Rule 14A Withdrawal is now Active on GST Portal – Relief After 3-Day Registration Rule & GSTR-1 Blocking Issue

The recent operationalisation of the 3-Day GST Registration framework under Rule 14A had led to considerable compliance challenges for taxpayers and professionals. In particular, system-driven validations linked to output tax liability resulted in instances where GSTR-1 filings were blocked, especially in cases where the monthly output tax liability in respect of supplies made to registered persons exceeded ₹2.5 lakh.

The practical issues arising from this implementation were examined in detail in our earlier article:

3-Day GST Registration Rule Causing GSTR-1 Blocking & ₹2.5 Lakh Error https://taxguru.in/goods-and-service-tax/3-day-gst-registration-rule-causing-gstr-1-blocking-rs-2-5-lakh-error.html

The concerns highlighted therein primarily related to automated restrictions being triggered on the portal, leading to avoidable hardship even in genuine cases of business transactions.

Important Development – Rule 14A Withdrawal Functionality Activated

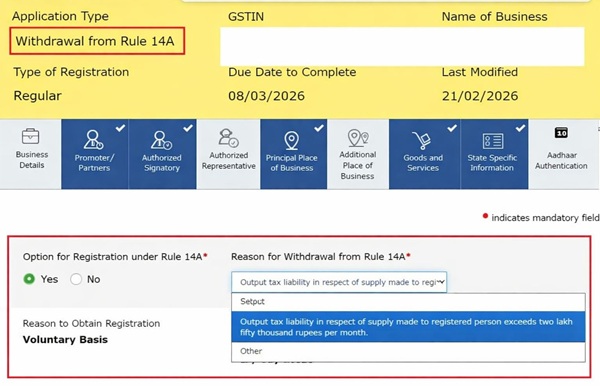

In a significant development, and pursuant to the GSTN advisory, the GST Portal has now enabled the functionality for “Withdrawal from Rule 14A” under the Registration module.

Taxpayers who had opted for registration under Rule 14A (including those who obtained registration on a voluntary basis under the said framework) may now initiate withdrawal through the portal.

Salient Features of the Portal Update:

- New Application Type available: “Withdrawal from Rule 14A”

- Option enabled within the Registration section

- Mandatory selection of reason for withdrawal

- Dropdown reasons include:

- Output tax liability in respect of supply made to registered person exceeds ₹2,50,000 per month

- Other

- Functionality currently active and operational

This update effectively provides a corrective mechanism for cases where automated validations had led to return filing constraints.

Portal Interface – Withdrawal Option

(Screenshot evidencing the live activation of the Withdrawal from Rule 14A functionality on the GST Portal.)

Practical Implications for Taxpayers and Professionals

The activation of this withdrawal mechanism carries significant practical relevance:

- It addresses compliance bottlenecks arising from system-based output tax validations.

- It offers relief in cases where GSTR-1 filing was restricted.

- It enables correction in voluntary registrations obtained under the expedited framework.

- It mitigates exposure to consequential late fees and interest due to return filing disruptions.

Professionals are advised to immediately review client registrations falling under the Rule 14A framework and assess whether withdrawal is warranted in appropriate cases.

Concluding Remarks

While Rule 14A was introduced with the objective of expediting the GST registration process, the initial implementation resulted in unintended procedural rigidity in certain scenarios. The activation of the withdrawal functionality reflects administrative responsiveness and restores necessary flexibility within the compliance framework.

Stakeholders should take prompt and informed action to regularise affected registrations and ensure seamless continuation of return filings.

******

Author’s Note: The views expressed are based on the current GST portal functionality and system disclosures. For any query related to above article, or if you face any issue in Income Tax, GST, SEZ, STPI, MCA compliances etc., especially in cases involving legal proceedings, notices, litigation, or demand matters. Please feel free to contact us at the details mentioned below:

Contact: +91-7842796315; Email: cakrupanand@gmail.com

Author Bio