Case Law Details

Principal Commissioner of Service Tax Vs Allahabad Bank (CESTAT Kolkata)

The Customs, Excise and Service Tax Appellate Tribunal (CESTAT), Kolkata dismissed the Revenue’s appeal and upheld the adjudicating authority’s order dropping the demand for reversal of CENVAT credit availed by the respondent on deposit insurance services provided by the Deposit Insurance and Credit Guarantee Corporation (DICGC).

The dispute arose after an investigation by the DGCEI, Kochi Regional Unit, based on intelligence that the respondent had wrongly availed CENVAT credit of Service Tax paid on deposit insurance services provided by DICGC. According to the Revenue, the deposit insurance premium was linked only to deposits accepted by the bank and had no nexus with any output service rendered by the respondent. It was also alleged that the respondent could not charge depositors any fee for insuring their deposits and that payment of the insurance premium was merely a transaction in money. On this basis, the Revenue contended that the deposit insurance service did not qualify as an input service under Rule 2(l) of the CENVAT Credit Rules, 2004.

The Revenue further alleged that the respondent had availed CENVAT credit of Rs. 19,86,29,413/- on three invoices issued by DICGC and that the credit had been taken before the dates of issuance of the invoices dated 11.04.2012, 20.09.2012 and 06.12.2012. Consequently, a show cause notice was issued demanding recovery of the credit along with applicable interest and proposing penalty under the Finance Act, 1994 and the CENVAT Credit Rules, 2004. However, the adjudicating authority dropped the demand, leading the Revenue to file the present appeal.

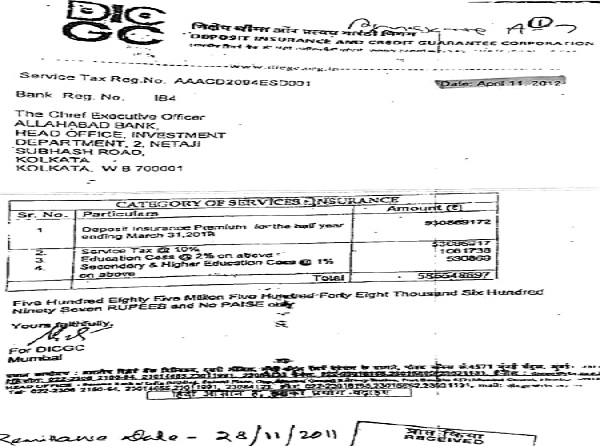

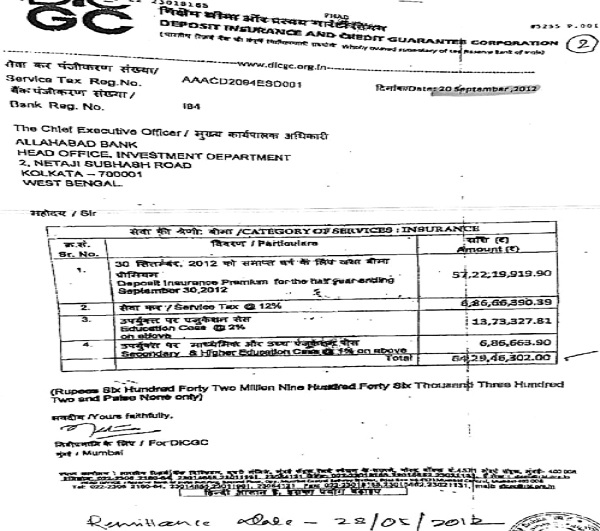

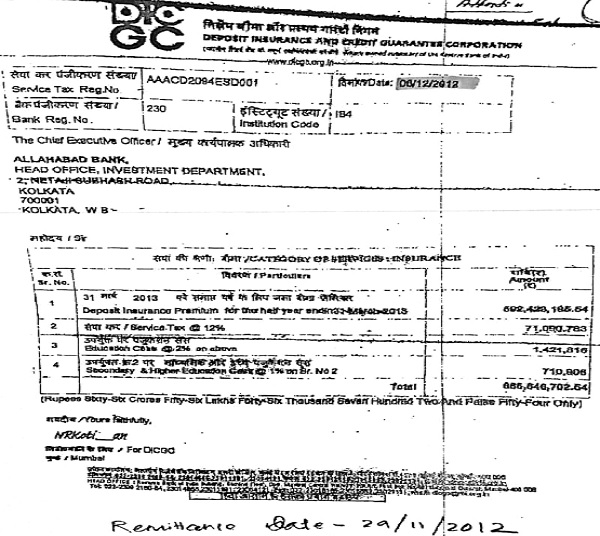

The Tribunal examined the three invoices and the remittance details reproduced in the record. It found that the payment corresponding to the invoice dated 11.04.2012 had been remitted on 28.11.2011, the payment for the invoice dated 20.09.2012 had been remitted on 28.05.2012, and the payment relating to the invoice dated 06.12.2012 had been remitted on 29.11.2012. The invoice copies on Pages 4 to 6 also reflected the remittance dates relied upon by the Tribunal.

Based on these findings, the Tribunal held that the respondent had already paid the entire Service Tax before issuance of the invoices and had thereafter availed the CENVAT credit. In these circumstances, it concluded that the adjudicating authority had correctly dropped the demand relating to the disputed invoices.

Finding no infirmity in the impugned order, the Tribunal upheld the order and dismissed the Revenue’s appeal.

FULL TEXT OF THE CESTAT KOLKATA ORDER

The Revenue is in appeal against the impugned order.

2. The facts of the case are as under: –

(i) On the basis of an intelligence that the assessee had wrongly availed CENVAT Credit of Service Tax paid on deposit insurance service provided by Deposit Insurance and Credit Guarantee Corporation (in short DICGC), which did not appear to qualify as input service as defined under Rule 2(1) of CENVAT Credit Rules, 2004, an investigation was initiated by DGCEI, Kochi Regional Unit. During investigation it was gathered that deposit insurance premium was linked only to the deposit accepted by the respondent/assessee and had no nexus with any other service rendered by the assessee and the assessee had to pay the deposit insurance premium to DICGC against each and every deposit accepted by the assessee. Further, the Revenue was of the view that the assessee could not charge any fee from the depositors for insuring their deposits and the payment of deposit insurance premium was, therefore, a transaction only in money and could not be associated with provision of any service; hence, it was alleged that the deposit insurance service had no connection with any output service of the respondent and could not qualify to be input service for the assessee within the meaning of Rule 2(1) of CENVAT Credit Rules, 2004. From the details of availment of CENVAT Credit in respect of deposit insurance service furnished by the assessee, it was seen that the assessee had availed CENVAT Credit to the tune of Rs.5,46,79,524/-Rs.7,07,26,382/- and Rs.7,32,23,507/- during March, 2012, September, 2012 and November, 2012 respectively against invoices issued on 11.04.2012, 20.09.2012 and 06.12.2012 respectively by DICGC. It was also alleged that the CENVAT Credit were availed during March, 2012 and November, 2012 even before date of issuance of invoices on 11.04.2012 and 06.12.2012 respectively.

(ii) Accordingly, a Show Cause Notice was issued demanding CENVAT Credit to the tune of Rs. 19,86,29,413/- along with applicable interest, in terms of Section 73 of Finance Act, 1994 read with Rule 14 of CENVAT Credit Rules, 2004 and also proposing imposition of penalty in terms of Rule 15 of CENVAT Credit Rules, 2004 read with Section 78 of Finance Act, 1994.

3. The matter was adjudicated vide the impugned order wherein the ld. adjudicating authority dropped the demand raised against the respondent.

4. Therefore, the Revenue is in appeal on the ground that the invoices were issued on 11.04.2012, 20.09.2012 and 06.12.2012 whereas the CENVAT Credit has been availed by the respondent during the months of March, 2012 , November, 2012 i.e., the respondent had allegedly taken the said credit prior to issuance of the invoices dated 11.04.2012, 20.09.2012 and 06.12.2012. Therefore, it is the Revenue’s contention that the respondent is not entitled to the said credit.

5. Heard the Ld. Authorized Representative of the Revenue and perused the records.

6. On perusal of the records, we find that the dispute has been raised with regard to three invoices wherein the dates are mentioned as “11.04.2012”, “20.09.2012” and “06.12.2012”. It is the case of the Revenue that the CENVAT Credit in respect of the said invoices has been taken prior to the issuance of the said invoices.

7. We have gone through the invoices in question. The same are extracted hereinbelow: –

–

–

8. On going through the aforesaid invoices, we find that the remittance for the invoice dated 11.04.2012 has been made on 28.11.2011. For the invoice dated 20.09.2012, the remittance has been made on 28.05.2012 and the invoice dated 06.12.2012 was remitted on 29.11.2012. This shows that the respondent has paid the entire amount of Service Tax thereon prior to issuance of the said invoices. Therefore, as the respondent paid the Service Tax and thereafter have availed the CENVAT Credit thereon, in these circumstances, we hold that the ld. adjudicating authority has rightly dropped the demand raised against the respondent for the invoices in question.

9. In view of this, we do not find any infirmity in the impugned order and hence, the same is upheld.

10. In the result, the appeal filed by the Revenue is dismissed.

(Operative part of the order was pronounced in open court)

Author Bio