1. The much-awaited ITR-3 form is now available online on the Income Tax portal, effective from July 30, 2025. This Form is often considered the most complicated income tax return form. But don’t worry — the author is here to make it very simple. This article aims to simplify the understanding of each Table in ITR 3.

2. Just like a strong foundation is essential to build a house, a smooth ITR-3 filing starts with correctly filling out the “General Information” Section. The General Information Section is the basis of the Income Tax Return, and any mistake in this section can lead to problems later.

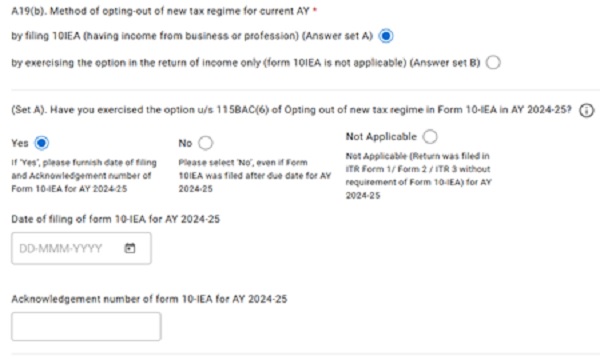

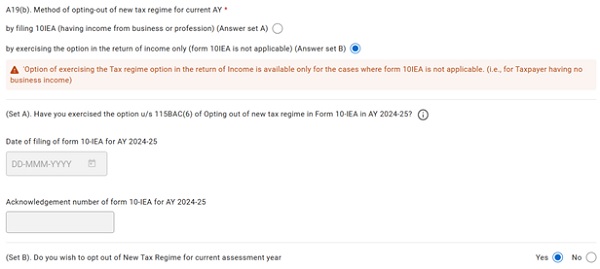

3. Let’s begin with Table A19(b) under the ‘General Information Section. This Table is meant for reporting the decision to opt out of the default new tax regime and adopt the old regime instead.

The new Tax Regime, introduced from Financial Year 2020–21, offers lower tax rates in exchange for foregoing most of the deductions and exemptions available under the old regime. It aims to simplify the tax structure for taxpayers.

With effect from FY 2023–24, the Finance Act 2024 has amended Section 115BAC, making the new tax regime the default option for taxpayers. However, the Act provides flexibility to switch from the default new regime to the old regime.

Individuals with business or professional income are allowed to switch regimes only once in their lifetime. In contrast, individuals with salary income or any other type of income can choose between the old and new regimes every assessment year when filing their return.

4. REPORTING CHANGE OF REGIME IN ITR 3: The Path is Dashboard > e-File > Income Tax Return > Select Status > Filing Return for AY 2025–26 > ITR-3. Then move to Select Schedule > Return Summary > Part A – General Information > Filing Status > A19b.

Table A19(b) of ITR-3 may appear complex at first glance. Let’s break it down and simplify the concept through practical illustration in different scenarios.

5. SCENARIO 1: Ms. Sangeeta, engaged in F&O business, decided not to opt for the new tax regime in FY 2023–24. Since the new regime is the default from this year onward, she filed Form 10-IEA to opt out and continue under the old regime. Ms. Sangeeta wishes to continue under the old tax regime and does not intend to opt for the new regime in FY 2024-25 as well.

She simply needs to select ‘Answer Set A’ in Table A19(b) and provide the acknowledgment number and date of filing of Form 10IEA in FY 2023–24(AY 2024-25)

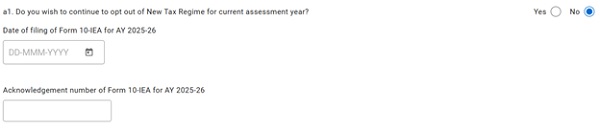

6. SCENARIO 2: In FY 2024–25, Ms. Sangeeta does not wish to continue with the old tax regime and chooses to switch to the new regime. Accordingly, she needs to file Form 10IEA within the due date, select ‘No’ in Table a1 of A19(B), and enter the acknowledgment number and filing date of the Form 10IEA for FY 2024-25.

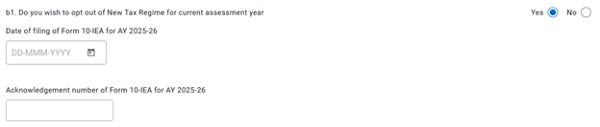

7. SCENARIO 3: Ms. Sangeeta had filed Form 10-IEA in FY 2023–24, intending to opt for the old tax regime, but the Form was submitted after the due date of return. As per the rules, Form 10-IEA must be filed within the due date to validly switch from the default new regime to the old regime. Since the filing was delayed, it is treated as not filed, and she continues to be taxed under the new regime by default.

7. SCENARIO 3: Ms. Sangeeta had filed Form 10-IEA in FY 2023–24, intending to opt for the old tax regime, but the Form was submitted after the due date of return. As per the rules, Form 10-IEA must be filed within the due date to validly switch from the default new regime to the old regime. Since the filing was delayed, it is treated as not filed, and she continues to be taxed under the new regime by default.

In FY 2024–25, Ms. Sangeeta now wishes to opt for the old tax regime. To do so, she must file Form 10-IEA for FY 2024-25 (AY 2025–26) within the due date. Select ‘Yes’ in Table b1 of ITR-3 and enter the details.

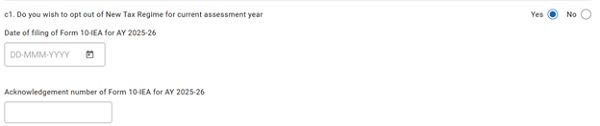

8. SCENARIO 4: Ms. Sangeeta was not engaged in any business or profession during FY 2023–24, so there was no requirement to file Form 10-IEA to opt for the old regime. However, from FY 2024–25, she has started dealing in F&O, which qualifies as business income. Since she intends to opt for the old regime in FY 2024-25, she must now file Form 10-IEA within the due date. Select ‘Yes’ in Table c1 of ITR-3 and enter the details.

9. SCENARIO 5: Ms. Sangeeta is not engaged in any business or profession and wishes to opt for the old tax regime. In this case, she needs to select ‘Answer Set B’ in Table A19(b) and click ‘Yes’ to confirm her choice.

9. SCENARIO 5: Ms. Sangeeta is not engaged in any business or profession and wishes to opt for the old tax regime. In this case, she needs to select ‘Answer Set B’ in Table A19(b) and click ‘Yes’ to confirm her choice.

However, if she wishes to continue under the default new tax regime, she simply needs to click ‘No’ in Table A1 under ‘ Set B.

10. SUMMARY: The following summary highlights key scenarios of tax regime changes and how they are to be reported

| Sl. | Scenario | Business / Profession Income | Regime Intended | From 10IEA required | Answer Set to Select | Table 19A1(b) option |

| (a) | FY 2023–24: Opted for the old regime and filed Form 10-IEA on time; wants to continue in FY 2024–25 | Yes | Old | Filed 2023-24 | Set A | Yes |

| (b) | FY 2024–25: Wishes to switch to the new regime | Yes | New | Required for switching (one-time option) | Set A | No |

| (c) | Filed Form 10-IEA in FY 2023–24 after due date (invalid); remains in the new regime | Yes | New (by default) | Not valid due to late filing | Set A | Yes |

| (d) | No business in FY 2023–24; starts F&O in FY 2024–25; wishes to opt for the old regime. | Yes | Old | Required in FY 2024–25 | Set A | Yes |

| (e) | No business/profession income; wishes to opt for the old regime | No | Old | Not Required | Set B | Yes |

| (f) | No business/profession income; continues in the default new regime | No | New | Not Required | Set B | No |

11. FORM 10IEA Form 10-IEA plays a crucial role in changing the tax regime. Let’s understand what this Form is and how it should be filed.

(a) From 10-IEA is a declaration made by the return filers for choosing the ‘Opting Out of New Tax Regime’ before the due date of return (15th of September 2025). Missing this filing means automatic enrollment into the new regime.

(b) Form 10-IEA is mandatory for taxpayers with business or professional income, particularly those filing under ITR-3 or ITR-4. This option can only be exercised once in a lifetime unless the taxpayer discontinues their business.

(c ) The Form requires details like PAN, assessment year, business status, IFSC units (if any), and a formal declaration.

(d) The Path to file Form 10IEA is: e file > Income Tax Forms> File Income Tax Forms> Select Form 10IEA > Assessment Year 2025-26>Confirm > have business income > select due date of return filing.

(e ) This Form is self-explanatory. The basic information will be pre-filled. Enter additional information, if any, like IFSC Units, etc. Click on the declaration and E-Verify using Aadhar, OPT, DSC, or EVC

(f) The transaction ID and acknowledgment number will be generated.

(g) The acknowledgment number & date of filing of Form 10-IEA must be mentioned in the tax return. Without it, the status of the old regime may not be recognized.

(h) Form 10-IEA is available only online and must be submitted before the ITR due date.

(i) Once verified, tax regime selection becomes binding, especially for business income taxpayers.

12. CONCLUSION: Choosing the right tax regime and reporting it correctly in ITR-3 is crucial for ensuring compliance and optimizing tax liability. Understanding the rules, forms, and scenarios simplifies the process and helps avoid common mistakes.

Disclaimer: The article is for informative purposes only.

The author can be approached at caanitabhadra@gmail.com

Author Bio

bank interest deficit due to premature closure of Fixed deposits. Due to the reported interest paid I am pushed to a higher taxable slab including higher surcharge and penalty interest .How can I offset this bank interest deficit to cut down my taxable income.

Last FY for business income I have filed “New Tax Regime” and this FY too business income I want to file in new regime. But can’t understand which option to choose here because all options are for opting out of new regime.

Select ‘ No’ , where it is asking “ do you wish to opt out from new regime?

You will remain in new regime .

LAST YEAR NO BUSINESS INCOME AND FILED UNDER OLD REGIME CURRENT YEAR BUSINESS INCOME WANTS TO GO FOR NEW REGIME

WHAT TO DO

Select: “Answer Set A”

Click on Not Applicable &

Click on ” No” in Table c1.