Case Law Details

ACIT Vs Bonlon Industries Ltd. (ITAT Delhi)

The Delhi ITAT disposed of Revenue appeals and the assessee’s cross-objections arising from orders of the CIT(A)/NFAC deleting additions made on account of alleged bogus purchases and related transactions involving RCI Industries & Technologies Ltd.

For Assessment Year 2018-19, the Assessing Officer had reopened the assessment and made an addition of ₹9.16 crore by estimating 12.5% of purchases from RCI Industries as bogus. The Revenue relied primarily on investigation reports, retrospective cancellation of the supplier’s GST registration, and non-response to notices. The assessee contended that it maintained complete books of account, stock registers, purchase invoices, transport documents, GST returns, bank statements, confirmations from the supplier, and corresponding sales records. It also explained that RCI Industries had entered Corporate Insolvency Resolution Process (CIRP), and therefore the Assessing Officer ought to have sought information from the Resolution Professional instead of drawing adverse inferences. The assessee further pointed out that similar transactions with RCI Industries had been accepted by the Department in other cases.

The Tribunal noted that the Revenue had not challenged the CIT(A)’s finding declaring the reassessment invalid on the additional legal ground. Nevertheless, it examined the deletion of the addition on merits. It observed that the CIT(A) had thoroughly analysed the evidence, including purchase invoices, e-way bills, GST returns, transport receipts, bank payments, stock records and confirmations. The books of account had not been rejected, the sales were accepted as genuine, and there was no evidence showing that the purchases were sham or intended to evade tax. The Tribunal also found merit in the assessee’s contention that notices should have been addressed to the Resolution Professional after commencement of CIRP. Holding that ad hoc disallowance of 12.5% of purchases without disproving the documentary evidence was unsustainable, it upheld the deletion of the addition and dismissed the Revenue’s appeal. The assessee’s cross-objection was dismissed as academic in view of the decision on merits.

For Assessment Year 2019-20, the Assessing Officer made additions under Sections 69C and 69A aggregating over ₹32.33 crore by treating purchases from and sales to RCI Industries as non-genuine. The additions were based on alleged bogus purchases, unexplained money arising from sales involving the amalgamated company Smita Global Pvt. Ltd., cancellation of the supplier’s GST registration, absence of certain transport documents and non-confirmation of transactions. The assessee argued that the purchases and sales were fully supported by invoices, GST returns, ledger accounts, bank statements, stock records, e-way bills and confirmations. It further submitted that relevant records had been seized by the GST authorities and requested the Assessing Officer to summon those records, which was not done. It also highlighted that RCI Industries had responded to notices through the Resolution Professional during CIRP and had furnished available records.

The Tribunal upheld the CIT(A)’s detailed findings deleting all additions. It observed that retrospective cancellation of the supplier’s GST registration did not invalidate transactions undertaken when the registration was valid. It accepted the finding that the outstanding trade creditors were not unusually old, the purchases and sales were fully reconciled, the books of account had not been rejected, and the Assessing Officer had failed to conduct proper independent enquiries despite possessing statutory powers. The Tribunal further agreed that no addition could be sustained merely on suspicion or general information when contemporaneous commercial records established genuine business transactions and corresponding sales had been accepted. Since the additions under Sections 69A and 69C were deleted, the consequential application of Section 115BBE also ceased to survive. Accordingly, the Revenue’s appeal for Assessment Year 2019-20 was dismissed.

Cases Discussed (Latest to Oldest):

- PCIT Vs Forum Sales Pvt. Ltd., ITA 862/2019, Delhi High Court, dated 01.03.2024.

- Home Developers Project Pvt. Ltd. Vs DCIT, ITA No. 390/Del/2019, ITAT Delhi, dated 26.07.2023.

- Rasilaben Yogeshbhai Patel vs. ITO Ward 5(3)(2), Ahmedabad, ITA No.631/AHD/2019, ITAT SMC Bench, dated 07.10.2022.

- Madhurittu Puri vs. DCIT, Circle International Taxation 2(2)(2), New Delhi, ITA No. 3063/Del/2022, ITAT Delhi.

- REKHA RAJESH JOGANI VS. INCOME TAX OFFICER WARD 19(3)(1), MUMBAI, ITAT Mumbai, 2025.

- Ashok Kumar Rungta Vs. Income Tax Officer 24(1)(1), Income Tax Appeal Nos. 1753, 1759 & 2780 of 2018, Bombay High Court.

FULL TEXT OF THE ORDER OF ITAT DELHI

The appeals of the Revenue and cross objections by the assessee are directed against the order dated 18.09.2025 & 24.09.2025, passed by CIT(A)/NFAC, Delhi u/s 250 of the Income Tax Act, 1961 (hereinafter referred to as “the Act”) wherein the addition made by the AO vide assessment order dated 19.05.2023 and 30.03.2025 were deleted.

2. These three appeals and the corresponding CO are being disposed off by this common order as the parties are same and factual matrix is also same and in order to avoid the multiplicity of decision, the same are being disposed off accordingly. ITA No. 7987/Del/2025 is taken as lead case.

ITA No. 7987/Del/2025 (Revenue) and

CO No. 6/Del/2026

3. The appeal of the Revenue is directed against order dated 18.09.2025 u/s 250 r.w.s. 254 of the Act passed by ld. CIT(A)/NFAC, Delhi wherein the addition has made vide assessment order dated 13.01.2023 by way of variation, making addition of 12.5% of bogus transaction for Financial Year 2017-18 out of bogus purchase as VAT and GST purchase of Rs.73,32,84,161/- i.e. Rs.9,16,60,520/-.

4. The facts in brief as culled out from the authorities below are that the assessee is a company filed his return of income for A.Y. 2018-19 declaring total income as Rs. Nil. During the year under consideration, information was received that assessee company had entered into the transaction of bogus purchases with Ms/ RCI Industries and Technologies Ltd. during the Financial Year 2017-18. Accordingly, the case was reopened u/s 147 of the Act by issuance of notice u/s 148 dated 31.03.2022. Further notices u/s 143(2), 142(1) of the Act alongwith show-cause notices were also issued to the assessee. The assessee filed response and assessment was completed u/s 147 r.w.s. 144/144B of the Act on 19.05.2023 by assessing total income of Rs.9,16,60,520/-.

5. Aggrieved with the said addition, the assessee filed appeal before the ld. CIT(A) who dismissed the same vide order dated 29.09.2025. The said order was challenged before the Hon’ble ITAT Delhi Bench ‘A’, New Delhi which remitted back the matter to the ld. CIT(A) with direction to decide the matter on merits. In his written submission before the ld. CIT(A) during the second round of hearing, the appellant submitted that it was engaged in the business of manufacturing and trading of nonferrous metal mainly in copper (copper wire and copper wire rod etc.). The assessee filed ITR on 29.11.2018 at the total income Rs. Nil, claiming refund of Rs.1,20,610/- which was processed u/s 143(1) vide order dated 24.05.2019 on returned and income. The AO, DCIT, Circle-4(2), New Delhi had passed order u/s 148(d) of the Act on 31.03.2022 and reopened the proceedings u/s 147 by issuing notice u/s 148 of the Act. the ld. AO, DCIT, Circle-4(2), New Delhi had passed assessment order u/s 147 r.w.s. 144B of the Act on 19.05.2023 assessing total income at Rs.9,16,60,520/- by making the addition of the said amount as suppressed profit on alleged bogus purchases. The said addition was challenged before the ld. CIT(A)/NFAC, Delhi wherein assessee claimed that there were no bogus purchases from RCI industries and explained that the total purchases made during the year were to the extent of Rs.247,93,48,111. These includes purchases made from RCI Industries of Rs.73,32,84,161/- which is alleged to be bogus purchases by the Assessing Officer. It is stated that the total sales as stated above has been shown in the P&L account at Rs .241,92,66,934/-.

6. It was further claimed that the books of account of the assessee have not been rejected and the sale figure has also not been rejected. And as such, it cannot be said that the assessee has sold the goods without making any purchases. It was further stated that RCI Industries has gone into insolvency proceedings initiated before the NCLT, who has appointed Resolution Professional (RP) to look after the affairs of the company. And the AO did not exercise his power to get necessary reply from the RP. And the AO simply issued notice to the RCI Industries, who were not supposed to respond to the sad notice allegedly issued. And on that basis, the AO has wrongly concluded that the purchases were not made from the RCI Industries. It is further stated that the assessee has filed all necessary documents, including Sales tax/GST returns, (Pages 455 to 596). Apart from other documents, which include purchase advice, transport receipts, bank statements, showing payments and confirmation from supplier, GST returns of the supplier and party-wise sales of Rs.241,92,66,934/-. It is further stated that the purchase and sales are matching, with inflow and outflow stock, and there is no defect in the stock register. Purchase and sales are interlinked and inseparable. It is further stated that AO has disallowed 12.5% of the purchase value from RCI Industries and allowed 87.5% of the entire purchase as genuine business expenditure. Hence, it is stated that a purchase cannot be partly bogus and partly genuine and as such, no addition was required to be made on that account. It is further stated that the AO has wrongly relied on the cancellation of GST registration of RCI Industries, which was made by the GST officer only on 21.02.2023, however from retrospective effect. It is further stated that the GST registration of the RCI Industries was valid when the purchases were made in the financial year 2017-18 relevant to A.Y. 201819. It was further stated that similar purchases & sales from RCI Industries has been accepted by the Revenue in other cases, i.e. Captain Industries PAN AAFFC0006A by the AO ACIT, Circle-14(1), Delhi. Another one is Myco Electrical Private Limited, Assessed PAN AAACM1868B by AO Assessment Unit, Income Tax Department, NFAC. Since, the single purchases/transactions made from RCI Industries by these other entities has been accepted by the department, hence considering the purchases by the assessee from RCI Industries as bogus despite all necessary documents having been produced before the AO, has violated Article 14 of the Constitution as rights to equality has been denied to the assessee.

7. We have noticed that before the ld. CIT(A), the assessee has raised additional grounds of appeal, which is produced at page 5 of the impugned order as under:

“11. That on the facts and circumstances of the case the jurisdictional assessing officer A.O. DCIT Circle 4(2), New Delhi has erred on the facts and in law issuing notices u/s 148 and 148A of the I. T. Act 1961, specifically after the introduction of Section 151A of I. T. Act 1961 and issuance of CBDT Notification No. 18/2022 dated 29.03.2022, resulting in framing the illegal assessment and is thus required to be quashed in view of the recent decision of the Hon’ble Supreme Court in the case of ADIT vs. Deepanjan Roy dated 16.07.2025 wherein it has been held that issue of Notice u/s 148 in faceless manner is mandatory.”

8. In this regard, additional grounds raised was allowed by the ld. CIT(A) holding that the assessment order passed on 19.05.2023 is null and void. However, the ld. CIT(A) proceeded to adjudicate the appeal on merit also. On merit, the grounds Nos. 1 & 4, raised before the ld. CIT(A) were dismissed. However, the remaining grounds of appeal, Nos. 5, 6 & 7, pertains to the addition of Rs.9,16,60,250/- on account of bogus purchases in the form of accommodation entry from RCI Industries & Technology Ltd. were considered and allowed.

9. Aggrieved by the impugned order, the Revenue has filed the present appeal before us and raised the following grounds of Appeal:

“1. That on the facts and in the circumstances of the case and in law, the Ld. Commissioner of Income Tax (Appeals) has erred in deleting the addition of Rs.9,16,60,520/- made by the Assessing Officer on account of bogus purchases from M/s RCI Industries & Technologies Ltd., without appreciating the detailed findings recorded in the assessment order based on credible and specific investigation reports received from the Directorate of Investigation and the DVU.

2. That the Ld. CIT(A) has erred in holding that since the books of account were not rejected under section 145(3), the addition could not be sustained, without appreciating that rejection of books is not a precondition for estimation of profits as bogus purchases claimed by assessee.

3. That the Ld. CIT(A) has erred in ignoring the fact that the addition made by the Assessing Officer was of the profit element embedded in the bogus purchases, computed at 12.5% in accordance with judicial precedents, and therefore represented a fair and reasonable estimation of income.”

10. On perusal of these grounds, it is evident that the Revenue has not challenged the decision on additional grounds wherein the ld. CIT(A) has held the assessment order bad in law.

11. We have heard the ld. AR and the ld. DR and examined the record. The ld. DR, on behalf of the Appellant Revenue while relying on the AO’s order has argued that the AO has rightly added 12.5% of the total bogus purchases because the GST number of RCI Industries and Technologies was cancelled suo motu by GST Department with effect from 01.07.2017. Hence, the alleged purchases made during Financial Year 2017-18 by the assessee has to be considered to be bogus as per GST Portal, the suo motu cancellation can be initiated by tax officials for 3 reasons.

“1. Any Tax payer other than composition tax payer has not filed the tax returns for continuous period of six months.

2. Supplies any goods and/ or services without issue of any invoice, in violation of the provision of the Act or Rules made there under, with the intension to evade tax.

3. Registration has been obtained by means of fraud, willful misstatement or suppression of facts etc., and for other reasons such as death of Soul proprietor, ceased to be liable to pay tax etc.,

From the reading of the above it was clear that the GST number of the above supplier was stood cancelled due to the reason as mentioned above.”

12. With regard to the documents furnished by the assessee, it is argued by the ld. DR that there is various deficiencies in those documents as pointed out by the AO and the same has been wrongly ignored by the ld. CIT(A) while deleting the addition made by the AO.

13. The ld. AR on the other hand argued that there is no explanation regarding the acceptance of similar purchases for A.Y. 2018-19 from RCI Industries Ltd. by the concerned AO in case of Capitan Industries and Myco Electricals (supra) vide order dated 23.03.2023 and 09.03.2023 respectively. With regard to the reliance of the AO on non-receiving of reply from RCI Industries when notice was issued u/s 133(6), it is argued that at the time of alleged notice which was issued in the year 2023 whereas the purchases were made in A.Y. 2018-19, the RCI Industries has undergone into insolvency proceedings by issuance of CIRP by the Hon’ble NCLT and Resolution professional was already appointed. It is argued that the AO has failed to issue notice to the Resolution professional for seeking the necessary information and issuance of notice to RCI Industries already under going insolvency was not legally justified and as such has been rightly rejected by the ld. CIT(A).

14. We have considered the rival submissions and examined the record. All the arguments raised by the Revenue with respect to the deleting the addition made @ 12.5% of the alleged bogus purchases has been considered and adjudicated upon as ground Nos. 5, 6 & 7 from para 7.1 onwards in the impugned order and the relevant findings from para 7.3 to 7.7 are extracted below as under:

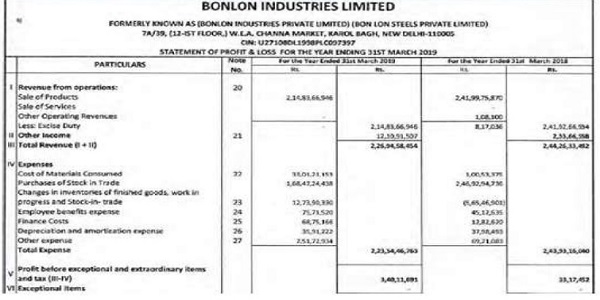

“7.3 I have carefully considered the submissions of the appellant. It has been claimed by it that the total purchases made during the year were to the extent of Rs.247,93,48,111/- as per profit and loss account (Raw material Rs. 1,00,53,375 + Purchase of Stock in Trade 2,46,92,94,736). This includes purchases made from RCI Industries at Rs. 73,32,84,161/- as per statement filed before the A.O. which has been taken as Bogus purchase. The total sales made by the appellant during the year were Rs. 2,41,92,66,934/-. It has also been claimed by the appellant that Books of accounts of the appellant have not been rejected. Also the sales figure has also not been rejected.

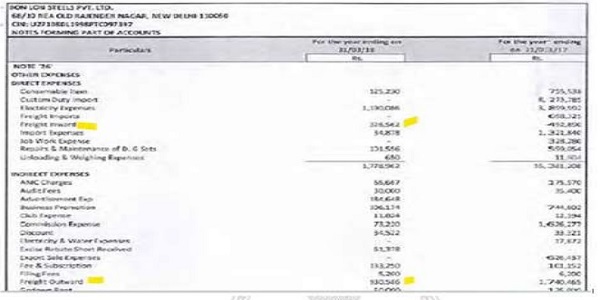

7.4 I have gone through the submissions of the appellant and other documents produced by him in the appellate proceedings. I have also gone through the P & L account furnished by the appellant. I have noticed that total trading sales is at Rs. 241,92,66,934/- and the Ld. A.O. disallowed the 12.5% of purchases amounting to Rs. 9,16,60,520/- of the traded goods from RCI industries. The Ld. A.O. did not reject any corresponding sales figures. The Ld. A.O. did not reject the books of the appellant and did not re-caste the trading account. I have also gone through the documents submitted by the appellant related to the so-called parties/suppliers. I have noticed that in most of the cases e-way bills are also enclosed and all the bills appear to be in order. All the said parties are filing ITRs and maintaining books of accounts. It is further noticed that the RCI Industries has gone into Insolvency proceedings and therefore the NCLT has appointed the Resolution Professional (“RP”) to look after the affairs of the company. It is further noticed that the appellant is maintaining stock register invoice by invoice. It is further noticed that the appellant has filed sale tax/GST returns, apart from other documents which purchase invoices, Transport receipts, bank statements showing payments, confirmation from supplier (RCI), GST returns of the supplier (RCI) and also filed quantity-wise purchases and Party-wise sales of Rs. 2,41,92,66,934/-. The purchase and sales are matching with inflow and outflow of stock. It is further noticed that all these documents were produced by the appellant before the Ld. A.O as seen from the submission of the appellant dated 24.03.2022, 28.03.2022, 30.11.2022, 23.01.2023, 17.02.2023 and 16.05.2023. The action of the A.O. by disallowing 12.5% of the purchases from RCI industries and without disturbing the sales & without rejecting the books of account is not justifiable. It is further noticed that Cancellation f GST registration of RCI was ma de by the GST Officer, as per notice dated 21.02.202 and registration was suspended from 21.02.2023. Also the order for cancellation of GST registration of RCI was made on 21.02.2023. Thus the GST registration was not cancelled during th e period relevant to A. Y. 2018-19 . AO’s argument regarding low freight has also been explained by the appellant by stating that:

In Para 4.4 of the Assessment Order, the Ld. AO has noted that the appellant has reported only 35,900/- as freight charges against the substantial amount of purchases. It has also been inferred that the same is irrational considering the volume of purchases.

RCI Industries & Technologies Ltd.-Financial Background 1.1.19):

| FY | Revenue from Operations (₹ Lakhs) | EBITDA (₹ Lakhs) | PBT (₹ Lakhs) | PAT (₹ Lakhs) | Equity Capital (₹ Lakhs) | Reserves & Surplus (₹ Lakhs) |

| 2014-15 | 118,727 | 3,095 | 2,755 | 2,188 | 2,020 | 10,506 |

| 2015-16 | 142,471 | 3,506 | 3,285 | 2,625 | 2,020 | 12,812 |

| 2016-17 | 175,670 | 4,120 | 3,982 | 3,280 | 2,020 | 15,581 |

| 2017-18 | 204,403 | 6,450 | 4,037 | 3,280 | 1,344 | 10,311 |

| 2018-19 | 197,780 | 4,565 | 4,565 | 3,667 | 1,344 | 11,936 |

1. It is pertinent to highlight that RCI Industries & Technologies Ltd. was a listed company on the Bombay Stock Exchange during FY 2017-18 and FY 2018-19, engaged in significant trading and manufacturing activities. The company had a large turnover and positive profitability during these years, reflecting genuine commercial operations and not a shell entity. Subsequently, due to financial distress, RCI Industries was admitted into Corporate Insolvency Resolution Process (CIRP) by the Hon’ble NCLT, New Delhi Bench-III, vide order dated 25.11.2022, copy enclosed (Annexure 5). The Resolution Plan has been duly approved and arguments concluded before NCLT, copy enclosed (Annexure 6), with the order reserved on 31.07.2025. This establishes that the entity was a functioning and credible listed company carrying substantial business during the relevant years.

2. Audited financial statements for the year ended on 31.03.2018 (Annexure 3) and for the year ended on 31.03.2019 (Annexure 4), which are duly filed before Stock Exchanges and government authorities and are available online, are enclosed herewith.

3. It is respectfully submitted that the assessee has purchased goods from RCI by means of a total 136 sales invoices from various locations in Delhi and Rajasthan with summary details as follows:

2.1 It can be seen from the purchase invoices the freight was always included in the purchase price and was not charged separately when sales were made in intrastate within Rajasthan, and interstate from Rajasthan to Delhi. Following is the location-wise summary of purchases made from RCI Industries (Copy Enclosed – Annexure 2).

Purchase Detail RCI Industries Ltd from 01-04-2017 to 31-03-2018

| From RCI Location | To Bonlon Location | Quantity (KGS) | Purchase Amount | GST/VAT Input | Freight | Gross Purchase |

| F-37(A-1) Khushkheda RIICO Ind Area, Bhiwadi Rajasthan | H-1/130(B)RIICO Ind. Area, Bhiwadi Rajasthan | 3,05,611 | 15,03,45,293 | 82,68,092 | Included in Price | 15,86,14,285 |

| F-37(A-1) Khushkheda RIICO Ind Area, Bhiwadi | J-1130 Phase-IIIRIICO Ind. Area, Bhiwadi | 5,49,822 | 22,11,28,689 | 1,21,62,078 | Included in Price | 23,32,90,767 |

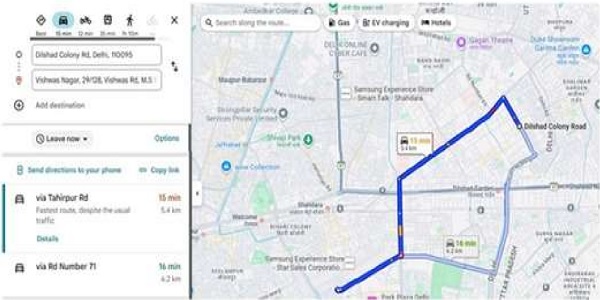

1.1. The above it is seen that only on 23 invoices at serial no 114-136 which are local purchases from RCI Location at 10/128/IV, Vishnu Gali, Vishwas Nagar, Delhi-110032 to Bonlon location at 488D1, Dilshad Garden, Delhi-110095, which was only a small distance of 5.4 km and 15/20 minutes commute only, the freight was charged extra on actual which varies from Rs.1300 to Rs.1900 per lorry.

Amount of 35,900/- has been recorded based on freight charges included in the purchase invoices raised by RCI Industries, as reflected in the party-wise purchase details already submitted and placed at Page No. 607 of the paper book. This freight amount was charged in the invoices raised and part of the purchase.

1.1. In addition, we are enclosing herewith a statement showing invoice-wise purchases made from RCI Industries, along with details of movement of goods (From and To locations) (Copy Enclosed Annexure 1) and remarks indicating the details of invoices included freight paid by RCI. These details clearly demonstrate that the freight component, wherever applicable, was either included in the invoices raised by the supplier or borne by the supplier, as the terms of purchase were ex-freight.

1.1. Appellant has also submitted date-wise and bill-wise details of other freight expenses of Rs. 11,49,048/- incurred on other purchases excluding RCI Industries and sales made at Page Nos. 288 to 299 of the paper book, which have been duly booked in the profit and loss account.

1.1. Goods purchased from RCI Industries, Delhi were transported from their godown located at Vishnu Gali, Vishwas Nagar, Shahdara, Delhi to the appellant’s godown at Jhilmil, Shahdara, Delhi, which is merely around 4 kilometers in distance.

Similarly goods purchase from RCI Industries, Bhiwadi Rajasthan were transported from their godown at RIICO Ind Area, Bhiwadi Rajasthan to appellant’s godown at same location i.e. at RIICO Ind Area, Bhiwadi, Rajasthan. Considering the very short distance and the high value & low volume of the metals, the freight costs incurred were understandably minimal.

1.1. are either borne by the supplier or the delivery is arranged at the buyer’s godown as part of the sale terms. Furthermore, in some cases, the purchases were made with instructions for delivery at the appellant’s godown, and sales were also made on a similar delivery basis. Hence, no additional freight expense was incurred by the appellant on such transactions.

1.1. it is submitted that in all the appellant company has incurred freight expenses of Rs. 11,49,048/- on purchases and sales as under:

| Other Operating Revenue – Freight Other | (108,100) |

| Direct Expenses – Freight Inward | 326,562 |

| Indirect Expenses – Freight Outward | 930,586 |

| Total Freight Expenses – As per P&L a/c | 1,149,048 |

1.1. expenses have been separately debited in Profit and Loss account as under (Page No. 16):

1.1. In view of the above submissions and supporting documentary evidence, it is submitted that the freight charges of 35,900/- as recorded in the books are bona fide and duly supported by bills and documents. The same have been incurred only in those instances where the supplier did not bear the cost. The observation of the Ld. AO regarding the irrationality of freight charges may kindly be reconsidered in view of the above explanation and facts.

From RCI Location |

To Bonlon Location |

Quantity (KGS) |

Purchase Amount |

GST/VAT Input |

Freight |

Gross Purchase |

F-37(A-1) Khushkheda RIICO Ind. AreaBhiwadi, Rajasthan |

G-1/663 Phase IRIICO Ind. AreaBhiwadi, Rajasthan |

96,981 |

3,98,59,191 |

71,74,652 |

Included in Price |

4,70,33,843 |

10/128/IV, Vishnu GaliVishwas NagarDelhi-110032 |

G-1/663 Phase IRIICO Ind. AreaBhiwadi, Rajasthan |

1,05,708 |

4,48,89,408 |

80,80,094 |

Included in Price |

5,29,69,502 |

F-37(A-1)Khushkheda RIICO Ind. AreaBhiwadi, Rajasthan |

G-1/663 Phase IRIICO Ind. AreaBhiwadi, Rajasthan |

1,59,803 |

7,43,54,326 |

1,33,83,778 |

Included in Price |

8,77,38,104 |

10/128/IV, Vishnu GaliVishwas NagarDelhi-110032 |

A-78, Jhilmil Ind. AreaG.T. RoadShahdara, Delhi-110095 |

35,720 |

1,58,95,400 |

28,61,172 |

Included in Price |

1,87,56,572 |

10/128/IV, Vishnu GaliVishwas NagarDelhi-110032 |

488-D1, Delshad GardenDelhi-110095 |

2,40,097 |

11,42,70,107 |

2,05,75,081 |

Freight charged extra – 35,900 |

13,48,81,088 |

Total |

15,53,742 |

66,07,42,415 |

7,25,05,847 |

35,900 |

73,32,84,161 |

7.5 On perusal of submission of the appellant, it is also noticed that in the following similar cases, the Ld. AO has accepted the purchase and sales transactions from RCI industries for the impugned assessment year 2018-19:

i. Captain Industries, C-6B/11, Janak Puri, New Delhi – 110058, assessed under PAN AAFFC0006K by the NFAC, Delhi order dated 23.03.2023.

ii. Myco Electricals Private Limited, D-2/3 (Front Side), Okhla Industrial Area, Phase II, Tehkhand, Delhi – 110020, assessed under PAN AAACM1868P by the A.O. Assessment Unit, Income Tax Department, NFAC order dated 09.03.2023.

7.6 The appellant has also relied upon the following judgement of Hon’ble Courts with request that it should be treated equally and without discrimination:

i. ITAT SMC Bench dated 07.10.2022 in the case of Rasilaben Yogeshbhai Patel vs. ITO Ward 5(3)(2), Ahmedabad in ITA No.631/AHD/2019,

ii. ITAT Delhi D Bench in the case of Madhurittu Puri vs. DCIT. Circle International Taxation 2(2)(2) New Delhi in ITA No. 3063/Del/2022,

iii. ITAT Mumbai in the case of REKHA RAJESH JOGANI VS. INCOME TAX OFFICER WARD 19(3)(1), MUMBAI (ITAT MUMBAI 2025),

iv. Hon’ble Delhi High Court in the case of PCIT Vs Forum Sales Pvt. Ltd. in Appeal Number: ITA 862/2019, dated 01/03/2024, v. Delhi ITAT in the case of Home Developers Project Pvt. Ltd. Vs DCIT in Appeal Number: ITA No. 390/Del/2019 dated 26/07/2023, vi. Bombay High Court in Income Tax Appeal No. 1753, 1759 & 2780 of 2018, in the case of Ashok Kumar Rungta Vs. Income Tax Officer 24(1)(1),

7.7 Considering the above facts and circumstances and legal position of the case, the action of the A.O. by disallowing partly the purchase from RCI industries on ad hoc basis and without disturbing the sales is not justifiable. Keeping in view of above observation, the addition made by A.O. is deleted and the grounds of the appellant are allowed.

Thus, grounds of appeal no. 5, 6 & 7 of the appellant are “allowed.”

15. We have examined the findings of the ld. CIT(A) extracted above wherein the additions so made by the assessment order were deleted on merit. We have also considered the submissions of the parties. In view of the detailed examination of the facts relating to the said addition by the ld. CIT(A), we have noticed that the findings returned by the ld. CIT(A) is based on meticulous examination of all the necessary facts and the materials produced by the assessee. The arguments raised by the respondents/assessee in these appeals are cogent and convincing. The arguments raised by the assessee regarding the Revenue in two other similarly placed matters involving purchases from RCI Industries and Technology Ltd. accepted the purchases as genuine and also that the AO has wrongly relied the non-receiving of reply to the notice from RCI Industries despite it has already gone into insolvency proceedings and the notice was required to be issued to the Resolution professional, are cogent and convincing and there is no rebuttal of the same by the Revenue.

16. For these reasons, we are of the considered opinion that the ld. CIT(A) has rightly deleted the addition made because the assessee has provided whole evidence proving that the purchases made from RCI Industries were genuine and not bogus. An addition of 12.5% of the total purchases made was not legally justified. Accordingly, the grounds raised by the revenue in the appeal are dismissed and the order of the ld. CIT(A) is confirmed.

CO No. 6/Del/2026

17. The assessee has raised following grounds in the Cross Objection:

1. Initiation of the proceedings by the A.O. DCIT, Circle 4(2), New Delhi vide Notice u/s 148A(b) and 148 of I. T. Act 1961 is without jurisdiction as the returned income was at a Loss of Rs. 4,22,818 being less than 15 Lacs and the correct jurisdiction falls with the Income Tax Officer Ward – 4(2), New Delhi, is thus unjust, illegal, arbitrary and against the facts and circumstances of the case.

2. Action of the CIT (A) in confirming the action of the A.O. who has failed to verify the correctness of the information received from the insight portal and has failed to showcase as to how information suggests that the income has escaped assessment making the assessment as illegal, arbitrary and against the facts and circumstances of the case (As per Ground of Appeal No. 5 before the CIT(A).

3. The impugned assessment order is bad in law as the same has been mechanically passed by the A.O. and does not provide any cogent explanation for making additions to the income of the appellant and the A.O. has failed to consider the replies of the appellant during the course of reassessment proceedings and also in the proceedings u/s 148A(b) of I. T. Act 1961 and has mechanically passed the impugned assessment order (As per Ground of Appeal No. 7 and 8 before the CIT (A).

4. The reassessment proceedings initiated by the A.O. based on information received from the insight portal is bad in law as the same is a borrowed satisfaction and no independent inquiry has been made (As per Ground of Appeal No. 9 before the CIT (A).”

18. In view of the our decision on the appeal in ITA No. 7987/Del/2025, wherein the finding of the ld. CIT(A) deleting the addition made on merit has been confirmed, the decision on ground raised in cross-objection has become academic and we have not decided the same. Moreover, all the grounds of cross-objection are legal grounds which in view of our finding on appeal has already rendered academic and need not be adjudicated. The cross-objection of the assessee is accordingly dismissed in above terms.

ITA No. 7989/Del/2025: A.Y. 2019-20

19. The Revenue has raised the following grounds in the appeal:

1. That on the facts and in the circumstances of the case, the Ld. CIT(A) has erred in deleting the addition of Ps. 21,21,45,681/- made by the Assessing Officer under section 69C of the Income-tax Act, 1961, despite the assessee’s failure to substantiate the genuineness of purchases claimed to have been made from M/s PCI Industries & Technologies Ltd., in view of non-production of complete invoices, absence of transporter details, absence of GP/LP, incomplete bilties, and the fact that the supplier’s GSTIN was cancelled w.e.f. 01.07.2017, rendering the alleged purchases unverifiable and non-genuine.

2. That on the facts and in the circumstances of the case, the Ld. CIT(A) has erred in deleting the additions of Ps. 31,37,286/- and Ps. 28,23,557/- made under section 69A on account of unexplained money arising from bogus sales recorded by M/s Smita Global Pvt. Ltd. with PCI Industries, despite the assessee’s failure to produce any documentary evidence of actual delivery of goods, such as GP/LP, transporter details, bilties, delivery

acknowledgements, purchase orders, and despite the buyer, M/s PCI Industries & Technologies Ltd., failing to confirm the sales in response to notice issued under section 133(6).

3. That on the facts and in the circumstances of the case, the Ld. CIT(A) has erred in deleting the additions of Ps. 5,53,82,101/- and Ps. 4,98,43,891/- made under section 69A on account of unexplained money arising from bogus sales recorded by the assessee, M/s Bonlon Industries Ltd. with RCI Industries, without rebutting the detailed findings of the Assessing Officer regarding absence of complete transportation records, incomplete bilties, absence of purchase orders, non-confirmation of sales by the alleged buyer, and non-compliance by the transporters summoned during investigation.”

20. For A.Y. 2019-20, the transactions with the M/s RCI Industries & Technologies Ltd. involved is as under:

“2.1 In this case, information was received to the department that an entity M/s RCI Industries and Technologies Limited was found to be engaged in both availing and issuing of bogus Input Tax Credit to its beneficiaries. On verification of the purchase parties of M/s RCI Industries and Technologies Limited, it was observed that M/s Smita Global Pvt. Ltd (PAN: AAFCS2391Q) has made a sale transaction of Rs. 3,J 3,71,856/- and Bonlon Industries Ltd. has made a ‘sale transaction of Rs. 55,38,21,013/-. Further, on verification of the sale parties of M/s RCI Industries and Technologies Limited it was observed that the assessee company i.e. Bonlon Industries Ltd. made a purchase of Rs. 21,21,45,681/-.

Transaction with M/s RCI Industries and Technologies Limited

| Purchase | Sale | |

| M/s Bonlon Industries Ltd. | Rs. 21,21,45,681/- | Rs. 55,38,21,013/- |

| M/s Smita Global Pvt. Ltd | – | Rs. 3,13,71,856/- |

21. We have noticed that M/s Smita Global Private Limited (PAN-AAFCS2391Q) was got merged with the assessee company, Bolton Industries Limited vide order of Hon’ble NCLT dated 13.06.2018 and effective date was 13.06.2018. The entity M/s Smita Global Private Limited had filed ITR dated 22.10.2019 at income of Rs.8,74,760/- under normal provision and Rs.8,52,959/- under MAT provision u/s 115JB of the Act. The assessee has filed ITR in accordance with notice u/s 148 of the Act dated 19.05.2023 at loss of Rs. 3,87,95,148/- under normal provisions and Rs. 3,44,34,682/- under MAT provision u/s 115JB of the Act. During the assessment proceedings, the Assessing Officer has issued notice u/s 133(6) of the Act dated 25.02.2025 to M/s RCI Industries and Technologies to verify the genuineness of the sale and purchase transaction with the assessee. A response was received on 25.03.2025 informing that the company is under CIRP and availability of information is limited on account of Board of Directors being under suspension and all the employee has left the organization and at present, the resolution professional has managing the affair of the company. Thus whatsoever available information was shared. However, the RCI Industries and Technologies has submitted few sample bills, ledgers and bank statements for around one month and it could not provide the relevant details of the documents required for proof of the genuineness of the transaction and actual delivery of goods. Similarly, no notice to Resolution Professional (RP) was issued by the AO to get the relevant information with respect to the RCI Industries before making the alleged addition. All explanations submitted by the assessee with respect to the purchases made by assessee and the sales made by Smita Global Pvt. Ltd. to M/s RCI Industries were not considered by the Assessing Officer before making various additions.

22. While completing the assessment, the AO has computed total income as under:

“14. In view of the above discussion, the computation of total income is as under:

| As per normal provisions of the Act | ||

| Particulars | Amount in (Rs.) | Amount in (Rs.) |

| Returned income of the assessee

(i) M/s Bonlon Industries Ltd |

(Rs. 3,87,95,027/-) |

(Rs. 3,79,20,267/-) |

| (ii) M/s Smita Global Pvt Ltd. | Rs. 8,74,760/- | |

| Add: addition made in order u/s 147 r.w.s. 143(3) of the Act

(i)Addition u/s 69C as per para 11 |

Rs.21,21,45,681/- |

Rs. 32,33,32,516/- |

| ii) Addition u/s 69A as per para 12 | Rs. 59,60,843/- | |

| (i) Addition u/s 69A as per para 13 | Rs. 10,52,25,992/- | |

| Income recomputed as per normal provisions of income tax act | Rs. 32,33,32,516/- | |

—

| As per MAT provisions u/s 115JB of the Act | ||

| Particulars | Amount in (Rs.) | Amount in (Rs.) |

| Returned income of the assessee

(iv) M/s Bonlon Industries Ltd |

Rs. 3,44,34,682/- | 3,52,87,641/- |

| (i) M/s Smita Global Pvt Ltd. | Rs. 8,52,959/- | |

| Add: addition made in order u/s 147 r.w.s. 143(3) of the Act | N/a | |

| Income recomputed as per MAT provisions u/s 115JB of the Act | 3,52,87,641/- | |

15. Hence, the total income of the assessee is assessed at Rs.32,33,32,516/-under normal provision of income tax and Rs.3,52,87,641/- as per MAT provisions u/s 115JB vide this order u/s 147 read with Section 143(3) of the Income Tax Act. Losses of Rs.(3,79,20,267/-) is to be carry forwarded to the next years. Further, the provisions of Section 115BBE are applicable in this case, which are reproduced below for reference.

Section 115BBE of the Income Tax Act:

“Where the total income of an assessee includes any income referred to in Section 68, 69, 69A, 69B, 69C, or 69D, and such income is not already accounted for or satisfactorily explained, the income tax payable on such income shall be calculated at the rate of 60% (plus surcharge and cess as applicable), without allowing any deductions or exemptions.”

16. Accordingly, since the amount of Rs. 32,33,32,516/-remains unexplained in the books of accounts, it will be taxed at the special rate prescribed under Section 115BBE, along with applicable surcharge and cess, without any deduction or set-off of losses. The interest u/s 234A, 234B, 234C of the Act is charged accordingly and given the credit of prepaid taxes as per the system. ITNS-150 is enclosed. Issued demand notice accordingly.”

23. Aggrieved by the said addition in the assessment order, the assessee filed appeal before the ld. CIT(A) who vide impugned order has deleted the said additions while allowing para 13, 14, 15 & 16 of the appeal and the relevant findings from para 14.21 to 16 are extracted below as under:

“14.21 Considering the above facts and circumstances and legal position of the case, the AO is directed to delete the following additions:

i. Ground of Appeal No. 13 – Addition of Rs. 31,37,286/- being estimated G.P. on sale

ii. Ground of Appeal No. 14 – Addition of Rs. 28,23,557/- being 50% of the GST

iii. Ground of Appeal No. 15 – Addition of Rs. 5,53,82,101/- being being estimated G.P. on sale

iv. Ground of Appeal No. 16 – Addition of Rs. 4,98,83,891/- being 50% of the GST

Thus, grounds of appeal no. 13, 14, 15 & 16 of the appellant are “allowed”.

15.1 In this ground, the appellant has stated that without prejudice the action of the A.O. in charging Tax us/ 115BBE of the I. T. Act 1961 is unjust, illegal, arbitrary and against the facts and circumstances of the case. I have perused the AO’s order, submission of the appellant, Form 35 and other material available on record.

15.2 It is noted that the AO made the addition u/s 69A and 690 of the Act, and as such, special tax rates as provided u/s 115BBE are applicable to the addition. Since, in this order, the addition u/s 69A and 690 of the Act has already been deleted, therefore, in this case the provisions of Section 115BBE of I. T. Act 1961 are not applicable.

Thus, ground of appeal no. 18 of the appellant is “allowed”.

16. In result, the appeal is “partly allowed.”

24. We have noticed that the assessment order dated 30.03.2025 against which appeal was filed before the ld. CIT(A), which has been considered and allowed by ld. CIT(A) vide impugned order, a writ has been filed in the Hon’ble High Court of Delhi bearing No. WP(C) 5131/2025. It is further noticed from the impugned order that the Hon’ble High Court has passed interim order holding that CIT(A)’s order would be subject to outcome of the writ petition, for limitation for issue of notice u/s 147 of the Act. Further the ld. CIT(A) can adjudicate the other matters for which the appeal has been filed. The ld. CIT(A) in the impugned order therefore held that ground Nos. 1, 2, 3 and 4 before him pertain to the issue pending before the High Court and therefore proceeded to decide only ground Nos. 4 to 18 raised before him which pertains to the addition made on merit.

23. We have noticed that the ground raised in the present appeal by the revenue pertains to the deleting the addition of Rs.21,21,45,680/- in u/s 69C of the Act on account of assessee’s failure to substantiate the genuiness of the purchase made from RCI Industries and Technologies Pvt. Ltd., deleting the addition of Rs.31,37,286/- and Rs.28,23,557/-made u/s 69A of the Act on account of unexplained money arising from bogus sales recorded by Ms/ Smita Global Pvt. Ltd. with RCI Industries.

25. Another ground pertains to deleting the addition of Rs.5,53,82,101/- and Rs. 4,98,43,891/- made u/s 69A of the Act on account of unexplained money arising from the bogus sales recorded by the assessee, M/s Bonlon Industries Limited with RCI Industries. We have further noticed that above three additions deleted by ld. CIT(A) which has been challenged before us in the appeal has been dealt with in the impugned order as ground Nos. 12, 13, 14, 15 & 16 which pertains to the addition of Rs.21,21,45,680/- u/s 69C of the Act and the addition of Rs.31,37,286/- and Rs.28,23,557/- made u/s 69A of the Act .

26. The ld. DR has raised the same arguments before us which was raised in ITA No.7987/Del/2025 stating that the ld. CIT(A) has wrongly deleted the addition made by the Assessing Officer. The ld. AR on the other hand has also raised the same arguments before us stating the impugned addition were made without any legal justification and the same has been rightly deleted by the ld. CIT(A) by meticulously examining the factual matrix and the material submitted by the assessee/appellant before the ld.CIT(A). To appreciate the finding returned by the ld. CIT(A) on ground Nos. 12, 13, 14, 15 & 16. The para 13.1 to 16 of the impugned order are relevant and extracted below as under:

“Ground of appeal No. 12

13.1 In these grounds, the appellant has agitated that action of the A.O. in making addition of Rs. 21,21,45,681/- u/s 69C of I. T. Act 1961 on account of purchases made from RCI Industries and Technologies Limited is unjust, illegal, arbitrary and against the facts and circumstances of the case. I have perused the Form 35, AO’s order, reply of the appellant, statement of facts and other material available on record.

13.2 I have considered the submission of the appellant.

On perusal of submission it is noted that In this case the notice issued under Section 148A(b) of the Income Tax Act, 1961, which states that the appellant company has availed of Input Tax Credit (ITC) of Rs. 76,59,66,694/-from M/s RCI Industries and Technologies Limited. It is seen that the total purchases made by the assessee from M/s RCI Industries and Technologies Limited during the Financial Year 2018-19 were only Rs. 21,21,45,681/-. Based on these purchases, the ITC claimed by the assessee was Rs. 3,81,86,222/-, which is 18% of the purchases is in compliance with the relevant provisions of the GST Act.

13.3 During the year under consideration the assessee made purchases of Rs. 21,21,45,681/- from RCI Industries which have been treated as non genuine purchases on various grounds including low gross profit/net profit, long standing creditors, cancellation of GST registration made by the GST department of RCI Industries w.e.f 01.07.2017, non furnishing of the information by RCI Industries in response to notice u/s 133(6) of I. T. Act 1961 including of transportation of goods.

RCI Industries GST Registration

13.4 It is seen that the Cancellation of GST registration of RCI was made by the GST Officer, Assistant Commissioner, Ward 201, Zone 11 Delhi as per notice dated 21.02.2023 and as per show cause registration was suspended w.e.f. 01.07.2017. Also the order for cancellation of GST registration of RCI was made on 02.03.2023. Thus the GST registration was not cancelled during the period relevant to F. Y. 2018-19 and was in force during the y ear under consideration when purchases were made.

13.5 The input tax credit was claimed by the app and was duly allowed by the GST department. The appellant could no t have been denied the input tax on retrospective cancellation of the supplier’s registration from where the appellant purchase goods. The appellant duly fulfilled the require me claiming input tax credit and was duly allowed by th department.

Long Outstanding Sundry Creditors

13.6 In Para 8 of the assessment order the A.O. has mentioned that the appellant has long standing creditors in the books of accounts and majority of creditors belong to RCI Industries. It is seen that for the year ending on 31.03.2017 the A.O. has mentioned that there were total creditors of Rs. 29.63 Crore and payable to RCI was shown as NIL therefore as per A.O.’s own admission there was no long outstanding creditor in respect of RCI Industries. For the year ending 31.03.2018 the A.O. has mentioned that out of the creditors of Rs. 25,27,18,547/-, the trade payable to RCI were Rs. 11,19,42,340/-. It is seen that these creditors were less than one year old as is apparent from the following details given in the balance sheet both for the year ending 31.03.2018 and 31.03.2019:

13.7 It is seen that the details of purchases and other expenses as per profit and loss account are as under:

13.8 The total purchases and expenses incurred by the appellant during the year ending 31.03.2018 were to the extent of Rs. 2,43,93,16,040/- giving average daily payment 66,83,058/- and the amount payable to RCI is only Rs. 11,19,42,340/- which is less than 17 days outstanding, which in any trade is not very long outstanding.

13.9 Similarly, the total purchases and expenses incurred by the assessee during the year ending 31.03.2019 were to the extent of Rs. 2,23,54,46,763/- giving average daily payment 61,24,512/- and the amount payable to RCI is only Rs. 7,54,39,459/- which is less than 13 days outstanding, which in any trade again isnot very long outstanding.

13.10 It is thus seen that the creditors are not outstanding for a long time and therefore cannot raise any doubt on the legitimacy of the transaction between the appellant and the RCI Industries. The outstanding creditors are only for 17 and 13 days in both the two years and therefore cannot be treated as non genuine business transactions on this account. In view of the various documents filed, it is established the appellant made genuine purchases and sales, backed by transport receipts, E-way bills. The payments for purchase have been made by normal banking channel and the payment against sales has again been received through normal banking channel. The account with RCI is fully reconciled and the balances with each other have been duly confirmed. Further the allegation that fake input tax credit has been availed, which is not there in the profit and loss account. In-fact the input and output tax credit is outside the profit and loss account and in these circumstances there is no escapement of income. Genuine transaction backed by voluminous documents as demonstrated above cannot be held to be non-genuine without any evidence and only on the basis of surmises and conjectures. The appellant duly filed copies of accounts with RCI showing that the credit transactions were of recent nature and these were not outstanding for long period.

13.11 It is further seen that the appellant made detailed submissions before the A.O. as per letter dated 26.03.2025 and submitted as under:

Purchase of Rs. 21,21,45,681/- from M/s RCI Industries and Technologies Limited

The assessee company purchased the goods of Rs. 21,21,45,681/- from RCI. Date-wise, Invoice wise quantity and amount-wise details are enclosed. In all the assessee paid GST of Rs. 3,81,86,223/- (IGST Rs. 3,44,57,494/-, SGST Rs. 18,64,364/- and CGST Rs. 18,64,364/-) to RCI on the purchases made. The total GST of Rs. 9,94,78,105/- (IGST, SGST & CGST) was charged from RCI on the sale made to them. Thus it cannot be said that output of Rs. 9,94,78,105/- was set off against the only input credit available of Rs. 3,81,86,223/-. Thus the balance output GST was adjusted against the purchases made from the other parties which was in the normal course of business carried on by the assessee. It may be mentioned that the complete records of the assessee were taken and seized by the GST department, Central GST New Delhi/DGGI Gurugram. Copy of letter dt. 24/09/2019 from GST department already placed on record at Page No. 42 and included in the paper book. Therefore, the available documents have been furnished. You may summon the documents seized on 24.09.2019 from the GST department and examine them with the help of the assessee to show that all the purchase and sale transactions with RCI were Bonafide and genuine. Without examination of the seized records no one can come to a conclusion that the transactions with RCI were bogus.

13.12 The A.O. was requested as per letter dated 26.03.2025 to summon the documents seized on 24.09.2019 from the GST department and examine them with the help of the assessee to show that all the purchase and sale transactions with RCI were bonafide and genuine, which the A.O. has failed to call for the complete record and his failure to do so, the purchase and sales cannot be treated as bogus. It was submitted before the A.O. that without examination of the seized records no one can come to a conclusion that the transactions with RCI were bogus. It is submitted that bogus purchases are entered into for reducing the profit. It involves obtaining bogus or inflated invoices from parties, who make bogus vouchers and charge nominal fees for these illegal services. Such is not the case with assessee for making purchases from RCI. Large amount of sales were made to RCI, which increases the income of the assessee. The sale is an income. No adverse inference on the facts and circumstances of the case called for.

Actual/physical movement of goods from the Premises of assessee company to the premises of M/s. RCI Industries and Technologies Limited

13.13 As seen from the aforesaid the Copies of E-way bills for movement of goods from assessee’s godown in Dilshad Garden, Delhi to PCI godown at Vish was Nagar, Delhi which is hardly 2.5 KM away have been placed on record with sale invoices. The goods were sent/delivered through local transport vehicles for which no GP/LP copy were required for the purpose. However for inter state sales the LP/GP copies were available but have been seized by GST department, Central GST New Delhi/ DGGI Guru gram.

Whether RCI Industries and Technologies Limited was involved in issuance as well as availing of bogus ITC Credit and as to why the transactions with them may not be treated as bogus transactions

13.14 So far the appellant is concerned no transactions with PCI is proved to be bogus. The appellant has sold/purchased goods to/from PCI, delivered through local transport in the case of intra-state sale within Delhi and inter-state sale/purchase through other transporter for which LP/GP copies were available, issued necessary invoices, sufficient stock was held, GST was charged and payment were received/made through bank transfers in the normal course of business carried on by the assessee. These were all genuine transactions were being entered with PCI since last so many years and were accepted in the past. If the output GST has been adjusted through input credit available, the relevant transactions would not ceased to be bogus transactions. It is seen that a request was made to summon and examinePCI to confirm that all the transactions made by the assessee company with them are genuine business transactions entered into the normal course of business carried on by the assessee company, which was not acceded to by the A.O. and on that basis no adverse inference could have been taken. On the basis of certain reports that the transactions with PCI are bogus, without examination and necessary inquiry, the genuine transactions cannot be treated as bogus.

Documents filed by the RCI

13.15 It is further seen that the documents given to the assessee company by PCI were also uploaded containing 328 pages vide online response filed on 18.03.2025 which contains the point wise reply to notice u/s 133(6) of PCI Industries along-with ITP Ack., Auditor Peport, Audited Financial Statements, Ledgers of Smita Global in the books of PCI, Ledgers of Bonlon Steels Pvt. Ltd. (Name changed to Bonlon Industries Ltd.) in the books of PCI, Bank Statements of PCI highlighting payments made, Copies of Sale & Purchase invoices along with Bilty and GR. As the RCI has gone into Insolvency Resolution Process and Resolution Professional (RP) could not upload the various documents. In these circumstances the appellant uploaded these documents for verification. The A.O. has not pointed out any discrepancy in these documents. In-fact no further enquiry or verification was done by the A.O.

13.16 It is seen that the purchases made by the assessee from RCI are the sales made by them to the appellant, which have been fully reconciled. Similarly sales made by the assessee to the RCI is purchase by them from the assessee, which again fully reconciles. When purchase and sales made from and to with RCI fully reconciles with the appellant and RCI, they cannot be considered as bogus. Complete quantity-wise details have been maintained which have been placed on record. The A.O. has not pointed out any specific entry of purchase and sales which is not reconcilable either with assessee company and with RCI. When this is so, sales and purchases to or from RCI cannot be considered as bogus as the same represents the purchase and sales of the assessee company.

Article 14 of the Indian Constitution, which guarantees equality before the law and equal protection of the laws, is applicable in income tax cases, meaning that taxation laws and their application must be fair and not discriminatory.

It is seen that under similar circumstances purchases made from RCI Industries accepted as genuine and not bogus in other cases.

Order dated 23.03.2023 in case of Captain Industries, C-6B/11, Janak Puri, New Delhi – 110058, assessed under PAN AAFFC0006K by the A.O. ACIT, Circle 49(1), Delhi

13.17 In this connection reference has been made to the following documents in the above case wherein similar Purchase/Transactions made from RCI Industries was accepted by the department:

i. Copy of the notice u/s 148A(b) of I. T. Act 1961 dated 16.03.2022 issued with the approval of PCIT, Delhi-10 to show-cause as to why the transaction of Rs. 65,75,38,711/- which includes purchases of Rs. 51,77,37,646/- from RCI Industries should not be treated as bogus transaction and assessment re-opened.

ii. Order u/s 148(d) of I. T. Act 1961 dated 29.03.2022 for issue of notice u/s 148 of I. T. Act 1961 with again Prior approval of PCIT Delhi-10

when the books of accounts and stock tally have been maintained no addition/disallowance is called for. In this case it was held:

16. In the instant case, we find that the Revenue in fact viewed the position as warranting a 100% disallowance of the expenses. In the context of the Impugned Order, that is understandable since one could question if there is no cogent and convincing evidence at all. A Division Bench of this Court did not consider that appeal to be worthy of consideration. In Nikunj, the ITAT reversed the entire disallowance on the part of the Assessing Officer and the CIT-A. But purporting to adopt Nikunj, in the instant case, the ITAT fell short of analysing if the disallowance of 10% was reasonable and justifiable.

17. This very bench had occasioned to deal with a similar issue in the case of Principal Commissioner of Income-tax-1 Vs. SVD Resins & Plastics (P.) Ltd. 2 , where, repelling a challenge by the Revenue, to a decision of the ITAT curtailing the disallowance of allegedly bogus purchases to 12.5%, the following observations were made:

“11. We may observe that in the facts of the present case, the basic premise on the part of the A.O. so as to form an opinion that the disputed purchases were not having nexus with the corresponding sales, appears to be not correct. It is seen that what was available with the department was merely information received by it in pursuance of notices issued under section 133(6) of the Act, as responded by some of the suppliers. However, an unimpeachable situation that such suppliers could be labeled to be not genuine qua the assessee or qua the transaction entered with the assessee by such suppliers, was not available on the record of the assessment proceedings. It is an admitted position that during the assessment proceedings, the assessee filed all necessary documents in support of the returns on which the ledger accounts were prepared, including confirmation of the supplies by the suppliers, purchase bills, delivery bank statements etc. to justify the genuineness of the purchases, however, such documents were doubted by the AO on the basis of general information received by the AO from the Sales Tax Department. In our opinion, to wholly reject these documents merely on a general information received from the Sales Tax Department, would not be a proper approach on the part of the AO, in the absence of strong documentary evidence, including a statement of the Sales Tax Department that qua the actual purchases as undertaken by the assessee from such suppliers the transactions are bogus. Such information, if available, was required to be supplied to the assessee to invite the response on the same and thereafter take an appropriate decision. Unless such specific information was available on record, it is difficult to accept that the AO was correct in his approach to question such purchases, on such general information as may be available from the Sales Tax Department, in making the impugned additions. This for the reason that the same supplier could have acted differently so as to generate bogus purchases qua some parties, whereas this may not be the position qua the others. Thus, unless there is a case to case verification, it would be difficult to paint all transactions of such supplier to all the parties as bogus transactions.

12. In our opinion, a full addition could be made only on the basis of proper proof of bogus purchases being available as the law would recognise before the AO, of a nature which would unequivocally indicate that the transactions were wholly bogus. In the absence of such proof, by no stretch of imagination, a conclusion could be arrived, that the entire expenditure claimed by the petitioner qua such transactions need to be added, to be taxed in the hands of the assessee.

13. In a situation as this, the A.O. would be required to carefully consider all such materials to come to a conclusion that the transactions are found to be bogus. Such investigation or enquiry by the AO also cannot be an enquiry which would be contrary to the assessments already undertaken by the Sales Tax Authorities on the same transactions. This would create an anomalous situation on the sale-purchase transactions. Hence, in our opinion, wherever relevant any conclusion in regard to the transactions being bogus, needs to be arrived only after the A.O. consults the Sales Tax Department and a thorough enquiry in regard to such specific transactions being bogus, is also the conclusion of the Sales Tax Department. In a given case in the absence of a cohesive and coordinated approach of the A.O. with the Sales Tax Authorities, it would be difficult to come to a concrete conclusion in regard to such purchase/sales transactions being bogus merely on the basis of general information so as to discard such expenditure and add the same to the assessee’s income.

14. Any half hearted approach on the part of the AO to make additions on the issue of bogus purchases would not be conducive. It also cannot be on the basis of superficial inquiry being conducted in a manner not known to law in its attempt to weed out any evasion of tax on bogus transactions. The bogus transactions are in the nature of a camouflage and/or a dishonest attempt on the part of the assessee to avoid tax, resulting in addition to the assessee’s income. It is for such reason, the approach of the AO is required to be well considered approach and in making such additions, he is expected to adhere to the lawful norms and well settled principles. After such scrutiny, the transactions are found to be bogus as the law would understand, in that event, they are required to be discarded by making an appropriate permissible addition

16. The assessee has happily accepted such finding as this has benefited the assessee, looked from any angle. However, in a given case if the Income-tax Authorities are of the view that there are questionable and/or bogus purchases, in that event, it is the solemn obligation and duty of the Income-tax Authorities and more particularly of the A.O. to undertake all necessary enquiry including to procure all the information on such transactions from the other departments/authorities so as to ascertain the correct facts and bring such transactions to tax. If such approach is not adopted, it may also lead to assessee getting away with a bonanza of tax evasion and the real income would remain to be taxed on account of a defective approach being followed by the department.”

The aforesaid analysis would squarely apply to the facts of the instant case. Not only has the Assessing Officer not conducted the exercise as expected of him, the CIT-A has effected a summary measure of disallowing 10% of the expenses and the ITAT has been happy to endorse the same as an equitable middle ground. Such an approach cannot be endorsed as a process known to law to disallow expenses on the premise of their being bogus.

Another decision of a Division Bench of this Court in the case of Principal Commissioner of Income-tax Vs. Shapoorji Pallonji and Co. Ltd. 3 is noteworthy. The relevant portions are extracted below:

17. On further appeal before the Tribunal by the respondent – assessee, Tribunal held as under: “16. Having heard rival submissions, we are of the view that there is merit in the submissions made by the assessee. We notice that the AO has simply relied upon the Sales Tax Department report about suspicious dealers, without making independent inquiries. On the contrary, the assessee has furnished all the materials to prove the genuineness of purchases and the AO has failed to show that those materials were bogus. Under these set of facts, we are of the view that there is no justification in doubting the genuineness of purchases made by the assessee. Further, these alleged bogus purchases forms a minor fraction of total volume of the assessee company and it is stated that there is no day to day involvement of the management. It was further submitted that the assessee is having strict internal controls. Hence we are of the view that the AO has not made a proper ground in support of the disallowance. Accordingly we set aside the order passed by Ld. CIT (A) on this issue and direct the AO to delete the addition of Rs.3,23,944/-.

18. Thus, we find that according to the Tribunal the assessing officer had merely relied upon information received from the Sales Tax Department, Government of Maharashtra without carrying out any independent enquiry. Tribunal had recorded a finding that assessing officer had failed to show that the purchased materials were bogus and held that there was no justification to doubt genuineness of the purchases made by the respondent – assessee.

19. We are in agreement with the views expressed by the Tribunal. Merely on suspicion based on information received from another authority, the assessing officer ought not to have made the additions without carrying out independent enquiry and without affording due opportunity to the respondent – assessee to controvert the statements made by the sellers before the other authority. Accordingly, we do not find any good ground to entertain this question for consideration as well.” [Emphasis Supplied]

23. The Supreme Court dismissed the Special Leave Petition challenging the aforesaid decision. In the instant case, the onus of bringing the purchases by the Appellant-Assessee under cloud was on the Respondent-Revenue, which has not discharged this burden in the first place. Apart from the inputs being received from the investigation wing, there is nothing concrete in the material on record that was used to confront the Appellant-Assessee. If the counterparties in these purchases could not be produced years later, simply adopting a 10% margin for disallowance, without any cogent or convincing evidence, in our opinion, would be unreasonable and arbitrary. It is repugnant for the ITAT to uphold such an addition of 10% of the allegedly bogus purchases to the income of the Appellant-Assessee, despite returning a firm finding that the AO Order was untenable not being backed by cogent and convincing evidence.

14.16 No addition is required to be made without appreciating the facts of the case, for the transactions of purchase and sale to RCI Industries. The assessee company has made Purchases and sales which are backed by proper purchase and sales bills and these purchases and sales have been confirmed by RCI Industries. The transactions were not entered into for decreasing the profit. No fake invoices have been taken/issued for availing input tax credit. The assessee company has established one to one nexus/link between the purchase and sales as shown in the Books of account of M/s RCI Industries Pvt. Ltd. Each purchase has corresponding sales mentioning the same quantity in purchase and sales. The purchases made were sold with profit margin then available. One to one reconciliation of purchases with sales has been established. Only the profit embedded in each amount of purchase and sales could be taxed, which has already been disclosed in the books of accounts. When the sales are treated/considered/accepted genuine and not bogus the corresponding purchase should have been held in-genuine or bogus and should have been accepted. No sales could be made without any purchase. In this connection reference may be made to the decision of the Jaipur Bench of ITAT in 31 DTR 456 in the case of Nisraj Real Estate wherein it was held that unverified purchases made by assessee could not be treated as unexplained expense u/s 69C and no addition can be made thereof u/s 69C proviso there under – as once sales were made by assessee, purchases were obviously made. In view of this no addition is called for as no income has escaped assessment.

Books of accounts not rejected – No addition

14.17 It is submitted that no addition on estimation basis without Rejecting Books of Accounts can be made by the A.O. This has been so held by the Jurisdictional Hon’ble Delhi High Court in the case of PCIT Vs Forum Sales Pvt. Ltd. in Appeal Number: ITA 862/2019, dated 01/03/2024 for A.Y. 2013-14. The High Court underscored that for any addition to be made on an estimation basis, rejecting the books of accounts is sine qua non. This principle is established to ensure a transparent and precise assessment process, avoiding arbitrary pick-and-choose methods that could lead to incomplete and erroneous computation of taxable income.

14.18 Further reliance has been placed on the judgement of Delhi ITAT in the case of Home Developers Project Pvt. Ltd. Vs DCIT in Appeal Number: ITA No. 390/Del/2019 dated 26/07/2023 for A. Y. 2012-13, wherein the Hon’ble ITAT in Para 23 of the order has held as under:

In our considered opinion without rejecting the books of account the AO has grossly erred in estimating the profit which is against the ratio laiddown by the Hon’ble High Court of Delhi in the case of National Industrial Corporation Limited 258 ITR 578. Since the addition is solely based on estimation without rejecting the books of accounts, we do not find any merit in the impugned addition the AO is directed to delete the same.

14.19 The appellant has duly filed the GST/Sales tax returns and other documents which establishes the genuineness of the transactions of sale. Books of accounts of the assessee have not been rejected. Similarly the sales have not been doubted. Purchase and sale invoices have been filed backed by stock tally and GST returns, which would indicate that the purchase and sales were genuinely made. The A. O. has accepted the findings of the sales tax department without conducting any independent enquiry. Input tax credit was claimed by the assessee on the purchases made from the RCI Industries. Output tax was paid on the sales made to RCI Industries. In a trade, trading is permissible and the profit shown on such sales is part of the trading results. The assessee is public limited company and the shares are quoted on the Bombay Stock Exchange. The trading done by the appellant did not result in revenue losses. In a trading business goods required by either party for its business are either purchased or sold at the price agreed upon. It is for an assessee and its supplier/customer when to buy any commodity from either of them at the rates agreed upon. There is no charge that over invoicing or under invoicing was undertaken to generate bogus loss. No sales could have been effected without making any purchases. Sales figure having been accepted, there is no justification in not accepting the purchases.

14.20 Further during the course of assessment proceedings the A.O. has issued the notice u/s 133(6) of the I. T. Act 1961 to RCI Industries and Technologies Ltd. dated 25.02.2025. A response to this notice was filed by the RCI before the A.O. on 25.03.2025. This has been duly mentioned in Para 11.6 of the Assessment order by the A.O. The A.O. has disallowed the purchases amounting to Rs. 21,21,45,681/- made from RCI Industries & Technologies Ltd., holding the same as non-genuine primarily on the basis of the cancellation of GST registration of the supplier and lack of certain documents filed in response to notice u/s 133(6) of I. T. Act 1961. It is seen that in the reply to notice the RCI has clearly mentioned the company is under Corporate Insolvency Resolution Process (CIRP), and hence, the availability of records is constrained due to the suspension of its board of directors and lack of cooperation from past employees. It is seen that nothing prevented the A.O. from issuing a further reminder or notice under section 133(6) to the Resolution Professional or seeking additional details through alternate channels, such as the Insolvency and Bankruptcy Board of India (IBBI) or the National Company Law Tribunal (NCLT). The AO chose not to make further inquiries despite having statutory powers available under the Act. The ledger accounts of RCI Industries & Technologies Ltd., as maintained and produced by the appellant, clearly reflect the transactions in question. These ledger accounts match the appellant’s books and show the purchase amounts along with corresponding payments made via banking channels. The matching of ledger balances is a crucial piece of corroborative evidence establishing the genuineness of the transactions, especially in cases where third-party documentation may be partially unavailable due to CIRP proceedings. RCI in response to notice u/s 133(6) of I. T. Act 1961 have duly furnished all the relevant documents in support of the purchases from RCI Industries & Technologies Ltd., including copy of ITR filed by RCI for A. Y. 2019-20, auditor’s report, complete audited financial statement alongwith notes to accounts, confirmation of accounts / ledger accounts of Bonlon Industries Ltd. and Smita Global Pvt. Ltd. in the books of RCI, Bank statements showing receipts and payments, copies of sales and purchase invoices along-with bilty/LR. It is incorrect to state that no transportation records have been provided. The RCI as well as appellant have duly submitted copies of LRs/bilty and E-way bills evidencing movement of goods. Non-availability of transporter details from the supplier’s end (RCI), especially given its status under CIRP, should not be held against the appellant when the appellant itself has provided such documentation. The fact that the supplier’s GST registration was cancelled suo moto by the GST Department, and retrospectively, does not automatically render the transactions void or fictitious. Purchases were made during the period when the supplier was active, and payments were duly made through banking channels. It is seen that mere GST registration cancellation cannot be a ground to treat the purchases as bogus if the buyer has discharged its burden by providing evidence of genuine transactions. The Cancellation of GST registration of RCI was made by the GST Officer, Assistant Commissioner, Ward 201, Zone 11 Delhi as per notice dated 21.02.2023 and registration was suspended from 21.02.2023 retrospectively from 01.07.2017. Also the order for cancellation of GST registration of RCI was made on 21.02.2023. Thus the GST registration was not cancelled during the period relevant to A. Y. 2019-20 and was in force.

14.21 Considering the above facts and circumstances and legal position of the case, the AO is directed to delete the following additions:

i. Ground of Appeal No. 13 – Addition of Rs. 31,37,286/-being estimated G.P. on sale

ii. Ground of Appeal No. 14 – Addition of Rs. 28,23,557/-being 50% of the GST

iii. Ground of Appeal No. 15 – Addition of Rs. 5,53,82,101/- being estimated G.P. on sale

iv. Ground of Appeal No. 16 – Addition of Rs. 4,98,83,891/- being 50% of the GST

Thus, grounds of appeal no. 13, 14, 15 & 16 of the appellant are “allowed”.

27. On perusal of the finding returned by the ld. CIT(A) and considering the arguments raised by both the parties before us, we are of the considered opinion that the finding returned by us in ITA No. 7987/Del/2025 (supra) wherein the similar addition has been deleted by the ld. CIT(A) and the said order has been confirmed by us, shall mutatis mutandis apply to finding returned by ld. CIT(A) in this appeal also. For these reasons, the deletion of the addition made by Assessing Officer and the impugned order passed by ld. CIT(A) is confirmed. The ground raised by the Revenue before us are accordingly dismissed.

CO No. 7/Del/2026

28. The assessee has raised following grounds in the Cross Objection:

“1. That on the facts and circumstances of the case the CIT (Appeal) has erred in not disposing of the following additional ground of appeal raised by the appellant: –

19. That on the facts and circumstances of the case the jurisdictional assessing officer A.O. DCIT Circle 4(2), New Delhi has erred on the facts and in law issuing notices u/s 148 and 148A of the I. T. Act 1961, specifically after the introduction of Section 151A of I. T. Act 1961 and issuance of CBDT Notification No. 18/2022 dated 29.03.2022, resulting in framing the illegal assessment and is thus required to be quashed in view of the recent decision of the Hon’ble Supreme Court in the case of ADIT vs. Deepanjan Roy dated 16.07.2025 wherein it has been held that issue of Notice u/s 148 in faceless manner is mandatory.

2. Action of the CIT (A) in confirming the action of the A.O. who has failed to verify the correctness of the information received from the insight portal and has failed to showcase as to how information suggests that the income has escaped assessment making the assessment as illegal, arbitrary and against the facts and circumstances of the case (As per Ground of Appeal No. 5 before the CIT (A)).

3. The impugned assessment order is bad in law as the same has been mechanically passed by the A.O. and does not provide any cogent explanation for making additions to the income of the appellant and the A.O. has failed to consider the replies of the appellant during the course of reassessment proceedings and also in the proceedings u/s 148A(b) of I. T. Act 1961 and has mechanically passed the impugned assessment order (As per Ground of Appeal No. 7 and 8 before the CIT (A))

4. The reassessment proceedings initiated by the A.O. based on information received from the insight portal is bad in law as the same is a borrowed satisfaction and no independent inquiry has been made.”