Case Law Details

Sridevi Mogulla Vs ITO (ITAT Hyderabad)

Hyderabad ITAT: Reassessment Beyond Three Years Invalid Where Actual Escaped Income Is Below ₹50 Lakh

The Hyderabad ITAT quashed the reassessment proceedings holding that the validity of a notice under section 148 issued beyond three years must be tested on the basis of the actual income alleged to have escaped assessment and not on inflated or incorrect figures adopted by the Assessing Officer. Where the actual cash deposits were less than ₹50 lakh, the extended limitation under section 149(1)(b) was unavailable, rendering the notice issued after three years time-barred and without jurisdiction.

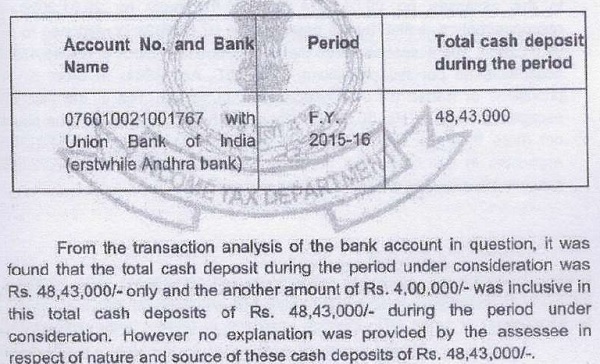

In the present case, the Assessing Officer initiated proceedings under section 148A by alleging cash deposits of ₹52.43 lakh, comprising two entries of ₹48.43 lakh and ₹4 lakh. The assessee, in reply to the show-cause notice under section 148A(b), demonstrated through the bank statement that the ₹4 lakh was already included in the figure of ₹48.43 lakh, and therefore the actual cash deposits were below ₹50 lakh. Despite this, the Assessing Officer proceeded to issue notice under section 148 after the expiry of three years from the end of AY 2016-17. Significantly, during the reassessment itself, the Assessing Officer accepted that the actual cash deposits were only about ₹48.43 lakh, thereby confirming the factual error in the reopening proceedings.

The Tribunal held that once the assessee had brought the correct factual position to the Assessing Officer’s notice before passing the order under section 148A(d), the Assessing Officer could not rely upon an incorrect and inflated figure merely to invoke the extended ten-year limitation. The Tribunal followed its earlier decision in Adilakshmi Vangala and also relied on the principles laid down by the Madras High Court and Bombay High Court, holding that the limitation period cannot be enlarged on the basis of non-existent or erroneous facts. Accordingly, the notice issued under section 148 and the consequential reassessment order were quashed as barred by limitation, and the remaining grounds were rendered infructuous.

Cases Discussed

- Adilakshmi Vangala, Hyderabad vs. ITO, Ward-6(1), Hyderabad (ITAT Hyderabad), ITA.No.2222/Hyd./2025

- Krishna Reddy Venkatsan, Tiruvallur vs. ITO, Tiruvallur (Madras High Court)

- Naresh Balachandra Rao Shinde vs. ITO (Bombay High Court)

- ARB Hotels Resorts (P.) Ltd. vs. Pr. CCIT (Allahabad High Court)

- CIT vs. Vegetable Products Ltd. (Supreme Court of India), (1973) 88 ITR 192 (SC)

FULL TEXT OF THE ORDER OF ITAT HYDERABAD

This appeal by the Assessee is directed against the order dated 29.12.2025 of the Ld. CIT(A)-National Faceless Appeal Centre [in short “NFAC”], Delhi, for the assessment year 2016-2017.

2. The Assessee has raised the following grounds of appeal:

1) The Ld. Assessing Officer erred in law and on facts in assuming jurisdiction under Section 147 by passing order under Section 148A(d) dated 28.03.2023 and issuing notice under Section 148 dated 29.03.2023 without complying with the mandatory provisions, procedure and limitations of Sections 147, 148, 148A and 149, and the Ld. Commissioner of Income Tax (Appeals) erred in not adjudicating this foundational jurisdictional defect and in sustaining the reassessment proceedings by way of set aside for fresh examination.

2) The Ld. Assessing Officer initiated reassessment for A. Y. 2016-17 beyond three years though the alleged escaped income as per impugned assessment order was below Rs. 50,00,000/ -, and the Ld. Commissioner of Income Tax (Appeals) erred in not holding the notice under Section 148 and the reassessment to be time-barred under Section 149(1)(a).

3) That the reassessment notice issued beyond the period of three years from the end of AY 2016-17 is time-barred under Section 149(1)(a), and the extended limitation under clause (b) (ten years) is inapplicable since the alleged escaped income Rs.40,39,300/ – as per the impugned order is far below Rs.50 lakhs, therefore, the proceedings are wholly without jurisdiction.

4) The Ld. Assessing Officer wrongly treated Rs.52,43,400/ – as escaped income by double-counting cash deposits under AIR-001 and CIB-410 for one bank account instead of the actual Rs.48,43,000/ -, and the Ld. Commissioner of Income Tax (Appeals) erred in not deciding this jurisdictional factual error under Section 149(1)(b).

5) The Ld. Assessing Officer failed to follow the substituted scheme of Sections 147 to 151, the law laid down in Union of India v. Ashish Agarwal and CBDT Instruction No.01/ 2022, and the Ld. Commissioner of Income Tax (Appeals) erred in not quashing the reassessment as without jurisdiction for non-compliance with the amended legal regime.

6) The Ld. Assessing Officer made an unsustainable addition of Rs.40,39,300/- under Section 69A read with Section 115BBE without proper enquiry into the explained sources, and the Ld. Commissioner of Income Tax (Appeals) erred in not deleting the addition despite the submission of detailed evidence of loans recovered, family support, agricultural income, rental income and cash redeposits.

7) Without prejudice, the Ld. Assessing Officer erred in treating Rs.40,39,300/- as unexplained instead of restricting any possible adverse inference, if at all, to Rs.21, 79,300/ – alone, and the Ld. Commissioner of Income Tax (Appeals) erred in not correcting this patent mistake in computation and appreciation of facts.

8) The Ld. Assessing Officer completed assessment under Section 147 read with Section 144 in violation of natural justice by issuing inadequate and selective notices under Section 133(6) to only 4 out of 20 identified persons with an unreasonably short response time of 3 days, and by not fairly considering the appellants written submissions and documents, and the Ld. Commissioner of Income Tax (Appeals) erred in not so holding.

9) The Ld. Commissioner of Income Tax (Appeals) wrongly invoked the proviso to Section 251(1)(a) to set aside and remand the case instead of deciding the legal and jurisdictional grounds on merits, thereby improperly sustaining an invalid reassessment by the Ld. Assessing Officer along with consequential interest and penalty exposure.

10) The Ld. Assessing Officer and the Ld. Commissioner of Income Tax (Appeals) failed to appreciate the appellants personal circumstances, educational purpose of funds for her sons USA studies, and consistent past tax compliance, and the appellant prays for all consequential reliefs as may be necessary in the interest of justice.

11) The appellant craves leave to add, amend, alter OR withdraw any ground and to seek any consequential OR incidental relief that the Honourable Tribunal may deem fit in the facts and circumstances of the case.

3. In ground no .3 the assessee has challenged the validity of the notice issued by the Assessing Officer u/ sec. 148 of the act being barred by limitation u/sec.149(1)(a) of the Income Tax Act [in short “the Act], 1961. Since this legal issue raised in ground no.3 is purely legal in nature and goes to the root of the matter therefore, we first take up ground no.3 for hearing and adjudication.

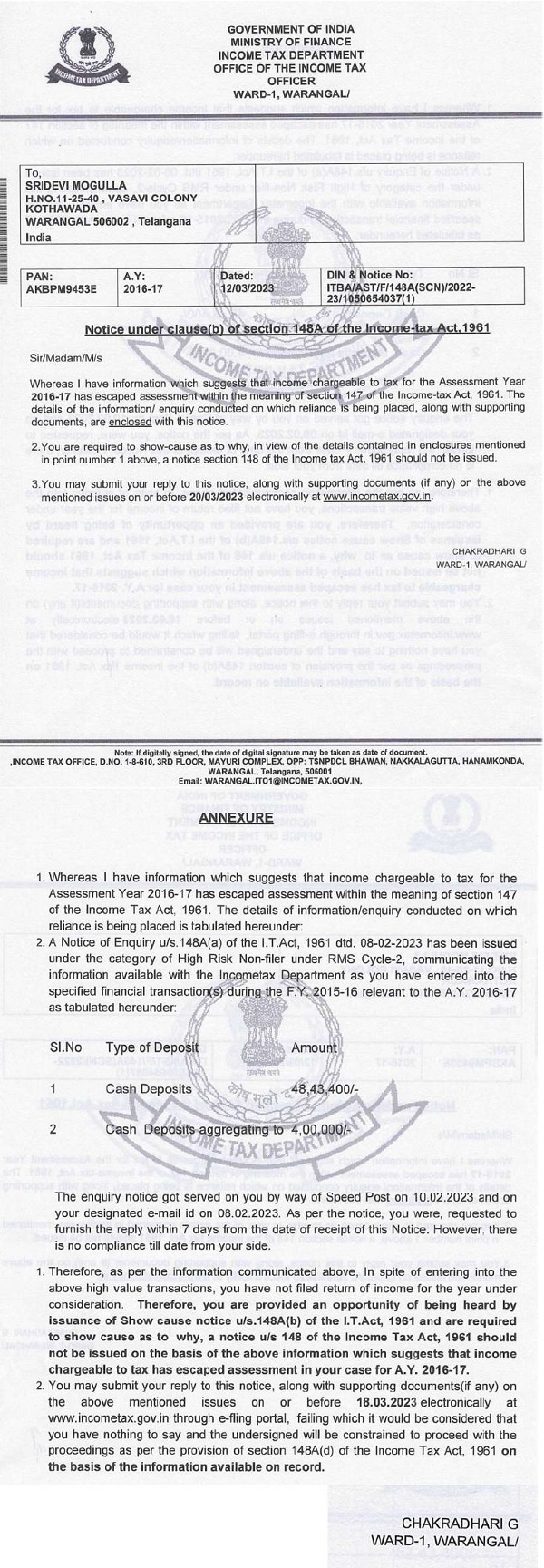

4. The learned Authorised Representative of the Assessee has submitted that the Assessing Officer has issued show cause notice u/sec.148A(b) of the Act dated 12.03.2023 proposing the reopening of the assessment to re-assess the income assessable to tax escaped assessment amounting to Rs.52,43,400/-. The assessee has filed reply to the show cause notice issued and explained that the total cash deposit in the bank account is only Rs.48,43,400/- and not Rs.52,43,400/- and therefore, the alleged income escaped assessment is below Rs.50 lakhs. The learned Authorised Representative of the Assessee has submitted that the assessee has thus objected to the reopening of the assessment as barred by limitation under the provisions of sec.149(1)(a) of the Act. He has then referred to the order passed by the Assessing Officer u/sec.148A(d) on 28.03.2023 and submitted that the Assessing Officer has ignored the said reply of the assessee that the income escaped assessment is less than Rs.50 lakhs and passed the order u/sec.148A(d) of the Act and thereafter issued notice u/sec.148 on 29.03.2023. The learned Authorised Representative of the Assessee has then referred to the bank account statement as well as the assessment order passed by the Assessing Officer and submitted that in the assessment order the Assessing Officer has accepted this fact that the total cash deposit in the bank account is only Rs.48,43,000/- and the amount of Rs.4 lakhs was inclusive in this deposit of Rs.48,43,000/-. Thus, the learned Authorised Representative of the Assessee has submitted that once the actual cash deposit in the bank account is only Rs.48,43,000/- which is less than Rs.50 lakhs then the reopening by issuing a notice after three years from the end of the assessment year is barred by limitation. In support of his contention, he has relied upon the order of this Tribunal dated 17.04.2026 in ITA.No.2222/Hyd./ 2025 in the case of Adilakshmi Vangala, Hyderabad vs. ITO, Ward-6(1), Hyderabad.

5. On the other hand, the learned DR has submitted that at the time of issuing the show cause notice as well as reopening of the assessment the Assessing Officer is required to consider the information available with him to form the belief that the income assessable to tax has escaped assessment is more than Rs.50 lakhs which is a prima facie fact at the time of reopening of the assessment considered by the Assessing Officer. Thus, the learned DR has submitted that it is a procedural aspect and if subsequently it is found that the total cash deposit in the bank account is less than Rs.50 lakhs will not render the reopening or re-assessment invalid. He has relied upon the Orders of the authorities below.

6. We have considered the rival submissions as well as relevant material on record. The Assessing Officer has issued show cause notice u/sec.148A(b) on 12.03.2023 placed at Page no.240 to 241 of the paper book as under:

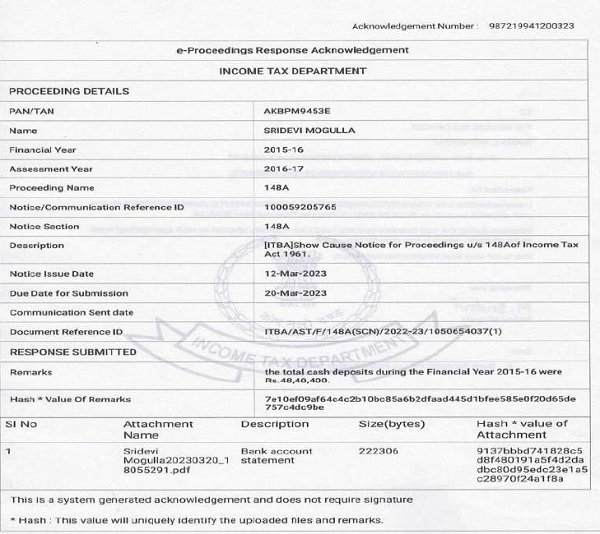

6.1. Thus, it is clear that the Assessing Officer has issued the show cause notice based on the information of two transactions of cash deposits of Rs.48,43,400/- and Rs.4 lakhs total amounting to Rs.52,43,400/-. In response to the said notice the assessee filed its reply dated 20.03.2023 acknowledgment of which is placed at Page no.140 of the paper book as under:

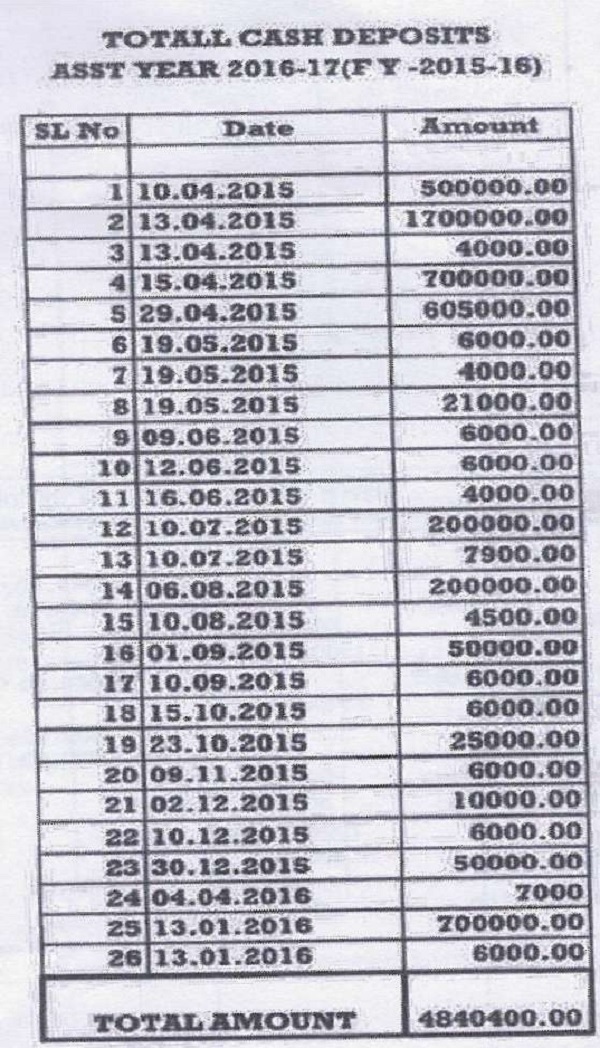

6.2. Along with this reply the assessee filed bank account statement and summary of the cash deposit as under:

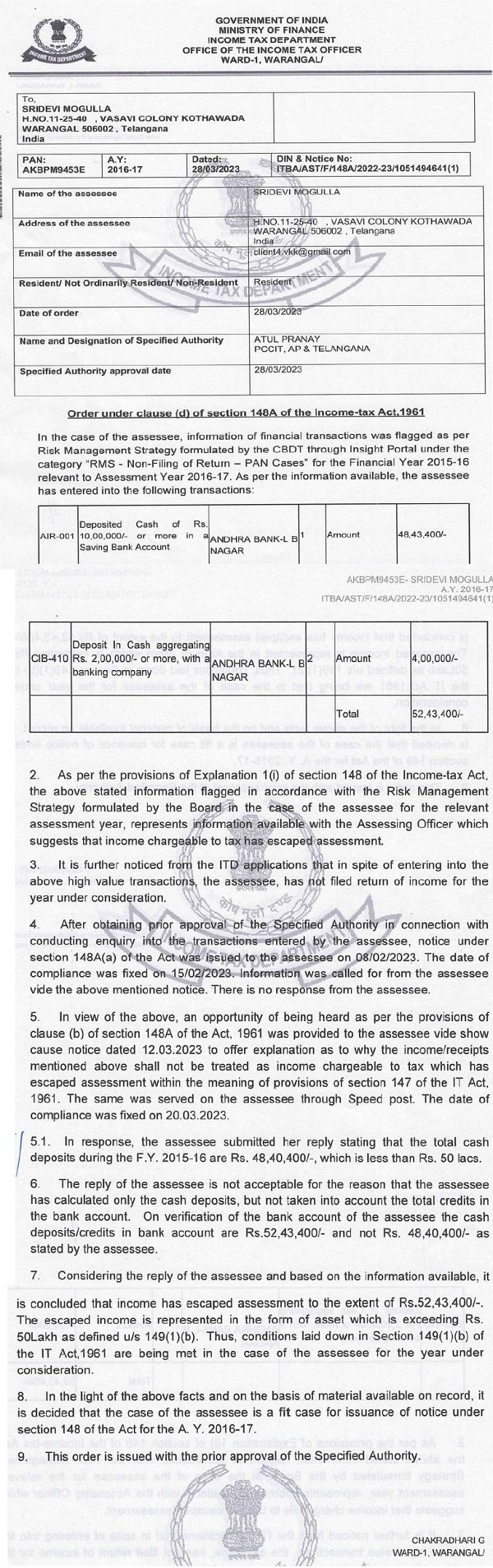

6.3. Thus, the assessee has explained that total amount of deposit is Rs.48,40,400/-. After considering this reply the Assessing Officer has passed the Order u/sec.148A(d) placed at Page nos.243 to 245 of the paper book as under:

6.4. Thus, in Para no.5.1 of the Order the Assessing Officer has acknowledged the reply of the assessee as the total amount of deposit of Rs.48,40,400/-. However, without disputing this fact the Assessing Officer has held that on verification of the bank account of the assessee the cash deposit in the bank account was at Rs.52,43,400/- and not Rs.48,40,400/- as stated by the assessee. It is pertinent to note that in the assessment order the Assessing Officer has accepted this fact at page no.5 as under:

6.5. Thus, during the course of assessment proceedings the Assessing Officer called the information u/sec.133(6) of the Act from the bank and as per the said information the Assessing Officer has noted that the total cash deposit in the bank account is Rs.48,43,000/- and addition was also proposed of the same amount. When the Assessing Officer proposed to reopen the assessment to assess the cash deposit in the bank account and the assessee brought into the notice of the Assessing Officer in reply to the notice u/sec.148A(b) of the Act that the total cash deposit in the bank account is only Rs.48,40,400/- which is less than Rs.50 lakhs then, the Assessing Officer was not permitted to issue notice u/sec.148 after expiry of three years from the end of the assessment year as provided u/sec.149(1)(a) of the Act. Undisputedly, the Assessing Officer has issued notice u/sec.148 of the Act on 29.03.2023 which is beyond three years from the end of the assessment year 2016-2017. An identical issue has been considered by this Tribunal in the case of Adilakshmi Vangala, Hyderabad vs. ITO, Ward-6(1), Hyderabad (supra), in Para nos.6 to 6.6 as under:

“6. We have considered the rival submissions as well as relevant material on record. There is no dispute that the Assessing Officer issued show cause notice u/ sec.148A(b) of the Act on 27.02.2023 which reads as under:

XXXXX XXXXX XXXXX

6.1. Thus, the Assessing Officer proceeded on the basis of the three transactions of cash deposit to reopen the assessment of the assessee. Thereafter, the Assessing Officer has passed an Order u/ sec.148A(d) of the Act on 23.03.2023 and then issued notice u/ sec.148 of the Act on 24.03.2023 reads as under:

XXXXX XXXXX XXXXX

6.2. Thus, it is clear that even at the time of passing the Order u/ sec.148A(d), the Assessing Officer has considered the same amount of cash deposits without even verifying the bank account statement of the assessee. In the assessment order the Assessing Officer finally held that the only transaction of cash deposit during the year is Rs.38,10,000/ – which is added to the total income of the assessee as under:

“Finding of the case

Section 69A of the Act deals with money etc, owned by the assessee and found in possession including in the bank accounts of the assessee which remain unexplained. The said section is reproduced below for ready reference:

Section 69A-Unexplained Money

“Where in any financial year the assessee is found to be the owner of any money, bullion, jewellery or other valuable article and such money, bullion, jewellery or valuable article is not recorded in the books of account, if any, maintained by him for any source of income, and the assessee offers no explanation about the nature and source of acquisition of the money, bullion, jewellery or other valuable article, or the explanation offered by him is not, in the opinion of the Assessing Officer, satisfactory, the money and the value of the bullion, jewellery or other valuable article may be deemed to be the income of the assessee for such financial year.”

In the present case, the assessee has deposited cash in the bank account amounting to Rs. 38,10,000/-which is treated as unexplained money u/s 69A of the Act, since she has not offered an acceptable or cogent explanation regarding the source thereof. As discussed above, the explanation offered by the assessee are entirely by self-sewing documents without third party evidence.”

6.3. Therefore, it is a case of wrong and incorrect facts or rather non-existing fact and transaction in the bank account of the assessee considered by the Assessing Officer at the time of issuing the show cause notice u/ sec.148A(b); at the time of passing the Order u/ sec.148A(d) as well as issuing notice u/ sec. 148 of the Act. Undisputedly, the actual transaction of deposit of cash is found to be only Rs.38,10,000/ – and therefore, the case of the assessee falls in the category of ‘income escaped assessment less than Rs.50 lakhs’ and consequently, as per the provisions of sec.149(1)(b) of the Act, the limitation for issuing the notice u/ sec.148A is only 03 years from the end of the relevant assessment year. There is no dispute that the notice u/ sec.148 of the Act issued on 24.03.2023 is beyond 03 years and therefore, the same is time barred and invalid. It is pertinent to note that i f a notice based on the correct and actual facts is invalid then, the same cannot be treated as valid by considering incorrect and nonexisting facts and hence, the period of limitation provided u/ sec.149(1)(b) of the Act cannot be enlarged or extended on the basis of incorrect facts or non-existing facts. It is a case of nonexisting transaction of cash deposit which are considered by the Assessing Officer and not a case that the transaction of deposit is rightly considered by the Assessing Officer however, the assessee was able to explain the source during the assessment proceedings and finally the Assessing Officer after accepting the source of cash deposit made an addition which is less than Rs.50 lakhs. Therefore, there is no quarrel on the point that the addition finally made by the Assessing Officer in the assessment would not necessarily render the case of the assessee in the category of `income escaped assessment is less than or more than Rs.50 lakhs’ but the primary facts are relevant to consider whether the income escaped assessment is less than or more than Rs.50 lakhs. The Assessing Officer relied upon the Judgment of Hon’ble Allahabad High Court in the case of ARB Hotels Resorts (P.) Ltd., vs. Pr. CCIT (supra) however, the Hon’ble Allahabad High Court has made a specific observation in Para no.22 as under:

“22. Last, we may also note as a Court of equity, the writ Court may not be persuaded to drop the entire proceedings at the fag end on a purely technical submission. Yet, that submission is not being accepted in the present facts. On a general principle, once component of escapement exists, it has to be finally determined by the assessing authority. We therefore refrain ourselves from exercising the discretionary jurisdiction to quash the entire proceedings at this late stage. To that rule of equity and good conscience, we abide

(iii) Considering the facts of the case and decision of the Hon’ble High Court of Allahabad on similar issue, the contention of the assessee is not found to be acceptable and hence rejected.”

6.4. Therefore, the Hon’ble High Court has declined to accept the objection of the assessee which is purely technical in nature in the writ proceedings and therefore, challenging the validity of the notice u/ sec.148 of the Act based on the factual finding given by the Assessing Officer in the assessment order would not render the notice u/ sec.148 as time barred. The Hon’ble Madras High Court in the case of Krishna Reddy Venkatsan, Tiruvallur vs. ITO, Tiruvallur (supra), has considered this issue in Para nos.2 to 6 as under:

“2. Learned counsel for the petitioner invited my attention to the notice under Section 148A(b), the reply thereto and the impugned order. In spite of providing the bank statement for the relevant period, learned counsel submits that it is erroneously recorded therein that the details of the bank statement needs to be verified.

3. Mr. B. Ramana Kumar, learned senior standing counsel, submits in reply that the assessee is under an obligation to establish that the amount escaping assessment is less than Rs.50,00,000/-. He submits further that both the cash deposit and the time deposit qualify as assets and that the assessing officer was justified in adding the two to compute total income escaping assessment.

4. The operative paragraph of the impugned order reads as under:

“3. In response to the said notice u/s 148A(b), assessee replied on 28.03.2022. According to assessee “He deposited in cash Rs.25,90,000/- and the same has been deposited as fixed deposit. Hence, the amount of income escaped is less than 50 lakhs.” Assessee submitted bank statement also for the relevant financial year.

I have considered the reply of assessee and the same is not acceptable because of the following reasons:

Though the assessee stated as the cash deposit again deposited as fixed deposit, the details of bank statement and others need to be verified.

Thus income in the form of asset has escaped assessment is not less than Rs.50 lakhs.”

5. It is evident from the above that the assessing officer failed to examine the bank statement so as to verify whether the cash deposits were used for purposes of creating the fixed deposit. In spite of the assessee providing the bank statement, this exercise was not undertaken. Without undertaking this exercise, it cannot be rationally determined as to whether income in the form of an asset of the value not less than Rs 50,00,000/- had escaped assessment during the relevant assessment year.

6. On perusal of the bank statement, it appears that the petitioner has an arguable case to contend that the cash deposits were used for purposes of creating the fixed deposit. Therefore, the matter warrants reconsideration. Consequently, the impugned order under Section 148A(d) and notice under Section 148 of the I-T Act are set aside and the matter is remanded to the assessing officer. After providing a reasonable opportunity to the petitioner, a fresh order shall be issued under Section 148A(d) of the I-T Act within two months from the date of receipt of a copy of this order.”

6.5. Thus, the Hon’ble Madras High Court has noted the fact that the Assessing Officer failed to examine the bank statement so as to verify correct and actual transactions of cash deposit and then set aside the notice issued u/ sec.148 of the Act and the matter was remanded to the Assessing Officer for passing a fresh Order u/ sec.148A(d) of the Act, after giving reasonable opportunity to the assessee. The Hon’ble Bombay High Court in the case of Naresh Balachandra Rao Shinde vs. ITO (supra), has also considered this issue in Para nos.6 to 9 as under:

“6. We have heard the learned counsel for the parties and we have perused the documents on record. To consider whether the writ petition could be entertained, it would be necessary to refer to certain undisputed facts. The notice under section 148 A(b) dated 23-3-2022 grants time to the petitioner to respond to the same by 29-3-2022. The period as granted is less than seven days as prescribed by section 148A(b) of the Act of 1961. Nevertheless, the petitioner has responded to the notice by his reply dated 29-3-2022.

Along with the reply, copy of the registered sale deed dated 3-2-2015 indicating that it was his daughter who had purchased the immovable property therein was supplied. The petitioner’s daughter is separately assessed for tax. The name of the petitioner is mentioned as special power of attorney holder for his daughter. The registered sale deed clearly indicates that the petitioner is not the purchaser of the immovable property mentioned therein but it is his daughter, a separate assessee. The amount of consideration mentioned is Rs.40,00,000/- and it is stated that the purchaser had availed housing loan for the same. On a bare perusal of the registered sale deed, it becomes evident that the petitioner is not the purchaser of the said property as stated in the notice issued under section 14BA (b) of the Act of 1961. Despite supplying copy of the registered sale deed to the Assessing Officer, it has not been taken into consideration by him before passing the order under section 148A(d) of the Act of 1961. The same thus clearly indicates lack of application of judicious mind to the material on record. The amount of Rs.40,00,000/- as mentioned in the notice issued on 23-3-2022 under section 148A(b) thus deserves to be excluded from consideration.

7. As regards deposit of cash of Rs.16,20,000/- is concerned, the petitioner had sought disclosure of the material of the source of information on the basis of which such notice was issued. The petitioner denied having deposited the aforesaid amount in his bank account. The material/source of information was not supplied to the petitioner. Be that as it may, even if the amount of Rs.40,00,000/- as mentioned in the notice dated 23-3-2022 is excluded from consideration for the reason that the petitioner is not the purchaser of the property in question, the amount remaining for consideration is Rs.20,71,500/- and Rs.16,20,000/- thus totaling Rs.36,91,500/-, In this regard, if the provisions of Section 149(1)(b) of the Act of 1961 are considered, it is seen that only if the amount in question that is likely to have escaped assessment is Rs.50,00,000/- or more, the time limit for issuing notice to re-open the assessment is three years but less than ten years. Thus if the income that is likely to escape assessment is only Rs.36,91,500/- after excluding the amount of Rs.40,00,000/-, it is clear that the proceedings are not liable to be re-opened as the amount involved is less than the one contemplated under section 149(1)(b) of the Act of 1961 and the same pertains to Assessment Year 201516. The notice under section 148(b) is dated 23-3-2022 which is beyond the permissible period of three years. On this count, a case for interference has been made out.

8. In the light of this undisputed position, it would be futile to require the petitioner to face proceedings under section 148 of the Act of 1961. The material on record that was placed before the Assessing Officer warranted consideration especially in the light of the fact that the document relied was a registered sale deed. If the amount of Rs.40,00,000/- mentioned therein is excluded from consideration, the notice as issued on 23-3-2022 falls foul of the provisions of section 149(1)(b) of the Act of 1961. Hence for this reason, we do not find that the petitioner should be required to further contest the proceedings under section 148 of the Act of 1961.

9. In that view of the matter, the order dated 31/3/2022 passed under section 145A(d) of the Income-tax Act, 1961 as well as notice dated 31-3-2022 issued under section 148 of the Act of 1961 are quashed and set aside. The respondents are free to take appropriate steps in accordance with law.”

6.6. Therefore, in view of the Judgment of the Hon’ble Supreme Court in the case of CIT vs. Vegetable Products Ltd. (1973) 88 ITR 192 (SC), we follow the Judgment of Hon’ble Madras High Court as well as Hon’ble Bombay High Court (supra) in deciding the issue in favour of the assessee. Accordingly, in the facts and circumstances of the case, when the actual transaction of cash deposit in the bank account of the assessee is only Rs.38,10,000/ – then, the notice issued by the Assessing Officer after 03 years from the end of the assessment year under consideration is barred by limitation and liable to be set aside. We Order accordingly.

7. This Tribunal by following the various decisions of the High Court has held that considering the incorrect and excess transaction of cash deposit at the time of passing the Order u/sec.148(A)(d) and issuing the notice u/sec.148 of the Act would not extend the period of limitation when the actual transaction is less than Rs.50 lakhs. Accordingly, by following the earlier decision of this Tribunal we hold that when the actual cash deposit in the bank account is less than Rs.50 lakhs which was also brought to the notice of the Assessing Officer then, the notice issued by the Assessing Officer u/sec.148 of the Act after the expiry of three years from the end of the assessment year is invalid being barred by limitation and the same is liable to be quashed. We Order accordingly.

8. Since, we have quashed the notice issued u/sec.148 of the Act being barred by limitation consequently vitiates the re-assessment order passed by the Assessing Officer therefore, the other grounds raised by the assessee become infructuous and not taken up for adjudication.

9. In the result, appeal of the Assessee is allowed.

Order pronounced in the open court on 15.07.2026.

Author Bio