The composition scheme under the CGST Act is intended specifically for small taxpayers in order to facilitate compliance and simplify tax levies. It is a supplementary scheme. A person who qualifies for this scheme must pay quarterly tax at the prescribed rate on his or her earnings. There is no input tax credit available if the composition scheme is chosen. The GST Return must be filed on an annual basis. As a result, compliance costs are reduced.

A registered person under this scheme must issue a ‘Bill of Supply,’ as he cannot issue taxable invoices or collect GST from customers. He must expressly state on the invoice, “Composition Taxable Person, ineligible to collect tax on Supply,” and he must prominently display “Composition Taxable Person” on business premises.

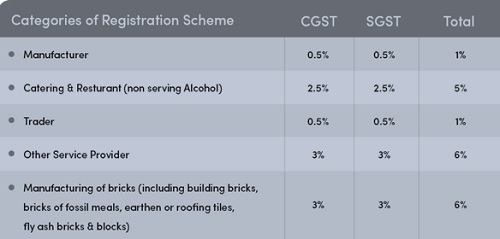

Under Section 10 of the CGST Act, the scheme was initially designed for small traders, manufacturers, and only one service, restaurant service providers. However, the benefits of the composition scheme were later extended to service providers other than restaurants, including mixed suppliers for marginal supply of services for the specified value in addition to the supply of goods to such eligible manufacturers and traders under Sec10 (2A).

Eligibility Criteria for Composition Scheme

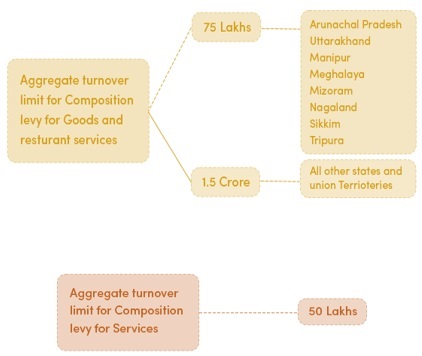

A registered person, manufacturer, trader, or restaurant/catering service provider (not serving Alcohol) can avail of this scheme if his aggregate turnover in the preceding financial year is up to Rs. 1.5 Cr. However, the turnover limit for composition levy for goods is up to Rs. 75 Lakh in respect of 8 Special Category States,

| Arunachal Pradesh | Megalaya |

| Mizoram | Sikkim |

| Uttarakhand | Ttipura |

| Nagaland | Manipur |

Similarly, a registered person providing services (other than the restaurant and catering services) can benefit from the composition scheme if the aggregate turnover in the previous financial year is up to Rs. 50 lakhs.

The option availed by a Registered person for Composition Scheme shall lapse the day on which his ‘Aggregate Turnover’ during a Financial Year exceeds the limit of Rs. 1.50 Cr. or Rs.75 Lakh or Rs. 50 Lakh, as the case may be. Financial Year is considered from the 1st of April to the 31st of March.

It is important to note that aggregate turnover is computed on an all-India basis of the person having the same Permanent Account Number, i.e., the same PAN.

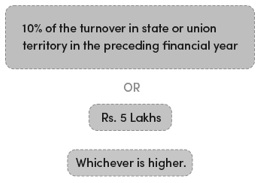

Further, a manufacturer or trader engaged in a marginal supply of services other than that of restaurant services can avail composition scheme for goods for a specified service value along with a supply of goods. This specified value is a value not exceeding

Suppose the value of the service exceeds the limit mentioned above. In that case, the registered person becomes ineligible for the composition scheme for goods and has to opt out of the scheme in the financial year.

Individuals’ ineligible to participate in the Composition Scheme

- A person who is engaged in the supply of goods or services which are not taxable under the Goods and Services.

- A person making interstate outward supply of goods or services (interstate supply means place of supplier and place of supply are in two different states or union territories)

- A person who is engaged in the supply of goods or services through an E-commerce platform

- A non-resident taxable person who is a supplier

- A supplier who is a casual taxable person

- Manufacturer of notified goods such as ice cream and other edible ice, pan masala, aerated water, tobacco & tobacco substitutes

- A supplier who has exceeded the aggregate turnover limit specified under the composition scheme in the current financial year.

Note: there is a restriction on the registered person under the composition scheme regarding interstate outward supply of goods or services, but there is no restriction on receiving such interstate, inward supply of goods or services or both.

Calculation of Aggregate turnover:

Aggregate turnover is defined as the total value of

- all taxable supplies,

- all exempt supplies,

- all inter-state supplies, and

- all exports of goods or services or both.

But it does not include the following:

> The value of inward supplies is subject to reverse charge taxation, including any cess paid under GST law, such as central tax, state tax, union territory tax, integrated tax, and any other cess.

> The value of the aggregate turnover of a person is computed on an all-India basis of a person having the same PAN.

> To calculate the aggregate turnover of a person, it will include the value of supplies made by such person from the 1st of April of a financial year up to the date when he becomes liable for registration under this Act. Still, it shall exclude the value of an exempt supply of services provided by extending deposits, loans, or advances so far as the consideration is represented by interest or discount.

> It is also noted that the value of exports and inter-state supply are considered only for determining the value of aggregate turnover of the preceding financial year. These values are not relevant for computing the value of the current financial year under the composition scheme, and the supplier is not permitted to conduct interstate supply or exports in the said financial year when he opts for the composition scheme.

Conditions and restrictions for levy of Composition Scheme

A person who wants to apply for a composition scheme have to follow the following rules and conditions levied by law

♦ The person shall not be manufacturing or trading the notified goods during the preceding financial year. Such notified goods include

-

- ice cream and other edible ice, whether or not containing cocoa.

- pan masala

- tobacco and other products made from tobacco substitutes

- aerated water

♦ The person has to pay tax under reverse charge on inward supply of goods or services or both

♦ The person cannot be a casual taxpayer

♦ The person cannot be a non-resident taxable person

♦ In lieu of a tax invoice, the individual must issue a ‘Bill of Supply.’

♦ At the top of the bill of supply issued by the person to the customer, the words “Composition taxable person, not eligible to collect tax on supplies” must be mentioned.

♦ The “composition taxable person” must be mentioned on a signboard at his prominent place of business as well as at every other place of business.

♦ The person must pay the Reverse Charge Mechanism tax on the goods he owns because the stock is taxed under reverse charge.

♦ No tax shall be imposed on the recipient of goods or services or both.

♦ If the scheme is used, it will cover all registered persons with the same PAN across India.

♦ The penalty shall be imposed on the Registered person in case of irregular availment of the composition scheme

Features of Composition Scheme

√ Reduction in compliance cost by maintaining fewer books of record and issuance of the taxable invoice

√ Brings ease for small taxpayers in filling out returns

√ Quarterly payment of taxes

√ Tax computed to pay under this scheme is less compared to regular GST payment

√ Simple calculation of tax based on the turnover computed

Difficulties in opting Composition scheme:

♦ The area or territory of conducting business will be limited to the same state where the person conducting the business as a person registered under this scheme is not allowed for interstate supply or any export of goods or services or both.

♦ Input Tax Credit cannot be availed under this scheme

♦ No E-commerce trading of goods or services can be done if opted for this scheme

♦ Cannot supply non-taxable goods example, Alcohol.

How should GST payment be made by a composition dealer:

GST Payment has to be made out of pocket for the supplies made. The GST payment to be made by a composition dealer comprises of the following:

- GST on supplies made.

- Tax on reverse charge, and

- Tax on purchase from an unregistered dealer.

Procedure for opting for Composition Scheme

I. Application for registration notification:

If a person is not registered under GST but wants to get registered and apply for an option to pay tax under the Composition Scheme has to file PART B of the registration form, i.e., GST REG-01. However, permission for the composition scheme shall be granted only after the person has successfully registered himself under GST. The effective date of registration under the composition scheme will be the date of registration under GST.

II. Intimation by a registered person:

The registered person shall electronically file an intimation in the prescribed form under GST Common Portal, i.e., www.gst.gov.in. The intimation must be filled out before the commencement of the financial year for which one wants to opt for the scheme. A statement in prescribed form is also to be furnished within 60 Days of the commencement of the relevant financial year.

The effective registration date under the composition scheme will be from the commencement of the said financial year.

Switching over from Normal Levy (GST Regime) to Composition Scheme (GST Regime)

Registered person shall pay an amount equivalent to the credit of input tax in respect of inputs held in stock and inputs contained in semi- finished or finished goods held in stock by way of debit in electronic credit ledger or electronic cash ledger.

> On capital goods as reduced by such percentage as may be prescribed.

> On the day immediately preceding the date of exercising composition option

> Any balance lying after payment of such amount shall be lapse.

> Furnish a statement in FORM GST ITC-3 within sixty days from the commencement of the relevant financial year.

REVERSAL OF INPUT TAX CREDIT (DETAILS IN FORM GST ITC-03)

For inputs lying in stock, and inputs contained in semi-finished and finished goods lying in stock

The ITC shall be calculated proportionately on the basis of corresponding invoices on which credit has been availed by the registered taxable person on such inputs

For capital goods lying in stock

The input tax credit involved in the remaining residual life in months shall be computed on pro- rata basis taking the residual life as five years;

Illustration

♦ Capital goods have been in use for 4 years, 6 month and 15 days.

♦ The residual remaining life in months= 5 months ignoring a part of the month

♦ Input tax credit taken on such capital goods=Ç

♦ Input tax credit attributable to remaining residual life=C multiplied by 5/6

♦ The amount determined above shall form part of the output tax liability of the registered person and the details of the amount shall be furnished in FORM GST ITC-03

♦ The amount shall be determined separately for input tax credit of IGST and CGST.

♦ Where the tax invoices related to the inputs lying in stock are not available, the registered person shall estimate the amount based on the prevailing market price of goods on the effective date of occurrence of any of the events i.e opt for composition scheme & taxable supply becomes wholly exempt as the case may be.

Switching over from Composition Scheme (GST Regime) to Normal Levy (GST Regime)

> A person shall be entitled to take credit of input tax in respect of inputs held in stock and inputs contained in semi-finished or finished goods held in stock and on capital goods.

> On the day immediately preceding the date from which he becomes liable to pay tax u/s Section 9

> Input tax credit cannot be availed in respect of any supply of goods or services or both to him after the expiry of 1 Year from the date of issue of tax invoice relating to such supply

> The ITC on capital goods shall be claimed after reducing the tax paid on such capital good by 5% per quarter of year or part thereof from the date of invoice or such other documents.

> The registered person shall make a declaration in FORM GST ITC-01 to the effect that he is eligible to avail of ITC.

> The declaration shall specify the details relating to the input lying in the stocks, inputs contained in semi-finished or finished goods lying in stocks or as the case may be capital goods.

> The declaration shall be duly certified by a practicing-chartered accountant or cost accountant if aggregate value of claim on account of central tax, state tax, integrated tax & union territory tax exceeds Rs.2.00 lakhs.

Returns to be filled under the Composition scheme.

GST Forms

| Form No. | Description |

| GST CMP-01 | Intimation to pay tax under section 10 (composition levy) (Only for persons registered under the existing law migrating on the appointed day) |

| GST CMP-02 | Intimation to pay tax under section 10 (composition levy) (For persons registered under the Act) |

| GST CMP-03 | Intimation of details of stock on date of opting for composition levy (Only for persons registered under the existing law migrating on the appointed day) |

| GST CMP-04 | Intimation/Application for withdrawal from composition Levy |

| GST CMP-05 | Notice for denial of option to pay tax under section 10 |

| GST CMP-06 | Reply to the notice to show cause |

| GST CMP-07 | Order for acceptance / rejection of reply to show cause notice |

Also, he is required to file a return annually, i.e., GSTR-4 & GSTR-9A, till the 30th of April of the following financial year.

Withdrawal from the Composition Scheme

The Withdrawal from the scheme by the taxpayer when he cease to satisfy any or all of the prescribed conditions.

- The option to avail composition scheme lapses from the day aggregate turnover exceeds the prescribed limit of Rs. 1.5Cr/75 lakh/50 lakhs as is the case in the government’s budget year.

- Will have to pay tax under the regular scheme from the day he ceases to levy composition scheme

- Will have to issue a taxable invoice in place of the bill of supply

- Will have to inform the authority about such withdrawal from the composition scheme within 7 days of the occurrence of such an event.

The taxpayer will indicate the effective date of withdrawal from the scheme in his intimation to the authorities.

Withdrawal from the scheme by the taxpayer voluntarily

- The taxpayer who intends to withdraw from the scheme has to intimate the authorities in the prescribed form about such withdrawal before the date of voluntary withdrawal.

The taxpayer will indicate the effective date of withdrawal from the scheme in his application to the authorities.

Withdrawal due to denial to pay tax under this scheme by the tax authorities

- When the tax authorities have some reason to believe that the taxpayer is not eligible to pay GST under the composition scheme or has violated any rules/provisions of GST, the authorities may issue Show Cause Notice, i.e., SCN, to the taxpayer.

- The taxpayer then has to submit the reply to SCN.

- Upon receiving such a reply, the authorities can accept or deny the option to avail of the Composition Scheme.

The effective date of withdrawal from the scheme will be the date of infringement of the rules/provisions of GST or any retrospective date determined by the tax authorities.

On such withdrawal from the scheme, the taxpayer has to furnish details of stock of inputs and inputs of semi-finished goods as well as finished goods held by him on the date of such withdrawal in the prescribed format within 30 days from the date of withdrawal.

GST on Bricks – New Bricks GST Rate

“The new tax structure for the Brick Kilns Industry would bring an extra burden on the suppliers in terms of an increase in tax liability and compliance requirements. The increase in the GST rate would also impact the prices of the residential affordable projects that use bricks for the construction of flats. Further, it may not have an impact on large developers using the modern technology of blocks, etc.”

“The rate of 6% or 12% may be analyzed separately in respect of each transaction. Whether to opt for the higher rate or not will depend on various factors such as the ability of the customer to avail of ITC, cost-benefit analysis of the value chain, etc. Developers etc should analyze this and approach the suppliers accordingly.”

The Government has notified a revised tax structure for the Brick Kilns sector effective from April 01, 2022. In this new tax structure, the Government has provided the GST rate of 12%[1] (with ITC) or 6%[2] (without ITC) for the below products (hereinafter referred to as ‘specified products’).

The rate structure implemented by the Government is an outcome of the recommendations of the 45th GST Council meeting. With the introduction of the new rates, the persons engaged in the supply of the specified products would not[3] be entitled to avail the composition scheme. In other words, they would not be entitled to the lower GST rate of 1% (without ITC). Further, the threshold limit of Rs. 40 Lakhs for GST registration has also been reduced to Rs. 20 Lakhs[4].

GST Rate structure before April 01, 2022

Prior to April 01, 2022, the suppliers of specified products could either opt for the composition scheme [5] (1% GST without ITC) or the normal scheme (5% GST with ITC) in order to discharge their GST liability. The GST impact on different suppliers is summarized in the table below:

Supplier having aggregate turnover up to Rs. 40 Lakhs – No registration was needed as turnover was less than the threshold limit of Rs. 40 lakhs.

Taxpayers opted for Composition Scheme 1%

- Benefit of composition scheme was available where turnover was up to Rs. 1.5 Crore

- No ITC was available to the supplier

- GST paid by the supplier could not be claimed as ITC by the recipient.

- Quarterly statement was required to be furnished with tax payment and one return on annual basis was required to be furnished

GST Rate structure after April 01, 2022

Under the new tax rate structure, the Government has notified a higher rate of GST i.e. 12% on the specified products, where the benefit of claiming ITC would be available to the supplier. Alternatively, the specified products can be supplied with the lower GST rate of 6% with a condition that the benefit of ITC would not be available in respect of goods or services used (exclusive or common) in supplying such goods.

The suppliers of the specified products would no longer be able to avail the benefit of the composition scheme under Section 10 of the CGST Act. The threshold limit of registration for such suppliers has also been decreased from Rs. 40 lakhs to Rs. 20 lakhs. In other words, the supplier of specified products would be required to register as a normal taxpayer under the GST law if their aggregate turnover in the financial year exceeds Rs. 20 lakhs.

The rate structure for the supply of specified products with effect from April 01, 2022, is summarized as under:

| Payment of tax at a higher rate 12% | No restriction in respect of ITC/ File monthly/ quarterly returns furnishing the details of outward supply, ITC, payment of tax, etc. |

| Payment of tax at a lower rate 6% | ITC would not be available in respect of the following: |

- Goods or services used exclusively in supplying such goods; and

- Common ITC to be reversed in accordance with Section 17(2) of the CGST Act

- File monthly/ quarterly returns furnishing the details of outward supply, payment of tax, etc.

Important case laws/Advance Ruling

1. Composition scheme opted vide new registration can’t be denied on delay in processing of previous applications

[Loafers Corner Café v. Union of India [2020] 121 taxmann.com 354 (Kerala)]

In the given case the petitioner while under the original registration, filed an application for a fresh GST registration opting for composition scheme. New registration was allotted to the petitioner subsequently, but during the period between the date of application for the new registration and the grant of the same consequent to a cancellation of the earlier registration, the return filed by the petitioner under the composition scheme could not be uploaded into the system. The system recognised only the earlier registration which was not under the composition scheme.

The Hon’ble High Court observed that the petitioner had applied for a cancellation of its earlier registration on 22-5-2018 and had applied for a new registration on 19-6-2018. The cancellation application filed by the petitioner was approved by the authorities only on 18-5-2019. The mere fact that the authorities took time to process the said applications and passed orders approving the cancellation and granting the new registration, cannot deprive the petitioner of benefit of the composition scheme opted through its application for new registration during the interim period.

Given the above, the Hon’ble High Court directed the authorities to make the necessary changes in the GST portal which enables the petitioner to file the returns for the said interim period without charging the petitioner any late fee or other charges.

2. HIGH COURT OF JUDICATURE FOR RAJASTHAN AT JODHPUR:

M/s. Varsha Ritu, Near Ambedkar Circle, Bikaner Through Proprietor Sh. Om Prakash Maru S/o Sh. Ramdev Maru, Vs. The Union of India, Through Principal Secretary, Department of Finance, Govt. Of India, The Chief Commissioner Of Central Goods And Service Jaipur the petitioner submits that the regular registration was cancelled vide order dated 11.06.2018 (Annex.4) with effect 31.03.2018 and, thus, as per law the respondents were free to grant composite registration, the petitioner further pointed out that instead of giving composite registration, they have given registration to petitioner as regular dealer vide order dated 09.06.2018 (Annex.1) and now even the regular registration is being cancelled vide order dated 30.09.2021 (Annex.7).

Counsel for the respondents made a limited submission that consideration for regular composite registration could not have happened earlier because the petitioner was already registered as a regular dealer. In light of aforesaid submissions, the writ petition is disposed of with direction to the respondents that they will reconsider registration of the petitioner as composite dealer w.e.f. 31.3.2018 while keeping into consideration the fact that the respondents themselves cancelled the registration as regular dealer w.e.f. 31.03.2018 vide order dated 11.06.2018 (Annex.4). Necessary order shall be passed by the respondents within a period of 60 days from today w.e.f. date on which petitioner had originally applied for composite registration, strictly in accordance with law.

3. Deep sons Auto Centre Through Its … vs The Union Of India

Petitioner was bonafide and prompt in making complaint to the GSTN on failing to submit form GST ITC-01 just after the prescribed date i.e. 12.08.2018. In that event, as per the petitioner, he loses ITC to the tune of Rs. 5.00 lakh if such switch over is not permitted. Proviso to Rule 40(1)(b) of JGST Rules, 2017, brought into force with effect from 01.07.2017 vide Notification dated 18.08.2017 bearing S.O. No. 64, issued by the Commercial Taxes Department, does confer the power upon the Commissioner of State Tax to extend the time limit. The instant rule is quoted hereunder:

The registered person shall within a period of thirty days from the date of becoming eligible to avail the input tax credit under sub-section (1) of section 18, or within such further period as may be extended by the Commissioner by a notification in this behalf, shall make a declaration, electronically, on the common portal in FORM GST ITC-01 to the effect that he is eligible to avail the input tax credit as aforesaid. Provided that any extension of the time limit notified by the Commissioner of State tax or the Commissioner of Union territory tax shall be deemed to be notified by the Commissioner.”

It was held that the petitioner should approach the Commissioner, State Taxes with a request for extension of time limit for submission of Form GST ITC-01, which may be considered in accordance with law. However, we make it clear that no observation made hereinabove should be read as a conscious interpretation of the provisions of Rule 40 (1) (b) of J.G.S.T. Rules, 2017 by this court at this stage. In case, such extension of time is granted by the State Tax Authorities, petitioner shall avail of the liberty by filing GST ITC-01 Form to switch over from the Composition Scheme to Normal Taxpayer Scheme. The Commissioner, State Tax shall take a decision on the petitioner’s representation within a time frame of four weeks from the date of receipt of copy of this order along with petitioner’s representation.

4. 1% GST payable on a Composition taxpayer engaged in manufacture of Sweet, Namkins, doing only the counter sales (AAR)

FACT OF THE CASE 1. The applicant, Chikkaveeranna Sweet Stall stated that he is running a sweet stall and is engaged in manufacturing the sweets and doing counter sales on a retail basis. He also states that he is registered as “Composition Taxpayer” under GST and selling the goods over the counter and not having any facility of restaurant or hotel. 2. The applicant stated that at present they are paying 1% composition tax on total turnover, as he is a manufacturer of sweets and not providing any goods for human consumption at the place of shop.

DECISION OF THE CASE 1. The coram of Dr. M.P.Ravi Prasad and T.Kiran Reddy ruled that Rate of GST applicable for a Composition tax payer who are engaged in the manufacture of sweet and namkeens and who is doing only the counter sales, is one percent (0.5% COST and 0.5% SGST) subjected to the condition mentioned in the Notification No. 8/2017-Central Tax dated: 27.06.2017 and further amended notifications. 2. The Karnataka Authority of Advance Ruling (AAR) held that 1% GST payable on a composition taxpayer engaged in manufacture of Sweet, Namkins, doing only the counter sales.

5. Pan shop seller not eligible to opt for composition scheme being manufacturing Gutka by mixing ingredients: (The AAAR, Madhya Pradesh )

Fact of the Case The applicant was running pan shop and dealing in all types of products which would be related to pan and necessary items generally accepted in pan shop in general trade parlance. It filed an application for advance ruling to determine whether it would be eligible to opt composition scheme as turnover shall be much less than Rs. 1.5 crores.

Decision of the Case: The Authority for Advance Ruling observed that as per Section 10(2)(b) of CGST Act, the benefit of composition scheme shall not be available to a person who is engaged in supply of goods that are not leviable to tax. Also, as per the Notification No. 14/2019-Central Tax, the persons who are engaged in manufacturing of the Tobacco or Pan Masala, are not eligible for composition scheme. In the instant case, one of the goods that shall be manufactured and sold from the applicant’s Pan Shop is Gutka, containing Tobacco or otherwise which would be similar to Pan Masala. Thus, the preparation of Gutka at the Pan Shop for sale would be covered in the Second Proviso of Notification No. 14/2019-Central Tax. Therefore, benefit of composition scheme shall not be available to applicant.

Personal hearing to taxpayer must before cancellation of GST Registration

Facts of the case:

The Appellant was filing returns under the Tamil Nadu Value Added Tax Act, 2006 and subsequently, under the GST regime also. The appellant’s registration was cancelled on 06.09.2018 on the ground of non-filing of returns. The said defect was subsequently rectified by the appellant. The appellant also remitted GST dues to the tune of Rs.66,781/- together with late fee. The appellant received notice dated 29.10.2019 in which certain defects have been pointed out. The defect includes sales omission and purchase omission also. It was also proposed to levy tax on service charges paid and discount paid. For the reasons best known to the appellant, no reply was submitted. Thereafter, the impugned order came to be passed levying tax and penalty on the appellant.

Judgement/Order:

Madras High Court held that Personal hearing must be afforded to taxpayer before cancellation of GST Registration. As in this case no such Opportunity was afforded to Taxpayer so High Court has Quashed the Cancellation order.

7. Del Small Ice Cream Manufacturers Welfare’s Association (Appellant) vs. Union Of India (Respondent) Delhi High Court

Decision of exclusion of ice cream from the benefits of Composition Scheme to be reconsidered

Facts of the case:

The appellant, Del Small Ice Cream Manufacturers Welfare’s Association claiming to represent the interest of more than 50 small scale ice cream manufacturing units operating in Delhi, filed the petition impugning the decision dated June 18, 2017 of the GST Council, in exercise of powers under Section 10(2)(e) of the CGST Act, 2017, of exclusion of ice cream from the benefits of Composition Scheme under Section 10 of the CGST Act. The appellant contended that the said exclusion was in violation of the spirit of Articles 14 and 19 of the Constitution of India and against the principles of natural justice. The Appellant also contended that ice cream cannot be clubbed with sin goods like Pan masala and Tobacco.

Judgment:

Delhi High Court directed the GST Council to reconsider the exclusion of small scale manufactures of ice cream from the benefit of Section 10(1) of the CGST Act, including on the aforesaid two parameters i.e. the components used in the ice cream and the GST payable thereon and other similar goods having similar tax effect continuing to enjoy the benefit.

8. The department cannot detain the goods on failure to fill Part-B of the E-way Bill if the supply is not taxable under GST. The Court observed that on perusal of the impugned order imposing tax and penalty against the petitioner, it is revealed that the basis for computing the additional tax is the IGST paid by the petitioners. Held by Gujarat High Court in the matter of M/s Neuvera Wellness Ventures (P) Ltd. Vs. State of Gujarat.

9. Mahadeo Construction Co. (Appellant) vs., Union of India (Respondents),Jharkhand High Court

Interest liability cannot be recovered under section 79 of CGST Act, 2017 without initiation of adjudication proceeding in the event assess disputes the computation or very leviability of interest/issuance of Show Cause Notice.

The issues involved in the present writ application were, namely—

(i) Whether interest liability under Section 50 of the Central Goods and Services Tax Act, 2017 (‘CGST Act’) can be determined without initiating any adjudication process. either u/s 73 or 74 of the CGST Act in the event of an assessee raising dispute towards liability of interest?

(ii) Whether garnishee recovery proceedings u/s 79 of the CGST Act can be initiated for recovery of interest u/s 50 of the said Act without initiation and completion of the adjudication proceedings under the Act?

Judgement: The hon’ble Jharkhand High Court held that interest liability under section 50 of the CGST Act, 2017 is although automatic, but it’s computation and demand can be raised only after initiation of Adjudication proceedings under Section 73 or 74 of the CGST Act, 2017 in case the assessee disputes the demand of interest. Garnishee proceedings under Section 79 of the CGST Act, 2017 cannot be initiated for recovery of interest without adjudicating the liability of interest, when the same is admittedly disputed by the assessee.

10. Vimal Raj (Appellant) vs. State Tax Officer (Respondents) Kerala High Court

Assessment order passed under GST after death was invalid.

Validity of order passed against a deceased – Section 93 of CGST Act, 2017 not followed – service of Show cause Notice. Assessment order passed under GST after death was invalid. Assessee was already dead as on the date of assessment order and therefore, the assessment orders is a nullity and no other issues are decided by this Court and such other issues are left open. Legal representatives or legal heirs of the said deceased assessee would be given reasonable opportunity of being heard.

Judgement : It appears that the respondent does not raise any serious dispute as to the factual assertion made by the petitioner that the assessee concerned (who appears to be the paternal grandfather of the petitioner herein) is said to be one of the legal hairs of the deceased assessee as the petitioner’s father who is the son of the assessee has died as early as on 27.03.2018 as evident from Ext.P3 death certificate issued by the Registrar of Births and Deaths, which is much before the rendering of the impugned Ext.P3 series of the assessment orders issued in March 2019 – Since, that appears to be the undisputed position, it is only to be held that Ext.P3 series of assessment orders rendered as late as in March, 2019 has been passed as against an assessee who is already dead by then and therefore, the impugned assessment orders is a nullity in the eye of law. The 1strespondent will be at liberty to take fresh action in the said assessment proceedings, after ascertaining from the competent Revenue Officials as to who all are the legal representatives or legal heirs of the said deceased assessee and then the respondent will be at liberty to render reasonable opportunity of being heard to such legal representatives and then finalise the assessment proceedings in the manner known to law. Petition disposed off.

Opportunity of being heard, Assessing Officer should wait till end of the working day when personal hearing is fixed, before finalizing assessment

Facts of the case:

The Appellant urged that effective opportunity was not given to him by the Assessing Officer (AO) as personal hearing notice was issued on February 13, 2020 listing the matter for hearing, the very next day i.e., February 14, 2020 and the impugned orders have been passed on the same day. The Appellant argued that principles of natural justice was violated. The Appellant prayed before the court to call for the records relating to the impugned order passed by the AO and quash the consequential recovery notice in Form GST DRC-07 issued by the AO.

Judgement:

Madras High Court quashed the Assessment order passed by the GST State Tax Officer dated February 14, 2020 where the Personal Hearing intimation was issued on February 13, 2020 posting the hearing on February 14, 2020. The Court was of opinion that the Assessing Officer, in all fairness, should wait till the end of the working day when personal hearing was fixed, before finalizing the assessment.

Author Bio