I. Introduction

The Goods and Services Tax framework in India recognizes that compliance under the regular tax mechanism may be burdensome for small businesses. To address this, the legislature introduced the Composition Levy under Section 10 of the Central Goods and Services Tax Act, 2017 (CGST Act). This mechanism permits eligible registered persons to discharge their GST liability at a flat percentage of turnover, in lieu of the standard mechanism with its associated invoice-matching, return-filing, and record-keeping obligations.

The scheme was originally available only for goods dealers and restaurant service providers. The Finance (No. 2) Act, 2019 expanded the scope by inserting Section 10(2A), extending a similar facility to eligible service providers not covered under the original provision.

This article provides a comprehensive analysis of the composition levy framework – its legal basis, eligibility, ineligibility, tax rates, compliance obligations, and practical implications for businesses considering this option.

II. Legal Framework

The composition levy is governed by the following provisions:

- Section 10, CGST Act, 2017 – Substantive provision

- Rules 3 to 7, CGST Rules, 2017 – Procedural and operational framework

- Relevant notifications under Section 10(1) and Section 10(2A)

III. Types of Composition Levy

The composition framework operates under two distinct sub-sections of Section 10:

A. Section 10(1) – Original Composition Levy

Applicable to:

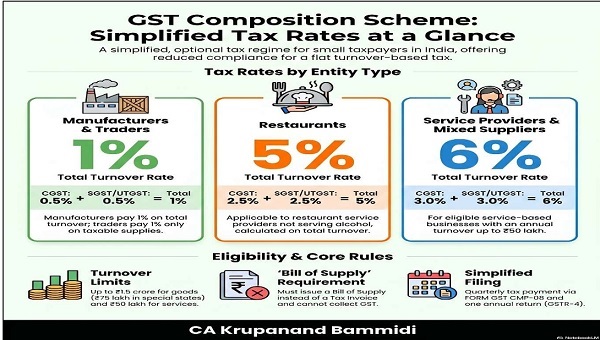

Manufacturers of goods (other than manufacturers of notified goods), traders (suppliers of goods), and persons engaged in supply of restaurant services as specified in paragraph 6(b) of Schedule II, CGST Act.

Aggregate Turnover Limit: Preceding financial year turnover not exceeding INR 1.5 crore. For persons in specified special category states, the limit is INR 75 lakh.

Rate: As prescribed, not exceeding 1% of turnover in state (see Section VII – Tax Rates).

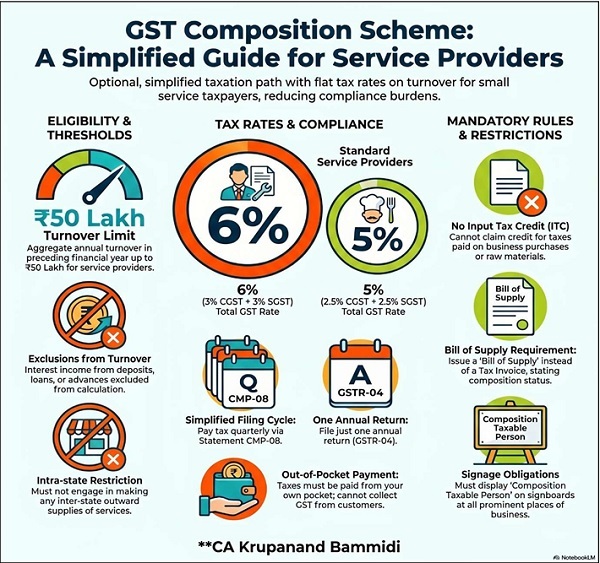

B. Section 10(2A) – Extended Composition Levy for Service Providers

Inserted by: Finance (No. 2) Act, 2019.

Applicable to: Registered persons not eligible under Section 10(1) – primarily pure service providers other than restaurant service providers.

Aggregate Turnover Limit: Preceding financial year turnover not exceeding INR 50 lakh.

Rate: 3% CGST + 3% SGST = 6% of turnover in state.

Note: For a new business with no preceding financial year, the turnover condition is met and the person may opt for composition from the date of registration, subject to all other eligibility conditions.

IV. Turnover Limits at a Glance

| Provision | Category of Taxpayer | Limit |

| Section 10(1) | Manufacturers of goods | INR 1.5 crore |

| Section 10(1) | Traders – suppliers of goods | INR 1.5 crore |

| Section 10(1) | Restaurant service providers | INR 1.5 crore |

| Section 10(2A) | Service providers (other than restaurant) | INR 50 lakh |

*Limit for Special Category States needs to checked for INR 75 lakh applicability.

V. Eligibility – Who Can Opt

A person is eligible to opt for composition levy if the following conditions are cumulatively satisfied:

- They are a registered person under the CGST Act.

- Aggregate turnover in the preceding financial year does not exceed the applicable limit: INR 1.5 crore under Section 10(1) for goods dealers and restaurant services; INR 50 lakh under Section 10(2A) for service providers. For special category states under Section 10(1), the limit is INR 75 lakh

- They are not engaged in any activity that renders them ineligible under Section 10(2), CGST Act or Rule 5, CGST Rules, 2017.

- Multiple registrations (same PAN) – Rule 3(4), CGST Rules: Where a person holds registrations in multiple states or union territories under the same PAN, the option for composition must be exercised uniformly for all registrations. If anyone registration is ineligible for composition, none of the registrations can opt.

- For new businesses with no preceding financial year: the turnover condition is treated as satisfied and they may opt at the time of fresh registration, subject to all other eligibility conditions being met.

VI. Ineligibility – Who Cannot Opt

A. Under Section 10(2), CGST Act – Conditions for Section 10(1)

A person is not eligible under Section 10(1) if engaged in any of the following:

a) Supply of services other than restaurant services. (Note: Such persons may separately qualify under Section 10(2A) if aggregate turnover does not exceed INR 50 lakh.)

b) Supply of goods not leviable to tax under the Act – for example, petroleum products, alcohol for human consumption, and other non-taxable goods.

c) Making inter-state outward supply of goods.

d) Making supply of goods through an electronic commerce operator required to collect tax at source under Section 52, CGST Act.

e) Manufacture of goods notified by the Government on recommendations of the GST Council under Section 10(2)(e).

B. Under Rule 5, CGST Rules, 2017 – Additional Restrictions

- Casual taxable persons (Rule 5(1)(a)).

- Non-resident taxable persons (Rule 5(1)(a)).

- Persons who hold goods in stock that were purchased in the course of inter-state trade, imported, or received from a branch outside the state [relevant at the time of transition to composition].

C. Structural Incompatibility – Inter-State Services

Even where the statute may not expressly prohibit inter-state outward supply of services for Section 10(2A) persons, the structure of the composition levy (CGST + SGST only) is fundamentally incompatible with inter-state supplies (which attract IGST). A composition dealer cannot charge IGST on inter-state supplies. Businesses with a pan-India customer base or online delivery model should not assume composition is available without verifying this position from the applicable notification.

VII. Tax Rates – Rule 7, CGST Rules, 2017

The rates of tax payable under composition are prescribed under Rule 7 of the CGST Rules, 2017:

| Provision | Category | CGST Rate | SGST Rate | Total Rate |

| Section 10(1) | Manufacturers (other than notified goods) | 0.5% | 0.5% | 1.0% |

| Section 10(1) | Traders – suppliers of goods | 0.5% | 0.5% | 1.0% |

| Section 10(1) | Restaurant service providers | 2.5% | 2.5% | 5.0% |

| Section 10(2A) | Service providers (other than restaurant) | 3.0% | 3.0% | 6.0% |

VIII. Aggregate Turnover vs. Turnover in State – A Critical Distinction

Two separate definitions govern distinct aspects of the composition framework. Confusing the two leads to errors in both eligibility assessment and tax computation.

| Parameter | Aggregate Turnover – Section 2(6) | Turnover in State – Section 2(112) |

| Basis | All-India; PAN-based; all registrations of the same person | State-specific; registrations in that state only |

| Includes | All taxable supplies + exempt supplies + exports + inter-state supplies across all states | All taxable supplies + exempt supplies + exports + inter-state supplies made from that state |

| Excludes | Inward supplies on which RCM is payable; CGST, SGST, IGST, Cess | CGST, SGST, IGST, Cess |

| Purpose | Determining eligibility threshold | Computing actual composition tax liability |

Critical practical implication: Composition tax is computed on total turnover in state, which includes exempt supplies. A business with a significant proportion of exempt supplies pays composition tax on receipts that would attract zero GST liability under regular registration. Regular registration is commercially preferable for such businesses.

IX. Conditions and Restrictions – Rule 5, CGST Rules, 2017

A composition dealer must comply with the following conditions throughout the period during which the composition option is in force:

- No collection of tax from customers: Section 10(4), CGST Act – Cannot collect any GST from recipients. The composition tax is entirely borne by the dealer.

- No input tax credit: Section 10(4), CGST Act – Not entitled to claim any credit of input tax. This bar is absolute and applies to all inward supplies including capital goods.

- Mandatory declaration on bills of supply: Rule 5(1)(f) – Every bill of supply must prominently bear: “Composition taxable person, not eligible to collect tax on supplies.”

- Signboard display: Rule 5(1)(g) – Every notice or signboard at the principal place of business and at every additional place of business must display: “Composition taxable person.”

- RCM compliance: Composition does not exempt a dealer from reverse charge. Tax under Section 9(3) and Section 9(4), CGST Act must be paid on applicable inward supplies. Since ITC cannot be availed, the RCM paid is an irrecoverable cost.

- No inter-state outward supply of goods: Section 10(2)(c) – Absolute prohibition.

- No supply of non-taxable goods: Section 10(2)(b).

- No supply through TCS e-commerce operators: Section 10(2)(d) – No supply of goods through operators required to collect TCS under Section 52.

X. Procedure to Opt In

A. New Registrants – via Form GST REG-01 – A person applying for fresh registration under Rule 8, CGST Rules may exercise the option for composition in Part B of Form GST REG-01. The registration is then granted as a composition dealer and the scheme is effective from the date of registration. (Rule 3(3), CGST Rules, 2017)

B. Existing Registered Persons – via Form GST CMP-02 (Annual Window) – A registered person wishing to opt for composition for a financial year must file Form GST CMP-02 (Intimation to Pay Tax under Composition Levy) prior to the commencement of that financial year, i.e., before 1st April. (Rule 3(2), CGST Rules, 2017)

The option is effective from the beginning of the financial year in which it is exercised. The GST portal typically disables the CMP-02 facility once the financial year commences. A person who misses the window must operate as a regular dealer for the entire year and opt in at the next annual window.

C. ITC Reversal on Opting In – Form GST ITC-03 – On the date of opting into composition, accumulated ITC must be reversed on stock of inputs, semi-finished goods, finished goods, and capital goods held on that date. (Rule 44(4), CGST Rules, 2017) The reversal amount is payable through Form GST ITC-03. For businesses with significant stocks or capital goods, this can be a material one-time outflow.

D. All Registrations – Same PAN Must Opt Uniformly – Rule 3(4), CGST Rules: Where a person holds registrations under the same PAN in multiple states, the CMP-02 filed by one registration is deemed to have been filed by all. All registrations then fall under composition. If any registration is ineligible, the option is not available for any registration under that PAN.

XI. Compliance Obligations

A. Quarterly Tax Payment – Form GST CMP-08

Composition dealers pay tax quarterly through Form GST CMP-08 (Statement-cum-Challan for Composition Dealers). The dealer self-assesses tax on turnover for the quarter at the applicable rate.

| Quarter | Period | CMP-08 Due Date |

| Q1 | April to June | 18th July |

| Q2 | July to September | 18th October |

| Q3 | October to December | 18th January |

| Q4 | January to March | 18th April |

B. Annual Return – Form GSTR-4

Composition dealers must file an annual return in Form GSTR-4 by 30th April of the succeeding financial year. This consolidates outward supply details and quarterly tax payments for the year.

Note: Composition dealers are NOT required to file GSTR-1 or GSTR-3B. The compliance burden is substantially lower than that of regular dealers. No invoice-level outward supply reporting is required on a monthly basis.

XII. Input Tax Credit – Position under Composition

Section 10(4), CGST Act: A composition taxable person shall not be entitled to any credit of input tax. This is an absolute and unconditional bar on ITC.

A. On Opting In – Reversal (Form GST ITC-03, Rule 44(4)) – On the date of opting for composition, the dealer must reverse ITC on:

- Stock of inputs held as on that date

- Inputs contained in semi-finished goods held as on that date

- Inputs contained in finished goods held as on that date

- Capital goods held as on that date (proportionate reversal for remaining useful life)

- The reversal amount must be paid through Form GST ITC-03.

B. On Opting Out – Reclaim (Form GST ITC-01, Rule 6(4)) – When a composition dealer reverts to regular registration, ITC may be claimed on:

- Stock of inputs held as on the date of switching

- Inputs contained in semi-finished and finished goods as on that date

- Capital goods (proportionate)

- Critical restriction – Rule 6(5), CGST Rules: ITC on services is NOT available on switching out of composition. Only goods-related ITC can be reclaimed. Form GST ITC-01 must be filed within 30 days of switching.

XIII. Invoicing – Bills of Supply

Composition dealers are prohibited from issuing tax invoices. They must issue Bills of Supply in lieu of tax invoices. (Section 31(3)(c), CGST Act read with Rule 49, CGST Rules, 2017). Requirements for a valid Bill of Supply under Rule 49:

- Mandatory declaration: “Composition taxable person, not eligible to collect tax on supplies”

- No GST amount to be shown or collected from the recipient

- Serially numbered and dated

- Name, address, and GSTIN of the supplier

- Name and address of the recipient

- HSN code or SAC (as applicable)

- Description, quantity, and value of supply

- Signature of the supplier or authorised signatory

B2B commercial implication: Since no GST is charged on bills of supply, the recipient (if a registered person) cannot avail any ITC on purchases from a composition dealer. This is a material commercial disadvantage in B2B transactions and is the primary reason composition is unsuitable for businesses serving registered corporate customers.

XIV. Reverse Charge Mechanism under Composition

Composition is not an exemption from the reverse charge mechanism. A composition dealer must pay GST under reverse charge on inward supplies covered by:

- Section 9(3), CGST Act: Notified categories – including goods transport agency (GTA) services, legal services from individual advocates, services from government or local authority (other than exempt services), import of services, sponsorship services, and other notified categories.

- Section 9(4), CGST Act: Purchases from unregistered persons (to the extent notified and applicable).

Critical cost implication: Since composition dealers cannot avail ITC (Section 10(4)), the RCM liability paid represents a direct and irrecoverable out-of-pocket cost. Businesses with material RCM-applicable inward supplies – freight, professional fees, government payments – must include this in their composition viability analysis. This is a frequently overlooked element that can materially erode the tax advantage of composition.

XV. Withdrawal from Composition – Rule 6, CGST Rules, 2017

A. Mandatory Withdrawal – Threshold Breach (Section 10(3)) – Section 10(3), CGST Act: The option lapses from the day on which aggregate turnover during the financial year exceeds the applicable limit. The dealer must file Form GST CMP-04 (Intimation of Withdrawal) within 7 days of crossing the threshold. (Rule 6(2), CGST Rules)

B. Mandatory Withdrawal – Other Ineligibility – If the dealer becomes ineligible for any other reason (commencement of inter-state supply of goods, manufacture of notified goods, etc.), Form GST CMP-04 must be filed within 7 days.

C. Voluntary Withdrawal – A composition dealer may opt out voluntarily at any time by filing Form GST CMP-04.

D. After Withdrawal

- Deemed to be a regular dealer from the date of withdrawal

- Must issue tax invoices for all subsequent supplies

- Must file GSTR-1 and GSTR-3B going forward

- ITC on stock of goods may be claimed via Form GST ITC-01 within 30 days

- ITC on services: not available (Rule 6(5), CGST Rules)

XVI. Consequences of Non-Compliance – Section 10(5)

Where a composition dealer is found to have contravened the provisions of Section 10 or the applicable rules, the proper officer may:

- Determine tax payable as if the person had never been on composition – i.e., assess as a regular dealer at applicable GST rates for the entire contravention period.

- Recover the determined tax shortfall with interest at 18% per annum under Section 50(1), CGST Act.

- Levy penalty equivalent to the tax determined under Section 122, CGST Act.

Practical exposure: A composition dealer found ineligible (e.g., for having made inter-state supplies of goods, crossed the turnover limit without switching, or supplied notified goods) faces retrospective assessment as a regular dealer. The full GST at applicable rates becomes payable on all outward supplies for the contravention period, without the benefit of ITC foregone during that period. This can result in significant financial exposure and must not be underestimated.

XVII. Composition vs. Regular Registration – Comparative Summary

| Parameter | Composition Scheme | Regular Registration |

| Tax rate | 1% / 5% / 6% on turnover in state (flat) | 5% / 18% on value of taxable supply |

| Tax base | Total turnover in state – taxable + exempt + exports | Taxable value of each supply. Exempt supplies: nil tax. |

| ITC | Not available – Section 10(4) | Available subject to Sections 16 and 17 |

| Tax collection from customer | Prohibited. Tax borne entirely by dealer. | Mandatory on every taxable supply. |

| Invoice type | Bill of Supply (no tax shown) | Tax Invoice |

| Inter-state supply | Goods: barred (Section 10(2)(c)). Services: verify from applicable notification. | Permitted. IGST applicable. |

| Returns | CMP-08 (quarterly) + GSTR-4 (annual) | GSTR-1 + GSTR-3B monthly or quarterly |

| Compliance burden | Low | Higher |

| Turnover limit | Goods: INR 1.5 crore | Services: INR 50 lakh | No upper limit |

| B2B suitability | Poor – recipients cannot avail ITC | Good – recipients can avail ITC |

| B2C suitability | Good – recipients do not need ITC | Adequate |

| RCM liability | Payable; ITC not available – irrecoverable cost | Payable; ITC available as credit |

XVIII. Practical Considerations

1. The B2C vs. B2B Distinction is Decisive

Composition is commercially viable primarily for businesses serving end consumers (B2C) – retail traders, restaurants, individual training providers, local service providers. Where customers are businesses (B2B) requiring ITC on purchases, the inability to issue tax invoices is a significant competitive disadvantage. B2B customers may actively prefer composition-registered suppliers’ regular-registered competitors who can provide ITC-eligible invoices.

2. Aggregate Turnover is PAN-Level – Monitor Carefully

Aggregate turnover is computed across all registrations of the same person under the same PAN, on an all-India basis. A business with multiple state registrations must monitor combined turnover continuously. An unexpected spike in turnover in one state can trigger mandatory exit from composition across all states.

3. RCM as a Hidden Cost in Composition Viability Analysis

The reverse charge liability with no corresponding ITC is an often-overlooked cost. A composition dealer paying GTA freight, legal fees, or government charges must pay GST under RCM on these and absorb the amount as a cost. This can materially erode the tax savings from composition.

4. ITC Reversal as a One-Time Transition Cost

On opting into composition, the entire balance of accumulated ITC on closing stock must be reversed as a cash payment through Form GST ITC-03. Businesses with significant inventories, work-in-progress, or recently acquired capital goods must plan for this one-time outflow before deciding to opt in.

5. Exempt Supplies – Composition May Be More Expensive

Since composition tax applies on total turnover in state including exempt supplies, a business with a significant proportion of exempt supplies pays composition tax on receipts that would attract zero GST liability under regular registration. For health care providers, educational institutions, and other entities with predominantly exempt supplies, regular registration (with nil GST liability on exempt outputs) is almost always preferable to composition.

6. Annual Opt-In Window – Do Not Miss It

The window to opt into composition for the next financial year closes before 1st April. A missed window means operating as a regular dealer for the entire financial year. New registrants may opt at the time of registration itself (Part B of Form GST REG-01) and should not miss this opportunity if composition is intended from the outset.

7. Growth Planning and Exit Strategy

Businesses with high growth trajectories should monitor their proximity to the applicable limit. Crossing INR 1.5 crore (goods) or INR 50 lakh (services) without timely exit triggers retrospective assessment with interest and penalty under Section 10(5). An exit plan should be prepared well before the limit is approached.

8. Multi-State or Online Businesses

Businesses delivering services online to customers across India (e-learning, software, consulting) make inter-state supplies. The structural incompatibility of composition (which generates only CGST + SGST) with inter-state IGST liability makes composition impractical for such businesses regardless of turnover.

XIX. Conclusion

The composition levy offers a simplified tax payment mechanism for small businesses – reduced compliance burden, flat rate taxation, and streamlined return filing. However, it is not universally advantageous. The suitability of composition over regular registration must be assessed on the specific facts of each business.

The key factors in the analysis are:

- Nature of customer base – B2C (favours composition) vs. B2B (favours regular)

- Aggregate turnover – well within limit (composition viable) vs. approaching limit (plan exit)

- Proportion of exempt supplies – high exempt proportion (regular registration preferred)

- Inter-state supply requirements

- RCM exposure on inward supplies – high RCM liability increases effective cost of composition

- ITC on closing stock at transition – significant stock means material one-time reversal outflow

- Nature of activities – services vs. goods determines applicable sub-section and limit

- The extension to service providers under Section 10(2A) is a welcome development. However, the significantly lower turnover cap of INR 50 lakh and the higher rate of 6% compared to goods dealers (1%) make the composition option less attractive for service providers. The analysis must be done carefully in each case.

Professional guidance is strongly advisable before opting for or withdrawing from the composition scheme, given the retrospective assessment consequences under Section 10(5) in cases of non-compliance, and the financial exposure that can arise from inadvertent breach of conditions.

*****

Author’s Note: The views expressed are based on the current portal disclosures. For any query related to above article, or if you face any issue in Income Tax, GST, SEZ, STPI, MCA compliances etc., especially in cases involving legal proceedings, notices, litigation, or demand matters. Please feel free to contact us at the details mentioned below:

Contact: +91-7842796315; Email: cakrupanand@gmail.com

Author Bio