Case Law Details

DCIT Vs S.S. Natural Resources Pvt. Ltd. (ITAT Kolkata)

The Income Tax Appellate Tribunal (ITAT), Kolkata, dismissed the Revenue’s appeal and upheld the order of the Commissioner of Income-tax (Appeals) deleting the penalty of ₹5,17,80,820 levied under Section 270A of the Income-tax Act for Assessment Year 2022-23.

At the outset, the Tribunal condoned a delay of 163 days in filing the Revenue’s appeal after considering the explanation that the delay resulted from obtaining administrative approval from the competent authorities. The assessee did not oppose the condonation, and the appeal was admitted for hearing.

The assessee, a private limited company engaged in exploration and mining of coal and related minerals, had participated in the insolvency resolution process for acquiring M/s Ramsarup Industries Limited. The resolution plan was approved by the National Company Law Tribunal on 4 September 2019, but litigation by the erstwhile promoters delayed the acquisition until the matter was decided in the assessee’s favour by the Supreme Court. During this period, the assessee borrowed funds from group concerns to meet obligations under the resolution plan and claimed interest expenditure of ₹7,75,53,350 as business expenditure in its return for AY 2022-23, which declared a business loss of ₹7,74,32,299. During scrutiny assessment, the Assessing Officer disallowed the interest expenditure, assessed the income at ₹1,21,053, initiated penalty proceedings under Section 270A(9), and ultimately levied a penalty at 200% of the tax payable on the disallowance after concluding that the assessee had misrepresented or suppressed facts.

The Commissioner (Appeals) quashed the penalty. The appellate authority noted that the assessee had claimed deduction of interest paid on capital borrowed for acquiring the company, while the Assessing Officer had disallowed the claim by referring to Section 36(1)(iii). The Commissioner (Appeals) recorded the assessee’s submission that Section 270A uses the expression “may” and that the claim arose from a technical and bona fide mistake without reliance on false evidence, as the relevant transactions formed part of its books of account. The assessee also contended that non-filing of an appeal against the quantum assessment did not automatically attract penalty proceedings and further argued that the Assessing Officer had failed to specify the particular clause of Section 270A(9) applicable to the alleged misreporting either in the assessment order, show cause notice, or penalty order. The Commissioner (Appeals) accepted these submissions and quashed the penalty.

Before the Tribunal, the Revenue argued that the assessee had accepted the quantum disallowance and had wrongly claimed an inadmissible deduction for interest expenditure, amounting to misreporting of income under Section 270A. It was submitted that the assessment order and penalty notice sufficiently indicated that the penalty was proposed for under-reporting resulting from misreporting, and therefore the Commissioner (Appeals) had erred in deleting the penalty.

The assessee supported the order of the Commissioner (Appeals), contending that all facts regarding the borrowings, finance costs, and utilisation of funds were fully disclosed in the financial statements. It submitted that the interest claim represented a considered legal position based on judicial precedents relating to borrowings for strategic acquisitions. According to the assessee, the issue involved a debatable legal claim rather than any misrepresentation or suppression of facts. The assessee also explained that it had not challenged the quantum addition because the assessed income was only ₹1,21,503 and the disallowed business loss had not been set off in future years, making further litigation unnecessary. It maintained that penalty proceedings were independent of assessment proceedings and that a bona fide, debatable claim could not constitute misreporting of income.

The Tribunal held that initiation of penalty proceedings must strictly comply with Section 274 and that a valid show cause notice must clearly specify the exact default or charge forming the basis of the proposed penalty. After examining the notice dated 24 January 2024, the Tribunal found it fundamentally defective because it failed to identify the specific clause of Section 270A(9) alleged to have been violated. Since Section 270A(9) contains distinct instances of misreporting, the Assessing Officer was required to clearly specify the particular default attributed to the assessee and explain how its ingredients were satisfied. The Tribunal agreed with the Commissioner (Appeals) that failure to do so rendered the notice vague and legally defective. Relying on the decisions referred to in the order, including the Chennai Bench decisions in Prakashchand Jain v. Dy. CIT and Enrica Enterprises (P.) Ltd. v. Dy. CIT, the Tribunal held that such a vague notice could not sustain the levy of penalty.

The Tribunal further observed that, even on merits, the assessee had claimed deduction of interest on loans used for acquiring a strategic investment through the corporate insolvency resolution process. The details relating to the borrowings, finance costs, and deployment of funds were reflected in the audited financial statements. It noted that judicial precedents cited by the assessee indicated that interest on borrowings used for investments in the same line of business had been regarded as allowable under Section 36(1)(iii) in certain cases. The Tribunal found that the issue was debatable, involving interpretation of Section 36(1)(iii), and that the assessee had disclosed the primary facts while making a bona fide legal claim. Accordingly, it concluded that the assessee could not be regarded as guilty of misrepresentation or suppression of facts and that the ingredients of Section 270A(9)(a) were absent.

For these reasons, the Tribunal held that the Assessing Officer was not justified in levying penalty under Section 270A, upheld the order of the Commissioner (Appeals) deleting the penalty, and dismissed the Revenue’s appeal.

Cases Discussed:

- Prakashchand Jain v. Dy. CIT, ITA No.68/Chny/2024 dated 07.03.2025.

- DCIT v. Chakradhar Contractors and Engineers (P.) Ltd. [2025] 171 com 133 (Pune Trib.).

- Manish Manohardas Asrani v. INT Tax [2025] 170 com 792 (Mumbai – Trib.).

- GE Capital US Holdings Inc. [2024] 163 taxmann.com 146 (Del).

- Enrica Enterprises (P.) Ltd. v. Dy. CIT [2024] 163 com 105 (Chennai-Trib.).

- Chambal Fertilizers and Chemicals Ltd. v. Office of the Principal Commissioner of Income-tax [2024] 158 taxmann.com 184 (Rajasthan).

- ING Saltwater Studio LLP vs. MENT s. NFAC, Delhi [2023] 157 com 749 (Mumbai – Trib.) [22-05-2023].

- Kishor Digambar Patil vs. Income-tax Officer [2023] 149 com 502 (Pune – Trib.) [30-03-2023].

- Schneider Electric South East Asia (HQ) PTE Ltd. v. ACIT [2022] 443 ITR 186 (Delhi).

- CIT v. Manjunatha Cotton & Ginning Factory (2013 35 com 250).

- Reliance Petro Products (P) Ltd. (322 ITR 158) (SC).

- Dharmendra Textile Processors (306 ITR 277) (SC).

- Dilip N. Shroff Vs. CIT (291 ITR 519) (SC).

FULL TEXT OF THE ORDER OF ITAT KOLKATA

This is an appeal preferred by the Revenue against the order of the Commissioner of Income-tax (Appeals), Kolkata-20 (hereinafter referred to as the “Ld. CIT(A)”] dated 02.05.2025 for the AY 2022-23.

2. At the outset, we observe from the appeal folder that there is a delay of 163 days in filing the appeal by the department and in support of this a condonation petition was filed. It was stated in the condonation petition that the delay has occurred due to obtaining the administrative approval from the competent authorities, which took quite a long time and accordingly, the delay may be condoned. The ld. AR, on the other hand, did not oppose the condonation of delay. Considering the reasons cited before us, we are inclined to condone the delay and admit the appeal for hearing.

3. The only issue raised by the assessee in this appeal relates to the levy of penalty of ₹5,17,80,820/- u/s 270A of the Act on account of under-reporting as a consequence of misreporting.

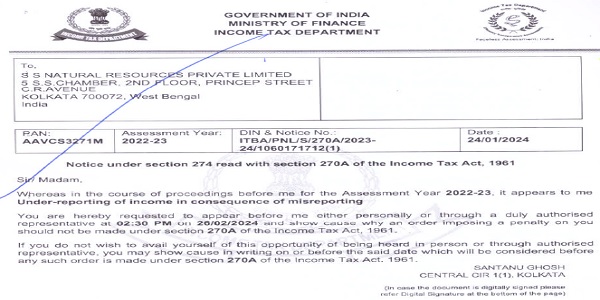

4. Brief facts of the case are that, the assessee is a private limited company formed with the purpose of conducting business activity of exploration and mining of coal and related minerals. The assessee is related to the Shyam Sel Group and was nominated to participate in the IBC process for acquiring M/s Ramsarup Industries Limited, a company engaged in the business of iron and steel. The resolution plan submitted by the assessee was accepted by the Hon’ble NCLT on 04.09.2019, however due to litigation filed by erstwhile promoters, the acquisition got stalled and the matters travelled to Hon’ble Supreme Court who decided in favour of the assessee. In the meantime, the assessee had availed loan from the group concerns for making payment(s) of security deposit with Banks, and obligations payable to the various stakeholders of M/s Ramsarup Industries Limited, as agreed in the resolution plan. The assessee had accordingly incurred interest expenditure of Rs.7,75,53,350/-during AY 2022-23 on the loans utilized for the strategic acquisition of M/s Ramsarup Industries Limited, which was debited to P&L A/c and claimed by way of business expenditure in the return of income for AY 2022-23. The assessee had filed its return of income on 06.11.2022 for A.Y. 2022-23 declaring business loss of Rs.(-) 7,74,32,299/-. The case of the assessee was selected for regular scrutiny and in the course of assessment proceedings, the ld. AO called upon the assessee to explain as to why interest cost of Rs.7,75,53,350/- debited in the P&L A/c should not be disallowed. The assessee has furnished the details of finance cost incurred during the year and claimed that the interest was paid towards expansion of business. The AO however was not agreeable to the explanation offered by the assessee and therefore disallowed the same and assessed the total income at Rs.1,21,053/-. The AO is noted to have initiated penalty proceedings u/s 270A(9) of the Act in relation to the aforesaid disallowance, for which notice u/s 274 of the Act was issued on 24.01.2024. Not being satisfied with the submissions of the assessee, the AO held that the assessee had misrepresented or suppressed the facts and therefore levied penalty at 200% of the tax payable on the addition of Rs.7,75,53,350/-.

5. In the appellate proceedings, the ld. CIT(A) has quashed the penalty levied by the AO after taking into account the submissions and arguments of the assessee, by observing as under:

“4. Decision:

Ground No.-1 & 2-

4.1 I have carefully considered the facts of the case and submission of the appellant. Assessee had filed original return of income for the assessment year 2022-23 u/s. 139(1) of the I.T. Act on 06.11.2022 declaring current year’s loss of Rs. 7,74,32,299/-. The return was processed u/s 143(1) of the IT Act, 1961 on 06.11.2022, accepting the returned loss. The case was selected under CASS for scrutiny assessment for AY 2022-23. It was observed that the appellant had debited finance cost to the tune of Rs. 7,75,53,350/-in its P/L account, though revenue from operation as well as profit and gains from business and profession is shown as NIL. The AO disallowed the amount of Rs. 7,75,53,350/- u/s 37 of the Income Tax Act, 1961. The appellant availed deduction of the amount of interest paid in respect of capital borrowed for the purpose of acquiring a company and claimed the same while computing income from business and profession in its computation of total income. However, quoting the provisions of section 36(1) (ii) of the IT Act, 1961, the AO made the addition of Rs. 7,75,53,350/. The provision of section 36(1)(iii) states as under:

“the amount of the interest paid in respect of capital borrowed for the purposes of the business or profession

Provided that any amount of the interest paid, in respect of capital borrowed for acquisition of an asset (whether capitalized in the books of account or not); for any period beginning from the date on which the capital was borrowed for acquisition of the asset till the date on which such asset was first put to use, shall not be allowed as deduction.]”

Consequent to assessment proceeding and the disallowances made by the AO, the appellant has not filed any appeal before the CIT (Appeals) regarding the addition of Rs.7,75,53,350/- and hence, the AO initiated penalty proceedings stating under reporting of the income u/s 270A and imposed a penalty of Rs.5,17,80,820/-. The appellant further submits that the section 270A begins with the word ‘may’ and not ‘shall’. The word ‘may’ indicate that a discretion is available with the AO, CIT (Appeals), PCIT not to levy penalty, having regard to the bona fide conduct of the assessee, co-operation shown in the completion of the assessment and general conduct of the assessee in the course of assessment proceedings. The addition/disallowance is a technical mistake. The assessee has not even made any claim on the basis of any false evidence, as the same is part of the books of account of the appellant. Appellant submitted the following case laws in support that there was no ill motive for such omission. It is only a mistake, said income deserves to be excluded from under reporting of income as per section 270A(6)(a) of the Act. The case should be treated as a bona-fide mistake, relying on the Hon’ble Supreme Court decisions:-

1. [Dilip N. Shroff Vs. CIT (291 ITR 519) (SC)]

2. [Dharmendra Textile Processors (306 ITR 277) (SC)]

3. [Reliance Petro Products (P) Ltd. (322 ITR 158) (SC))

4.2 As per appellant, while filing the return it claimed a deduction as interest cost to the tune of Rs. 7,75,53,350/-. The appellant availed deduction of the amount of interest paid in respect of capital borrowed for the purpose of acquiring a company namely; M/s Ramsarup Industries Pvt. Ltd. and claimed the same while computing income from business and profession in its computation of total income. The appellant has borrowed loan to acquire the company and for the purpose of making payment to various stakeholders of M/s Ramsarup Industries Ltd. However, due to some litigation in the company the loan amount could not be capitalized but interest on the loan was paid. Hence, in lack of awareness the appellant has deducted the interest paid on the loan amounting to Rs. 7,75,53,350/- as capital loss/interest cost in the return. Finding the above deduction as misreporting of income the AO has imposed the penalty of Rs. 5,17,80,820/.

Further appellant submits that mere non-filing of appeal against quantum order does not automatically attracts penalty proceeding sand also discussed the following judicial judgements-

-

- Hon’ble Supreme Court in case of Sir Shadilal Sugar Mills (168 ITR 7051)

- Hon’ble Karnataka High Court in case of CIT v. Manjunatha Cotton & Ginning Factory (2013 35 com 250)

- Hon’ble Delhi Bench of ITAT in the case of Rai Industrial Power Pvt. Ltd. Vs DCIT (ITA 4862/Del/2013)

- Hyderabad Tribunal in case of Kalpalatha v. ACIT (66 TAXMAN 111 (HYD.))

4.3 Appellant further submitted on 29-04-2025 that in terms of the requirements of each clause of the said sub section (9) of Section 270A is analyzed and explained by the appellant, Assessing Officer has not specified anywhere in the penalty order as to under which clause of section 270A (9) the case of the assessee falls. Nor these details were specified in the show cause notice or discussed in the assessment order. Assessing Officer has not specified in respect of this disallowance also as to under which clause of section 270A(9) the same is covered. Appellant submitted the following case laws where penalty cannot be imposed u/s 270A(9) where AO has not mentioned the limb/clause of sub-section (9) of section 270A in which assessee falls-

(i) HIGH COURT OF RAJASTHAN Chambal Fertilizers and Chemicals Ltd. v. Office of the Principal Commissioner of Income-tax [2024] 158 taxmann.com 184 (Rajasthan)

(ii) In the case of Schneider Electric South East Asia (HQ) PTE Ltd. v. ACIT [2022] 443 ITR 186 (Delhi),

(iii) ING Saltwater Studio LLP vs. MENT s. NFAC, Delhi [2023] 157 com 749 (Mumbai – Trib.)[22-05-2023]

(iv) 2023] Kishor Digambar Patil vs. Income-tax Officer [2023] 149 com 502 (Pune – Trib.)[30-03-2023]

(v) IN THE ITAT PUNE BENCH ‘A’ DCIT v. Chakradhar Contractors and Engineers (P.) Ltd. [2025] 171 com 133 (Pune Trib.)

(vi) IN THE ITAT MUMBAI BENCH ‘D’ Manish Manohardas Asrani v. INT Tax [2025] 170 com 792 (Mumbai – Trib.)”

6. The Ld. DR for the Revenue contended that the assessee had not disputed the quantum disallowance of ₹7,75,53,350/- made by the AO. He submitted that the assessee had mispresented by claiming deduction for interest expense which otherwise was not allowable and therefore the legal consequence u/s 270A of the Act was that the assessee had misreported the income. The Ld. DR submitted that the AO had specified in the assessment order as well as the penalty notice that the penalty was sought to be levied for under-reporting of income as a consequence of mis-reporting and therefore there was no infirmity in the manner of initiation of penalty proceedings u/s 270A of the Act. The ld. DR prayed before us to reverse the order of the Ld. CIT(A) and restore the penalty levied by the AO.

7. The Ld. AR, on the other hand, placed strong reliance on the above findings of the Ld. CIT(A) and submitted that the order is reasoned and well-founded and that the Ld. CIT(A) had rightly deleted the penalty. He further submitted that impugned disallowance was not a consequence of any misrepresentation or suppression of any facts. He showed us that, the details of borrowing, finance cost, utilization of funds etc. were disclosed on the face of the Profit & Loss Account and that the deduction for interest claimed by the assessee was a considered legal view taken on the basis of several judicial precedents. The Ld. AR took us through the background facts relating to the assessee and its acquisition of M/s Ramsarup Industries Limited through the IBC process and he explained that, the interest paid on borrowings for acquiring strategic investments has been held to be an allowable deduction by several judicial forums. In support, he cited the decisions of the Hon’ble Supreme Court in the cases of S A Builders Ltd. vs. CIT (158 Taxman 74), Hero Cycles Pvt. Ltd. vs. CIT (63 taxmann.com 308), Sharp Business System vs. CIT (181 taxmann.com 657). The ld.AR submitted that the AO had disagreed with this legal position adopted by the assessee and made the impugned disallowance of interest. He submitted that, though the assessee had a valid claim but since the disallowance led to assessed income of only Rs.1,21,503/- and that the disallowed business loss had not been set-off in future years, it was only to avoid time and cost involved in litigation that the assessee did not pursue this matter in appeal. The Ld. AR submitted that the penalty proceedings are independent of the assessment proceedings and that it was open for the assessee to show that the interest claimed in the return of income was justified and that only because the claim was found to be a debatable one on which two views were possible, it cannot be viewed to be a case of misrepresentation or suppression of facts to levy penalty for alleged misreporting of income. The Ld. AR relied upon the following decisions wherein it was held that, penalty cannot be levied u/s 270A of the Act where the claim made was a bonafide one and debatable in nature. In defence of his arguments, the ld. AR relied on the following decisions:

– CIT vs Gurdaspur Co-operative Sugar Mills Ltd (35 taxmann.com 395) [P&H HC]

– CIT v. IFCI Ltd (9 taxmann.com 114) [Del HC]

– GM Modular (P.) Ltd. vs PCIT (185 taxmann.com 495) [Bom HC]

– Essae Suhagraja (P.) Ltd. vs DCIT (181 taxmann.com 302) [ITAT Bang]

– Bharatkumar Jaishinh Soni vs ITO (179 taxmann.com 421) [ITAT Mum]

8. We have heard rival submissions and perusing the materials available on record, we find that the sole issue for our adjudication is whether the ld.CIT(A) was justified in deleting the penalty imposed by the AO u/s.270A of the Act for the impugned assessment year. It is a settled proposition of law that initiation of penalty proceedings must be in strict conformity with the statutory mandate prescribed u/s.274 of the Act. The issuance of a proper and legally sustainable notice u/s.274 of the Act is sine qua non for the valid assumption of jurisdiction to impose penalty. It has been consistently held that a legally valid notice necessarily connotes that the assessee must be clearly apprised of the precise default, contravention, or charge forming the foundation of the proposed penalty proceedings. Failure to specify the relevant charge or default reflects non-application of mind on the part of the authority and thereby vitiates the very initiation of penalty proceedings. Now let us examine the final show cause notice issued by the AO on 24.01.2024 which is extracted below for ready reference:

9. On a careful perusal of the above show cause notice, it is evident that, the show-cause notice issued by the AO suffered from a fundamental defect inasmuch as it is vague, uncertain, and lacked the requisite particulars. In the present case, the impugned notice does not delineate which particular limb or clause of section 270A(9) of the Act is attracted. Sub-section (9) of Section 270A of the Act enumerates various instances that amount to “misreporting of income” such as misrepresentation or suppression of facts, failure to record investments, recording of false entries, or claim of expenditure not substantiated, etc. Each of these instances constitutes a distinct and independent ground, carrying serious penal consequences. We are in agreement with the ld. CIT(A) that it was incumbent upon the AO to state in clear and unambiguous terms which of these specific defaults was being attributed to the assessee, along with the manner in which the ingredients of the alleged default stood satisfied in the facts of the case. The failure to so specify renders the notice fundamentally defective.

10. Apart from the judicial precedents relied upon by the ld. CIT(A), we find that the similar issue had come up for consideration before the ITAT, Chennai in Prakashchand Jain v. Dy. CIT (ITA No.68/Chny/2024 dated 07.03.2025), wherein following the another decision of the co-ordinate bench of this Tribunal in Enrica Enterprises (P.) Ltd. v. Dy. CIT [2024] 163 com 105 (Chennai-Trib.), it was held as under:

“9. According to us, the assessee should be informed in the show-cause notice with certainty and accuracy of the exact nature of the fault alleged against him. In this case, it has been noted that the impugned notice issued by the Assessing Officer is silent about which limb/clause of subsection (9) of section 270A of the Act has been attracted in the facts of the case so as to deserve levy of penalty, and how the ingredients of subsection (9) of section 270A are satisfied. Therefore, the show-cause notice proposing penalty is found to be vague and does not meet the requirement of law to legally impose penalty. Consequently, the levy of penalty is fragile in the eyes of law and is held to be ab initio bad in law.”

11. Following the decision (supra), we are of the considered view that the ld. CIT(A) had rightly appreciated the aforesaid legal position and quashed the penalty levied by the AO u/s270A of the Act.

12. Alternatively, even on merits, it is noted that, the assessee had claimed deduction for interest of Rs.7,75,53,350/- paid on loans utilized in the process of acquisition of strategic investment, M/s Ramsarup Industries Limited through CIRP process of NCLT for furtherance of the business objectives of the assessee. It is observed that the details of finance cost, the utilization of borrowings and its deployment was discernible from the face of the audited financials. As pointed out by the ld. AR, some Courts have held that, the interest relatable to the borrowings which was utilized to make investments in the same line of business as that of the assessee, may be viewed as expenditure incurred for the purposes of business and thus allowable as deduction u/s 36(1)(iii) of the Act. We find that the facts involved in the present case are somewhat similar to the judicial precedents cited by the Ld. AR to justify the claim of interest expenditure. According to us therefore, the impugned issue on which the disallowance was made by the AO was a debatable one involving interpretation of the provisions of Section 36(1)(iii) of the Act. It is seen that, the primary facts had been disclosed by the assessee and the disallowance was made on account of a bona fide legal claim made by the assessee. Hence, we are of the view that the assessee cannot be held to be guilty of misrepresentation or suppression of facts and thus the ingredients contemplated u/s 270A(9)(a) of the Act is found to be missing. Our view is supported by the decision of the ITAT, Bangalore in the case of Essae Suhagraja (P.) Ltd (supra) wherein it was held as under:-

“22. We have carefully considered the rival contention and perused the orders of the learned lower authorities. Briefly stated the fact shows that the assessee has claimed deduction of Rs.50 lakhs towards the Keyman insurance premium paid which is allowed to the extent of the insurance content and to the extent of the investment sum of Rs.4,646,000 was disallowed. The assessment order also speaks about the initiation of penalty u/s. 270 A of the Act. Accordingly, penalty at the rate of 200% of the tax was charged at Rs.2,338,610. In fact, we find that Keyman insurance premium payable by the assessee with respect to the life of its director is held to be allowable u/s. 37 (1) of the Act by several judicial precedents. The expenses itself are held to be allowable by some of the Benches of the Tribunal, the issue becomes highly debatable and divergent views are available that where the keyman insurance policy is allowable as deduction or not. The penalty has been levied on such disallowance. However, as the issue of disallowance has already been concluded and not at all before us, it is only a matter that on such disallowance whether the penalty can be levied under the provisions of section 270A of the Act or not? We find that when the disallowance itself is a debatable issue, no penalty could have been levied. Similarly, it is also the claim before us that penalty proceedings are initiated for under-reporting of income in consequence to misreporting of income. Penalty can be levied on 6 types of acts on behalf of the assessee. It is also true that ld. AO, neither in the assessment order nor even otherwise has stated that under which subclause of 270A of the Act penalty is levied. The Hon’ble Delhi High Court in GE Capital US Holdings Inc. [2024] 163 taxmann.com 146 (Del) has categorically held that it is incumbent upon the AO to ascertain the provisions of section 270A stood attracted either on account of underreporting or misreporting of the income. A finding misrepresentation is required to be written and recorded in the assessment order. In the absence of the same, penalty deserves to be deleted. Accordingly, we allow the appeal of the assessee and direct the ld. Ao to delete the penalty levied of Rs.23,38,610 being 200% of tax of Rs.11,69,305 on disallowance of keyman insurance premium expenditure of Rs.46,46,000 in the hands of the assessee.”

13. For the reasons discussed above, we hold that the AO was unjustified in levying the penalty u/s 270A of the Act and thus, uphold the order of Ld. CIT(A) deleting the same by dismissing the appeal of the revenue.

14. In the result, the appeal of the Revenue is dismissed.

The order is pronounced in the open Court on 25/06/2026.

Author Bio