The Ministry of Corporate Affairs has introduced the Companies Compliance Facilitation Scheme, 2026 as a one-time opportunity for companies to regularise long-pending ROC filings at concessional additional fees. Considering the extent of non-compliances observed across companies, this scheme provides a structured route for clean-up and compliance alignment.

1. What is the objective of CCFS-2026

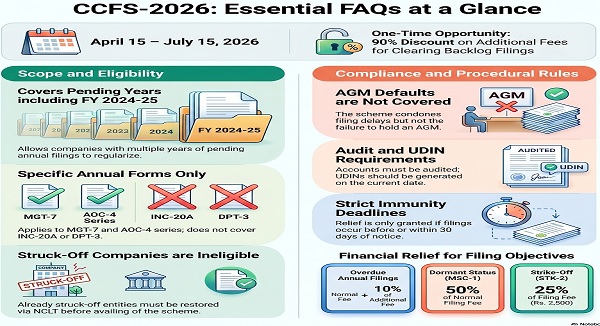

The scheme enables companies to file overdue annual returns and financial statements by paying reduced additional fees. It also facilitates companies to opt for dormant status or proceed for strike off, wherever applicable.

2. What is the validity period of the Scheme

The scheme is operational from 15 April 2026 to 15 July 2026. Only filings made within this window are eligible for the concessional benefit.

3. Which companies are eligible

All companies are generally eligible except:

- Companies where strike off action has been initiated

- Companies that have already applied for strike off

- Companies that have applied for dormant status before commencement

- Amalgamated or dissolved companies

- Vanishing companies

4. Which forms are covered

The scheme primarily applies to annual filing related forms including:

- MGT-7 and MGT-7A

- AOC-4 series (including NBFC variants)

- Certain related forms such as ADT-1, FC-3 and FC-4

Forms such as INC-20A and DPT-3 are not covered.

5. Whether FY 2024-25 filings are covered

Yes, all pending annual filings including FY 2024-25 are covered.

6. What is the fee benefit under the Scheme

Only 10 percent of the additional fee is payable for delayed annual filings. Normal filing fees remain fully applicable.

7. Is there any concession in normal filing fees

No. The scheme provides concession only on additional fees.

8. What is the fee for dormant status application

For MSC-1 filing, only 50 percent of the normal filing fee is payable.

9. What is the fee for strike off

For STK-2 filing, only 25 percent of the normal filing fee is payable.

10. Whether immunity from penalty is available

Immunity is available in certain cases, particularly where filings are made before issuance of adjudication notice or within 30 days of such notice.

11. Is any separate application required for immunity

No separate form is required.

12. Whether immunity is available for non-holding of AGM

No. The scheme condones delay in filing, not failure to hold AGM.

13. Whether audit is mandatory before filing

Yes. Pending financial statements must be audited and UDIN must be generated before filing.

14. What happens if the Scheme is not availed

Companies may be subject to enforcement actions including higher additional fees and potential strike off.

15. Can multiple years be regularised

Yes. Multiple years of pending filings can be regularised under the scheme.

16. What steps should companies take

- Identify pending filings

- Verify eligibility

- Complete audits

- File within scheme period

17. Whether strike off can be filed without clearing past filings

Generally, all pending filings must be completed before applying for strike off, subject to specific conditions.

Practical Observations

- This scheme is particularly useful for companies with 3 to 6 years of backlog where additional fees have become prohibitive.

- The combination of reduced additional fees and concessional rates for dormant status and strike off provides multiple exit or regularisation routes.

- Professionals should carefully evaluate cases involving adjudication or prosecution, as eligibility for immunity may vary.

- Immediate action is advisable as last-minute filings may face technical or system constraints on the MCA portal.

Conclusion

CCFS-2026 is a significant compliance window that should not be overlooked. From a professional standpoint, it offers an opportunity to clean up legacy non-compliances at a fraction of the usual cost, while aligning company records with statutory requirements.

A structured review of client portfolios and proactive execution during the scheme period will be essential to fully utilise the benefits available.

Author’s Note

The scheme presents a significant opportunity for companies to clean up long-standing non-compliances at a substantially reduced cost. However, each case should be evaluated carefully, especially where adjudication or prosecution exposure exists.

*****

The views expressed are based on the current MCA disclosures. For any query related to above article, or if you face any issue in Income Tax, GST, SEZ, STPI, MCA compliances etc., especially in cases involving legal proceedings, notices, litigation, or demand matters. Please feel free to contact us at: Contact: +91-7842796315; Email: cakrupanand@gmail.com

Author Bio