Demystifying the GST: A Comprehensive Legal Overview of India’s Monumental Tax Reform

1.0 Introduction:

For decades, India’s indirect tax landscape was a fragmented and complex web. Businesses, especially those operating across state lines, navigated a daunting labyrinth of central excise, state-level VAT, octroi, entry tax, and service tax, each with its own compliance rules. This created a cascading “tax on tax” effect, inflated costs, and hampered the dream of a unified national market. The solution arrived on the historic midnight of July 1, 2017: the Goods and Services Tax (GST).

The launch of the Goods and Services Tax (GST) on 1st July 2017 was not merely a change in tax law; it was a revolutionary reform that transformed India’s indirect tax system. By bringing together multiple state and central taxes under one umbrella, GST has paved the way for a “One Nation, One Tax, One Market” structure.

Hence more than just a tax change, GST represents a fundamental restructuring of India’s federal financial architecture. This blog provides a detailed legal overview, delving deep into its meaning, constitutional foundations, key components, and its profound impact on the Indian economy.

2.0 Meaning and Definition of GST:

GST is a destination-based, multi-stage, comprehensive indirect tax levied on every value addition. To truly understand its revolutionary nature, we must dissect this definition:

- Destination-Based Consumption Tax: Unlike previous origin-based taxes (like VAT, which was collected by the state of manufacture), GST is collected by the state where the goods or services are ultimately consumed. This aligns tax revenue with the consuming state’s economy, ensuring a fairer distribution of resources across India.

- Multi-Stage Levy: The journey of a product from raw material to consumer involves multiple stages: manufacture, wholesale, distribution, and retail. GST is levied at each of these stages, but its design ensures that the final burden does not pile up.

- Value Addition: This is the core mechanism that prevents cascading. If a manufacturer buys raw materials for ₹100 (plus GST) and adds value of ₹50 to create a new product, the tax is only levied on the final sale price minus the cost of inputs. The tax already paid on the raw materials (₹100) is claimed as a credit.

- Legal Definition: Article 366 (12A) of the Constitution defines GST as “any tax on supply of goods, or services or both except taxes on the supply of the alcoholic liquor for human consumption.” It is legally characterized not by a single phrase but by the entire framework that taxes the “supply” of anything—goods, services, or a combination—at a specified rate, with a robust mechanism for input tax credit across the entire supply chain.

- The Constitutional Foundation:

Implementing GST required a monumental shift in the Constitution’s financial framework. The Seventh Schedule of the Indian Constitution clearly divided taxing powers:

- Union List (Entry 84): Parliament had exclusive power to levy taxes on the manufacture of goods (Excise Duty) and on services (Service Tax).

- State List (Entry 54): State Legislatures had exclusive power to levy taxes on the sale of goods (VAT) and on the entry of goods into a local area (Entry Tax, Octroi).

This clear division made a dual, concurrent tax system impossible without constitutional change.

The 101st Constitutional Amendment Act, 2016 was the pivotal instrument that made GST a reality. Its key provisions include:

- Insertion of Article 246A: This new article grants concurrent power to both Parliament and the State Legislatures to make laws with respect to GST. However, Parliament has exclusive power to levy IGST on inter-state supplies and imports.

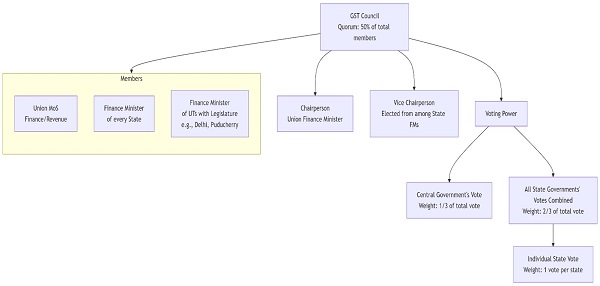

- Insertion of Article 279A: This article mandated the creation of the GST Council within 60 days of the commencement of this Article. The Council, a quintessential example of cooperative federalism, was tasked with making recommendations on all aspects of GST.

- Definition of the GST Model: The amendment provided the legal basis for the dual GST model:

- CGST (Central GST): Levied by the Centre on intra-state The revenue is collected by the Centre.

- SGST (State GST): Levied by the State on intra-state The revenue is collected by the State.

- IGST (Integrated GST): Levied by the Centre on inter-state supplies and imports. The IGST collected is then apportioned between the Centre and the Destination State, ensuring the destination-based principle is upheld.

This amendment fundamentally redefined fiscal federalism in India, making Centre-State collaboration the cornerstone of indirect taxation.

4.0 The Engine of Federal Cooperation: The GST Council

The GST Council is arguably the most powerful federal institution in India’s financial history, designed to ensure continuous harmony between the Centre and the States.

4.1 Expanded Structure and Composition:

- Chairperson: The Union Finance Minister.

- Vice-Chairperson: Nominated from among the Finance Ministers of the States. This position rotates among the states.

- Members:

- The Union Minister of State in charge of Revenue or Finance.

- The Finance Minister/Taxation Minister of each state government and union territory with a legislature (e.g., Delhi, Puducherry).

4.2 Key Functions and Responsibilities:

The Council’s recommendations are crucial on a wide range of issues, including:

- The goods and services that may be subjected to or exempted from GST.

- The model GST Laws, principles of levy, apportionment of IGST, and principles related to place of supply.

- The GST rate structure, including floor rates and bands.

- Special provisions for special category states (like the North-Eastern states) and states like Jammu & Kashmir.

4.3 Voting Mechanism and Power Dynamics:

- The Centre has 1/3rd of the total votes cast.

- All the states combined have 2/3rds of the total votes cast.

- Every decision of the GST Council requires a 3/4th majority of the weighted votes cast.

The Predecessor and the Problem: A Deeper Look at VAT

The Value Added Tax (VAT) system, implemented state-wise from 2005, was an improvement over the earlier sales tax regime but was plagued with inherent flaws that GST was designed to fix:

- The Cascading Effect (Tax on Tax): VAT was levied on the value of the product including the cost of previous taxes (like non-creditable Central Excise Duty). For example, a manufacturer paid excise duty on his product. When a wholesaler bought it, he paid VAT on a price that included the excise duty. This double taxation embedded tax costs into the price of goods, increasing the final cost for the consumer.

- A Fragmented Economic Market: Each state had its own VAT Act, with different rates, exemptions, and compliance procedures. This created significant hurdles for inter-state trade. The Central Sales Tax (CST) levied on inter-state movement of goods was a cost that could not be set off against local VAT, making products more expensive outside their state of origin.

- The Goods-Services Divide: VAT was primarily a tax on goods. Services were taxed separately by the Centre under Service Tax. This dichotomy meant a business could not claim credit for taxes paid on input services against its VAT liability on goods, and vice-versa. This broken credit chain was a major inefficiency.

GST solved this by creating a unified tax for both goods and services, enabling a seamless flow of input tax credit across all stages and across all state borders, thereby eliminating the cascading effect.

| Feature | VAT | GST |

| Tax Scope | Only Goods | Goods & Services |

| Taxation Base | Origin-based | Destination-based |

| Cascading Effect | Present | Eliminated via ITC |

| Uniformity | Different rates across states | Uniform national system |

6.0 Foundational Terminology in GST: A Legal Lexicon

- Supply (Section 7 of CGST Act): This is the taxable event under GST. It is an all-encompassing term that includes sale, transfer, barter, exchange, license, rental, lease, and disposal. It also includes import of services for a consideration, whether or not in the course of business.

- Input Tax Credit (ITC) (Section 16): The cornerstone of the GST mechanism. It is the credit a registered person can claim for the GST paid on any purchase of goods or services used or intended to be used in the course or furtherance of business. This credit can be used to offset the GST liability on output supplies. ITC ensures that tax is only paid on the value added at each stage.

- GSTN (GST Network): A non-profit, non-government company that provides the shared IT infrastructure and services to all stakeholders. It handles the entire technological ecosystem for registration, return filing (through forms like GSTR-1, GSTR-3B), tax payment, and ITC matching. It is the digital backbone without which GST’s compliance structure would not function.

- HSN Code (Harmonized System of Nomenclature): An internationally accepted standard (developed by the World Customs Organization) for classifying goods. Under GST, businesses with a turnover of over ₹5 crore must use 6-digit HSN codes, while those below can use 4-digit codes. This brings uniformity.

- SAC Code (Services Accounting Code): A system similar to HSN, developed by the Central Board of Indirect Taxes and Customs (CBIC) for classifying services under GST.

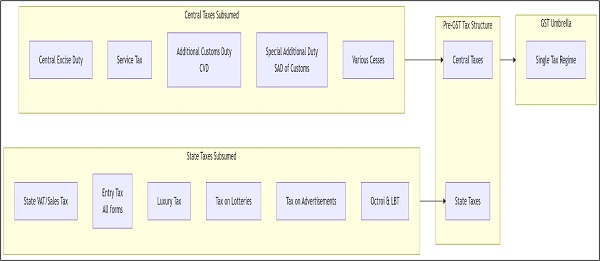

7.0 The Great Subsumption: Taxes Replaced by GST

One of the primary objectives of GST was to create a single tax by merging a multitude of central and state levies. The following taxes were subsumed:

Important Note on Exclusions: While the intent is to bring “all” goods and services under GST, five petroleum products (crude, petrol, diesel, ATF, natural gas) and alcohol for human consumption are temporarily kept out of GST’s scope as per Article 366(12A) of the Constitution. They are still taxed under the old VAT/Excise system. Basic Customs Duty is also levied separately on imports.

8.0 A Balanced View: Objectives, Tangible Benefits, and Persistent Challenges:

8.1 Core Objectives:

- One Nation, One Market, One Tax: To integrate India into a single, unified common market by removing state barriers.

- Eliminate Cascading: To ensure tax is levied only on value addition at each stage through a seamless credit mechanism.

- Boost Compliance and Revenue: To widen the tax base by bringing more businesses into the formal economy, thereby increasing tax revenues for governments.

- Enhance Competitiveness: To reduce the overall tax burden on goods, making Indian products more competitive in the international market.

8.2 Documented Benefits:

- Reduced Logistics and Inventory Costs: The removal of inter-state check-posts under the e-way bill system has drastically cut transportation time and costs.

- Formalization of the Economy: The digital, invoice-matching system of GST has reduced cash transactions and brought a large number of SMEs into the organized sector.

- Simplified Compliance: For pan-India businesses, dealing with one authority (GST) and one law is simpler than complying with multiple state VAT laws and central excise/service tax.

- Consumer Benefits: The removal of cascading has, in many sectors, led to a reduction in the overall tax burden on end consumers.

8.3 Persistent Challenges and Drawbacks:

- Technical Hurdles: The GSTN portal, especially in the initial years, faced frequent outages and technical glitches, causing compliance headaches.

- High Compliance Burden for SMEs: The requirement for regular monthly/quarterly return filings, digital invoice generation, and adherence to complex procedures has been challenging for small businesses with limited resources.

- Multi-Tier Rate Structure: The presence of multiple tax slabs (0%, 5%, 12%, 18%, 28%) and a special rate for diamonds (0.25%) and luxury/sin goods, coupled with cesses, complicates the system. This deviates from the ideal of a simple, single-rate tax.

- Frequent Amendments: While the GST Council’s responsiveness is a strength, the sheer volume of frequent notifications, circulars, and rate changes creates uncertainty and a need for constant vigilance among businesses.

- Pending Inclusions: The fact that key products like petroleum and alcohol remain outside GST means the dream of a truly “comprehensive” tax is yet to be fully realized.

9.0 Conclusion:

The implementation of the Goods and Services Tax is arguably the most significant socio-economic reform in India since liberalization in 1991. It is a testament to India’s ability to undertake complex, federal reforms through dialogue and consensus.

While the journey has been marked by initial turbulence, the long-term trajectory is positive. The GST Council continues to be a dynamic institution, fine-tuning the law based on stakeholder feedback. As the system matures, glitches are ironed out, and compliance becomes more ingrained, GST is poised to fully deliver on its promise of transforming India into a truly integrated economic powerhouse. It remains a work in progress, but its foundational impact on the Indian economy is undeniable and profound.

10.0 REFERANCES:

♦ V.S. Datey, GST Law & Practice with Customs & FTP (Taxmann Publications Ltd., New Delhi, 2018).

♦ Shailesh Kumar Dubey and Dr. Rajeev Kumar Sinha, “A comprehensive study based on India’s GST Amendments and its Impact”, 11, Issue 6, International Advanced Research Journal in Science, Engineering and Technology 160 (2024).

♦ Tek Chand, “An Overview of Existing Issues and Challenges in GST Regime in India”, Volume 9, Issue 9, International Journal of Novel Research and Development 645(2024).

♦ Krishna Samaddar, “A comprehensive study on the concept of GST and its impact on Indian economy”, Volume 6, Issue 2, International Journal of Creative Research Thoughts (IJCRT) 627(2018).

♦ “What is GST in India? Meaning, Types, and Registration” , available at : https://www.bajajfinserv.in/gst#:~:text=Frequently%20asked%20questions,What%20is%20GST%3F,structure%20for%20businesses%20and%20consumers, last viewed on 4th September 2025.

♦ “Goods and Services Tax: What is GST in India?”, available at: https://cleartax.in/s/gst-law-goods-and-services-tax, last viewed on 4th September 2025.

♦ “Overview of GST”, available at: https://www.gstcouncil.gov.in/sites/default/files/gst-knowledge/Overview-of-GST.pdf, last viewed on 4th September 2025.

♦ “Goods and Services Tax (GST): Definition, Types, and How It’s Calculated”, available at: https://www.investopedia.com/terms/g/gst.asp, last viewed on 4th September 2025.

♦ “What is GST? (Goods and Services Tax)”, available at: https://groww.in/p/tax/gst, last viewed on 4th September 2025.