. The “tax payable” figure is derived from Table 4N, which only includes transactions from the current financial year. If a taxpayer has paid tax in the current year that relates to a prior year (e.g., adjustments made via Table 10 or 11 of the previous year’s GSTR-9), the “tax paid” will be higher than the “tax payable”. This results in a negative difference, incorrectly suggesting an overpayment. Conversely, a downward adjustment for a prior year (less tax paid) will show a positive difference.

Suggestion

It is recommended that Table 9 be amended to introduce additional reporting fields/columns:

- A new column should be introduced in Table 9. This column would allow taxpayers to separately report the tax paid or reduced during the current financial year that specifically pertains to transactions from the last financial year.

- A dedicated column to capture tax payments made via Form DRC-03 during the financial year.

This solution would align the logic of Table 9 with the logic used for ITC in the new Table 6A1. It would permit a true comparison of tax payable versus actual tax paid for the current year and help reduce unnecessary litigation.

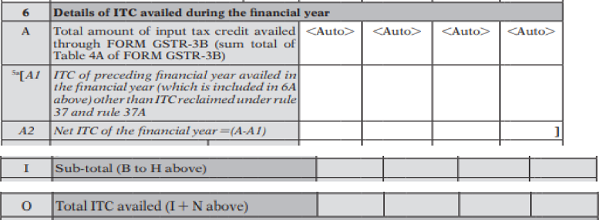

11. Net ITC Mismatch: GSTR-9 (Table 7J) vs. GSTR-3B (Table 4C) Table Reference: GSTR-3B -Table 4C (Net ITC Available)

Table Reference: GSTR-9-Table-6(Details of ITC availed during the financial year) & Table-7 (Details of ITC Reversed and Ineligible ITC for the financial year)

Table Reference: Table-7 (Details of ITC Reversed and Ineligible ITC for the financial year)

![]()

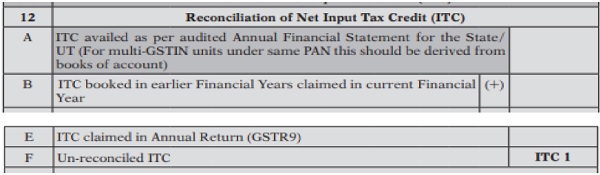

Table Reference: GSTR-9C-Table 12 (Reconciliation of Net Input Tax Credit (ITC))

Issue

The new amendments (vide Not. No. 13/2025-CT) have created a direct mismatch between the Net ITC reported in the GSTR-9 and the consolidated GSTR-3B returns. The current formula for GSTR-9, Table 7J (Net ITC Available for utilization), is Table 6O minus Table 7I. Since Table 6O represents only the ITC pertaining to the current financial year (excluding prior-year credit), the resulting figure in Table 7J does not reflect the total net ITC availed by the taxpayer during the year. However, the consolidated Net ITC as per GSTR-3B (Table 4C) for the financial year is the sum of Table 6A (Total ITC availed) minus Table 7I (Total ITC Reversed). This GSTR-3B figure includes the prior-year ITC claimed in the current year (which is now reported in Table 6A1).

The current formula creates an artificial discrepancy that is likely to trigger departmental notices (e.g., in Form ASMT-10). Tax authorities routinely conduct automated reconciliations comparing the Net ITC reported in Table 7J of Form GSTR-9 against the Net ITC declared in Table 4C of Form GSTR-3B.

Historical precedents indicate that such mismatches are a frequent trigger for scrutiny. Consequently, retaining the current formula imposes an unnecessary compliance burden on taxpayers, forcing them to engage in litigation or extended correspondence solely to resolve a difference that arises from the form’s structural logic rather than any actual tax non-compliance.

Consequential issue in GSTR 9C

The insertion of Table 6A1 in Form GSTR-9, which segregates ITC pertaining to the preceding financial year, has created a reconciliation discrepancy in Table 12 of Form GSTR-9C. Currently, Table 7J of GSTR-9 computes Net ITC exclusive of prior-period claims. However, Table 12E of GSTR-9C remains auto-populated from this restricted Table 7J figure. This creates a structural conflict with Table 12B of GSTR-9C, which is designed to capture ITC booked in earlier years but claimed in the current year. Consequently, this misalignment results in an artificial unreconciled difference in Table 12F, effectively rendering Table 12B of GSTR-9C redundant.

Suggestion

The formula for calculating Table 7J (Net ITC Available for utilization) in Form GSTR-9 should be amended to include the ITC of the preceding financial year. The new formula should be Table 7J = (Table 6O + Table 6A1) – Table 7I.

This amendment is crucial for alignment.

- Table 6O represents the total ITC for the current financial year.

- Table 6A1 represents the total ITC for the previous financial year. Adding (6O + 6A1) correctly computes the total ITC availed during the financial year, which is the same as the figure in Table 6A. Therefore, the revised formula (Table 6O + Table 6A1) – Table 7I becomes equivalent to Table 6A – Table 7I. This calculation will perfectly match the consolidated Net ITC figures from GSTR-3B (Table 4C), resolving the mismatch and preventing unnecessary notices.

Further, this solution will resolve the GSTR-9C mismatch by fixing the source data in GSTR-9. Once Table 7J reflects the correct, comprehensive total ITC, the auto-population into Table 12E of GSTR-9C will function as intended.

12. Lack of Specific Reporting Field for Reclaim of Excess ITC Reversed under Rule 42

Issue

Rule 42(2) of the CGST Rules, 2017 mandates that registered persons must recalculate input tax credit (ITC) reversals on common credits at the end of the financial year. If the aggregate of monthly reversals exceeds the calculated annual liability, the taxpayer is entitled to reclaim the excess amount. However, the current structure of Form GSTR-3B and Form GSTR-9 lacks a dedicated field to report this specific reclaim.

- In GSTR-3B: Taxpayers are forced to report this reclaim under Table 4(A)(5) (“All Other ITC”). Since this table is primarily for fresh credits flowing from invoices, adding reclaims here artificially inflates the figure, leading to a variance between GSTR-3B and GSTR-2B (which does not contain this reclaim value). This mismatch triggers automated scrutiny notices.

- In GSTR-9: There is ambiguity regarding whether to report this in Table 6H (Reclaimed ITC) or net it off against reversals in Table 7C, leading to inconsistent reporting practices.

Suggestion

It is recommended that:

1. Form GSTR-3B: A dedicated row be inserted (e.g., under Table 4(D) or a separate reclaim section) specifically for “ITC Reclaimed under Rule 42/43”, distinct from fresh ITC availment.

2. Form GSTR-9: A specific instruction or row be added to explicitly capture reclaims arising from annual re-calculation under Rule 42 / 43, ensuring it is not mixed with other reclaims or fresh credits.

Justification

Rule 42 / 43 provides a substantive right to reclaim excess reversals. The absence of a specific reporting mechanism forces taxpayers to use generic fields, causing artificial discrepancies between GSTR-3B and GSTR-2B. Providing a dedicated field will ensure accurate data capture, prevent unnecessary automated notices due to ITC mismatches, and streamline the annual reconciliation process.

13. Lack of Reporting Mechanism for Residual or Inadvertent ITC in Form GSTR-9 Issue

The recent amendment to Table 6M of GSTR-9 restricts reporting exclusively to ITC availed through Forms ITC-01, ITC-02, and ITC-02A. This change has effectively removed the earlier residual category used to report miscellaneous credits, such as inadvertent double claims, clerical errors, or ITC not attributable to specific heads (Inputs/Services/Capital Goods). Consequently, taxpayers are forced to misclassify these amounts under other heads (like Table 6B) just to match the auto-populated total in Table 6A. This distortion compromises data accuracy and triggers reconciliation disputes during audits.

Suggestion

It is suggested to insert a new dedicated row (e.g., Table 6N) in Part III of GSTR-9 titled “Any other ITC availed but not specified above”. This field would serve as a catch-all for miscellaneous or erroneous credits that do not fit into the specific categories of Inputs, Input Services, Capital Goods, or ITC-01/02 transfers.

Justification

The current framework forces taxpayers to fit irregular ITC into regular categories, which is technically incorrect and misleading. Introducing a separate residual row preserves the integrity of the specific tables while allowing a transparent disclosure of miscellaneous claims. This ensures accurate reconciliation between GSTR-3B and GSTR-9 without exposing compliant taxpayers to allegations of misreporting.

14. Absence of Specific Reporting Rows for Real Estate Tax Rates in Form GSTR-9C

Issue

Table 9 of Form GSTR-9C (Reconciliation of Rate-wise Liability) mandates the reconciliation of tax liability as per Audited Financial Statements with the tax liability declared in the Annual Return. However, the table currently lacks dedicated rows for reporting supplies taxable at the specific concessional rates applicable to the Real Estate sector. In standard industry practice, residential real estate projects attract GST at 1.5% (for affordable housing) and 7.5% (for other housing), which effectively translates to 1% and 5% after the mandatory 1/3rd land abatement. Due to this structural limitation, taxpayers in the real estate sector are forced to report these turnovers under the “Others” category or club them with different rate slabs. This often results in distorted reconciliation statements and triggers unnecessary discrepancy notices during departmental processing.

Suggestion

It is recommended that Table 9 of Form GSTR-9C be amended to insert separate, dedicated rows for tax rates of 1.5% and 7.5% (covering the effective 1% and 5% liability). This change would specifically cater to the unique rate structure mandated for the real estate sector.

Justification

The introduction of specific rows will allow real estate developers to accurately map their liability as per books with their GST returns without resorting to workarounds. This enhancement will ensure precise reconciliation, reduce artificial mismatches under the “Others” category, and streamline the audit process for both the taxpayer and the tax administration.

15. Ambiguity regarding “Audited Financial Statement” for Taxpayers Exempt from Audit under Other Statutes

Issue

Section 44 of the CGST Act mandates that every registered person (above a prescribed threshold) must furnish an annual return accompanied by a self-certified reconciliation statement, reconciling the value of supplies with the audited annual financial statement.

The provision explicitly states:

“Every registered person, other than an Input Service Distributor, a person paying tax under section 51 or section 52, a casual taxable person and a non-resident taxable person shall furnish an annual return which may include a self-certified reconciliation statement, reconciling the value of supplies declared in the return furnished for the financial year, with the audited annual financial statement for every financial year electronically, within such time and in such form and in such manner as may be prescribed”

However, a legislative vacuum arises for certain categories of taxpayers who are not liable to tax audit under any other statute. For instance:

- Section 10(26) of the Income Tax Act: Members of Scheduled Tribes residing in specified areas (e.g., North-East India, Ladakh) are exempt from Income Tax, and consequently, may not be liable for a tax audit under Section 44AB even if their turnover exceeds the GST Audit threshold (currently ₹5 Crores).

- Section 44AB: Under Section 44AB of the Income Tax Act, the tax audit threshold has been enhanced to ₹10 Crores (for digital businesses). However, the GST law mandates filing the Reconciliation Statement (Form GSTR-9C) for turnover exceeding ₹5 Crores. This creates a vacuum for taxpayers in the ₹5 Cr – ₹10 Cr bracket, who are exempt from statutory audit under the Income Tax Act but are compelled to file GSTR-9C, which effectively requires them to reconcile their GST returns with financial statements that are not legally required to be audited.

In such cases, the phrase ‘audited annual financial statement’ creates a deadlock. It is unclear whether these taxpayers are forced to conduct a separate audit solely for GST purposes, and if so, under which Act or auditing standards this audit is to be performed.

Suggestion

It is recommended that an Explanation or Proviso be inserted in Section 44 (or relevant Rule 80) to clarify that: “Where the registered person is not liable to get their accounts audited under any other law for the time being in force, the reconciliation shall be done with the Annual Financial Statement or Financial Statement maintained by such person, whether audited or not.”

Justification

The current provision inadvertently imposes a mandatory audit requirement on entities that are substantively exempt from it under their governing financial laws. Clarifying that “Books of Accounts” or “Unaudited Financial Statements” can serve as the basis for reconciliation in these specific cases will resolve the ambiguity regarding the “Applicable Act” for audit, prevent unnecessary compliance costs, and align GST requirements with the Income Tax framework.

16. Merger of GSTR-9 and GSTR-9C

Issue

Currently, the annual compliance framework requires the filing of two separate forms: GSTR-9 (Annual Return) and GSTR-9C (Reconciliation Statement). However, the requirement for certification of GSTR-9C by a Chartered Accountant or Cost Accountant is no longer mandatory, as it is now self-certified. Consequently, maintaining two separate returns leads to unnecessary complexity and redundancy in reporting.

Suggestion

Forms GSTR-9 and GSTR-9C be merged into a single return. To achieve this, the following key reconciliation tables from GSTR-9C should be incorporated directly into GSTR-9:

- Table 5: Outward Supply Reconciliation

- Table 9: Tax Reconciliation

- Table 12: Inward Supply Reconciliation

Merging these forms will simplify the compliance process for taxpayers and eliminate the duplication of data and effort currently required to file two separate documents.

The issue of differential turnover thresholds on merger of the two forms may be taken care of by conditional logic based on AATO. The specific tables incorporated from GSTR-9C (i.e., Table 5 – Outward Supply Reconciliation, Table 9 – Tax Reconciliation, and Table 12 – Inward Supply Reconciliation) should remain optional or disabled for taxpayers with an AATO up to INR 5 Crores.

C. REVERSE CHARGE MECHANISM (RCM)

17. Concerns in Sub-leasing of Residential Dwellings under Reverse Charge

Issue

Entry No. 5AA of Notification No. 13/2017-Central Tax (Rate) mandates that the service of renting a residential dwelling to a registered person shall attract GST under reverse charge. While this provision targets end-use renting, it creates a systemic anomaly in sub-leasing scenarios. In a typical sub-lease arrangement, the primary lessee (First Lessee) pays GST under reverse charge on the rent paid to the original landlord. However, when this First Lessee further sub-leases the property to another registered person (Sub-lessee), the liability on the outward supply once again falls under reverse charge on the Sub-lessee. Consequently, the First Lessee is burdened with accumulated Input Tax Credit (ITC) derived from the reverse charge paid in the first leg, which they are unable to utilize effectively as their corresponding outward supply attracts no forward tax liability.

Suggestion

The applicability of Entry No. 5AA be re-evaluated to address the sub-leasing value chain. A clarification or amendment be introduced to specify that reverse charge does not apply to the second leg of the transaction (sub-lease) where the supplier (First Lessee) is a registered person willing to discharge tax under the forward charge. Alternatively, the applicability of reverse charge be restricted based on the registration status of the original lessor to prevent this cascading effect.

Justification

The current structure creates a break in the credit chain, leading to the blockage of working capital for compliant taxpayers acting as intermediaries. Allowing the utilization of credit or shifting the liability to forward charge in sub-leasing scenarios ensures that GST remains a tax on value addition rather than a cost burden on the intermediate business, thereby eliminating double taxation and cascading costs.

18. Clarification on Scope of ‘Other than Residential Dwelling’ under RCM Entry no. 5AB

Issue

Entry No. 5AB of Notification No. 13/2017-Central Tax (Rate) mandates the payment of tax under Reverse Charge Mechanism (RCM) on the service of renting of any immovable property other than residential dwelling by an unregistered person to a registered person. However, the phrase ‘other than residential dwelling’ creates interpretational ambiguity regarding its scope. While it clearly includes commercial buildings (shops, offices, godowns), it is unclear whether the entry also encompasses vacant land or commercial plots leased for business purposes. Since ‘dwelling’ implies a built structure, the exclusion of residential dwellings could logically imply that all other forms of immovable property (including land) are covered. Conversely, it could be interpreted to apply only to ‘non-residential buildings.’ This lack of clarity creates uncertainty for registered recipients renting vacant plots from unregistered landowners regarding their liability to discharge tax under RCM.

Suggestion

It is suggested that a Clarification should be issued specifying the precise scope of the term ‘other than residential dwelling’ used in Entry 5AB. Specifically, it should be clarified whether this entry extends to the renting of vacant plots of land, or if it is restricted solely to constructed commercial/industrial premises.

Justification

Clarifying the scope is essential to prevent interpretational disputes during audits. If taxpayers interpret the entry to exclude land (paying no RCM) while the Department takes a contrary view, it will lead to demands for tax, interest, and penalties. A clear definition ensures uniform compliance across the trade and prevents litigation on what constitutes the class of property liable for RCM.

19. Concerns in Discharging Reverse Charge Liability for Immovable Property Located in a Different State

Issue

Entry no 5AB of Notification No. 13/2017-Central Tax (Rate) mandates that the renting of commercial immovable property by an unregistered person to a registered person attracts GST under the reverse charge. A critical statutory impasse arises when the registered recipient is located in one State while the immovable property and the unregistered supplier are located in another State.

For instance: Consider a scenario where a taxpayer registered in Delhi rents a commercial space (e.g., a warehouse or vacant plot) in Haryana from an unregistered supplier. The recipient utilizes this space exclusively for storage or ancillary purposes and does not effect any taxable outward supplies from this location. Pursuant to Section 12(3) of the IGST Act, 2017, the place of supply (POS) is the location of the property, i.e., Haryana. Since the supplier is also located in Haryana, the transaction is classified as an Intra-State supply under Section 8 of the IGST Act, attracting CGST + Haryana SGST. However, the recipient registered in Delhi cannot discharge this liability because the GST portal does not permit a taxpayer registered in one state to pay the SGST of another state in their Form GSTR-3B. Consequently, to legally discharge this reverse charge liability, the recipient is forced to obtain a separate registration (Casual Taxable Person or full registration) in Haryana solely for the purpose of paying this tax. This creates an unnecessary compliance burden and compels multi-state registration for a single expense line item.

Suggestion

To resolve this, a Simplified ‘Pay-Only’ Registration Mechanism should be introduced, functioning as follows:

Existing GST registered taxpayers should be given an option to opt for a ‘Single-Click PAN-Level Registration’ (or a Unique Assessment Number – UAN) for the State where the property is located (e.g., Haryana), directly from their Home State dashboard (e.g., Delhi).

Since the taxpayer is already fully KYC-verified in their Home State, the system should rely on the existing consolidated KYC dataset linked to the PAN. no fresh physical verification or document upload should be required for this limited-purpose registration.

This Registration should be restricted solely to the purpose of discharging inward RCM liabilities, without the burden of filing full-fledged outward supply returns.

Justification

Implementing a Unique Identification number like solution leverages the existing PAN-based trust framework. It allows the taxpayer to legally discharge the SGST of the destination state (satisfying the Place of Supply rules) without the administrative hassle of obtaining and maintaining a full-fledged registration for a passive activity. This ensures the State Government receives its due revenue while upholding the principle of Ease of Doing Business.

20. Unnecessary Cash Flow Blockage due to Mandatory Cash Payment of Reverse Charge Mechanism (RCM) Liabilities

Issue

The provisions under GST law mandates that tax liability under the Reverse Charge Mechanism (RCM) must be discharged exclusively via the Electronic Cash Ledger. Taxpayers cannot utilizing their accumulated Input Tax Credit (ITC) to settle this liability, even though the same amount becomes available as ITC immediately after payment. This creates an artificial working capital blockage, increases the cost of compliance, and places Indian businesses at a cash-flow disadvantage compared to their global peers, without generating any additional net revenue for the Exchequer.

Suggestion

It is suggested to amend Section 49(4) of the CGST Act, 2017 and relevant rules to allow the utilization of Electronic Credit Ledger (ITC) for the discharge of RCM liabilities. To ensure revenue neutrality and prevent any potential loss to the Exchequer, this facility may be restricted to taxpayers engaged exclusively in making taxable supplies (including zero-rated supplies).

Justification

With the GST regime having stabilized over the last eight years, the initial safeguards requiring cash payment to track compliance are no longer necessary. Permitting the use of the Electronic Credit Ledger to discharge RCM liabilities would align India with global best practices and remove a significant liquidity constraint for MSMEs and large corporates alike. This measure is revenue-neutral for the Exchequer, adheres to the principle of tax neutrality, and eliminates the administrative paradox of paying cash merely to claim the same amount back as credit.

D. E-WAY BILL

21. Concerns with Levy of Maximum Penalty (200%) for Minor Procedural Lapses in Transit

Issue

The CBIC issued Circular No. 64/38/2018-GST dated 14.09.2018, explicitly instructing field formations not to initiate detention proceedings under Section 129 for minor discrepancies (e.g., errors in PIN code, vehicle number, or HSN) where there is no intent to evade tax. However, field officers in some cases disregard this binding instruction. Vehicles are routinely detained, and the maximum penalty of 200% of tax is imposed for clerical errors or minor lapses (such as the expiry of an E-way bill by a few hours) that fall outside the narrow list of six exceptions provided in the Circular. This forces compliant taxpayers to engage in expensive litigation to seek relief that is already guaranteed by the Board’s instructions.

The exhaustive list given in the Circular only protects taxpayers from six specific errors (Spelling, PIN Code, Address, Doc Number, HSN, Vehicle Number). However, in real-world scenarios if an e-way bill expires by just 1 hour due to traffic, or if there is a minor route deviation, maximum penalty is levied on the ground that such deviations are not covered in the list of six lapses given in the Circular. This leaves the taxpayer no option but to approach the High Court.

Suggestion

It is suggested that instead of providing an illustrative list of ‘minor discrepancies,’ the Board may specify list of ‘Major Discrepancies’ that solely warrant detention under Section 129. Furthermore, fresh instructions should be issued mandating strict compliance with the same to prevent arbitrary action by field officers.

Justification

The Ease of Doing Business is severely compromised when field officers act contrary to Board instructions. Strengthening the implementation of this Circular and widening its scope will reduce unnecessary litigation and protect bona fide taxpayers from coercive recovery measures for technical faults.

22. Restricted Data Access on E-Way Bill Portal

Issue

The current infrastructure of the E-way Bill portal imposes severe restrictions on data accessibility, specifically:

1. Restricted Report Generation: The facility to generate bulk reports is often limited to a narrow time window (typically 8:00 AM to 12:00 PM), which does not align with standard business hours.

2. Limited Data Retention: The portal allows users to view or download E-way bill details only for the past 5 days. These limitations create a significant hurdle for taxpayers and transporters who operate on a 24×7 basis. The inability to access historical data (beyond 5 days) hinders monthly reconciliation with Forms GSTR-1 and GSTR-3B, forcing businesses to rely on third-party tools or daily manual downloads, thereby increasing the compliance burden.

Suggestion

The portal infrastructure be upgraded to support:

- 24×7 Availability (or significantly wider time bands) for report generation to align with the continuous nature of logistics operations.

- Extended Data Visibility: The period for viewing or downloading E-way bill details be extended to at least 30 days. Alternatively, an “Archive” or “History” section may be introduced to allow retrieval of older records for audit and reconciliation purposes.

Justification

Reconciliation is the backbone of GST compliance. Restricting access to data hampers the taxpayer’s ability to verify their own records against Government data. Removing these technical constraints is a low-cost, high-impact measure that directly improves the Ease of Doing Business and reduces inadvertent reporting errors.

23. Ambiguity in “Ship From” Location in E-way Bill

Issue

Under GST law, any place where goods are stored must be registered as an Additional Place of Business. However, field officers in some instances raise issues where the “Ship From” location is not a storage facility of the supplier but a transient dispatch point. Common legitimate scenarios include:

- “Bill-to-Ship-to” Transactions: Where goods are dispatched directly from the Vendor’s premises to the final customer.

- Import Clearances: Direct dispatch from Ports/ICDs to customers without entering the supplier’s warehouse.

- Job Work: Direct dispatch from a Job Worker’s premises.

28

Suggestion

It is suggested that a Circular be issued to clarify the treatment of the “Ship From” address in the E-way Bill:

1. Clarification on Exceptions: Explicitly state that the “Ship From” address need not be the Supplier’s registered Place of Business in specific non-storage scenarios such as Bill-to-Ship-to (Vendor’s premise), Direct Port Delivery, or registered Job Work premises.

2. Strict Enforcement for Storage: Reiterate that for actual Third-Party Warehouses where goods are stored, the taxpayer must register them as an Additional Place of Business to ensure compliance.

Justification

While the requirement to register a warehouse is clear under Section 2(85), extending this mandate to Vendor premises or Transit points (like Ports) creates an impossible compliance burden. Penalizing valid transactions where the “Dispatch From” location belongs to a third party (Vendor/Job Worker) and is already part of the GST ecosystem puts form over substance. A clarification will distinguish between “Storage” (requiring registration) and “Transit/Direct Dispatch” (not requiring registration), preventing arbitrary litigation.

24. Revenue Leakage via Refund Claims due to Collection of Section 129 Penalties through Home-State Login

Issue

A significant procedural gap is being observed in the enforcement of Section 129 (Detention and Seizure). When a conveyance is intercepted in a State where the taxpayer is not registered (e.g., Interception State), enforcement officers often direct the taxpayer to pay the penalty as “IGST” using their existing Home-State login credentials (via Form DRC-03 or voluntary payment) instead of creating a Temporary Registration in the Interception State.

Since the payment is made through the Home-State GSTIN, the statutory orders (Form GST MOV-07 and MOV-09) issued by the Interception State officer are often not visible or linked to the taxpayer’s electronic liability register in the Home State. Unscrupulous taxpayers exploit this disconnect by subsequently filing a refund application in their Home State, claiming the payment was made in error. The Home State jurisdictional officer, finding no corresponding demand order or Show Cause Notice (SCN) in their system, often processes the refund, treating it as an excess payment. This results in revenue leakage and renders the enforcement action futile.

Suggestion

A Circular be issued mandating the following procedure for all field formations:

1. Mandatory Temporary Registration: In cases of interception of unregistered persons (or persons registered in other states), officers must follow Section 25(8) of the CGST Act read with Rule 16A of the CGST Rules to suo-moto generate a Temporary User ID within the State of interception.

2. Linked Payment: The penalty under Section 129 must be demanded and collected only against this Temporary ID.

3. Prohibition on Home-State Challans: The system/officers should be restricted from accepting Section 129 penalty payments made via generic “Voluntary Payment” challans from the taxpayer’s Home-State login.

Justification

Mandating Temporary Registration ensures that the demand order (MOV-09) and the payment are legally locked within the jurisdiction of the Interception State. This prevents the taxpayer from claiming a refund in their Home State, as the Home State portal would have no record or jurisdiction over that Temporary ID. This measure is essential to secure Government revenue and ensure the finality of enforcement proceedings.

E. AUDIT

25. Concerns with Overlapping Audits and Parallel Proceedings

Issue

Despite the statutory intent of Section 6(2)(b) of the CGST Act to prevent parallel proceedings, taxpayers sometmes face simultaneous or consecutive verification proceedings by both Central and State authorities for the same issue in a financial year. It is observed that while one authority conducts a comprehensive ‘Audit’ under Section 65, the counterpart authority often initiates ‘Scrutiny’ or ‘Investigation’ proceedings on specific issues for the same period. This overlapping jurisdiction compels taxpayers to submit the same voluminous records twice, leading to significant duplication of effort and administrative costs.

Suggestion

It is suggested that a clear ‘Single Audit’ mechanism be enforced in line with the judicial mandate.

Exclusivity of Audit/Scrutiny: As clarified by the Hon’ble Supreme Court in M/s Armour Security (India) Ltd., actions arising from the audit of accounts or detailed scrutiny of returns must be initiated exclusively by the tax administration to which the taxpayer is administratively assigned. Cross-authority intervention in routine verification be prohibited.

Intelligence-Based Actions: While intelligence-based enforcement actions may be initiated by any authority, strict instructions must be issued to ensure they do not result in parallel proceedings on the same subject matter. Before initiating any investigation, the authority must verify if proceedings on the same subject matter are already pending with the counterpart authority.

Justification

The Hon’ble Supreme Court in M/s Armour Security (India) Ltd. (Civil Appeal No. 6092 of 2025) has explicitly held that audit and scrutiny functions are domain-specific to the assigned authority. Adhering to this principle respects the “Single Interface” mechanism. While intelligence-based actions are a valid exception, restricting them to distinct subject matters prevents harassment and ensures that compliant taxpayers are not penalized with redundant procedural requirements, thereby enhancing the Ease of Doing Business.

26. Fragmentation of Adjudication arising from Multiple SCNs for a Single Audit Issue

A single audit conducted under section 65 of CGST Act often results in multiple distinct observations or audit paragraphs. Currently, instead of issuing one comprehensive Show Cause Notice (SCN) for the entire audit period, officers in some instances issue separate SCNs for different issues (e.g., one SCN for RCM liability and another for ITC reversal). This problem is exacerbated when the monetary value of these separate SCNs falls under different adjudicating limits, leading to a scenario where linked issues arising from the same audit are adjudicated by different authorities (e.g., Superintendent to Joint Commissioner). This fragmentation results in disjointed proceedings, increased litigation costs, and the risk of contradictory legal interpretations in orders passed for the same taxpayer for the same period.

Suggestion

Instructions be issued that post-completion of an audit under Section 65 of CGST Act, a single, comprehensive SCN be issued covering all disputed observations for that audit period. Consequently, the adjudication for this common SCN must be undertaken by a Single Adjudicating Authority (determined by the total disputed amount), ensuring a holistic and consistent resolution of all issues.

Justification

Consolidating all audit observations into a single SCN ensures that the adjudicating authority has a complete view of the taxpayer’s compliance profile. It prevents the splitting of causes of action and ensures judicial consistency, saving both the Department and the taxpayer from the burden of multiple parallel hearings.

27. Issuance of Demand Notice (DRC-01) without Final Audit Report (ADT-02) Issue

Section 65(6) of the CGST/SGST Act mandates that upon the conclusion of an audit, the proper officer must inform the registered person of the finalized findings via Form ADT-02. The standard procedure requires that draft observations be reviewed (often by a Monitoring Committee) before the Final Audit Report is issued, ensuring that only sustainable objections result in a Show Cause Notice (SCN).

However, in certain instances—particularly during departmental audits— proceedings are initiated without this intermediate step, possibly due to the constraints of impending limitation periods. In such cases, a summary SCN issued in Form DRC-01 based merely on draft observations, without first issuing the ADT-02. This effectively skips the finalization stage, depriving the taxpayer of their statutory right to know the confirmed findings and reconcile them before a formal demand is crystallized.

Suggestion

It is suggested that the GST Portal functionality be modified to technically restrict the generation of a DRC-01 (in cases marked as ‘Audit’ under Section 65) unless a valid ARN of a generated ADT-02 is linked to it. This “hard-stop” will ensure that all formations, including State authorities, strictl adhere to the statutory sequence of Audit Conclusion (ADT-02) → Demand Generation (DRC-01), ensuring compliance with due process norms such as those prescribed in the Guidelines for issuance of SCN – Delhi GST [F. No. 1(2)/DTT/L&J/Misc./2019-20/77-79 ] [Dated 01-02-2022], which mandate that SCNs be issued only after proper inquiry and ascertainment of facts.

Justification

The issuance of ADT-02 is not a mere formality but a substantive statutory requirement that marks the conclusion of the audit verification. jumping directly to a demand notice violates the principles of natural justice and the due process laid down in Section 65. Enforcing this sequence via the portal prevents procedural irregularities and reduces litigation arising from premature SCNs.

28. Standardized SOP for Audit

Issue

There is a lack of uniformity in the audit approach across different jurisdictions. Under Rule 101(3) of the CGST Rules, officers are empowered to require documents, but the absence of a standardized, exhaustive checklist results in subjective and inconsistent interpretations. There are several instances where the information sought extends beyond the standard scope, leading to requests for documents that appear unrelated to the specific GST compliance under review. This lack of standardization leads to harassment, as a taxpayer with branches in multiple states faces completely different documentation standards for the same business profile.

Suggestion

A Uniform Audit Checklist and Standard Operating Procedure (SOP) be issued and be made binding on all formations.

1. The document list be exhaustive; demanding documents outside this list should require specific supervisory approval.

2. All audit proceedings, including the issuance of the Audit Memo (ADT-01), exchange of observations, and submission of replies, must be conducted exclusively through a Centralized Online Audit Module to minimize physical interface and ensure transparency.

Justification

Standardization is key to a fair tax regime. An exhaustive checklist limits discretionary power and ensures that audits remain focused on tax compliance rather than becoming an intrusive, open-ended investigation into the taxpayer’s entire business operations.

F. REFUNDS

29. Accumulation of ITC due to Subsidy-Induced Valuation Gap Issue

The accumulation of Input Tax Credit (ITC) is on account of statutory price controls exercised by the Government via subsidies, which artificially suppress the taxable value of output supplies. This structural anomaly is best illustrated by the recent developments in the Fertilizer Industry. Although the GST Council (in its 56th Meeting) rationalized the tax rates for key inputs (like Ammonia and Sulphuric Acid) from 18% to 5% to align with the output rate, this measure has not resolved the accumulation issue. Even with aligned rates, the ‘Inverted Duty Structure’ effectively persists because input tax is paid on the full commercial price, while output tax is collected only on the subsidized MRP, creating a permanent valuation gap that rate rationalization alone cannot bridge.

Despite the rate alignment (Input @ 5% and Output @ 5%), manufacturers suffer from massive ITC accumulation. This creates a “Value Inversion” trap: GST is paid on the full commercial cost of raw materials, but output tax is collected only on the subsidized, low MRP. Since the input tax quantum consistently exceeds the output tax liability, the credit accumulates permanently.

However, refund cannot be claimed as Section 54(3)(ii) of CGST Act, 2017 allows refund only in case of inversion arising out of rate difference.

The purpose of the subsidy is effectively defeated when taxpayers are unable to claim a refund of the credit that accumulates as a direct result of the price control mechanism

Suggestion

It is suggested that the refund benefit under the ‘Inverted Duty Structure’ be extended to industries where the taxable value of supplies is reduced due to Government subsidies.

Justification

Allowing the inverted duty refund on in case of subsidized outward supplies will ease the flow of working capital, enhance the Ease of Doing Business and will by aligned with the overall objective of supporting the subsidized industries.

30. Standardisation in GST Refund Documentation

Issue

A major challenge faced by taxpayers in the GST refund process is the absence of uniformity across field formations. Officers often ask applicants to repeatedly submit the same documents, even when such documents were already furnished with earlier refund applications or are readily available on the GST portal. This inconsistent approach not only creates administrative burden but also leads to avoidable delays, increased compliance costs, and uncertainty for taxpayers.

Suggestion

A standardised, legally-recognised document checklist be introduced for all refund categories, aligned with the list already prescribed in Master Circular No. 125/44/2019–GST, as amended by Circular No. 135/05/2020–GST.

To ensure consistency, this document list be formally incorporated into the GST Rules or statutory framework, preventing discretionary requests for additional or repetitive documents.

Justification

The lack of uniformity in GST refund documentation leads to repetitive and unnecessary requests from different field officers, even for documents already submitted or available on the GST portal, thereby, introducing a standardised document checklist would ensure uniform procedures across jurisdictions, and make the refund process more transparent and efficient and would improve the overall ease of doing business under GST.

31. Inclusion of Input Services and Capital Goods in Inverted Duty Refunds

Issue

Under the present framework of Section 54(3) of the CGST Act read with Rule 89(5) of the CGST Rules, refund of unutilised input tax credit under the inverted duty structure is restricted only to input goods. Input services and Capital goods are expressly excluded from the refund formula. This exclusion leads to partial credit accumulation, disrupting the intended neutrality of GST as a value-added tax.

The issue has become more pronounced after the rate rationalisation effective from 22 October 2025, which has increased inversion in several service-intensive sectors. As a result, businesses with significant input service components face deeper working-capital blockage and an artificial cost burden contrary to the design of GST.

Suggestion

Rule 89(5) be amended to include input services and capital goods within the scope of refund under the inverted duty structure.

Justification

Allowing refund of inputs, input services and capital goods will bring much-needed parity, especially for sectors where service inputs constitute a major portion of operational costs. Such an amendment will correct the distortion created by the current formula, align the refund mechanism with the foundational neutrality principle of GST.

32. Aligning GST Refund Documentation with Modern Banking Frameworks Issue

In the case of export of services, refund sanctioning authorities continue to insist on submission of Foreign Inward Remittance Certificates (FIRCs) or Bank Realisation Certificates (BRCs) as the sole acceptable proof of receipt of payment in convertible foreign exchange. However, under the current FEMA and banking framework, authorised dealer banks typically issue Foreign Inward Remittance Advices (FIRAs) or provide digitally authenticated remittance confirmations (such as SWIFT messages), and FIRCs/BRCs are no longer routinely generated. The rigid insistence on FIRCs/BRCs—despite the availability of legitimate digital remittance evidence—results in unnecessary delays, deficiency memos, and rejection of refund claims, even where export proceeds have been duly received and recorded through authorised channels.

Suggestions

- Recognise Modern Digital Remittance Documents: The requirement for FIRC/BRC as the only acceptable evidence be relaxed. Documents such as FIRA, SWIFT confirmations, or other digitally authenticated inward remittance advices issued by authorised dealer banks under FEMA should be accepted as valid proof of receipt of foreign currency.

- Integrate GST Refund Mechanism with RBI’s EDPMS: The GST refund processing system should be integrated with the RBI’s Export Data Processing and Monitoring System (EDPMS) to enable automatic, system-based validation of inward remittances, thereby reducing manual uploads and eliminating repetitive documentation.

Justification

The current insistence on manual FIRCs/BRCs creates a procedural deadlock, as the banking sector under FEMA has transitioned to digital evidences like FIRA and SWIFT. Rejecting these valid proofs prioritizes procedural form over the substantive requirement of ‘receipt of payment’ mandated by Section 2(6) of the IGST Act. Aligning GST procedures with modern banking realities and integrating with RBI’s EDPMS would ensure a tamper-proof verification trail, eliminating administrative bottlenecks while upholding the integrity of export realizations.

33. Reform of RFD-03 Issuance to Prevent Procedural Denial of Refunds Issue

In many cases, refund sanctioning authorities issue Deficiency Memos (Form RFD-03) repeatedly, often for minor or procedural concerns. This practice restarts the refund filing cycle each time and continues until the statutory time limit of two years expires, effectively depriving taxpayers of their legitimate refund claims. The absence of a time-bound or standardized approach to acknowledging refund applications allows repeated issuance of RFD-03 to be misused as a tool for deferring or avoiding the acceptance of refund claims. This undermines the purpose of the refund framework and results in unnecessary compliance burden, uncertainty, and cash-flow blockage for taxpayers.

Suggestion

- Acknowledgment of refund claims (Form RFD-02) be generated automatically upon submission of a complete application in Form RFD-01.

- Any deficiencies or clarifications required thereafter may be examined through the adjudication process using Form RFD-08 (show cause notice), without resorting to repeated issuance of RFD-03.

Automatic Interest on Delayed Refunds: The system should be configured to automatically calculate and credit interest to the taxpayer’s bank account for any delay beyond the statutory 60-day period (similar to the mechanism in Income Tax), without requiring the taxpayer to file a separate claim or application for the same.

Justification

The above mechanism would prevent misuse of deficiency memos, protect the taxpayer’s statutory time limits, and ensure that refund applications are processed on merits rather than rejected on procedural grounds.

34. Introduction of a Scheme Analogous to MOOWR (Manufacturing and Other Operations in Warehouse Regulations, 2019) for Small and Medium Export of Services under GST

Issue

Currently, service exporters face significant liquidity challenges due to the upfront payment of GST on input services and capital goods. While the law provides for a refund of unutilized Input Tax Credit (ITC) under Rule 89(4) or export without payment of IGST under Bond/LUT, the refund process is often delayed (averaging 60–90 days), leading to substantial working capital blockage. Unlike the goods sector, which benefits from schemes like MOOWR (Manufacturing and Other Operations in Warehouse Regulations, 2019) allowing duty-free procurement for export production, service exporters—especially MSMEs in high-growth sectors like IT/ITeS, R&D, and Consulting—lack a comparable deferment mechanism.

There is now a growing need to introduce a new scheme under the Goods and Services Tax (GST) framework, modeled on the Manufacturing and Other Operations in Warehouse Regulations (MOOWR), 2019, but specifically designed to facilitate the export of services.

Suggestion

This proposed scheme—tentatively titled Services Export Operations Without Payment of Tax (SEOWOT) or a similar nomenclature—aims to revolutionize the export ecosystem for service providers by enabling seamless operations without the upfront payment of GST on input services or procurements. Drawing parallels from the success of MOOWR in the goods sector, this initiative would address longstanding pain points in service exports, which currently contribute significantly to India’s foreign exchange earnings yet grapple with liquidity constraints and compliance burdens.

Core Objectives and Rationale

The primary thrust of SEOWOT would be to facilitate smooth operations for service exporters, particularly in high-growth sectors such as IT/ITeS, consulting, R&D, financial services, and digital platforms. Under the extant GST framework, exporters of services are entitled to refund of unutilized Input Tax Credit (ITC) on inputs/input services under Rule 89(4) of CGST Rules, or they may export under bond/LUT (Letter of Undertaking) without paying IGST, claiming refunds later. However, this often results in working capital blockage due to delayed refunds (average processing time: 60-90 days).

By mirroring MOOWR’s deferment mechanism—where manufacturers can procure goods without payment of duty for warehouse-based operations— SEOWOT would allow eligible service exporters to:

- Procure input services (e.g., cloud computing, software licenses, professional consultancy, telecom) and capital goods (e.g., servers, laptops) without payment of GST.

- Undertake export-oriented operations in a designated “virtual warehouse” or registered premises, with deferred tax liability until actual export realization.

- Avail automatic ITC accumulation in an electronic ledger, convertible to refunds upon proof of export (e.g., via Form GSTR-1, FIRC, or e-BRC).

- This would minimize operational costs by eliminating the need for upfront tax outflows, reducing effective cost of capital by 10-15% for MSME exporters, as per industry benchmarks.

Justification

Introducing SEOWOT would align the service export ecosystem with the facilitation measures already available to goods manufacturers. By eliminating upfront tax outflows, the scheme would significantly improve liquidity for MSME exporters, reduce the administrative cost of refund processing for the Department, and make Indian services more price-competitive in the global market.

G. INPUT TAX CREDIT (ITC)

35. Lack of Mechanism to Verify Supplier Tax Payment

Issue

The GST portal currently lacks a mechanism to verify whether suppliers have actually discharged tax liability in GSTR-3B for the invoices reported in their GSTR-1. While GSTR-2B displays the invoices uploaded by suppliers, it does not provide any linkage to confirm whether the corresponding tax has been paid. This absence of back-end reconciliation between GSTR-1 (outward supplies) and GSTR-3B (tax payment) results in significant uncertainty for bona fide recipients. Genuine taxpayers often face denial of input tax credit solely due to supplier noncompliance, despite having no independent means to verify the supplier’s tax payment status. This creates compliance risk, undermines the trust-based credit system, and increases the possibility of disputes.

Suggestion

It is suggested that Section 16(2)(c) of the CGST Act, which mandates that Input Tax Credit (ITC) can only be availed if the tax has been actually paid to the Government, be suitably amended.

Justification

The rationale for this provision was valid when the GST framework lacked real-time oversight. However, the current ecosystem has evolved significantly with the introduction of Auto-Populated Form GSTR-3B (derived from GSTR-1), where any variance between declared liability and actual payment is immediately visible to the Department. Furthermore, automated enforcement mechanisms like Rule 88C (Intimation in Form DRC-01B) ensure that such payment gaps are instantly flagged and scrutinized at the supplier’s end.

Since the system is now robust enough to detect and resolve non-payment by the supplier in real-time, enforcing Section 16(2)(c) against a bona fide recipient—for a default that is already under the officer’s radar. Crucially, even if the Department later recovers the tax from the supplier, the buyer is never informed. As a result, they remain unaware that their credit eligibility is restored, often causing them to miss the strict deadline for claiming ITC (Section 16(4)). Therefore, recovery efforts should focus solely on the supplier, and a buyer’s right to credit should not depend on back-end payment verifications they cannot see.

36. Mechanism for Re-Credit of 1% Tax Paid Through Electronic Cash Ledger Under Rule 86B

Issue

Rule 86B restricts the utilisation of input tax credit by mandating payment of at least 1% of the tax liability through the Electronic Cash Ledger (ECL) in specified cases. However, there is currently no mechanism on the GST portal to claim re-credit of this mandatory 1% payment where the taxpayer has already discharged the full tax liability through the Electronic Credit Ledger (ECrL). This results in an unintended excess cash outflow and amounts to collection of tax, since the additional 1% paid via ECL does not represent an actual tax liability. The absence of a re-credit mechanism also leads to non-compliance with the intended framework of Rule 86B and creates reconciliation and cash-flow challenges for taxpayers.

Suggestion

A dedicated facility should be introduced on the GST portal to enable taxpayers to reclaim or re-credit the 1% tax mandatorily paid through the Electronic Cash Ledger pursuant to Rule 86B. This may be implemented through a special column or re-credit functionality, linked to the DRC-03B mechanism proposed for reverse charge adjustments. Such a system would ensure that the mandatory cash payment under Rule 86B does not result in unintended excess tax collection and would align the compliance framework with the economic intent of the rule. Establishing this mechanism will improve cash-flow neutrality, reduce administrative disputes, and ensure consistency in tax accounting and reporting.

Justification

Rule 86B requires taxpayers to pay at least 1% of their tax liability through the Electronic Cash Ledger, even when sufficient input tax credit is available. Businesses face avoidable cash outflows, reconciliation issues, and unintended excess tax payments that do not reflect any real tax obligation, thereby, introducing a dedicated re-credit facility would ensure that the mandatory payment does not translate into permanent cash blockage. Such a mechanism would maintain cash-flow neutrality, promote accurate tax accounting, and reduce future disputes, while aligning the compliance process with the true intent of Rule 86B.

37. Inability to Transfer Unutilized ITC Across States in Case of Mergers via Form ITC-02

Issue