Case Law Details

J.K. Engicon Private Limited Vs Commissioner of CGST & CX (CESTAT Kolkata)

J.K. Engicon Private Limited and JK & BSECPL (JV) filed appeals before the CESTAT Kolkata against orders confirming service tax demands under the Reverse Charge Mechanism (RCM) on amounts described as “Royalty on Mineral” in their accounts. As both appeals involved an identical issue, they were heard and decided together.

The first appellant, JK & BSECPL (JV), was engaged in providing works contract services relating to roads and bridges, which were fully exempt from service tax. It acted as a sub-contractor for a road and bridge construction contractor and had not obtained service tax registration because neither the main contractor nor the sub-contractor was liable to service tax on those works. During scrutiny of its balance sheet for 2016-17, the department noticed an expenditure entry of ₹1,04,00,677 under “Royalty on Mineral” and issued a show cause notice dated 22.10.2021, alleging liability to pay ₹15,60,102 as service tax under RCM by invoking the extended limitation period.

The second appellant, J.K. Engicon Private Limited, was engaged in works contract services for organisations including the North Eastern Railway and Public Works Department. During verification of records for FY 2016-17 and part of FY 2017-18, the department found royalty payments of ₹24,40,966 and issued a show cause notice dated 22.10.2021, demanding ₹3,66,145 under RCM by invoking the extended period.

The appellants argued that they were carrying out road and bridge construction covered by the service tax exemption under Notification No. 25/2012-ST dated 20.06.2012. They asserted that they had never obtained any mining licence or rights from the State Government. According to them, the amounts reflected in the balance sheet as royalty represented sums withheld by their clients until Form M and Form N were submitted, after which the withheld amounts were released. They therefore contended that no service tax was payable under RCM. They also challenged the show cause notices as time-barred. Despite these submissions, the adjudicating authority confirmed the demands with interest and penalty, and the Commissioner (Appeals) dismissed their appeals.

The appellants submitted that the show cause notices wrongly assumed that they had paid royalty for obtaining permission or licences to use natural resources. They explained that they had never received any mining rights. Instead, they executed road construction work awarded through the main contractor and purchased stone chips and sand from vendors who themselves held mining licences. Since those vendors were the licence holders liable to pay royalty, the appellants argued that they had not received any taxable service from the Government involving assignment of mining rights.

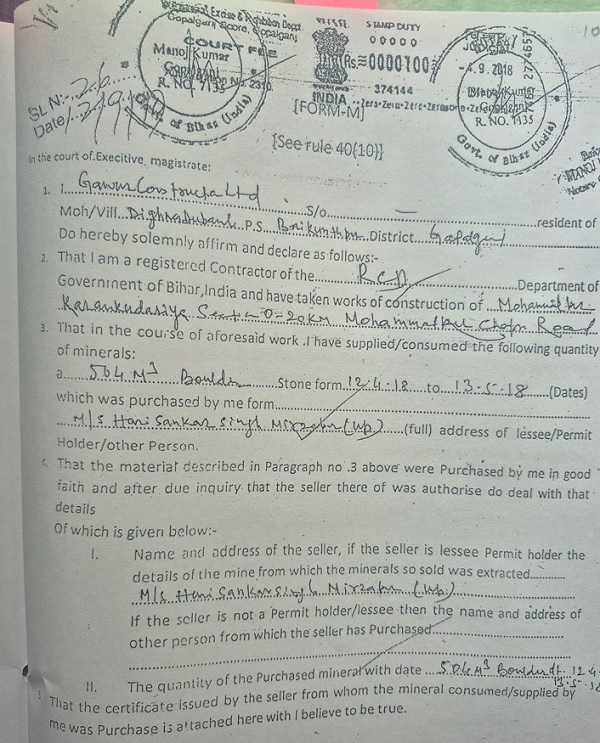

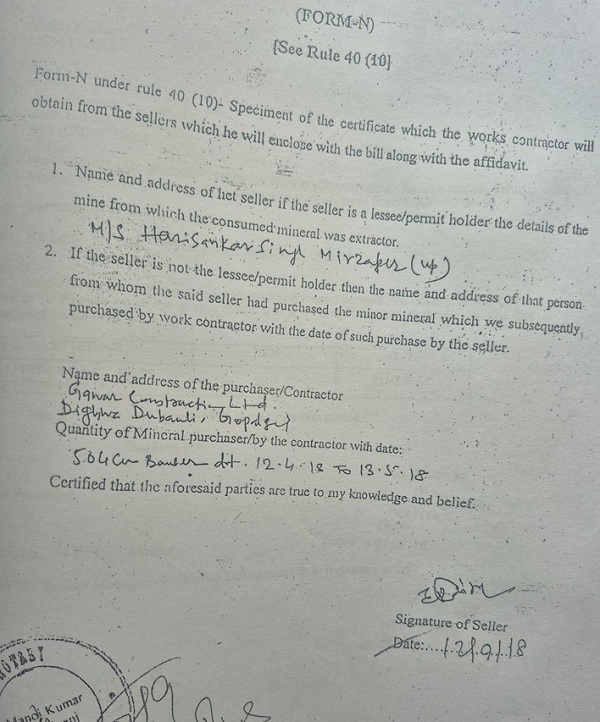

They relied upon Rule 40(10) of the Bihar Minor Mineral Concession Rules, 1972, which requires works contractors to purchase minerals only from licensed dealers and to submit Form M and Form N with their bills. If these forms are not furnished, the concerned works department withholds the royalty portion from contractors’ bills. The appellants explained that this withholding mechanism ensured procurement from authorised suppliers, and the withheld amount was released after submission and verification of the prescribed forms. Accordingly, the entries in their balance sheets represented only such withheld amounts and not royalty paid by them to obtain mining rights. Sample Forms M and N were produced before the Tribunal.

On limitation, the appellants contended that the show cause notices issued in 2021 and 2022 for transactions relating to 2016-17 were barred by limitation. They maintained that they genuinely believed no service tax was payable because they had neither obtained mining licences nor paid royalty to the State Government. They further argued that the department had conducted no independent investigation and had merely relied upon figures appearing in their balance sheets. Since all documents had been produced during departmental verification, the department already possessed the relevant information and therefore could not invoke the extended limitation period. The appellants also relied upon earlier Tribunal decisions supporting their plea on limitation.

The Revenue argued that the appellants themselves had recorded expenditure under the head “Royalty on Mineral” in their balance sheets. Following the amendment effective from 1 April 2016, royalty payments attracted service tax under RCM. According to the department, the tax liability came to light only during detailed verification of the appellants’ books of account, thereby justifying the confirmed demands.

The Tribunal observed that prior to 31 March 2016, royalty paid for mining rights fell within the negative list under Section 66D of the Finance Act, 1994. Following the amendment effective 1 April 2016, services provided by the Government to business entities became taxable, requiring the holder of a mining licence paying royalty to discharge service tax under RCM. The Tribunal explained that royalty is collected where the Government grants mining rights through a licence permitting extraction of minerals over a specified period, and such licence holders are liable to pay service tax on royalty.

However, the Tribunal found that the show cause notices did not specify what mining licence had been obtained by the appellants, which authority had granted such licence, or how royalty had been paid. It also noted that no evidence had been produced to establish that the appellants possessed mining rights or had filed statutory mining returns. The Revenue had failed to produce any material proving the existence of a mining licence. On this ground alone, the Tribunal held that the confirmed demands could not survive.

The Tribunal further noted that the entire demand rested solely on entries in the balance sheets. Referring to Rule 40(10) of the Bihar Minor Mineral Concession Rules, it accepted the appellants’ explanation that the Bihar Road Development authorities withheld the royalty component until Forms M and N established that minerals had been procured from licensed suppliers. After examining sample documents, the Tribunal found that amounts shown as “Royalty on Mineral” represented only amounts withheld by the Government department, not royalty paid by the appellants for any mining licence. It therefore concluded that the documentary evidence supported the appellants’ case and set aside the impugned orders on merits.

The Tribunal also accepted the plea of limitation. It observed that the show cause notices had been issued solely on the basis of balance sheet entries without corroborative evidence. Since the appellants had not obtained mining rights and had produced evidence demonstrating that no service tax was payable, they could legitimately have entertained a bona fide belief that no RCM liability arose. The Tribunal referred to its earlier decisions holding that demands based merely on Form 26AS or balance sheet data, without independent evidence, could not sustain invocation of the extended limitation period. Applying those decisions, it held that the allegation of suppression was unsupported by evidence and that the demands were also barred by limitation.

Accordingly, the Tribunal allowed both appeals, set aside the impugned orders on merits as well as on limitation, and held that the appellants would be entitled to consequential relief in accordance with law.

FULL TEXT OF THE CESTAT KOLKATA ORDER

At the time of Hearing, the Ld. Consultant appearing for both the appellants submits the issue is identical in both the cases. Hence, it is prayed that both the appeals may be taken up for disposal together. The Ld. AR agrees the issue is identical. Hence, with the consent of both the sides, the appeals have been taken up together for disposal.

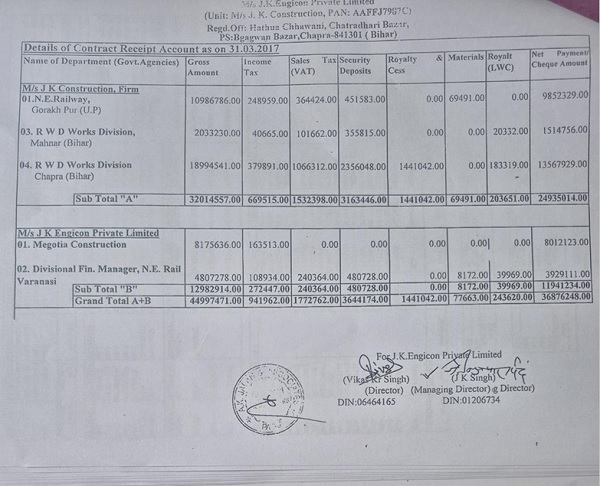

2. The Appellant, M/s. JK & BSECPL (JV), is engaged in the business of providing „Works Contract’ service in respect of roads and bridges, which are fully exempt from Service Tax. They were undertaking contract as sub-contractor of Gawar Construction Limited, who is engaged in construction of Road and Bridge. Since no Service Tax is applicable for the main contractor and the sub-contractor [the appellant], the appellant has not got themselves registered with the Service Tax Dept. Based on the Balance Sheet of the appellant, the Revenue Dept. noted that the appellant had disclosed expenditure on account of “Royalty on Mineral” amounting to Rs 1,04,00,677/-, during the period 2016-17. On such amount, the Dept. issued SCN dated 22.10.2021 alleging that the appellant is liable to pay service tax amounting to Rs. 15,60,102/- on RCM basis. The SCN was issued by invoking the extended period provisions.

3. The appellant, M/s. J. K. Engicon Private Limited, is engaged in the business of proving of „Works Contract’. During the material period, they have provided the works contract service Mainly to NE Railway, Gorakhpur and Varanasi, PWD Division and others. During verification process initiated by Central GST & CX, range – Chappra, for the FY 2016-17 and 2017-18 (April to June 2017), from the documents submitted by the appellant, The Revenue has found that the appellant has made payment on account of „“Royalty” amounting to Rs 24,40,966/- as found from the appellant’s payment certificate. On such amount, the Dept. issued SCN dated 22.10.2021 alleging that the appellant is liable to pay service tax amounting to service tax amounting to Rs. 3,66,145/- RCM basis. The SCN was issued by invoking the extended period provisions.

4. The appellants submitted that they are undertaking road and bridge construction work on which full Service Tax exemption has been granted in terms of Notification No.25/2012 ST dated 20.6.2012. They have not obtained any License towards any Mining activity from any State Govt authorities. The amount shown in the Balance Sheet is on account of withholding of the amounts by the clients on account of Royalty. Such amounts are subsequently released when the requisite Form M and N are submitted. Therefore, it was pleaded that no Service Tax is required to be paid on RCM basis. The appellants also submitted that the SCN issued on 22.10.2021 and 21.04.2022, is time barred. However, the Adjudicating authority, after due process, went on to confirm the demand along with interest and penalty. On Appeal, the Commissioner (Appeals) dismissed the Appeals. Hence, the appellants are before the Tribunal.

5. The Ld. Chartered Accountant, appearing on behalf of the appellant, makes the following submissions:

6. In the SCN it has been alleged that the appellant has paid „Royalty‟ to the Government for giving the permission or license for using natural resources of Material/adjacent land in the state as per norms and rate. It is thus an assignment of right to use any natural resources. However, the appellant had never been granted any permission or license for using natural resources of Material/adjacent land. M/s. Gawar Construction Limited has been awarded the works contract for Construction of Road (State Highway) from Bihar State Road Development Corporation Limited. Further, M/s. Gawar Construction Limited has given such contract to the appellant on subcontract basis. The appellant has never been granted any permission regarding assignment of right to use any natural resources. Since, there is no service involved, the question of payment of service tax under RCM does not arise at all. That the appellant has granted a work order from M/s. Gawar Construction Limited for Construction of Road (State Highway) from Bihar State Road Development Corporation Limited. To complete the above contract, the appellant purchased stone chips and sands (Minerals) from the vendors. These vendors got the license from the mining department for permission regarding assignment of right to use any natural resources. The appellant has purchased the stone chips and sands from these vendors only.

7. As per the Rule 40(10) of the Bihar Minor Mineral Concession Rules, 1972, which states that

“To prevent evasion of royalty it is provided that works contractor shall purchase the minerals from lessee/permit holder and authorised dealers only and no Works Department shall receive the bill which the works contractors submit to recover cost etc. of mineral used by them in completion of the works of the Works Department under any agreement from the works contractor if the said bill is not accompanied by an affidavit in Form ‘M’ with particulars in Form ‘N’ of these Rules alongwith a photo copy of the said affidavit and particulars. It shall be the duty of the officer who receives or on whose behalf the said bill is received to send the photo copy of the Affidavit and particulars to the District Mining Officer/Assistant Mining Officer within whose jurisdiction the mineral was allegedly purchased, for verification.

If contents of the said affidavit on verification by the concerned District Mining Officer/Assistant Mining Officer is found to be false either wholly or partly it shall be presumed that the concerned mineral was obtained by illegal mining and in that event the said District Mining Officer/Assistant Mining Officer shall take action as prescribed in these Rules against the maker of the said affidavit:

Provided that if the Works Contractor deposits or pays the royalty in respect of the mineral so consumed/supplied by him as shown in the aforesaid affidavit and particulars the said District Mining Officer/Assistant Mining Officer in his discretion may not take action as prescribed in this Rule”.

8. Therefore, in the present case, the appellants have purchased the stones and other minerals from such registered vendors. The Bihar Govt Department which is the authority granting the contract of Road and Bridge Building, retains the value of Royalty from the Bills submitted by the Contractor, to ensure that the Form M and Form N are submitted by the Vendor for having purchased the Minerals from the Registered License Holder Vendors, who are liable to pay the Royalty to the Govt. Thus, the amount shown in the Balance Sheet is the amount being withheld by the Bihar Govt, till the Form M and Form N is submitted by the contractor. The withheld amounts are released as and when such Forms are submitted by the contractor. This is an ongoing process. The sample copies of such Form M and N is enclosed for the perusal of the Hon’ble Tribunal.

9. Further, the appellants have not been granted any Mining rights by way of any License. The Service Tax is payable only when any Mining Rights have been obtained by anyone on which Royalty is paid to State Govt. In this case, the Revenue Dept has not brought in any evidence to the effect that the appellants had obtained any Mining Rights on which they are paying the Royalty.

10. Based on the above submissions, the Ld Consultant prays that the appeals may be allowed on merits.

11. He also takes the stand that the SCN issued on 22.10.2021 and 21.04.2022 for the transactions taking place in 2016-17 is clearly hit by time bar. He submits that appellant had not obtained any Mining License and were not paying any Royalty to any State Govt Dept. On the other hand part of their Invoice value was being withheld by the State Govt Authorities, for want of Form M and Form N to be submitted by the appellants. Therefore, the appellants carried a bona fide belief that no Service Tax is payable on RCM basis for such transactions.

12. It is submitted that the Department has not conducted any independent investigation in this instant case. Further, it is evident from the Show Cause Notice itself that the Department (Anti evasion unit) has simply taken the figures available in Balance Sheet provided by the appellants and accordingly worked out the differential demand. It is well settled by the CESTAT in several cases that where the demand is based solely on balance sheet data, the extended period is not invocable and the demand is liable to be set aside on limitation alone. Also, The Department itself admitted that the appellant has provided numbers of documents as asked for time to time, when asked by the Department. Therefore, the entire information was in the knowledge of the Revenue. The appellants rely upon the following cases for arguments on limitation:

I. M/s. Munna Construction v. Commissioner of C. . & S.T., Jamshedpur [Final Order No. 77625 of 2024 dated 22.11.2024 in Service Tax Appeal No. 76359 of 2014 (CESTAT, Kolkata)]

II. M/s. Arya Logistics v Commissioner of C. Ex. & S.T., Rajkot [Final Order No. 11700 of 2023 dated 17.08.2023 in Service Tax Appeal No. 12389 of 2014 (CESTAT, Ahmedabad)]

III. M/s. Balajee Machinery v Commissioner of C.G.S.T. & Excise, Patna-II [2022 (66) GSTL 440 (Tri.-Kol)] Service Tax Appeal Nos.75393 & 75451 of 2024

13. In view of the above submissions, it is prayed that the appeals may be allowed even on account of time bar.

14. The Ld. A R appearing for the Revenue submits that the appellants have recorded that they have incurred expenditure on account of „Royalty on Mineral‟ in the Balance Sheet. As per the Service Tax provisions, on payment of Royalty, the Service Tax is payable on RCM basis with effect from 01.04.2016 in view of the amendment carried out to Section 66D of the Finance Act 1994. The non-payment of Service Tax liability came to light only on account of detailed verification of the books of accounts of the appellant. Therefore, he justifies the confirmed demands.

15. Heard both the sides. Perused the appeal papers and other documents submitted.

16. The Royalty payment made for rights granted towards Mining was earlier covered under Negative List – Section 66D till 31.03.2016. With effect from 1-4-2016, however, section 66D(a)(iv) of the Finance Act was amended and ‘all services provided by the government to a business entity’ were excluded from the negative list of services. Thus, services rendered by the government to a business entity became chargeable to service tax with effect from 1-4-2016. During the period under discussion in the present case, requires the License Holder to pay the Service Tax on RCM basis.

17. The Royalty is collected for the rights being conferred to any party by way of License, by which the party is allowed to mine the mineral for a particular number of years. Generally, such Mining Lease [Right] is conferred for a number of years. As and when the goods are mined, the right holder is required to pay the Royalty. The Service Tax is to be paid on RCM basis for such Royalty paid by the License Holder.

In the present case, the SCN is totally silent as to what kind of License was obtained by the appellant from which authority. It is also silent as to how such Royalties were being paid by the appellant. In case of such Licenses, the License holder is also required to file periodical Returns with the State Govt. authorities towards the quantity of goods which are mined and Royalty paid. The Revenue has not brought in any evidence in this context. On this ground itself, the confirmed demand fails.

18. The entire demand is based on the entry made in the Balance Sheet showing the expenditure on account of „Royalty on Mining‟. The appellants have explained the reason for such entries. As could be seen from the Rule 40(10) of the Bihar Minor Mineral Concession Rules, 1972, extracted above, Bihar State Road Development Corporation, insists that the Stones are procured from the License Holders, who are liable to pay the Royalty. Till the proof of having purchased the stones from such License Holders is not made available by the appellant by way of Form M and N, the Royalty portion is withheld and is released once the Forms are submitted.

19. I have gone through some of the sample documents submitted by the appellants, which are reproduced below:

20. From the above Statement it is seen that Rs.14,41,043/- has been withheld by RWD Works Division under the Heading of Royalty. This cannot be viewed as Royalty payment by the appellant towards any License granted for Mining by the State Department.

–

21. The above Form M and N submitted by the main contractor shows that such Forms are being submitted to get the withheld amounts released by the Road Development Corporation.

22. The above documentary evidence prove that the „Royalty on Mineral‟ accounted for by the appellant is only on account of such withheld amounts.

23. Considering the factual details and statutory provisions discussed above, I set aside the impugned Orders and allow the appeals on merits.

24. As canvassed by the appellants, the SCN has been issued based on the entries made in the Balance Sheet itself, without any corroborative evidence. The factual details point out that they appellant has not been granted any Mining Rights. Therefore, the appellant could have carried a Bonafide belief that no Service Tax is required to be paid on RCM basis. The SCN has been issued on 22.10.2021 and 21.04.2022 and the appellants have been able to counter the demand by proper evidence showing that no Service Tax is payable.

25. This Bench in several cases has held that mere reliance of 26AS / Balance Sheet, without any corroborative evidence, for issuing of Show Cause Notice is not legally sustainable for extended period and the demand would be hit by time bar. This Tribunal in the case of Tabassum Enterprises vs. C, CGST & CX vide Final Order No.75452/2025 dated 19.09.2025 (Service Tax Appeal No.75037 of 2025) has held as under:

“5. I find that the present demand has been raised and confirmed on the basis of data provided by the Central Board of Direct Taxes (CBDT). It is observed that the said demand has been confirmed without the support of any independent or corroborative evidence from the Service Tax records. Such mechanical reliance on Income Tax data, without verification of the nature of receipts or proof of taxable services rendered, is impermissible in law It is a settled legal position that mere entries in income tax returns or Form 26AS cannot, by themselves, establish liability under the Finance Act, 1994, unless corroborated by evidence demonstrating rendition of taxable service.

5.1. In support of this view, I rely upon the decision in the case of M/s. Rishu Enterprise vs Commissioner of C.G.S.T. & Excise, Dibrugarh, in Final Order No. 75177 of 2024 dated 08.02.2024 in Service Tax Appeal No. 75509 of 2022 [CESTAT, Kolkata], wherein this Tribunal has observed as under: – “8. In view of the judicial pronouncement of this Tribunal, we hold that merely on the basis of Form 26-AS issued by the Income Tax Department, the demand of Service Tax is not sustainable against the appellant. ……….. .

11. In view of this, we hold that the impugned demand is not sustainable against the appellant on the basis of the details provided by the Income Tax Department in Form 26AS and the extended period of limitation is not invokable .”

5.2. The same view has been held by the Tribunal at Allahabad in the case of M/s.Quest Engineers & Consultant Pvt. Ltd. v. Commissioner of C.G.S.T. &C.Ex., Allahabad [2022 (58) G.S.T.L. 345 (Tri. – All.)] observing as follows: –

“12. …. ….We further find that Form No. 26AS is not a statutory document for determining the taxable turnover under the Service Tax provisions. We find that Form No. 26AS is maintained on cash/ receipt basis by the Income Tax Department for the purpose of tax deducted at source, etc. being the relevant data for Income Tax. Whereas under the Service Tax provisions, the service tax is chargeable on mercantile basis (accrual basis) on the service provided whether the value of such service is received or not. Thus, we find that the whole basis of show cause notice is incorrect and/or misconceived .”

5.6. Following the ratio of the decisions cited supra, I hold that the demand of service tax confirmed in the impugned order, solely relying the data received from CBDT, without adducing corroborative evidence in support, cannot be sustained. Thus, I observe that the demand confirmed in the impugned order is liable to be set aside on this ground itself.”

26. The ratio of the cited case law is squarely applicable to the facts of the present case. I find that in the present case the allegation of suppression has not been corroborated by any evidence by the Revenue against the Appellants. Therefore, following the ratio of the cited case law, I set aside the impugned orders on account of time bar also.

27. The appeals are allowed. The appellants would be eligible for consequential relief, if any, as per law.

(Order pronounced in the open court on 15.06.2026.)

Author Bio