“What is Interest?” I asked my students before commencing the discussion on Article 11 of the Model Tax Convention. One of my students got up and said, “Interest is a feeling or emotion that we all have towards your teaching.” Followed by a burst of celebration.

Overwhelmed, while absorbing a new angle for the meaning of “Interest”, I felt proud that my students are as creative as their teacher.

So, what is Interest? In simple words, Interest is a sum paid for the use of money.

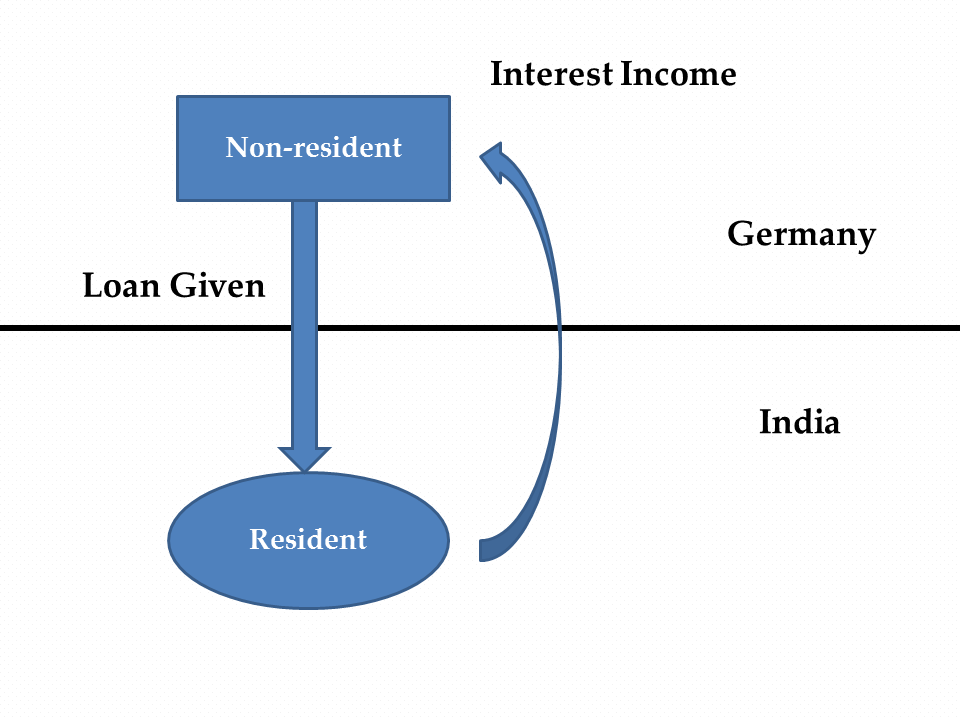

Let us understand the concept of Interest in the context of cross-border taxation with the help of an example. When an Indian Company borrows money by way of Loan from a person resident of Germany, the Indian Company will pay Interest at agreed rate to such Non-resident. Now, the question arises, which country gets the right to tax such Interest Income of the Non-resident?

Fig. 1

Will the Interest be taxable in India, being a Source State? Or will it be taxable in Germany, being a Residence State? Or will it be taxable in both the countries?

Paragraph 1 of Article 11 of the OECD MC states that, “Interest arising in a contracting state and paid to a resident of the other contracting state may be taxed in that other state.”

Let us simplify this and replace “contracting state” with respective countries.

“Interest arising in India and paid to a resident of Germany may be taxed in Germany.”

Hence, Paragraph 1 gives Residence State the right to tax such Interest. Even without this paragraph, Germany could tax such Interest. It is to be noted that this Article does not apply to Interest arising in a third state or to Interest arising in a contracting state which is attributable to a permanent establishment which an enterprise of that state has in the other contracting state.

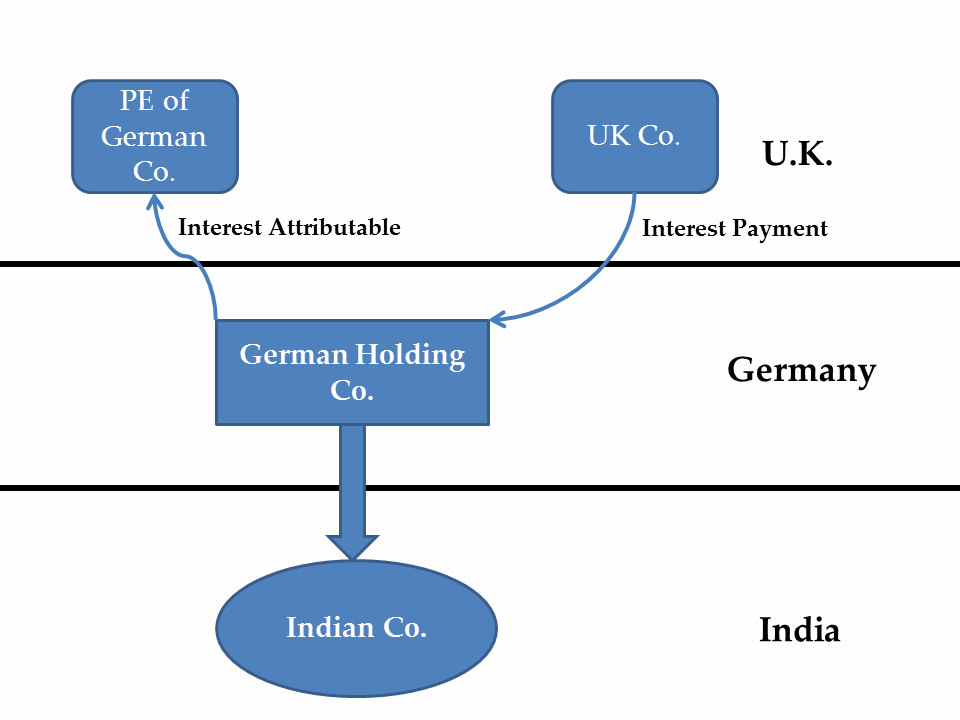

Fig. 2

In the above figure, there is an Indian company. It has holding company in Germany. There is a third company in U.K., which pays Interest to German holding company. Obviously, this Interest will not be taxable in India since it arises in U.K. (third state).

Similarly, if German holding company has P.E. in U.K. and Interest is attributable to such P.E., it will definitely not be taxable in India as it does not arise in India.

The term used in paragraph 1 is “paid”. This term should not be restricted to actual physical payment as it might include performance in kind or set off amounts.

Further, the said right given to Germany is not exclusive as the words “may be” taxed are used. As per paragraph 2 of Article 11, right to tax such Interest is given to Source State as well.

Paragraph 2 of Article 11 of the OECD MC states that, “However, Interest arising in a contracting state may also be taxed in that state according to the laws of that state, but if the beneficial owner of the Interest is a resident of the other contracting state, the tax so charged shall not exceed prescribed percent of the gross amount of the interest. The competent authorities of the contracting states shall by mutual agreement settle the mode of application of this limitation.”

Thus, it is clear that Interest is taxed in both the states, India (Source) and Germany (Residence) [Refer Fig. 1]. The source country is provided a limited right to tax Interest as per its domestic laws at concessional rate. The benefit of concessional tax rate is given subject to fulfillment of certain conditions. Accordingly, the recipient of Interest should be:

a) A beneficial owner of Interest; and

b) A resident of other country.

It may be pertinent to note that India taxes Interest payments made to non-residents at source, by way of withholding tax payments.

Now, the question arises, if both source as well as residence country tax the Interest, how the double taxation is avoided? The answer is by giving double taxation relief under Article 23.

It is important to understand what “Interest” means as per paragraph 3 of Article 11. This is because, if a certain payment cannot be characterized as “Interest”, the above discussion on paragraphs 1 and 2 is meaningless.

Definition of “Interest” as per paragraph 3 is exhaustive and covers all kinds of Income which may be regarded as Interest in domestic laws of various countries. However, for meaning of the term “Interest”, domestic law is never to be referred.

Many a times, difficulty arises whether a particular payment is characterized as “Interest” or “Dividend”. With respect to this, it is interesting to have a look at the commentary of Klaus Vogel on Double Taxation Convention. It reads as interest is no more than the remuneration received for making capital available subject to repayment, and does not include profits from providing funds in cases where the provider accepts the hazards of the borrower’s business. This distinguishes interest from business profits within the meaning of Article 7 – to the extent that such profits, too, are made by providing capital – and from dividends within the meaning of Article 10. On the other hand the creditor’s general hazard i.e. the risk of not being able to enforce this debt-claim on account of the borrowers insolvency or of the debt being irrecoverable, do not by themselves involve the lender in the hazards of the borrowers business.

Paragraph 4 of Article 11 deals with P.E. situations. This article states that paragraph 1 and 2 of this article will not apply if the beneficial owner of the Interest i.e. the lender has a P.E. in the Interest Source state which carries on business and debt claim is effectively connected with that source state P.E. In such case Article 7 – Business Profits or Article 14 – Independent Personal Services will apply.

For E.g. Citibank, USA has a branch in India. A Ltd, an Indian Co. has taken a loan from Citibank, India branch and is paying interest to it. This interest shall be taxable as business profits in the hands of Citibank, USA in India as it is effectively connected with the P.E. in India.

Paragraph 5 of Article 11 provides for Extraterritorial taxation of Interest. It states that, “Interest shall be deemed to arise in a contracting state when the payer is a resident of that state. Where, however, the person paying the interest, whether he is a resident of a contracting state or not, has in a contracting state a permanent establishment in connection with which the indebtedness on which the Interest is paid was incurred, and such interest is borne by such permanent establishment, then such interest shall be deemed to arise in the state in which the permanent establishment is situated.”

Let us understand this with the help of an example. There is a UK Co. which has taken loan from a US Co. The UK Co. has a branch (which constitutes PE) in India. The loan taken from US Co. is for the branch in India. Interest is paid by the UK Co. to the US Co. which is ultimately borne by the branch in India. Therefore, in such a case, the interest arises in the state in which the PE is located i.e. India.

It can be observed that:

- If the PE borrows – Interest clearly arises in Source Country and is taxable.

- If HO borrows specifically for the PE, funds are used for business of PE and Interest is borne by the PE. It is taxable in Source Country.

- If HO borrows generally for all its worldwide PEs and subsidiaries. Some indirect interest cost is attributable to the PE. It does not arise in Source Country. Article 11 cannot apply.

Paragraph 6 of Article 11 provides for Arm’s Length Condition. The rule given in paragraph 6 will operate where a special relationship prevails between the payer of interest and beneficial owner of the interest and the amount of the interest paid exceeds the amount which would have been agreed upon by the payer and the beneficial owner had they stipulated at arm’s length. Therefore, benefit of article 11 for lower tax rates applies only to the arm’s length interest. Here, Special relationship means i) participation in management, control or capital (direct or indirect) and ii) relatives (relationship by blood or marriage).

For E.g. A subsidiary company in India pays interest @ 15% to the holding company in USA but interest @ 10% to another unrelated company in USA, the excess of 5% would be required to be scrutinized. The exact nature of excess amount has to be determined in order to categorize such income as dividend or other income under the domestic laws. Possibly Article 7, 10 or 21 of the relevant tax treaty may apply.

Now, as to when the Interest “arises” in India, let us compare the Income Tax Act, 1961 (“Act”) and the Article 11 of the Treaty.

| Payer | Act | Treaty |

| Government | Always | Always |

| Indian Resident | Always except when used for a business or profession carried on outside India or for any source of income outside India. | Always |

| Non-Resident | Only when used for the purposes of business or profession carried on in India. | Only if Non-Resident has a P.E. / Fixed Base in India and interest is born by such P.E. / F.B. |

Provisions of the Act would prevail or the Treaty? As laid down in Section 90(2) of the Act, provisions of Act or Treaty whichever are beneficial to the assessee shall apply. Hence, one needs to analyze when the Interest arises in India as per Section 9(1)(v) and as per Article 11 of the Treaty. The one which is more beneficial to the assessee shall prevail.

As apparent from the discussion in this article, income characterization is an important and intricate tax treaty interpretation issue – because that affects application (or non-application) of specific articles of a relevant tax treaty. Needless to say, one should never lose focus of the domestic Act while analyzing the cross-border transaction.

About Author:

Mr. Arun Valera is a First Generation Entrepreneur and a member of the Institute of Chartered Accountants of India with merit ranking in his CA foundation exam. He is also a Law Graduate.

He is passionate to share the knowledge and experience related to International and Domestic Taxation. He teaches CA aspirants at various institutions. He has authored various articles on topics close to his heart. He holds a certificate in creative writing workshop conducted by Xavier Institute of Communications. Currently he is pursuing Diploma in International Taxation from the Institute of Chartered Accountants of India (ICAI).

Author Bio