Dear Friends

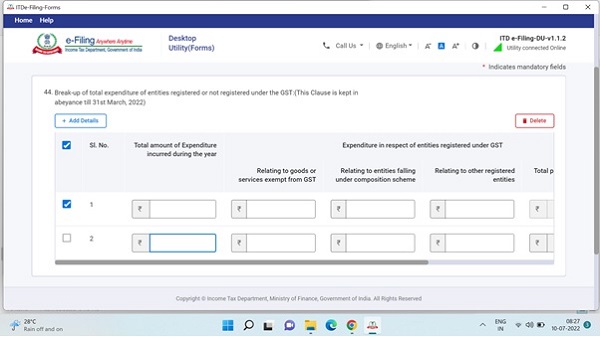

The Clause 44 of the Form 3CD is effective for Assessment Year 2022-23 i.e. for the Financial Year 2021-22 because the compliance of this clause was kept in abeyance till 31/03/2022 but for all the reports submitted after that date the clause is mandatory.

Since the audits for the Financial Year 2021-22 are under process hence we should study how to report and comply this clause and how the Assesssee under audit will submit the data under this clause.

The primary duty of submission of the details is of Auditee and for verification of the information supplied under this clause can be verified form the GSTR-2A, GSTR-2B, AIS and other records available with the dealer.

Most of the information required for this clause is already available with the Law makers in the form of GSTR-2A and AIS and what is the use of this information in Form 3CD is better known to the lawmakers but since the clause is there hence the Assesssee and Auditor has to follow and comply it.

Let us see an Example with certain notes: –

S.NO. |

Total Amount of Expenditure incurred during the year |

Expenditure in respect of entities registered under GST |

Expenditure relating to entities not registered under GST |

|||

Relating to Goods or Services exempt form GST |

Relating to the Entities falling under Compositions Scheme |

Relating to other Registered Entities |

Total Payments to Registered Entities |

|||

(1) |

(2) |

(3) |

(4) |

(5) |

(6) |

(7) |

1. |

22355475.00 |

199660.00 |

177040.00 |

19488780.00 |

19865480.00 |

2489995.00 |

WORKING AND CALCULATION

TRADING AND PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDING ON 31-3-2022

| PARTICULARS | AMOUNT | PARTICUALS | AMOUNT |

| Opening Stock | 720000.00 | Sales | 22345000.00 |

| Purchases | 19676875.00 | Closing Stock | 845000.00 |

| Gross Profit | 2793125.00 | ||

| Total | 23190000.00 | Total | 23190000.00 |

| Salary | 555000.00 | Gross Profit | 2793125.00 |

| Travelling | 234500.00 | ||

| Office Expenses | 365600.00 | ||

| Repair and Maintenance | 117600.00 | ||

| Interest | 305600.00 | ||

| Local Conveyance | 34500.00 | ||

| Festival Expenses | 132400.00 | ||

| Commission | 75000.00 | ||

| Business Promotion | 123400.00 | ||

| Depreciation | 76560.00 | ||

| Net Profit | 772965.00 | ||

| Total | 2793125.00 | Total | 2793125.00 |

CALCULATION FOR PRESENTATION IN CLAUSE 44 OF FORM 3CD

S.NO. |

Total Amount of Expenditure incurred during the year |

Expenditure in respect of entities registered under GST |

Expenditure relating to entities not registered under GST |

|||

Relating to Goods or Services exempt form GST |

Relating to the Entities falling under Compositions Scheme |

Relating to other Registered Entities |

Total Payments to Registered Entities |

|||

(1) |

(2) |

(3) |

(4) |

(5) |

(6) |

(7) |

Purchases |

19676875.00 |

0.00 |

120340.00 |

18456000.00 |

18576340.00 |

1100535.00 |

Salary |

555000.00 |

0.00 |

0.00 |

0.00 |

0.00 |

555000.00 |

Travelling & Petrol Expenses |

234500.00 |

176500.00 |

0.00 |

0.00 |

176500.00 |

58000.00 |

Office Expenses |

365600.00 |

5600.00 |

56700.00 |

75600.00 |

137900.00 |

227700.00 |

Repair and Maintenance |

117600.00 |

0.00 |

0.00 |

45780.00 |

45780.00 |

71820.00 |

Interest |

305600.00 |

0.00 |

0.00 |

0.00 |

0.00 |

305600.00 |

Local Conveyance |

34500.00 |

17560.00 |

0.00 |

0.00 |

17560.00 |

16940.00 |

Festival Expenses |

132400.00 |

0.00 |

0.00 |

0.00 |

0.00 |

132400.00 |

Commission |

75000.00 |

0.00 |

0.00 |

75000.00 |

75000.00 |

0.00 |

Business Promotion |

123400.00 |

0.00 |

0.00 |

101400.00 |

101400.00 |

22000.00 |

Capital Expenditure- Car |

735000.00 |

0.00 |

0.00 |

735000.00 |

735000.00 |

0.00 |

Reporting Amount |

22355475.00 |

199660.00 |

177040.00 |

19488780.00 |

19865480.00 |

2489995.00 |

Depreciation |

76560.00 |

NA |

NA |

NA |

NA |

NA |

One can give consolidate figures for all the expenditure under this clause or one can give Revenue and Capital Expenditure under the serial Number 1 and 2 but it should be noted there is no place in the utility to mention the expenditure under the head Revenue and Capital Expenditure with name. Hence consolidate figure can also serve the purpose.

Further in case of Depreciation, In my opinion there is no need to include figure of depreciation in these figures because in that case further bifurcation is not possible but if you choose to include the figure of depreciation then use your discretion and ask the client to submit the details in such manner.

This is illustrative description of the figures to be reported in the Clause 44 of Form 3CD based on certain opinion of the Author of this Article. The comments for improvement of the study are invited to make it more useful.

Author Bio

Well explained. Thanks

what is the treatment of GST not taken on the expenses like Bank Charges gst not taken.

and what is the treatment of block credit u/s 17(5) such as car purchase

what is the treatment of Expenses of RCM ?

Dear Sir,

Thank you for posting illustration .

In para 82.3 of Guidance Note on Tax Audit under Section 44AB of the Income Tax Act, 1961 AY 2022-23, has mentioned not to report remuneration to employees need not to reported under this clause in any of the columns

from 3 to 7. Can you please explain reason for reporting salaries under column 7 of your illustration

Goods purchased are routed through Inventory and Charged to Expense on the basis on Consumption. then how to compile the GST amount on expenditure charged to expense.

How to get the excel file that you explained in the video

PLEASE SHARE BRIEF EXPLAIN ON ASHWINJAIN144@GMAIL.COM

Where to Show Interest on TDS , Late Filing Fees for TDS , Income Tax ( current year ) , Prior period tax , Preliminary Expenses written off , audit fees payable , legal expense incurred for filing Fees of MCA returns in case of Tax Audit of Private Limited Company

Where to show Import purchases and Purchase attract RCM under GST ACT

Very Well Explained

Clause clarified in very easiest manner and very informative

TAX PAYERS WILL HAVE WORK HARD TO GET THE DATA. THANKS FOR THE INFORMATION

is it so easy to bifurcate the expenditure like this from the books of accounts or tally software?

good informative