SEBI initiated proceedings against Rajesh Exports Limited (REL) and its Chairman and Managing Director, Rajesh Mehta, following a shareholder complaint alleging potential financial misrepresentation relating to large outstanding trade receivables. An investigation covering the period from April 1, 2020 to March 31, 2024 was undertaken, along with a forensic audit.

SEBI observed prima facie non-cooperation by REL during the investigation and forensic audit. The company allegedly failed to provide access to ERP systems, books of accounts, journal dumps, and key records relating to overseas subsidiaries. According to the forensic audit report, only a small portion of selected transaction samples could be verified through complete documentation, while substantial information remained unavailable.

The investigation found that a substantial portion of REL’s consolidated revenue and profitability originated from overseas subsidiaries and step-down subsidiaries, particularly entities connected with Valcambi SA. SEBI noted that REL failed to upload audited financial statements of several subsidiaries and step-down subsidiaries despite statutory disclosure requirements. It also failed to provide detailed customer-wise sales data, vendor-wise purchase data, debtors, creditors, and related-party transaction information relating to those entities. According to SEBI, these omissions impaired regulatory verification and investor transparency.

SEBI further examined REL’s consolidated financial statements and observed significant discrepancies. While REL maintained that Valcambi SA was the principal operating entity driving group revenues, audited standalone financial statements of Valcambi reflected revenues that constituted only a negligible fraction of the consolidated revenues reported by GGR and REL. SEBI found that REL failed to furnish supporting records such as invoices, customer details, vendor records, confirmations, inventory trails, or other primary evidence capable of verifying the reported overseas revenues. Based on available material, SEBI formed a prima facie view that approximately ₹15,15,385 crore, representing about 99.80% of subsidiary-attributed revenues during FY 2020-21 to FY 2024-25, appeared to be misrepresented.

The investigation also identified inconsistencies in multiple sales-related submissions made by REL to SEBI. Customer-wise sales figures varied materially across different submissions, and REL’s explanations were found unsatisfactory. SEBI observed that furnishing contradictory information impeded independent verification of reported sales figures and raised concerns regarding the reliability of the company’s disclosures.

On the standalone financial statements, SEBI examined transactions allegedly recorded with Affluence Shares and Stocks Private Limited. REL reported sales and purchases exceeding ₹11,400 crore with Affluence between FY 2021-22 and FY 2023-24. However, Affluence informed SEBI that REL was never its client and that no transactions had been executed with or on behalf of REL. Investigation indicated that the transactions substantially corresponded to gold derivative trades conducted by Rajesh Mehta through his personal account with Affluence. SEBI observed no direct banking transactions between REL and Affluence and found no documentary evidence showing that Rajesh Mehta acted as an authorized conduit for REL. SEBI therefore formed a prima facie view that REL had recorded non-genuine sales and purchases aggregating to ₹11,486.60 crore and ₹11,488.42 crore respectively, resulting in inflation of standalone financial statements.

SEBI concluded that the available material prima facie indicated misrepresentation of consolidated and standalone financial statements, dissemination of misleading financial information, obstruction of investigation, and violations of provisions of the SEBI Act, PFUTP Regulations, LODR Regulations, and disclosure requirements under applicable laws.

WTM/KV/CFID/CFID-SEC6/32431/2026-27

SECURITIES AND EXCHANGE BOARD OF INDIA

INTERIM ORDER

UNDER SECTIONS 11 (1), 11 (4) AND 11B OF THE SECURITIES AND EXCHANGE BOARD OF INDIA ACT, 1992 IN THE MATTER OF RAJESH EXPORTS LIMITED

In respect of:

| Sr. No. | Name of Noticees | PAN |

| 1. | Rajesh Exports Limited (REL) | AAACR8642N |

| 2. | Rajesh Mehta | ADKPM0172C |

(The entities mentioned above are individually referred to by their respective names or Noticee No. and collectively referred to as “Noticees”, unless the context specifies otherwise)

A. BACKGROUND

1. The present proceedings have emanated from an investigation conducted for the period between April 01, 2020 to March 31, 2024 (hereinafter referred to as “Investigation Period”) by the Securities and Exchange Board of India (hereinafter referred to as “SEBI”) involving abovementioned Noticees. Wherever deemed necessary, reference has been made to period outside the investigation period.

2. SEBI received a complaint vide e-mail dated March 11, 2024 wherein a shareholder of Rajesh Exports Limited (hereinafter referred to as “Company”/ “REL”) has alleged potential financial misrepresentation in the books of REL with respect to large sum of trade receivables outstanding for more than two years.

3. REL is a public limited company incorporated on February 01, 1995 under CIN No: L36911KA1995PLC017077 having its registered office at #4, Batavia Chambers, Kumara Krupa Road, Kumara Park East, Bangalore – 560001. The Company is a gold refiner and manufacturer of gold products. It exports its products to various countries around the world. It also sells its products in wholesale and retail in India and through its own retail showrooms under the brand name ‘SHUBH Jewellers’. It is a mid-cap company having INR 3,210 crore market capitalization as on June 03, 2026. The shares of the Company are listed on BSE (531500) and NSE (RAJESHEXPO) and the share price as on June 03, 2026, was INR 108.70 (Face Value: INR 1/- per share).

4. Pursuant to preliminary examination of the complaint received from the shareholder, SEBI appointed an Investigating Authority on October 23, 2024 to, inter alia, investigate into possible violations of provisions of the Securities Contracts (Regulation) Act, 1956 (hereinafter referred to as the “SCRA”), the Securities and Exchange Board of India Act, 1992 (hereinafter referred to as the “SEBI Act”), the Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015 (hereinafter referred to as the “LODR Regulations”) and the Securities and Exchange Board of India (Prohibition of Fraudulent and Unfair Trade Practices Relating to Securities Markets) Regulations, 2003 (hereinafter referred to as the “PFUTP Regulations”) and other applicable provisions of securities laws. A Forensic Auditor viz. BDO India Services Pvt Ltd (hereinafter referred to as “Forensic Auditor”/ “BDO”) was also appointed in the matter on December 03, 2024.

B. PRIMA FACIE FINDINGS OF INVESTIGATION AND CONSIDERATION OF ISSUES

5. During the course of investigation, the Investigating Authority (hereinafter referred to as the “IA”) issued various summons for personal appearance and for production of documents to the Noticees. The Noticees submitted information and documents in multiple tranches, which were incomplete in many aspects even after providing sufficient time to furnish the same. The Noticees have also not cooperated with the Forensic Auditor and resultantly, the Forensic Audit Report (hereinafter referred to as “FAR”) dated March 25, 2026 has been prepared subject to several limitations that have impeded the audit process and consequently the ongoing investigation. Based on the information available on record, the prima-facie findings and observations with respect thereto are discussed in the subsequent paragraphs. The relevant provisions of securities laws prima facie violated by the Noticees as discussed in this order are reproduced in Annexure-A for ease of reference.

B.1. Non-cooperation by the Noticees

6. Upon perusal of the FAR submitted by the Forensic Auditor, it is prima facie observed that the conduct of REL has been characterized by significant noncooperation, resulting in several limitations that have impeded the audit process.

7. The Forensic Auditor has highlighted grave restrictions on the scope of their audit, notably:

I. REL failed to provide access to its Enterprise Resource Planning (ERP) systems and Books of Accounts. Furthermore, the vital Journal Dump of the company was withheld, effectively shielding the underlying accounting entries from independent scrutiny.

II. With respect to foreign subsidiaries, REL refused to share requisite data, taking shelter under the Swiss Federal Act on Data Protection. Consequently, the Forensic Auditor’s review was confined solely to financial statements, without access to primary evidentiary records.

III. Even where ledgers were produced, they were found to be deficient since Narrations were only partially visible, and the omission of corresponding ledger account names rendered it impossible to ascertain the true nature or purpose of the recorded transactions.

8. The FAR reveals a systematic failure on the part of REL to substantiate its financial figures through transaction testing. Out of a selected sample of INR 7,021.36 crores, REL provided a complete set of documents for a negligible 2.03% of the sample value. Similarly, in the testing of sales samples totalling INR 12,217.15 crores, the Forensic Auditor could verify only 35.07% of the value with complete documentation. For the remainder of the samples, documentation was either partial or completely absent, leaving substantial transactions entirely unsubstantiated. Such a high degree of data and document pendency, as tabulated in the ‘Limitations – Data Pendency’ section of the FAR, prima facie suggest a deliberate attempt to withhold information and raise serious concerns regarding the authenticity of the financial disclosures made by REL.

B.2. Non‑disclosure of material consolidated financial information

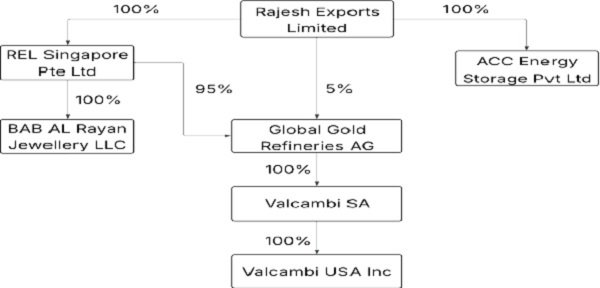

9. As per the Annual Reports and submissions of REL, it is noted that REL has a multi-layered corporate structure comprising domestic operations and multiple overseas subsidiaries/ step-down subsidiaries, with a substantial portion of consolidated operations originating outside India. The corporate structure of REL is illustrated below.

Figure No. 1

Corporate Structure of REL

Note: During FY 2024-25 REL’s shareholding in ACC Energy Storage Pvt Ltd was reduced from 100% to 51.05%.

10. REL, vide emails dated August 27, 2024 and September 13, 2024, inter-alia, provided below-mentioned details regarding the aforesaid subsidiaries of REL:

I. Rajesh Exports Limited, India: A listed public limited company engaged in the import and sale of gold bullion, manufacture of gold products, and export, wholesale and retail sale (including under the brand ‘Shubh Jewellers’) of gold products.

II. REL Singapore Pte Ltd, Singapore (hereinafter referred to as ‘REL Singapore’): A wholly owned subsidiary of REL, stated to be a holding Company and not engaged in any day to day business activity.

III. Global Gold Refineries AG, Switzerland (hereinafter referred to as ‘GGR’): An entity in which REL Singapore Pte Ltd holds 95% and REL holds 5%. It is stated to be a holding company of Valcambi SA and not engaged in day to day business activities.

IV. Valcambi SA, Switzerland (hereinafter referred to as ‘Valcambi’): A wholly owned subsidiary of GGR engaged in refining precious metals and sale of branded precious metal bars including gold bullion bars to various entities including bullion banks, international banks, central banks, bullion exchanges and bullion dealers; receives precious metals under arrangements such as purchase, loan and safekeeping.

V. Valcambi USA Inc, USA (dissolved in December 2023): A wholly owned subsidiary of Valcambi SA engaged in marketing Valcambi brand in North America.

VI. Bab AL Rayan Jewellery LLC, UAE: A wholly owned subsidiary of REL Singapore Pte Ltd, stated to be engaged in procuring scrap gold/ gold dore bars and refining/ manufacturing gold products for sale/export.

VII. ACC Energy Storage Pvt Ltd, India: A wholly owned subsidiary of REL, stated to be a start-up engaged in the research of Advanced Energy Storage Devices with operations yet to begin.

VIII. Upon analysis of the ‘Revenue from Operations’ and ‘Profit After Tax’ of REL on standalone and consolidated basis, as disclosed in its financial statements, it is observed that significant component of REL’s consolidated operations are emanating from its subsidiaries/ step-down subsidiaries. The same is tabulated as under:

Table no. 1

Revenue from Operations and Profit After Tax of REL on standalone and

consolidated basis (INR in crore)

| Particulars | FY

2020-21 |

FY

2021-22 |

FY

2022-23 |

FY

2023-24 |

FY

2024-25 |

FY

2025-26 |

| Consolidated Revenue from Operations (A) | 2,58,306 | 2,43,128 | 3,39,690 | 2,80,676 | 4,23,099 | 7,78,716 |

| Standalone Revenue from Operations (B) | 2,060 | 6,237 | 5,762 | 5,401 | 7,027 | 9,189 |

| Revenue from Operations emanating from subsidiaries/ stepdown subsidiaries (A-B) | 2,56,245 | 2,36,891 | 3,33,928 | 2,75,276 | 4,16,072 | 7,69,527 |

| Consolidated Profit After Tax (C) | 845 | 1,009 | 1,432 | 336 | 95 | 113 |

| Standalone Profit After Tax (D) | 99 | 23 | 30 | 17 | 24 | 32 |

| Profit After Tax emanating from subsidiaries/ stepdown subsidiaries (C-D) | 746 | 987 | 1,402 | 318 | 71 | 81 |

12. In view of the above and based on REL’s own submissions and disclosures, it is observed that REL’s subsidiaries/ step-down subsidiaries constitute a significant component of REL’s consolidated operations. Accordingly, the revenue, profitability, receivables, payables, inventory etc., of REL’s subsidiaries/ step-down subsidiaries have a direct and material bearing on REL’s consolidated financial position, performance and valuation, and consequently on the decision making of investors investing in the equity of REL in the Indian securities market. Therefore, the financial information relating to REL’s subsidiaries/ step-down subsidiaries assumes material significance for assessment of REL’s consolidated financial statements.

Non-availability of financial statements of REL’s subsidiaries/ step-down subsidiaries

13. It is noted that under the provisions of section 128(1) of the Companies Act, 2013, every company is under a statutory obligation to maintain books of account and financial statements that reflect a “true and fair view” of its state of affairs. This transparency is further reinforced by Section 136(1) of the Companies Act, 2013, which mandates companies with subsidiaries to place separate audited financial statements of each such subsidiary on their website. Furthermore, Regulation 46(2)(s) of the LODR Regulations casts a specific duty upon listed entities to publish the separate audited financial statements of every subsidiary on its website at least 21 days prior to the Annual General Meeting.

14. Upon examination of material on record, it is noted that REL has failed to upload the financial statements of any of its subsidiaries or step-down subsidiaries (SDSs) on its website. By failing to provide these statements, particularly for significant entities like Valcambi SA which drive the bulk of REL’s consolidated operations, the company has effectively shielded its primary revenue-generating components from the scrutiny of investors, auditors and regulators alike. Such non-disclosure deprives the shareholders of their right to assess the true financial health and risks associated with the consolidated entity, thereby impairing their ability to make informed investment decisions in the equity of REL in securities market.

15. It is further observed that when directed to rectify these omissions, REL’s compliance was marked by selective and incomplete disclosures. While certain statements for REL Singapore, GGR, and Valcambi SA were provided, the following material financial statements remain outstanding:

I. Standalone financial statements of REL Singapore for FY 2023-24 to FY 2024-25;

II. Standalone financial statements of Bab AL Rayan Jewellery LLC for FY 2020-21 to FY 2024-25;

III. Consolidated financial statements of GGR for calendar years 2024;

IV. Standalone financial statements of GGR for calendar years 2020 to 2024;

V. Standalone financial statements of Valcambi SA for calendar years 2020;

VI. Standalone financial statements of Valcambi USA Inc for calendar years 2020 to 2023;

VII. Standalone financial statements of ACC Energy for FY 2022-23 to FY 202425.

16. The conduct of CA P V Ramana Reddy, the Proprietor at M/s P V Ramana Reddy & Co, and CA P L Venkatadri, Partner at M/s BSD & Co, the Statutory Auditors of REL (Statutory Auditors) also warrants scrutiny. During their depositions on January 16, 2026, the statutory auditors undertook to provide the missing subsidiary financial statements and their complete audit working papers.

However, as on the date of this Order, no such documents have been received by SEBI, indicating a lack of cooperation with the investigatory process.

17. REL was granted multiple opportunities to explain these lapses via summons dated January 30, February 09, and February 16, 2026. In its response dated March 17, 2026, REL contended that its standalone and consolidated filings were “adequate” and that subsidiary financials were “clearly derivable” from the consolidated figures. The response of REL received vide email dated March 17, 2026, inter alia stated as under:

“…REL has diligently published the stand alone financial statements and the consolidated financial statements on it’s website for all the years which can be found on the website. From the consolidated and the standalone financial statements, the financial statements of the subsidiaries are clearly derivable. We are of the opinion that publishing the standalone and consolidated financial statements was adequate and fulfilled the required provision.”

18. I find the aforementioned contention of REL to be fundamentally untenable. The requirement to publish subsidiary-wise financial statements under Section 136(1) of the Companies Act and Regulation 46(2)(s) of the LODR Regulations is an independent, mandatory disclosure requirements that cannot be substituted by consolidated reporting at the company’s discretion as has been done by REL. Consolidated statements, by their very nature, involve the elimination of intra-group transactions and provide an aggregated view that masks entity-specific risks, cash flows, and related-party exposures. REL’s argument that these details are “derivable” is conceptually flawed and appears to be an attempt to circumvent the transparency requirements essential for the integrity of the securities market.

Non availability of information at consolidated level

19. It is observed that REL exercises absolute control (100%) over GGR and Valcambi SA through a combination of direct and indirect holdings. Notwithstanding this control, SEBI issued multiple communications—including emails dated June 28, July 11, August 06, August 21, and September 04, 2024, as well as summons dated June 16, July 02, and July 24, 2025—seeking granular details of consolidated operations, specifically party-wise data for sales, purchases, debtors, creditors, and inventory. In its responses, REL contended that it lacked access to such information, citing the restrictive nature of Swiss laws and confidentiality agreements governing GGR and Valcambi SA.

20. To substantiate its claim of legal impossibility, REL, vide email dated September 13, 2024, submitted copies of the Swiss Federal Act on Data Protection (‘FADP’) and a sample confidentiality agreement. REL asserted that these statutes prohibit the cross-border transfer of “personal data” to India. This position was further reiterated by an email from the CEO of Valcambi, forwarded by Mr. Rajesh Mehta on September 12, 2024. I have examined the provisions of the FADP and find REL’s reliance on the same to be misplaced. The relevant Articles of the FADP are reproduced as under::

“Art. 1 Purpose: This Act has the purpose of protecting the personality and fundamental rights of natural persons whose personal data is processed.

Art. 2 Personal and material scope of application:

1 This Act applies to the processing of personal data of natural persons…”

Art. 16 Principles

1 Personal data may be disclosed abroad if the Federal Council has decided that the legislation of the State concerned or the international body guarantees an adequate level of protection.

…..

Art. 17 Exceptions

1 In derogation from Article 16 paragraphs 1 and 2, personal data may be disclosed abroad in the following cases:

a. ………

b. …….

c. Disclosure is necessary in order to:

1. safeguard an overriding public interest; or

2. establish, exercise or enforce legal rights before a court or another competent foreign authority.

…..

21. From a plain reading of the aforesaid provisions, I note that the protection afforded by the FADP is explicitly limited to “natural persons” and does not extend to corporate information or the data of legal entities like Valcambi. Even otherwise, Article 17 of the FADP provides statutory exceptions allowing personal data transfers if disclosure is necessary to establish, exercise, or enforce legal rights before a competent foreign authority such as SEBI. Consequently, REL’s plea that it is legally barred from furnishing corporate financial data to a regulator is untenable.

22. I further note that a listed entity operating in the Indian securities market cannot rely upon private confidentiality arrangements or foreign data protection provisions to defeat or dilute its statutory disclosure obligations under Indian securities laws. Where a listed entity chooses to structure its operations through overseas subsidiaries and thereafter consolidates the financial results of such entities into its public disclosures, it remains under a continuing obligation to maintain and furnish sufficient underlying information to enable regulatory verification and investor transparency.

23. From the aforesaid, it is prima facie evident that while REL’s consolidated financial performance is almost entirely (approx. 97%-99%) dependent on its overseas subsidiaries, particularly Valcambi SA, the company has systematically withheld the financial statements of these entities from the public domain. Furthermore, it has failed to provide the necessary underlying data (party-wise details of vendors, customers, etc.) to the Investigating Authority despite repeated summons.

24. The cumulative effect of these omissions is that investors have been presented with consolidated revenue and balance sheet figures without any means to verify the underlying financial numbers of the subsidiaries. This has created a severe information asymmetry, keeping the public investors and shareholders in the dark regarding the true financial position of REL’s consolidated operations and the veracity of its reported performance.

Information/ Documentation required from REL:

25. REL failed to provide the below-mentioned financial statements of its subsidiaries/ step-down subsidiaries:

I. Standalone financial statements of REL Singapore for FY 2023-24 to FY 2024-25;

II. Standalone financial statements of Bab AL Rayan Jewellery LLC for FY 2020-21 to FY 2024-25;

III. Consolidated financial statements of GGR for calendar years 2024;

IV. Standalone financial statements of GGR for calendar years 2020 to 2024;

V. Standalone financial statements of Valcambi SA for calendar years 2020;

VI. Standalone financial statements of Valcambi USA Inc for calendar years 2020 to 2023;

VII. Standalone financial statements of ACC Energy for FY 2022-23 to FY 2024-25.

26. Additionally, REL also failed to provide the below-mentioned information pertaining to its subsidiaries/ step-down subsidiaries for each year under investigation:

I. sales register indicating the customer wise list of sales;

II. purchase register indicating the vendor wise list of purchases;

III. detailed breakup of customer wise debtors;

IV. detailed breakup of vendor wise creditors;

V. list of related parties and related party transactions

27. By failing to provide above information, despite multiple emails and summons, REL obstructed the investigation and impaired SEBI’s ability to verify the authenticity of consolidated financial statements, thereby violating Section 11(2) (ia) and 11C (3) of the SEBI Act, 1992. Further, by failing to upload the audited financial statements of its subsidiaries/ step-down subsidiaries on its website, REL violated Regulation 46(2)(s) of the LODR Regulations and Section 136(1) of the Companies Act, 2013.

B.3. Misrepresentation of Financial Statements – Consolidated basis

28. I note that REL, in its annual reports for FY 2020-21 to FY 2024-25, disclosed consolidated revenues from operations aggregating to approximately INR 15,44,899 crore and consolidated purchases aggregating to approximately INR 15,43,533 crore. The details thereof are reproduced below:

Table no. 2

Sales and Purchases of REL on consolidated basis (INR in crore)

| Particulars | 2020-21 | 2021-22 | 2022-23 | 2023-24 | 2024-25 | Total |

| Sales | 2,58,306 | 2,43,128 | 3,39,690 | 2,80,676 | 4,23,099 | 15,44,899 |

| Purchases | 2,59,600 | 2,41,771 | 3,35,980 | 2,78,167 | 4,28,015 | 15,43,533 |

29. In order to examine the genuineness and verifiability of the aforesaid consolidated sales and purchase figures, SEBI sought customer-wise and vendor-wise details pertaining to the consolidated revenues and purchases. However, despite repeated summons dated June 16, 2025, July 02, 2025 and July 24, 2025 and subsequent reminders, REL failed to furnish party-wise breakups, sales registers, purchase registers, invoices, purchase orders or any other supporting documentary evidence.

30. I note that REL furnished incomplete figures relating to the top customers and vendors on a consolidated basis, as it did not disclose the identities of such counterparties by contending that the same pertained to GGR/Valcambi SA and could not be disclosed due to Swiss laws and confidentiality obligations. In the absence of underlying transactional records and supporting documents, the consolidated sales and purchase figures disclosed by REL could not be independently verified.

31. I further note from the annual reports of REL that more than 97% of REL’s consolidated revenues during FY 2020-21 to FY 2024-25 were attributed to its subsidiaries and step-down subsidiaries.

Table no. 3

Comparison of REL’s consolidated and standalone revenues

(INR in crore)

| Particulars | 2020-21 | 2021-22 | 2022-23 | 2023-24 | 2024-25 | 2025-26 |

| Consolidated Revenue from Operations of REL (A) | 2,58,306 | 2,43,128 | 3,39,690 | 2,80,676 | 4,23,099 | 7,78,716 |

| Standalone Revenue from Operations of REL (B) | 2,060 | 6,237 | 5,762 | 5,401 | 7,027 | 9,189 |

| Revenue from Operations of Subsidiaries/ step- down subsidiaries of REL (C=A-B) | 2,56,245 | 2,36,891 | 3,33,928 | 2,75,276 | 4,16,072 | 7,69,527 |

| % of Revenue from Operations of Subsidiaries/ step- down subsidiaries of REL (C/A) | 99.20% | 97.43% | 98.30% | 98.08% | 98.34% | 98.82% |

32. Thus, it is observed that the consolidated financial position and operational scale projected by REL before investors was substantially dependent upon the revenues allegedly generated by its overseas subsidiaries and step-down subsidiaries.

33. REL, vide email dated April 10, 2025, inter alia furnished the consolidation workings for FY 2020-21 to FY 2023-24. Upon examination of the same, it is observed that REL arrived at the consolidated revenue from operations of REL by undertaking a line-by-line consolidation of the revenues of REL (standalone), REL Singapore and ACC Energy, after giving effect to certain “inter-company adjustments”. REL further stated that the audited financial statements of the step-down subsidiaries were first consolidated at the level of REL Singapore and thereafter forwarded to REL for preparation of the final consolidated financial statements.

34. However, I note that the aforesaid explanation by REL appears inconsistent with the notes to financial statements mentioned in REL Singapore’s Annual Reports itself which inter-alia reads as under:

“These financial statements are the separate financial statements of the Company. The Company is exempted from the preparation of consolidated financial statements as the consolidated financial statements are prepared by the Company’s ultimate holding company, Rajesh Exports Limited where the consolidated financial statements are available for public use.”

35. From the aforesaid it is evident that REL Singapore prepared only standalone financial statements and was exempted from preparing consolidated financial statements on the ground that the ultimate holding company, i.e., REL, prepared consolidated financial statements.

36. I further note that while the standalone financial statements of Valcambi SA were audited under Swiss law by KPMG SA, the consolidated financial statements of GGR were voluntarily prepared under a “Group Accounting Manual” and were not subjected to any statutory audit under Swiss law. It is also observed that KPMG SA specifically clarified that its opinion on GGR’s consolidated financial statements did not constitute a statutory audit opinion under Swiss law.

37. In view of the aforesaid, I note prima facie inconsistencies in the process of consolidation described by REL. While REL stated that audited financial statements of the overseas entities were consolidated at the level of REL Singapore, the material available on record indicates that REL Singapore itself did not prepare consolidated financial statements.

38. REL, vide email dated August 27, 2024, furnished audited standalone financial statements of REL Singapore for FY 2020-21 to FY 2022-23. Upon perusal of the same, it is observed that REL Singapore reported nil revenue from operations during the relevant period. I further note that ACC Energy, which was incorporated on July 04, 2022, also reported nil/negligible revenues during the relevant period.

39. REL, through various communications and through the depositions of its Managing Director (MD) and Chief Financial Officer (CFO), inter alia, stated that REL Singapore, GGR and ACC Energy had no substantive business operations and that Valcambi SA constituted the principal operating entity of the group. It was further stated that Bab Al Rayan Jewellers LLC and Valcambi USA had ceased operations several years earlier and that the consolidated revenues of REL, other than the standalone revenues of REL India, substantially emanated from Valcambi SA.

40. In light of the aforesaid statements, it is prima facie observed that the consolidated revenues disclosed by REL were substantially dependent upon the financials attributed to Valcambi SA. In order to examine the aforesaid claim, the standalone revenues of Valcambi SA (audited) were compared with the consolidated revenues reported by GGR (unaudited) and REL (audited).

Table no. 4

Comparison of consolidated revenue of GGR and standalone revenue of

Valcambi SA with consolidated revenue of REL

| Particulars | 2020 | 2021 | 2022 | 2023 | 2024 | |

| Consolidated Revenue from sale of goods |

CHF in million |

29,162 | 25,779 | 35,372 | 31,828 | Not provided by REL |

| INR/CHF | 79.06 | 80.89 | 82.34 | 91.97 | ||

| and services of GGR (unaudited)(A) |

INR in crore |

2,30,555 | 2,08,519 | 2,91,264 | 2,92,714 | Not provided by REL |

| % of A in C | % | 89.26% | 85.76% | 85.74% | 104.29% | |

| Standalone Revenue from sale of goods and services of Valcambi SA (audited) (B) | CHF in million |

74.13 | 90.10 | 90.25 | 59.01 | 44.87 |

| INR/CHF | 79.06 | 80.89 | 82.34 | 91.97 | 95.08 | |

| INR in crore |

586.11 | 728.82 | 743.14 | 542.68 | 426.63 | |

| % of B in C | % | 0.23% | 0.30% | 0.22% | 0.19% | 0.10% |

| Particulars | 2020-21 | 2021-22 | 2022-23 | 2023-24 | 2024-25 | |

| Consolidated Revenue from Operations of REL (audited) (C) |

2,58,306 | 2,43,128 | 3,39,690 | 2,80,676 | 4,23,099 | |

Note: GGR & Valcambi prepare financial statements on calendar year basis i.e., Jan – Dec. As per Ind AS 21, the translation of revenue from operations is to be done at average exchange rate for that year. Accordingly, the average exchange rates taken from www.exchangerates.org.uk are used for converting INR/CHF.

41. Upon comparison, I note that the standalone revenues of Valcambi SA constituted only a negligible fraction of the consolidated revenues reported by GGR and REL. For instance, during CY 2023, the standalone revenue of Valcambi SA amounted to approximately INR 542.68 crore, whereas GGR reported consolidated revenues of approximately INR 2,92,713.71 crore and REL reported consolidated revenues of approximately INR 2,80,676.35 crore.

42. Thus, it is observed that the standalone revenues of Valcambi SA constituted less than 0.50% of the consolidated revenues reported by GGR and REL, which appears fundamentally inconsistent with REL’s repeated assertion that Valcambi SA was the principal operating entity driving the group’s revenues and the fact that GGR is holding company and is not having any day to day operations.

43. Upon being called upon to explain the aforesaid discrepancy, REL contended that Valcambi SA accounted only for “processing revenues” or “value addition”, whereas GGR recognized the gross value of gold transactions together with processing charges. However, I note that the aforesaid explanation appears prima facie The audited standalone financial statements of Valcambi SA, prepared in accordance with Swiss law and audited by KPMG SA, correctly recognize only the processing charges/value addition as revenue and do not reflect any recognition of the alleged “true and fair sales revenue” now sought to be relied upon by REL. REL has failed to furnish adequate documentary and accounting basis supporting such treatment for example accounting opinions, principal-agent assessments, bullion ownership records, inventory risk allocation, inter-company arrangements or reconciliation statements demonstrating the basis on which gross transaction values aggregating to several lakh crores came to be recognized at the GGR level despite the principal operating entity reflecting only processing charges as standalone revenues. It is not clear as to how the consolidating entity changes fundamental of accounting by including market value of goods belonging to third party as its revenue, when the operating entity itself accounts for only value addition (as it does not claim to take ownership of goods belonging to someone else).

44. I further note that REL’s explanation effectively implies that GGR, despite being merely a holding company with no independent operational activities or trading operations, recognized incorrectly market value of goods as revenues arising from processing transactions undertaken by Valcambi SA, even though such revenues were not recognized in the books of Valcambi SA itself as Valcambi SA was only accounting for value addition. In my view, such accounting treatment is prima facie internally inconsistent, commercially implausible and unsupported by verifiable underlying records.

45. It is pertinent to note that despite repeated summons and opportunities granted by SEBI, REL failed to furnish party-wise sales details, invoices, purchase records, confirmations, customer details or vendor details in respect of the alleged overseas revenues. SEBI also sought information directly from Mr. Michael Mesaric, Chief Executive Officer of Valcambi SA. However, no response was received. Consequently, SEBI was prevented from independently verifying the authenticity and genuineness of the purported consolidated revenues disclosed by REL.

46. From the material available on record, I note the following prima facie findings:

I. the overwhelming majority (approx. 97%-99%) of REL’s consolidated revenues were attributed to overseas subsidiaries and step-down subsidiaries;

II. REL failed to furnish verifiable records supporting such revenues despite repeated summons;

III. REL Singapore and other subsidiaries admittedly had little or no substantive operations;

IV. Valcambi SA, projected as the principal operating entity, disclosed only negligible standalone revenues in its audited financial statements on account of value addition/ processing charges; and

V. the inflated unaudited revenues disclosed by GGR at the consolidated level is not supported either by audited standalone financial statements or by underlying transactional records or concept of accounting.

47. At this prima facie stage, the issue is not merely that certain information remains unavailable, but that the revenues disclosed by REL at the consolidated level appear incapable of independent verification despite repeated regulatory requisitions and opportunities granted over an extended period. The failure of REL to furnish transaction-level records, customer details, vendor confirmations, invoices, inventory trails, or other primary evidentiary material, coupled with the negligible standalone revenues disclosed by only overseas operating entity and the absence of demonstrable substantive operations by others, renders the consolidated revenue figures of REL commercially implausible. This prima facie raises doubt on the genuineness of the disclosures in the financial statements. Viewed cumulatively, the material available on record indicates that the consolidated financial statements of REL appear to have materially overstated and misrepresented the operational scale and financial performance of the group during FY 2020-21 to FY 2024-25. The FY-wise impact of such misrepresentation is tabulated below:

Table no. 5

FY-wise impact of misrepresentation

(INR in crore)

| Particulars | 20-21 | 21-22 | 22-23 | 23-24 | 24-25 | Total |

| Consolidated Revenue of REL (A) | 2,58,306 | 2,43,128 | 3,39,690 | 2,80,676 | 4,23,099 | 15,44,899 |

| Standalone Revenue of REL (B) | 2,060 | 6,237 | 5,762 | 5,401 | 7,027 | 26,486 |

| Revenue of Subsidiaries/ Step-down subsidiaries1 (C=A-B) | 2,56,245 | 2,36,891 | 3,33,928 | 2,75,276 | 4,16,072 | 15,18,413 |

| Particulars | 2020 | 2021 | 2022 | 2023 | 2024 | Total |

| Revenue of Valcambi SA (CHF in million) |

74.13 | 90.10 | 90.25 | 59.01 | 44.87 | 358.36 |

| Avg. INR/CHF rate (www.exchang-erates.org.uk) | 79.06 | 80.89 | 82.34 | 91.97 | 95.08 | – |

| Revenue of Valcambi SA (INR in crore) (D) |

586.11 | 728.82 | 743.14 | 542.68 | 426.63 | 3,027.38 |

| Misrepresentation (E=C-D) | 2,55,659 | 2,36,163 | 3,33,185 | 2,74,733 | 4,15,646 | 15,15,385 |

| % of Misrepresentation (E)/(C)*100 | 99.77 | 99.69 | 99.78 | 99.80 | 99.90 | 99.80 |

48. From the table above, I note that REL has prima facie misrepresented approximately INR 15,15,385 crore i.e. representing 99.80% of its revenues which are attributed to subsidiaries during the period FY 2020-21 to FY 2024-25. The aforesaid conduct appears to have prima facie enabled REL to portray an inflated and misleading picture of its operational scale, consolidated financial position and financial health before investors and the securities market.

49. It is admitted position that GGR (unaudited) was a mere a holding company without having any operations. Yet GGRs’ revenue from operations were significantly higher than the revenue from operations of Valcambi SA (audited). It is further noted that REL has considered the inflated revenue from operations of GGR in its consolidated financial statements, which prima facie appears to be inflated.

50. Further, despite having the audited financial statements of Valcambi SA with it, and knowing the real position of Valcambi SA, REL considered the unaudited consolidated figures recorded by GGR for the purpose of its own consolidation. It is also noted that REL failed to disclose the audited financial statements of Valcambi SA on its website, thereby keeping the investors in dark from knowing the true and fair picture of the financial affairs of the Company.

51. I note that the consolidated revenues and financial disclosures of REL constituted material information for investors and market participants in assessing the valuation, operational strength, growth trajectory, liquidity position and overall financial health of REL. The disclosures relating to overseas subsidiaries and step-down subsidiaries formed the substantial basis of REL’s projected scale of operations and market standing. Consequently, dissemination of financial statements containing prima facie unverifiable, unsupported and materially inconsistent financial information appears to have created a misleading impression regarding the true financial position and operational capabilities of REL, thereby impairing informed price discovery in the scrip of REL in the securities market.

52. The material available on record prima facie indicates that REL employed a scheme or device which appears to have misled investors by portraying an inflated picture of its operational scale and financial position. Accordingly, REL has prima facie violated Regulations 3(b), 3(c), 3(d), 4(1), 4(2)(e), 4(2)(f), 4(2)(k) and 4(2)(r) of the PFUTP Regulations read with Sections 12A(a), 12A(b) and 12A(c) of the SEBI Act, 1992.

53. I further note that by disseminating financial statements and disclosures containing such prima facie unverifiable and improperly consolidated financial information, REL has prima facie failed to ensure accuracy, completeness and transparency in its disclosures to stock exchanges and failed to present a true and fair view of its consolidated financial performance and position before the investors. Accordingly, REL has violated Regulations 4(1)(c), 4(1)(e), 4(1)(g), 4(1)(h), 4(1)(j) and 4(2)(e)(i) of the LODR Regulations.

B.4. Discrepancies in submissions made by REL

54. I note that the sales (revenue from operations) and purchase figures disclosed by REL in its Annual Reports for FY 2020-21 to FY 2024-25 on a standalone basis are as follows:

Table no. 6

Sales and Purchases of REL on standalone basis

(INR in crore)

| Particulars | 2020-21 | 2021-22 | 2022-23 | 2023-24 | 2024-25 | Total |

| Sales | 2,060 | 6,237 | 5,762 | 5,401 | 7,027 | 26,486 |

| Purchases | 1,784 | 6,118 | 5,637 | 5,364 | 6,950 | 25,853 |

55. In order to verify the authenticity and correctness of the sales figures disclosed by REL in its Annual Reports, SEBI issued summons dated June 16, 2025, July 02, 2025 and July 24, 2025 for production of documents, inter alia seeking customer-wise lists of sales and vendor-wise lists of purchases on a standalone basis from REL. In response thereto, REL furnished certain information through a pen-drive received by SEBI on August 06, 2025 (hereinafter referred to as “Submission I”).

56. I further note that prior to furnishing Submission I, REL had made multiple submissions before SEBI containing sales related information in different formats. Vide email dated June 28, 2024, SEBI sought from REL details of sales made by REL on a standalone basis to Aurofin SA, ESG Edelmetall Handel GmbH & Co, Al Jameelat Jewellery LLC and Al Sultan Jewellery LLC for the period April 01, 2020 to March 31, 2024. In response thereto, REL, vide email dated July 10, 2024, furnished a summary of sales pertaining to the aforesaid entities (hereinafter referred to as “Submission II”).

57. Further, vide emails dated June 28, 2024, July 11, 2024, August 06, 2024 and August 21, 2024, SEBI sought from REL the list of top 20 customers of REL on a standalone basis for FY 2021-22, FY 2022-23 and FY 2023-24. In response thereto, REL, vide email dated August 27, 2024, furnished the sought information (hereinafter referred to as “Submission III”).

58. I also note that vide email dated April 10, 2025, REL furnished certain compilations in the nature of sales registers and purchase registers on a standalone basis. However, the narration column in the ledgers furnished by REL was only partially visible and the ledgers did not contain corresponding ledger account names or sufficient particulars enabling independent verification of the nature of the entries recorded therein.

59. Upon comparison of Submission I, Submission II and Submission III, material discrepancies and inconsistencies were observed in the sales figures furnished by REL to SEBI. I note that the sales figures pertaining to the aforesaid overseas entities as reported by REL vide Submission II materially differed from the figures appearing in the customer-wise sales list furnished vide Submission I. It is further observed that certain entities whose names appeared in Submission II did not appear at all in Submission I for the corresponding periods. The discrepancies noted are tabulated below:

Table no. 7

Comparison of Submission I & Submission II

(INR in crore)

| Name of the customer |

Sale as per Submission I |

Sale as per Submission II |

Discrepancy noted |

| ESG Edelmetall Handel GmbH & Co | 652.76 | 749.07 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| AI Jameelat Jewellery LLC | – | (149.14) | Name of the entity not present in the customer wise list |

| Al Sultan Jewellery LLC | – | (5.46) | Name of the entity not present in the customer wise list |

| 2021-22 | |||

| Aurofin SA | 247.07 | 323.83 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| ESG Edelmetall Handel GmbH & Co | – | 3.55 | Name of the entity not present in the customer wise list |

| AI Jameelat Jewellery LLC | – | 44.30 | Name of the entity not present in the customer wise list |

| Al Sultan Jewellery LLC | – | 8.68 | Name of the entity not present in the customer wise list |

| 2022-23 | |||

| Aurofin SA | – | 145.64 | Name of the entity not present in the customer wise list |

| ESG Edelmetall Handel GmbH & Co | – | 21.18 | Name of the entity not present in the customer wise list |

| AI Jameelat Jewellery LLC | – | 274.91 | Name of the entity not present in the customer wise list |

| Al Sultan Jewellery LLC | – | 24.90 | Name of the entity not present in the customer wise list |

| 2023-24 | |||

–

| Name of the customer |

Sale as per Submission I |

Sale as per Submission II |

Discrepancy noted |

| Aurofin SA | – | 3.36 | Name of the entity not present in the customer wise list |

| ESG Edelmetall Handel GmbH & Co | – | 6.28 | Name of the entity not present in the customer wise list |

| AI Jameelat Jewellery LLC | – | 52.28 | Name of the entity not present in the customer wise list |

| Al Sultan

Jewellery LLC |

– | 1.71 | Name of the entity not present in the customer wise list |

60. I further note that the sales figures pertaining to several customers as reported by REL vide Submission III also materially differed from the customer-wise sales figures furnished vide Submission I. In several instances, entities appearing in one submission did not appear in the corresponding submission for the relevant financial year, while in numerous other instances the sales amounts materially varied across submissions. The discrepancies noted are tabulated below:

Table no. 8

Comparison of Submission I & Submission III

(INR in crore)

| Name of thecustomer |

Sale as per Submission I |

Sale as per Submission III |

Discrepancy noted |

| 2021-22 | |||

| Almas Jewellery Co |

935.34 | – | Name of the entity not present in the customer wise list |

| Retail Division Sales |

414.21 | 32.10 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| Amar Jewellers | 104.85 | 1,104.85 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| Jain Jewels | 91.34 | – | Name of the entity not present in the customer wise list |

| N R

Jewellers |

73.21 | – | Name of the entity not present in the customer wise list |

| Al Jameelat Jewellery LLC | 44.30 | – | Name of the entity not present in the customer wise list |

| Shankeshw ar Jewellers | 42.86 | – | Name of the entity not present in the customer wise list |

| Ashta Siddhi Bullion |

33.62 | – | Name of the entity not present in the customer wise list |

| Al Sultan Jewellery LLC |

33.58 | – | Name of the entity not present in the customer wise list |

| M S Bullion | 32.82 | – | Name of the entity not present in the customer wise list |

| D M R | 31.83 | – | Name of the entity not present in the customer wise list |

| Pankaj Jewellers | 29.32 | – | Name of the entity not present in the customer wise list |

| ESG

Edelmetall |

24.73 | – | Name of the entity not present in the customer wise list |

| Namrata Jewellers | 21.42 | – | Name of the entity not present in the customer wise list |

| Bangalore Refinery | 17.91 | 17.91 | No discrepancy |

| Sidhi Art | 17.27 | – | Name of the entity not present in the customer wise list |

| D M Jewells | 12.12 | – | Name of the entity not present in the customer wise list |

| 2022-23 | |||

| Almas Jewellery Co |

1,726.12 | – | Name of the entity not present in the customer wise list |

| Retail Division Sales |

361.23 | 23.21 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| Al Jameelat Jewellery LLC | 274.91 | – | Name of the entity not present in the customer wise list |

| Aurofin SA | 145.64 | – | Name of the entity not present in the customer wise list |

| Amar Jewellers | 100.88 | 100.88 | No discrepancy |

| Augmont Enterprises | 70.33 | 8.91 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| Namrata Jewellers | 57.26 | 57.26 | No discrepancy |

| Ashta Siddhi Bullion |

43.34 | 43.34 | No discrepancy |

| Nakoda Bullion | 36.75 | 36.75 | No discrepancy |

| Choksi Devang Pravinchand ra | 31.12 | – | Name of the entity not present in the customer wise list |

| Al Sultan Jewellery LLC |

24.90 | – | Name of the entity not present in the customer wise list |

| ESG

Edelmetall |

21.18 | – | Name of the entity not present in the customer wise list |

| Shankeshw ar Jewellers | 20.40 | 20.40 | No discrepancy |

| Sidhi Art | 14.80 | 14.80 | No discrepancy |

| SPN Gold & Precious | 13.97 | 13.97 | No discrepancy |

| Swastic Corporation | 6.55 | 6.55 | No discrepancy |

| Riddhi Siddhi Bullion |

3.95 | 3.95 | No discrepancy |

| Hundia Exports | 3.81 | 3.81 | No discrepancy |

| Dilipkumar Manilal Ranpara | 2.62 | 2.62 | No discrepancy |

| 2023-24 | |||

| Almas Jewellery Co |

520.12 | – | Name of the entity not present in the customer wise list |

| Nakoda Bullion & Traders | 356.43 | 387.19 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| JK Sons Precious Metals | 339.35 | 417.36 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| Retail Division Sales |

264.32 | 18.02 | Name of the entity not present in the customer wise list |

| Deep Trading |

221.26 | 271.93 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| Dilipkumar Manilal Ranpara | 172.36 | 210.24 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| Sidhi Art | 142.37 | 148.70 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| Harikala Bullion | 98.90 | 172.11 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| Parekh Brothers | 90.00 | 116.81 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| Swastic Corporation | 83.08 | 83.08 | No discrepancy |

| Jain Jewels | 80.50 | 103.33 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| Ashta Siddhi Bullion |

74.81 | 74.81 | No discrepancy |

| Namrata Jewellers | 69.32 | 72.42 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| M S Bullion | 67.10 | 91.34 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| N R

Jewellers |

63.60 | 94.93 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| Pankaj Jewellers | 63.59 | 72.26 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| Balaji Bullion |

62.09 | 70.26 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| C B

Brothers |

58.74 | 60.00 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| Aarav Bullion |

53.68 | 59.98 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| Al Jameelat Jewellery LLC | 52.28 | – | Name of the entity not present in the customer wise list |

| SPN Gold & Precious | 42.40 | 45.50 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| P R Trading | 38.50 | 38.50 | No discrepancy |

| Gurukrupa Commoditie s | 37.31 | 37.31 | No discrepancy |

| Dishant Ornament | 34.62 | 34.62 | No discrepancy |

| Somnath Trading Company | 32.44 | 48.73 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| Jyotirmay Jewels | 28.85 | 28.85 | No discrepancy |

| Karuna Bullion | 26.56 | 26.56 | No discrepancy |

| Aarav Jewellers | 26.07 | 67.17 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| Nakoda Bullion | 22.35 | 9.08 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| Giriraj Trading |

20.70 | 20.70 | No discrepancy |

| Dhanlaxmi Jewellers | 19.29 | 24.86 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| Vitraag Gold | 18.00 | 18.00 | No discrepancy |

| Kothari Gold | 17.56 | 17.56 | No discrepancy |

| Parth Gold | 16.27 | 19.41 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| Choksi Vachharaj Makanji | 15.24 | 20.25 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| Augmont Enterprises | 13.45 | 14.07 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| Choksi Devang Pravinchand ra | 12.97 | 34.90 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| Suvidhi

Gold Pvt Ltd |

10.57 | 37.36 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| Vrajkamal Ornament | 10.37 | 10.37 | No discrepancy |

| Rupali Gold | 8.80 | 8.80 | No discrepancy |

| Labh

Commoditie s |

7.71 | 8.95 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| H P Jewels | 6.72 | 6.72 | No discrepancy |

| Sreenathji Bullion | 12.94 | 17.89 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| ESG

Edelmetall |

6.28 | – | Name of the entity not present in the customer wise list |

| Radha Mohan |

5.94 | 20.43 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| VP

Jewellers |

5.87 | 5.87 | No discrepancy |

| Hasmukh Bullion | 5.27 | 5.27 | No discrepancy |

| Pooja Jewellers | 4.97 | 8.73 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| Sapna Bullion |

4.28 | 4.28 | No discrepancy |

| D M R | 3.71 | 52.09 | Name of the entity present in the customer wise list. However, mismatch in amount is noted |

| Aurofin SA | 3.36 | – | Name of the entity not present in the customer wise list |

| D M Jewells | 3.08 | 3.08 | No discrepancy |

| Bhansali Bullion | 2.91 | 2.91 | No discrepancy |

| Vitraag Trading | 2.29 | 2.29 | No discrepancy |

| Nakoda Coins |

2.15 | 2.15 | No discrepancy |

| KM Impex | 1.82 | 1.82 | No discrepancy |

| Shyam Enterprise | 1.79 | 1.79 | No discrepancy |

| Trikut Trading |

1.76 | 1.76 | No discrepancy |

| Al Sultan Jewellery LLC |

1.71 | – | Name of the entity not present in the customer wise list |

61. In view of the aforesaid discrepancies, SEBI, vide summons dated March 06, 2026, granted an opportunity to REL to explain the materially varying and inconsistent submissions made before SEBI in relation to its sales figures. In response thereto, REL, vide email dated March 17, 2026, inter alia stated that no sales figures had been furnished vide email dated July 10, 2024 and further requested SEBI to rely only upon the latest data furnished through the pen-drive received on August 06, 2025 while ignoring earlier submissions in case discrepancies were found therein.

62. I note that REL’s contention that no sales figures were furnished vide email dated July 10, 2024 is factually incorrect. A perusal of the annexures accompanying REL’s emails dated July 10, 2024 and March 17, 2026 indicates that sales related data had in fact been furnished by REL therein. Prima facie, the aforesaid response appears to be an attempt by REL to distance itself from its earlier submissions after inconsistencies therein were pointed out during the course of investigation.

63. I further note that REL’s explanation that different submissions were made in response to different queries does not satisfactorily explain the material variations in the underlying sales figures across submissions. Irrespective of whether the information sought pertained to “top customers” or “customer-wise sales”, the underlying sales figures disclosed by the company ought to have remained internally consistent and reconcilable.

64. I note that in the instant matter, information was sought from REL in exercise of powers conferred upon SEBI under section 11(2)(ia) and section 11C(3) of the SEBI Act, 1992. In terms of the said provisions, REL was mandatorily required to provide accurate information/ documents to SEBI. However, as noted above, material inconsistencies and contradictions across the submissions made by REL are found, which raise serious concerns regarding the integrity, reliability and authenticity of the sales data furnished by REL during the course of investigation. REL’s request that earlier submissions be ignored and only the latest submission be relied upon is also not acceptable, as REL was required to furnish accurate data and information in response to emails/summons issued by SEBI. Further, each and every submission furnished by REL before SEBI forms part of the evidentiary record and contradictions therein materially affect the credibility of the disclosures and information furnished by REL.

65. In view of the foregoing, I note that REL failed to furnish a satisfactory explanation for the materially varying and inconsistent submissions made before SEBI in relation to its sales figures. By furnishing contradictory figures at different stages of the investigation, REL impeded SEBI’s ability to independently verify the reported sales figures. The furnishing of inconsistent and misleading information by REL obstructed and hampered the investigative process and demonstrates non-cooperation with the Investigating Authority. Accordingly, I find that REL has, prima facie, violated Section 11(2) (ia) of the SEBI Act, 1992.

66. While the inconsistencies and contradictions noted in the various submissions furnished by REL materially impair the reliability and credibility of the information placed before SEBI, Submission I, being the latest and comparatively most granular dataset furnished by REL during the course of investigation, has been provisionally relied upon for limited analytical purposes and without prejudice to further investigation, verification and reconciliation. Such reliance does not amount to acceptance of the correctness or authenticity of the contents thereof.

B.5. Misrepresentation of Financial Statements – Standalone basis

67. Upon examination of the customer-wise list of sales and vendor-wise list of purchases furnished by REL on a standalone basis for the period FY 2021-22 to FY 2023-24(Submission I), it is observed that REL had recorded sale transactions aggregating to INR 11,487 crore and purchase transactions aggregating to INR 11,488 crore with an entity namely Affluence Shares and Stocks Private Limited (hereinafter referred to as “Affluence”). The aforesaid transactions constituted approximately 66.02% of REL’s standalone sales and 67.11% of REL’s standalone purchases during the said period.

68. The financial year-wise comparison of REL’s standalone sales and purchases vis-à-vis transactions recorded with Affluence is tabulated below:

Table no. 9

Comparison of REL’s standalone sales and purchases vis-à-vis transactions with Affluence

(INR in crore)

| FY | Sales | Sales to Affluence | % of total sales |

Purchases | Purchases from Affluence |

% of total purchases |

| 2021-22 | 6,237 | 4,625 | 74.17% | 6,118 | 4,627 | 75.62% |

| 2022-23 | 5,762 | 4,935 | 85.66% | 5,637 | 4,935 | 87.54% |

| 2023-24 | 5,401 | 1,926 | 35.67% | 5,364 | 1,927 | 35.92% |

| Total | 17,399 | 11,487 | 66.02% | 17,119 | 11,488 | 67.11% |

69. I note that despite the substantial quantum of transactions allegedly undertaken with Affluence, the sales and purchases recorded by REL with Affluence reflected negligible differences over multiple financial years, resulting in near-zero or negative value addition. The same is tabulated below:

Table no. 10

Comparison of sales and purchases recorded with Affluence

(INR in crore)

| FY | Sales to Affluence | Purchases from Affluence | Difference |

| 2021-22 | 4,625.32 | 4,626.67 | (1.35) |

| 2022-23 | 4,934.98 | 4,935.24 | (0.26) |

| 2023-24 | 1,926.29 | 1,926.51 | (0.22) |

| Total | 11,486.60 | 11,488.42 | (1.82) |

70. In order to verify the genuineness of the aforesaid transactions, the customer-wise sales and vendor-wise purchase data furnished by REL were examined along with GST records, bank statements, ledger extracts and supporting documents furnished by REL and Affluence.

71. I note that review of the GSTR-2A records of REL for the period FY 2020-21 to FY 2023-24 did not reveal any purchase transaction between REL and Affluence. Further, the Forensic Auditor selected sample purchase and sale transactions allegedly undertaken by REL with Affluence and sought supporting documentation in respect thereof. However, REL failed to furnish supporting documents for the aforesaid sample transactions. I further note that pursuant to summons dated June 16, 2025, July 02, 2025 and July 24, 2025, REL furnished the ledger of Affluence through a pen-drive submitted to SEBI on August 06, 2025. However, the narration column in the ledger was only partially visible and the ledger did not contain corresponding ledger account names or sufficient particulars enabling independent verification of the nature of the recorded entries.

72. Upon examination of the Ledger of Affluence in the books of REL for FY 2021-22 to FY 2023-24, it is observed that the ledger reflected 102 sale entries aggregating to INR 11,330 crore and 102 purchase entries aggregating to INR 11,332 crore. A comparison of these entries with the customer-wise list of sales and vendor-wise list of purchases furnished by REL revealed discrepancies in FY 2021-22, wherein the sales and purchases disclosed by REL exceeded the amounts recorded in the ledger by approximately INR 157 crore and INR 157 crore respectively.

73. I note that other than the aforesaid sale and purchase entries, the Ledger of Affluence contained nine additional entries. Upon comparison with the bank statements of REL, seven entries were traced to transactions between REL and Mr. Rajesh Mehta and not between REL and Affluence. No direct banking transaction between REL and Affluence was observed in the bank statements of REL during FY 2020-21 to FY 2023-24. It is further observed that REL transferred an aggregate amount of INR 7.45 crore to Mr. Rajesh Mehta through multiple tranches, and Mr. Rajesh Mehta transferred back an aggregate amount of INR 3.57 crore to REL. The relevant entries were reflected in the bank statements of REL.

74. The examination of financial statements of Affluence – a SEBI registered stock broker – from FY 2021-22 to FY 2023-24 revealed an aggregate Revenue from Operations of INR 113.22 crore and aggregate Purchases of Stock-in-Trade of INR 84.64 crore during the said period. I note that as per Form MGT-7 filings of Affluence, the source of revenue of Affluence was disclosed as financial advisory, brokerage and consultancy services. The disclosed scale and nature of operations of Affluence prima facie appear to be inconsistent with REL’s claim of having undertaken sale and purchase transactions aggregating to more than INR 11,400 crore each with Affluence during FY 2021-22 to FY 2023-24.

75. In response to SEBI summons dated September 19, 2025 and September 30, 2025, Affluence, vide emails dated September 23, 2025 and October 01, 2025, inter alia stated that:

I. REL was never a client of Affluence;

II. No agreement or contract was entered into with REL; and

III. No sale or purchase transactions were executed with or on behalf of REL.

76. I further note that officials of Affluence, including Mr. Dhiren Shah, promoter of Affluence, in their depositions recorded before SEBI on October 03, 2025, stated that Affluence had trading relations only with Mr. Rajesh Mehta in his personal capacity and had not undertaken any transactions with REL. Affluence subsequently furnished KYC documents, contract notes and ledger statements pertaining to Mr. Rajesh Mehta. On examination of the contract notes and ledger of Mr. Rajesh Mehta in the books of Affluence, it is observed that Mr. Rajesh Mehta traded in gold derivatives through Affluence on 102 trading days during FY 2021-22 to FY 2023-24. The records indicate that Mr. Rajesh Mehta made aggregate net payments of INR 7.45 crore to Affluence and incurred aggregate net losses amounting to INR 3.50 crore in the said transactions.

77. I note that comparison of:

I. customer-wise sales and vendor-wise purchase data furnished by REL,

II. the Ledger of Affluence in the books of REL,

III. REL’s bank statements,

IV. Rajesh Mehta’s bank statements, and

V. contract notes and ledger of Mr. Rajesh Mehta in the books of Affluence, prima facie indicates that the sale and purchase transactions recorded by REL with Affluence substantially corresponded with the transactions executed by Mr. Rajesh Mehta in gold derivatives through his personal trading account with Affluence.

78. It is further observed that:

I. INR 7,45,00,000 was transferred by REL to Mr. Rajesh Mehta,

II. Rajesh Mehta utilised the said funds for trading in gold derivatives through his personal account with Affluence,

III. Affluence refunded the net balance of INR 3,94,35,510 to Mr. Rajesh Mehta after accounting for trading loss of INR 3,50,64,490, and

IV. Mr. Rajesh Mehta transferred INR 3,91,07,478 thereof back to REL.

79. I note that out of the nine entries in the Ledger of Affluence in the books of REL, other than sale and purchase entries, seven entries were found reflected in the ledger of Mr. Rajesh Mehta maintained by Affluence. However, two credit entries amounting to INR 1.18 crore and INR 45.16 lakh respectively were neither reflected in the bank statements of REL nor in the ledger of Mr. Rajesh Mehta maintained by Affluence. Prima facie, the aforesaid entries appear to have been recorded to reconcile or tally the Ledger of Affluence in the books of REL.

80. During the course of investigation, explanations were sought from REL and its KMPs regarding the accounting treatment adopted by REL in recording the aforesaid transactions. Mr. Suresh Gowda, Managing Director of REL, and Mr. Vijendra Rao, CFO of REL, in their depositions recorded before SEBI, inter alia stated that there was nothing improper in such accounting treatment.

81. Subsequently, in reference to the aforesaid transactions, vide email dated March 17, 2026, REL stated that:

I. REL intended to conduct digital sale and purchase of gold through MCX;

II. due to litigation with MCX, trades were routed through the personal account of Mr. Rajesh Mehta;

III. the margin money was provided by REL through Mr. Rajesh Mehta;

IV. Mr. Rajesh Mehta acted merely as a conduit; and

V. the transactions were conducted for and on behalf of REL and therefore recorded in REL’s books of accounts.

82. I note that REL’s explanation that trades executed through the personal account of Mr. Rajesh Mehta constituted transactions of REL is unsupported by contemporaneous documentary evidence. The trades were admittedly undertaken through the personal trading account of Mr. Rajesh Mehta, the contractual relationship existed between Mr. Rajesh Mehta and Affluence, and the transactions were settled through his personal account. Further, REL failed to furnish any agreement, authorization, board approval, audit committee approval or contemporaneous record demonstrating that Mr. Rajesh Mehta acted as an authorized conduit or nominee for REL in respect of the impugned trades.

83. Prima facie, recording trades executed through the personal account of Mr. Rajesh Mehta as REL’s own sale and purchase transactions resulted in inflation of REL’s standalone sales and purchase figures during FY 2021-22 to FY 2023-24. The near matching of sales and purchases, absence of meaningful commercial value addition, absence of direct banking transactions between REL and Affluence, denial by Affluence regarding existence of transactions with REL, and absence of supporting documentation collectively raise serious concerns regarding the genuineness and economic substance of the transactions recorded by REL with Affluence.

84. I further note that the aforesaid transactions involving routing of company funds through the personal account of Mr. Rajesh Mehta for derivative trading activity were neither disclosed as related party transactions nor placed before the Board of Directors or Audit Committee of REL for approval. Prima facie, such utilisation of company funds without requisite approvals and disclosures appears prejudicial to the interests of the company and its public shareholders.

85. In view of the foregoing, I prima facie find that REL misrepresented its standalone financial statements for FY 2021-22 to FY 2023-24 by recording non-genuine sales and purchase transactions aggregating to INR 11,486.60 crore and INR 11,488.42 crore respectively in the name of Affluence. The financial impact of the aforesaid transactions on the standalone financial statements of REL is tabulated below:

Table no. 11

Impact of Misrepresentation – Affluence

(INR in crore)

| Particulars | 2021-22 | 2022-23 | 2023-24 | Total |

| Revenue disclosed by REL in its Annual Reports (A) | 6,237 | 5,762 | 5,401 | 17,399 |

| Fictitious revenue – Affluence (B) | 4,625 | 4,935 | 1,926 | 11,487 |

| % of Fictitious Revenue identified (B/A*100) | 74.17% | 85.66% | 35.67% | 66.02% |

| Purchases disclosed by REL in its Annual Reports (C) | 6,118 | 5,637 | 5,364 | 17,119 |

| Fictitious purchases – Affluence (D) |

4,627 | 4,935 | 1,927 | 11,488 |

| % of Fictitious purchases identified (D/C*100) | 75.62% | 87.54% | 35.92% | 67.11% |

86. By disseminating annual reports and financial statements containing the aforesaid transactions to stock exchanges and investors, REL prima facie communicated false and misleading information regarding its operational scale, revenue and financial performance. Accordingly, REL has prima facie violated Regulations 3(b), 3(c), 3(d), 4(1), 4(2)(e), 4(2)(f), 4(2)(k) and 4(2)(r) of the PFUTP Regulations, read with Sections 12A(a), 12A(b) and 12A(c) of the SEBI Act, 1992.

87. Further, by publishing financial statements containing the aforesaid transactions and failing to ensure accurate, complete and transparent disclosures to stock exchanges and investors, REL has prima facie violated Regulations 4(1)(a), 4(1)(b), 4(1)(c), 4(1)(e), 4(1)(g), 4(1)(h), 4(1)(j), 4(2)(e)(i), 33(1)(a), 33(1)(c) and 48 of the LODR Regulations.

Foreign Exchange Fluctuations and Interest on Fixed Deposits/Mutual Funds

88. Upon examination of the customer-wise list of sales furnished by REL on a standalone basis, along with the “Sales 2” sub-ledger furnished by REL vide email dated April 10, 2025, it is observed that during FY 2020-21 to FY 202324, REL recorded:

I. foreign exchange fluctuations arising from revaluation of foreign currency debtors aggregating to INR 866.60 crore as part of Revenue from Operations; and

II. interest income on Fixed Deposits/Mutual Funds aggregating to INR 204.00 crore as part of Revenue from Operations.

89. The financial year-wise comparison of REL’s standalone sales vis-à-vis the aforesaid foreign exchange fluctuations and interest income is tabulated below:

Table no. 12

Comparison of REL’s standalone sales vis-à-vis foreign exchange fluctuations and Interest

(INR in crore)

| FY | Sales | Exchange Fluctuation |

% of Exchange fluctuation on sales |

Interest | % of Interest on sales |

| 2020-21 | 2,060 | 149 | 7.22% | 159 | 7.73% |

| 2021-22 | 6,237 | 188 | 3.01% | 22 | 0.35% |

| 2022-23 | 5,762 | 467 | 8.10% | 23 | 0.40% |

| 2023-24 | 5,401 | 64 | 1.18% | – | 0.00% |

| Total | 19,459 | 867 | 4.45% | 204 | 1.05% |

90. I note that examination of the vendor-wise list of purchases furnished by REL on a standalone basis, along with the “Purchase 2” sub-ledger furnished vide email dated April 10, 2025, revealed that REL had recorded foreign exchange fluctuations arising from revaluation of foreign currency creditors aggregating to INR 716.18 crore as part of Purchases / Cost of Materials Consumed during FY 2020-21 to FY 2023-24.

91. The financial year-wise comparison of REL’s standalone purchases vis-à-vis the aforesaid foreign exchange fluctuations is tabulated below:

Table no. 13

Comparison of REL’s standalone purchases vis-à-vis foreign exchange fluctuations

(INR in crore)

| FY | Purchases | Exchange Fluctuation | % of Exchange fluctuation on purchases |

| 2020-21 | 1,784 | 207 | 11.63% |

| 2021-22 | 6,118 | 114 | 1.86% |

| 2022-23 | 5,637 | 353 | 6.27% |

| 2023-24 | 5,364 | 42 | 0.78% |

| Total | 18,903 | 716 | 3.79% |

92. Upon being called upon to explain the aforesaid accounting treatment, REL, vide email dated April 10, 2025, inter alia stated that:

I. exchange differences arising upon settlement or year-end revaluation of foreign currency receivables/payables were adjusted through “Sales 2” and “Purchase 2” ledgers; and

II. such treatment reflected the actual realization/payment value of export and import transactions.

93. I note that Paragraph 28 of Ind AS 21 (“The Effects of Changes in Foreign Exchange Rates”) provides that exchange differences arising on settlement or translation of monetary items are required to be recognized in profit or loss in the period in which they arise. Prima facie, foreign currency trade receivables and payables constitute monetary items within the meaning of Ind AS 21 and the exchange differences arising therefrom are required to be recognized separately as foreign exchange gain/loss in the Statement of Profit and Loss. However, REL recorded such exchange differences as part of Revenue from Operations and Cost of Materials Consumed by routing the same through sales and purchase ledgers.

94. I further note that review of the audited standalone financial statements of REL for FY 2020-21 to FY 2023-24 did not reveal any specific disclosure explaining the inclusion of foreign exchange fluctuations within Revenue from Operations or Cost of Materials Consumed. Prima facie, the absence of transparent disclosure regarding such material accounting treatment appears to have resulted in a misleading presentation of REL’s operational performance.

95. I also note that REL disclosed in the notes to accounts that Revenue from Operations included interest income earned on Fixed Deposits and Mutual Funds allegedly maintained for margin purposes relating to buyers’ credit facilities. However, the accounting policies disclosed in the Annual Reports of REL for FY 2020-21 to FY 2022-23 stated that interest income was recognized under “Other Income” in the Statement of Profit and Loss. Paragraph 65 of Ind AS 115 (“Revenue from Contracts with Customers”) provides that effects of financing, including interest revenue or interest expense, are required to be presented separately from revenue arising from contracts with customers. Prima facie, interest income earned on Fixed Deposits and Mutual Funds does not arise from contracts with customers and does not represent consideration for transfer of goods or services. Accordingly, inclusion of such interest income within Revenue from Operations appears inconsistent with the recognition and presentation requirements under Ind AS 115.

96. In view of the aforesaid accounting treatment, it prima facie appears that REL inflated its Revenue from Operations and Cost of Materials Consumed by including: