Case Law Details

DCIT Vs Salem Mines and Aggregates (ITAT Chennai)

Chennai ITAT: Bogus Purchase Addition Cannot Rest on Suspicion; Search Data Must Be Corroborated with Independent Evidence

The Chennai ITAT delivered an extensive ruling holding that additions towards alleged bogus purchases and suppressed profits cannot be sustained merely on the basis of incomplete seized Tally data, assumptions, or suspicion. During a search, the Revenue relied upon seized electronic accounting data to allege suppression of profits and treated purchases of aggregates from certain suppliers as bogus. However, the Tribunal noted that the assessee had subsequently furnished a detailed reconciliation explaining that the seized Tally data represented incomplete books, in which several expenditure items had not been transferred to the Profit & Loss Account, thereby artificially inflating profits. The Investigation Wing itself accepted a substantial part of this reconciliation during the post-search proceedings.

The Tribunal upheld the deletion of additions relating to purchases from suppliers whose identity, GST registration, PAN, statutory records, banking transactions, and corresponding sales stood established. It observed that the Revenue had not unearthed any incriminating material during the search to show that the suppliers were fictitious, that the invoices were accommodation entries, or that money had flowed back to the assessee. It also noted that the GST authorities had accepted the transactions, the suppliers themselves had confirmed the sales, and the corresponding sales made by the assessee had never been disputed. In such circumstances, purchases could not be branded as bogus merely because of conjectures regarding mining activity, inward movement of goods, or deficiencies in the suppliers’ records.

The Tribunal further held that electronic data seized during search is only a starting point for investigation and cannot, by itself, constitute conclusive evidence when the assessee furnishes a credible reconciliation supported by books of account and documentary evidence. It emphasised that additions under the Income-tax Act must rest on cogent corroborative material, and not on presumptions or theoretical possibilities. At the same time, where the assessee failed to produce sufficient evidence to substantiate purchases from a particular supplier, the Tribunal sustained the disallowance relating to that supplier. Thus, the appeals were disposed of by granting relief in respect of substantiated purchases while sustaining additions only where the assessee failed to discharge its burden of proof.

Cases Discussed

- PCIT v. Sunil Mittal (HUF)

- DCIT v. Radiance Realty Developers India Ltd.

- CIT v. SPL Infrastructure Pvt. Ltd. (Madras High Court)

- CIT v. Bholanath Polyfab (P.) Ltd. (Gujarat High Court)

- Shri Shanti Swaroop Jain v. CIT (ITAT Agra),

- ITO v. Sri Puspal Kumar Das

- Syed Mubarak Ali v. ACIT (ITAT Chennai)

- PCIT v. SVD Resins & Plastics Pvt. Ltd. (Bombay High Court)

- PCIT v. Nitin Ramdeoji Lohia (Bombay High Court)

- CIT v. Nikunj Eximp Enterprises (P.) Ltd. (Bombay High Court)

- CIT v. Nangalia Fabrics (P.) Ltd. (Gujarat High Court)

- CIT v. M.K. Brothers (Gujarat High Court)

- PCIT v. Vijay Kumar Goel (Allahabad High Court)

FULL TEXT OF THE ORDER OF ITAT CHENNAI

These cross appeals, preferred by the Revenue and the Assessee, are directed against the separate orders, all dated 27.02.2026, passed by the Learned Commissioner of Income Tax (Appeals)-18, Chennai (hereinafter referred to as the “Ld.CIT(A)”). The impugned appellate orders arise out of the separate assessment orders passed on different dates by the Deputy Commissioner of Income Tax, Central Circle-1(4), Chennai (hereinafter referred to as “the AO”), pertaining to the Assessment Years (A.Y.) 2018-19 to 2021-22.

2. The assessments for the A.Y.2018-19, 2019-20 and 2020-21 were framed u/s.147 of the Income-tax Act, 1961 (hereinafter referred to as “the Act”), whereas the assessment for the Assessment Year 2021-22 was completed u/s.143(3) of the Act.

3. Since the issues arising for consideration in all the five appeals are substantially identical, emanating from the same search and seizure proceedings, involving common facts, identical evidentiary material and common reasoning by both the lower authorities, the appeals were clubbed, heard together and are being disposed of by this consolidated order. At the time of hearing, both the learned Departmental Representative and the learned Authorized Representative fairly submitted that the issues involved in these appeals are common in nature and arise out of the same search proceedings. Accordingly, with the consent of both the parties, the appeals were heard analogously. In the interest of judicial consistency, to avoid repetition of facts and duplication of discussion, and for the sake of convenience and brevity, we deem it appropriate to dispose of all the five appeals by way of this common and consolidated order. However, wherever the facts or grounds of appeal are distinct or require separate adjudication, the same have been dealt with independently under the relevant assessment year or appeal.

4. For the sake of convenience and ready reference, the particulars of the appeals under consideration before us are set out hereunder:

| S. No | AY | ITA No. | Appeal By | Assessment order passed u/s. and date of the order |

Date of order of CIT(A) |

| 1 | 2018-19 | 2528 / Chny / 2026 | Revenue | 147 of the Act dated 20.03.2025 |

27.02.2026 |

| 2 | 2019-20 | 2527 / Chny / 2026 | Revenue | 147 of the Act dated 27.03.2024 |

27.02.2026 |

| 3 | 2020-21 | 2524 / Chny / 2026 | Revenue | 147 of the Act dated 27.03.2024 |

27.02.2026 |

| 4 | 2020-21 | 2013 / Chny / 2026 | Assessee | ||

| 5 | 2021-22 | 2014 / Chny / 2026 | Assessee | 143(3) of the Act dated 30.12.2022 |

27.02.2026 |

5. The brief facts of the case, as borne out from the assessment records, are that the assessee is a partnership firm engaged in the business of manufacturing and sale of aggregates and sand. A search and seizure operation u/s.132 of the Act was conducted in the case of the assessee, its group concerns and its partner, Shri Subramani Perumal, on 02.03.2022.

6. During the course of the search proceedings, various books of account, documents, loose sheets and electronic devices containing incomplete data maintained in the Tally Accounting Software (hereinafter referred to as the “seized Tally data”) were found and seized. On examination of the seized Tally data, the Authorized Officer of the search observed that there existed a difference between the profits reflected therein and the income disclosed by the assessee in the returns of income filed for the assessment years under consideration.

7. It was noticed by the Authorized Officer that, as per the stock summary available in the seized Tally data, purchases of diesel issued for consumption by vehicles had erroneously been accounted for as inward stock entries, resulting in an inflated closing stock of diesel. Accordingly, the Authorized Officer, rectified this anomaly while preparing the profit suppression analysis during the course of the search by treating the closing stock of diesel as reflected in the seized Tally data as having been consumed during the relevant previous years and, consequently, allowing the same as expenditure.

8. The Authorized Officer further observed, on verification of the stock summary and the ledger accounts of M/s.Nayara Energy Limited, M/s.Essar Oil Limited and M/s.Indian Oil Corporation Limited contained in the seized Tally data pertaining to AY(s) 2019-20 and 2020-21, that the diesel purchases recorded therein had not been claimed as expenditure in the seized Tally data. Accordingly, while computing the alleged suppressed profits, the said purchases were also treated as allowable expenditure.

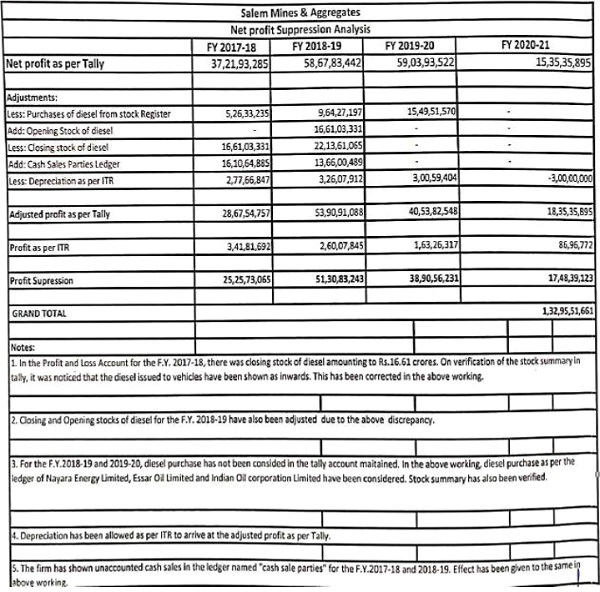

9. On the basis of the aforesaid exercise, the Authorized Officer worked out the alleged suppressed profit of the assessee for AY 2018-19 to 2021-22 at Rs.132,95,51,661/- during the course of the search. The AO, while framing the assessment, reproduced the workings prepared by the Authorized Officer at the time of search, as extracted at page 3 of the assessment order for A.Y.2018-19, which are reproduced hereunder:

10. In connection with the aforesaid allegation of suppression of profits, the statement of Shri Subramani Perumal, partner of the assessee firm, was recorded u/s.132(4) of the Act during the course of the search proceedings. In response to Question No.42, Shri Subramani Perumal stated that the assessee firm had effected both accounted and unaccounted purchases and sales. However, insofar as the quantum of the alleged suppression of profits worked out by the search team was concerned, he did not admit or confirm the said computation. On the contrary, he requested that a period of one week be granted to enable him to verify the relevant books of account and supporting documents so as to ascertain the correct quantum, if any, of such alleged suppression.

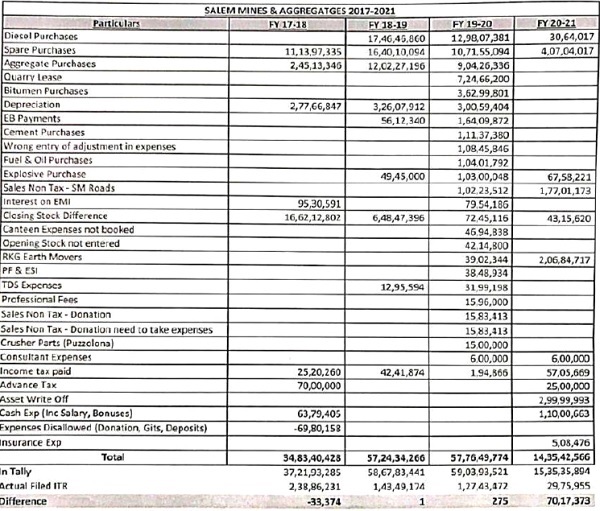

11. During the course of the post-search proceedings before the Joint Director of Income Tax (Investigation) (OSD), Unit-2(4), Chennai (hereinafter referred to as “the JDIT(Inv)”), the assessee, vide its reply dated 07.04.2022, furnished a detailed reconciliation of the profits reflected in the seized Tally data vis-à-vis the profits disclosed in the returns of income filed for the assessment years under consideration. The assessee explained that the seized Tally data represented an incomplete set of books wherein several heads of expenditure had not been transferred to the Profit & Loss Account. Consequently, the profits reflected in the seized Tally data stood artificially inflated and did not represent the true financial results of the business.

12. In support of the above explanation, the assessee furnished a reconciliation statement before the JDIT(Inv), reconciling the alleged suppressed profits with the profits disclosed in the returns of income. The said reconciliation statement has been extracted by the AO at page 5 of the assessment order for the A.Y.2018-19, which is as under:

13. From the aforesaid reconciliation, the assessee demonstrated that there was no suppression of profits for the AY(s) 2018-19, 2019-20 and 2020-21. In so far as the A.Y.2021-22 is concerned, the reconciliation disclosed a difference of Rs.70,17,373/-. Against the said difference, the assessee had already offered an additional income of Rs.1,00,00,000/- by filing a revised return of income on 31.03.2022, thereby covering the entire difference arising out of the reconciliation.

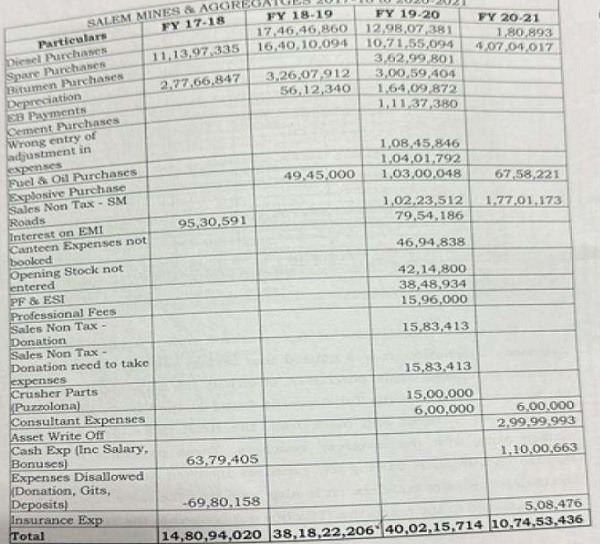

14. It is further noticed from page 5 of the assessment order for the A.Y.2018-19 that the reconciliation furnished by the assessee was duly examined by the JDIT(Inv) during the post-search investigation. Upon verification of the supporting books of account and documentary evidences produced by the assessee, the JDIT(Inv) accepted the genuineness of various expenditure claimed in the reconciliation, including Diesel Purchases, Spare Purchases, Explosive Purchases, Sales Non-Tax (SM Roads), Consultant Expenses, Cash Expenses (including Salary and Bonus) and Insurance Expenses. Accordingly, these expenditures were accepted during the course of the post-search investigation. The details of such expenses, as accepted by the Investigation Wing, have been extracted by the AO at page 6 of the assessment order for the A.Y.2018-19, which is as under:

15. However, the issues relating to (i) the alleged difference in closing stock, (ii) purchases of aggregates, and (iii) certain non-allowable items such as income-tax paid, advance tax paid, tax deducted at source and lease rent were left open by the JDIT(Inv) for examination by the AO during the course of the assessment proceedings. In so far as the items relating to income-tax paid, advance tax paid, tax deducted at source and similar inadmissible expenditures are concerned, no dispute survives, since the assessee had already disallowed and added back the same while computing its taxable income in the respective returns of income. Thus, the controversy that survives for adjudication is confined only to the additions made on account of the alleged bogus purchases of aggregates and the alleged difference in closing stock.

16. During the course of the assessment proceedings, the AO proposed (i)to disallow the purchases of aggregates claimed by the assessee by treating the same as non-genuine and bogus, and (ii) to treat the value of the closing stock reflected in the seized Tally data as business income of the assessee for the respective assessment years under consideration.

17. On a perusal of the assessment orders passed for all the assessment years involved in the present batch of appeals, it is noticed that the reasoning adopted by the AO for making the aforesaid additions is identical in substance and materially similar in all respects. Since the facts, the evidence relied upon, the explanation offered by the assessee, and the findings recorded by the AO are common across all the years, both the parties fairly agreed that A.Y.2018-19 may be treated as the lead assessment year. Accordingly, for the sake of convenience and to avoid repetition of facts, the reasoning adopted by the AO in A.Y.2018-19 is examined herein, and the findings rendered thereon shall, wherever applicable, govern the remaining assessment years also.

18. In response to the show cause notice issued by the AO, the assessee submitted a detailed explanation justifying the purchases of aggregates made during the relevant previous year. It was contended that the assessee was engaged in the business of quarrying and supply of blue metal aggregates to various customers pursuant to contractual commitments. According to the assessee, the contracts entered into with its customers stipulated strict delivery schedules and timelines, and any delay in execution of the supply obligations would expose the assessee to contractual penalties and business losses.

19. The assessee further explained that although it owned quarrying operations, the production from its own quarry was not always sufficient to meet the contractual demand within the stipulated time. In such circumstances, as a matter of normal commercial practice, the assessee procured aggregates from third-party suppliers as well as from M/s. P.S. Blue Metals, a proprietary concern belonging to one of the partners of the assessee-firm, so as to honour its delivery commitments. It was submitted that such purchases were dictated by business exigencies and constituted a regular and accepted practice in the trade.

20. The assessee further submitted that all purchases effected from M/s.P.S.Blue Metals were duly recorded in its regular books of account and were supported by tax invoices. The transactions had suffered GST, and the corresponding sales had also been disclosed by M/s.P.S.Blue Metals in its own books of account. It was further pointed out that the purchases recorded in the hands of the assessee correspondingly stood reflected as sales in the books of the proprietary concern of its partner, thereby establishing the identity of the supplier as well as the genuineness of the transactions. On the aforesaid premises, the assessee contended that the purchases could not be characterised as bogus merely on the basis of suspicion or surmises and requested the AO to refrain from making any disallowance.

21. With regard to the proposed addition on account of the closing stock reflected in the seized Tally data, the assessee submitted that the figures appearing therein did not represent the actual value of the closing stock physically held by the assessee. It was explained that owing to an accounting error, substantial purchases of diesel and explosives had inadvertently remained grouped under the head “Closing Stock” instead of being transferred to the respective expenditure accounts.

22. The assessee specifically pointed out that the AO himself, in the show cause notice, had observed that it was commercially and practically impossible for the assessee to maintain such an extraordinarily large quantity of diesel and explosives as closing stock. Relying upon this very observation, the assessee submitted that the abnormal figures appearing in the seized Tally data themselves demonstrated that they could not represent actual stock.

23. To substantiate its explanation, the assessee furnished the relevant ledger extracts from the seized Tally data and demonstrated that the amounts reflected under the closing stock account substantially represented purchases of diesel and explosives which had not been appropriately classified in the accounting software. It was explained that these purchases ought to have been transferred to the respective consumption or expenditure ledgers and that the apparent inflation in closing stock was merely the result of an accounting misclassification rather than the existence of any actual inventory.

24. Accordingly, it was contended that no addition could be made merely on the basis of the figures appearing in the seized electronic records without appreciating the accounting treatment and the corresponding ledger entries. The assessee therefore requested the AO to accept the explanation and to refrain from making any addition towards the alleged difference in closing stock.

25. The AO, however, was not persuaded by the explanations furnished by the assessee. Rejecting the contentions advanced during the assessment proceedings, the AO proceeded to make additions towards the alleged bogus purchases of aggregates as well as the alleged excess closing stock.

26. While dealing with the issue relating to the purchases of aggregates, the AO observed that the assessee had claimed purchases of boulders and blue metal aggregates despite allegedly having unrestricted access to sufficient quantities of boulders through excessive extraction from its own quarry beyond the licensed limits. According to the AO, no evidence indicating inward movement of boulders or aggregates from outside sources was either found during the course of the search or subsequently produced by the assessee during the assessment proceedings. The AO further observed that the customised software application, namely “Modomines”, maintained by the assessee did not contain any inward entries evidencing purchases of aggregates from third parties or from its partner.

27. Although the assessee had claimed that the purchases were made from M/s.P.S.Blue Metals, the proprietary concern of Shri Subramani Perumal, the AO observed that, upon examination, Shri Subramani Perumal stated that he procured the materials from various third-party suppliers before supplying them to the assessee. However, according to the AO, despite repeated opportunities, neither the assessee nor Shri Subramani Perumal furnished the names, Permanent Account Numbers (PAN), addresses, quarry details, invoices or other supporting particulars relating to such primary suppliers. The AO therefore concluded that the assessee had failed to establish the actual source of procurement of the aggregates and held that no genuine purchases had in fact taken place. Proceeding on this premise, the AO treated the expenditure claimed towards purchase of aggregates as bogus expenditure incurred with the intention of suppressing the taxable profits of the assessee.

28. With regard to the issue of closing stock, the AO observed that the financial statements reflected a closing stock. According to the AO, such a claim was inherently improbable, since diesel is a consumable item required for day-to-day quarrying operations and there could be no commercial justification for maintaining stock exceeding even the annual consumption of diesel by the assessee. The AO further observed that similar abnormalities were noticed in the succeeding financial years as well, thereby strengthening the conclusion that the closing stock figures disclosed by the assessee were not genuine.

29. The AO rejected the assessee’s explanation that the figures merely represented purchases of diesel and explosives inadvertently grouped under the closing stock account. According to the AO, the explanation was unsupported by any credible documentary evidence. The assessee had not furnished invoices, bills, vouchers, e-way bills, goods receipt notes, bank statements or confirmations from the alleged suppliers to substantiate the accounting treatment claimed. The AO further observed that the books of account for the relevant previous year had already been subjected to statutory audit and the audit report in Form No.3CD had been furnished prior to the date of search. According to the AO, had the purchases actually remained unposted to the appropriate expenditure ledgers, the statutory audit could not have been completed in the manner claimed by the assessee. The AO therefore characterised the explanation as a mere self-serving statement unsupported by documentary evidence and, consequently, rejected the assessee’s contention. On the aforesaid reasoning, the AO proceeded to add the amount reflected as closing stock in the seized Tally data u/s.37 of the Act for the relevant assessment years.

30. Consequently, the additions made by the AO for the respective assessment years, which are the subject matter of adjudication before us, are set out hereunder:

(Amount in Rs.)

| Particulars | AY 2018-19 | AY 2019-20 | AY 2020-21 | AY 2021-22 |

| Disallowance on account of alleged bogus purchases of aggregates u/s.37 | 2,45,13,346 | 12,02,27,196 | 9,43,26,680 | income in the return filed u/s.148, the AO disallowed only the balance amount.) |

| Addition towards alleged closing stock difference u/s.37 | 16,62,12,802 | 6,48,47,396 | 72,45,116 | – |

| Total Addition made by the AO | 19,07,26,148 | 17,92,74,594 (Sum of the above additions amounts to Rs.18,50,74,592/-. However, the AO has erroneously arrived at a figure of Rs.17,92,74,594/-) |

10,15,74,102 | 1,06,84,717 |

31. Consequently, the impugned assessment orders came to be passed by the AO, determining the total income of the assessee as under:

(Amount in Rs.)

| Particulars | AY 2018-19 | AY 2019-20 | AY 2020-21 | AY 2021-22 |

| Assessment completed u/s. | 147 | 147 | 147 | 143(3) |

| Date of order | 20.03.2025 | 27.03.2024 | 27.03.2024 | 30.12.2022 |

| Total income returned by the assessee | 3,41,81,690 | 2,60,07,840 | 8,87,92,520 | 1,86,96,770 |

| Total additions made by the AO as detailed supra | 19,07,26,148 | 17,92,74,594 | 10,15,74,102 | 1,06,84,717 |

| Assessed Income |

22,49,07,838 | 20,52,82,434 | 19,03,66,622 | 2,93,81,487 |

32. Being aggrieved by the assessment orders passed by the AO, making additions towards the alleged bogus purchases of aggregates and the alleged difference in the valuation of closing stock, the assessee preferred appeals before the Ld.CIT(A). The Ld.CIT(A), vide separate orders dated 27.02.2026, allowed the appeals relating to AY(s) 2018-19 and 2019-20, partly allowed the appeal for A.Y.2020-21, and dismissed the appeal for A.Y.2021-22. Aggrieved by the relief granted by the Ld.CIT(A), the Revenue is in appeal before us, whereas the assessee is in appeal in respect of the issues decided against it.

33. The nature of the additions involved and the identical grounds raised by the Revenue and the Assessee, the issues arising in these appeals issue-wise to be adjudicated as under:

Issue No.1: Disallowance of bogus purchase of aggregates u/s.37 of the Act:

34. The details of disallowances u/s.37 of the Act made by the AO on account of the alleged bogus purchases of aggregates for the respective assessment years are as under:

Amount in Rs.

| Particulars | AY 2018-19 | AY 2019-20 | AY 2020-21 | AY 2021-22 |

| Disallowance on account of alleged bogus purchases of aggregates u/s.37 | 2,45,13,346 | 12,02,27,196 | 9,43,26,680 | 1,06,84,717 |

35. In A.Y.2021-22, the total purchases from the concerned supplier amounted to Rs.2,06,84,717/-. Since the assessee had already offered a sum of Rs.1,00,00,000/- as additional income in the return of income filed in response to the notice issued u/s.148 of the Act, the AO restricted the disallowance to the balance amount of Rs.1,06,84,717/-.

36. On perusal of the assessment orders and the order of the Ld.CIT(A) further reveals that the aforesaid disallowances relate to the purchases made from the following suppliers during the respective assessment years:

| AY | Supplier | Amount (Rs. |

| 2018-19 | M/s. P.S. Blue Metals, a proprietary concern of Shri Subramani Perumal, one of the partners of the assessee-firm | 2,45,13,346 |

| 2019-20 | M/s. P.S. Blue Metals, a proprietary concern of Shri Subramani Perumal, one of the partners of the assessee-firm | 12,02,27,196 |

| 2020-21 | M/s. P.S. Blue Metals | 7,77,33,236 |

| M/s. RKG Earth Movers | 1,10,97,410 | |

| M/s. Shri Chennai Mines | 17,68,467 | |

| M/s. RKG Earth Movers (being payments reflected in the seized Tally data) | 39,02,344 | |

| 2021-22 | M/s. RKG Earth Movers | 2,06,84,717 |

37. Thus, it is evident that the impugned additions have been made by the AO by treating the purchases effected from the above parties as non-genuine and consequently disallowing the corresponding expenditure claimed by the assessee u/s.37 of the Act. The correctness and sustainability of the said disallowances are the subject matter of adjudication before us.

38. The assessee, before the Ld.CIT(A), assailed the impugned additions by contending that the purchases in question were effected from existing and identifiable concerns, viz., M/s.P.S. Blue Metals, M/s.RKG Earth Movers and M/s.Shri Chennai Mines, all of whom were duly registered under the GST Act and possessed valid PAN and GST registrations. It was further submitted that M/s.P.S. Blue Metals and M/s.Shri Chennai Mines were assessed to income-tax by the very same AO. Therefore, according to the assessee, once the identity and existence of the suppliers were never in dispute, there existed no justification for the AO to characterize the purchases as bogus.

39. The assessee further submitted that the purchases were duly supported by cogent documentary evidence comprising GSTR-2A reflecting the impugned transactions, ledger accounts of the suppliers, bank statements evidencing payments through normal banking channels, sales registers maintained by the suppliers, GST assessment orders accepting the transactions as genuine and income-tax assessment orders passed in the cases of the suppliers wherein the corresponding sales effected to the assessee stood accepted. It was contended that once the transactions had been accepted by the GST authorities as well as by the AO while completing the assessments of the suppliers, the very same AO could not, without bringing any contrary material on record, treat the corresponding purchases in the hands of the assessee as non-genuine.

40. It was further contended that no incriminating material whatsoever had been brought on record either during the course of search or in the assessment proceedings to establish that the impugned purchases represented sham transactions or accommodation entries. According to the assessee, no material had been unearthed to suggest that the suppliers were fictitious entities, that the invoices were merely accommodation bills, that any cash had flown back to the assessee or that the payments made through banking channels had been returned in any manner. It was also pointed out that even the statement recorded from Shri P.Subramani during the course of search did not contain any admission indicating that the purchases effected by the assessee were bogus.

41. The assessee further submitted that the AO had neither rejected the books of account maintained by the assessee nor pointed out any discrepancy in the quantitative records, stock records, GST records or the audited financial statements. It was emphasized that the books of account were duly audited u/s.44AB of the Act and had been accepted by the AO except to the extent of the impugned disallowance.

42. The assessee also contended that the corresponding sales arising out of the impugned purchases had been fully accepted by the AO. Such sales were duly reflected in the audited financial statements and reconciled with the GST returns. It was argued that once the sales were accepted as genuine, the corresponding purchases could not simultaneously be held to be bogus in the absence of any material to establish that the sales themselves were fictitious. It was submitted that no business could effect sales without corresponding purchases and, therefore, the disallowance was contrary to the settled principles governing assessment of business income.

43. The assessee further submitted that if the entire purchases were disallowed, the resultant Gross Profit ratio would increase abnormally, which would be commercially unrealistic and wholly inconsistent with the nature of the assessee’s business. It was argued that the AO had not brought on record any comparable industry data or similar cases to justify such an abnormal Gross Profit ratio.

44. The assessee also assailed the observations of the AO regarding alleged excessive mining, absence of inward movement of materials and the failure of the suppliers to furnish details of their vendors, by submitting that such findings were founded merely on assumptions and surmises. It was contended that no technical report, scientific analysis or independent evidence had been brought on record to establish excessive mining. It was further explained that the blue metal aggregates purchased from the suppliers were transported directly from the crushing units to the customers and, therefore, there was no occasion for any inward movement of such materials into the assessee’s quarry premises. It was also submitted that any alleged deficiency in the maintenance of records by the suppliers could not constitute a valid ground for disallowing genuine purchases effected by the assessee.

45. The assessee also placed considerable reliance upon the findings recorded by the GST authorities, who, after conducting detailed verification both in the case of the assessee and the suppliers, had accepted the transactions as genuine and specifically recorded that the transactions were not circular in nature. It was therefore submitted that the AO could not arrive at a contrary conclusion without conducting any independent enquiry or confronting the findings recorded by the GST authorities.

46. The assessee further placed reliance upon various judicial precedents, including the decisions of the Hon’ble Bombay High Court in PCIT v. SVD Resins & Plastics Pvt. Ltd., PCIT v. Nitin Ramdeoji Lohia and CIT v. Nikunj Eximp Enterprises (P.) Ltd., the Hon’ble Gujarat High Court in CIT v. Nangalia Fabrics (P.) Ltd. and CIT v. M.K. Brothers, the Hon’ble Allahabad High Court in PCIT v. Vijay Kumar Goel and various decisions of the Coordinate Benches of the Tribunal, wherein it has consistently been held that where purchases are supported by bills, books of account, banking records and corresponding sales have been accepted, such purchases cannot be treated as bogus merely on suspicion or on account of deficiencies noticed in the case of the suppliers.

47. On the strength of the aforesaid submissions, the assessee contended that the entire addition rested merely upon conjectures and presumptions without any corroborative material. Since the identity of the suppliers stood established, the purchases were duly reflected in the statutory GST records, payments had been made through banking channels, the corresponding sales stood accepted, no incriminating material had been found during the course of search and the trading results remained consistent with earlier years, the disallowance made u/s.37 of the Act on account of alleged bogus purchases was wholly unsustainable. Accordingly, the assessee prayed for deletion of the additions made in respect of purchases from M/s.P.S.Blue Metals, M/s.RKG Earth Movers and M/s. Shri Chennai Mines for the AY(s) 2018-19 to 2020-21.

48. With regard to the addition of Rs.39,02,344/- made for A.Y.2020-21 on the basis of payments reflected in the seized Tally data in favour of M/s.RKG Earth Movers, the assessee submitted that the said amount represented payments made towards aggregate purchases, all of which had been discharged through normal banking channels, thereby ruling out any inference of cash transactions or non-genuine dealings. It was further submitted that the AO had not disputed the genuineness of the payments nor alleged that the expenditure had been incurred for any purpose other than the legitimate business of the assessee. Consequently, the expenditure qualified for deduction u/s.37(1) of the Act.

49. The assessee further submitted that the Gross Profit ratio declared for A.Y.2020-21 was 19.32%, which was substantially in line with the Gross Profit ratio of 19.40% disclosed in the immediately preceding assessment year, thereby indicating consistency in the trading results and negativing any allegation of inflation of expenditure or suppression of income. It was also contended that the AO had not rejected the books of account u/s.145 of the Act and had accepted the sales disclosed by the assessee. Therefore, in the absence of any specific defect, a partial disallowance of business expenditure was legally untenable. It was submitted that even assuming there were certain deficiencies in the supporting vouchers relating to the aforesaid payments, such minor lapses could not justify disallowance when the genuineness of the transactions, the sales and the overall business results remained undisputed. Accordingly, deletion of the addition of Rs.39,02,344/- was sought.

50. Insofar as the addition of Rs.1,06,84,717/- made for A.Y.2021-22 was concerned, the assessee submitted that the Gross Profit ratio for the relevant year stood at 20.38% as against 19.32% in the immediately preceding year, thereby reflecting an improvement in profitability and completely dispelling the allegation of inflation of purchases or suppression of profits. It was contended that if the entire disallowance of Rs.2,06,84,717/- made by the AO were sustained, the resultant Gross Profit would increase to Rs.10,92,69,451/-, translating into an unrealistic Gross Profit ratio of 25.14%, which was commercially impracticable and wholly inconsistent with the nature of the assessee’s business. It was further submitted that the AO had neither produced any comparable industry data nor demonstrated that similarly placed concerns ordinarily earned such an elevated Gross Profit ratio.

51. The assessee further submitted that although the purchases were genuine, having regard to certain deficiencies noticed in the supporting documentation relating to aggregate purchases amounting to Rs.2,06,84,717/, it had, purely with a view to avoid protracted litigation and by way of abundant caution, voluntarily disallowed a sum of Rs.1,00,00,000/- while computing its taxable income. Consequently, it was submitted that the balance addition of Rs.1,06,84,717/- made by the AO u/s.37 of the Act deserved to be deleted.

52. Without prejudice to the above submissions, the assessee alternatively contended that even assuming, without admitting, that certain deficiencies existed in the supporting documentation relating to the impugned purchases, the settled legal position is that the entire purchases cannot be disallowed and, at the highest, only the profit element embedded in such purchases could be brought to tax.

53. On the aforesaid premises, the assessee prayed before the Ld.CIT(A) that the additions made by the AO u/s.37 of the Act towards the alleged bogus purchases of aggregates for the AY(s) 2018-19 to 2021-22 be deleted in their entirety.

54. Upon due consideration of the submissions advanced by the assessee and the material available on record, the Ld.CIT(A) granted relief in varying degrees across the assessment years under consideration. The additions made by the AO were deleted in entirety for AY(s) 2018-19 and 2019-20. In respect of A.Y.2020-21, the Ld.CIT(A) sustained the addition only in part, whereas for A.Y.2021-22, the addition was confirmed in full. The particulars of the relief granted by the Ld.CIT(A) for the respective assessment years are summarized hereinbelow for the sake of ready reference:

| AY | Supplier | Amount (Rs.) | Relief given by the CIT(A) |

| 2018-19 | M/s.P.S.Blue Metals, a proprietary concern of Shri Subramani Perumal, one of the partners of the assessee-firm | 2,45,13,346 | Deleted |

| 2019-20 | M/s. P.S. Blue Metals, a proprietary concern of Shri Subramani Perumal, one of the partners of the assessee-firm | 12,02,27,196 | Deleted |

| 2020-21 | M/s.P.S. Blue Metals | 7,77,33,236 | Deleted |

| M/s.RKG Earth Movers | 1,10,97,410 | Sustained | |

| M/s.Shri Chennai Mines | 17,68,467 | Deleted | |

| M/s.RKG Earth Movers (being payments reflected in the seized Tally data) | 39,02,344 | Deleted | |

| 2021-22 | M/s.RKG Earth Movers | 1,06,84,717 | Sustained |

55. The findings of the Ld.CIT(A), insofar as they relate to the deletion and the sustenance of the above additions, are extracted hereunder for the sake of ready reference.

56. The Ld.CIT(A), while deleting the additions made by the AO on account of the alleged bogus purchases of aggregates, has recorded substantially identical findings for all the assessment years under consideration. The findings and reasoning recorded by the Ld.CIT(A) for the A.Y.2018-19 are treated as the lead findings and are extracted hereunder:

“5.3.7 I have carefully examined the assessment order and the submissions made by the appellant. Before adverting to the substantive issue regarding the genuineness of the purchases and the contentions raised by the appellant, it is appropriate to record a prima facie observation with regard to the Tally data found during the course of search. As noted in the assessment order, the initial cross-verification of the Tally data impounded during the search proceedings with the financial statements and the return of income filed by the appellant indicated a suppressed profit of Rs.25,25,73,065/-. However, during the post-search proceedings, the appellant reconciled the differences between the two sets of data and arrived at a residual difference of Rs.33,374/-. The tabulated reconciliation statement furnished by the appellant was incorporated in the assessment order at page 5. !t is on the basis of this cross-verification exercise that the Assessing Officer proceeded to disbelieve the purchases claimed from M/s P.S. Blue Metals, amounting in aggregate to Rs.2,45,13,346/- (and the entry of closing stock difference of Rs.16.62 crores appearing in the seized Tally needs no cross-verification at all, and the reasons will be discussed in the relevant paras below / grounds). !n effect, the appellant was able to substantially reconcile and reduce the variance between the two sets of data during the post-search proceedings. Therefore, the unequivocal inference that emerges from this exercise is that the Tally data found during the course of search cannot, by itself and without further corroborative evidence, be treated as conclusively establishing suppression of profit or claim of non-genuine expenses, particularly when the differences have been largely reconciled through documentary explanation at the time of post-search proceedings itself.

5.3.8 Now adverting to the reasons recorded by the Assessing Officer for disbelieving the purchases from M/s P.S. Blue Metals, it is observed that the principal ground taken in the assessment order is that the appellant had access to sufficient boulders through alleged excessive mining from its own quarry, and that such extraction was made without incurring corresponding expenditure. The first limb of this reasoning, in substance, amounts to an allegation that the appellant had carried out mining operations in excess of the licensed or permitted capacity. However, no material whatsoever has been brought on record in the assessment order to substantiate such an allegation. An addition or disallowance cannot be sustained on the basis of presumption that the appellant must have mined beyond permissible limits, particularly when such an allegation carries regulatory and penal implications under the relevant mining laws. In the absence of any seized material evidencing unrecorded production, the very foundation of the Assessing Officer’s reasoning lacks evidentiary support.

5.3.9 In the second limb of the Assessing Officer’s reasoning, namely that the appellant had extracted boulders “without incurring any expenses”, is equally untenable. Mining activity, by its very nature, involves substantial and unavoidable expenditure towards labour, machinery, fuel, blasting materials, transportation, statutory levies, royalty payments, and environmental compliance. The assessment order does not demonstrate, with reference to seized material or third-party evidence, that such expenditure was either not incurred or was incurred outside the books of account. In fact, the books of account of the appellant reflect regular expenditure towards quarry operations, and no specific defect therein has been pointed out to show suppression of production or inflation of purchases. Without rejecting the books of account under the applicable statutory provisions and without establishing that the recorded expenses are fictitious or incomplete, it is not open to the Assessing Officer to presume that raw materials were generated at nil cost and, on that premise, to disbelieve the purchases effected from M/s P.S. Blue Metals. The reasoning adopted, therefore, proceeds on an assumption that the appellant possessed unaccounted stock generated without cost, and that the purchases recorded in the books were merely accommodative. However, such a conclusion must be supported by tangible and corroborative material evidencing either excess production, unaccounted stock, or circulation of funds. In the absence of such material, the disallowance does not meet the threshold of evidentiary standards required to sustain an addition.

5.3.10 The next observation of the Assessing Officer is that no evidence of inward movement of boulders was found during the course of search, and therefore the purchases were treated as non-genuine. In response, the appellant has submitted that, depending upon business exigencies and urgent customer requirements, the materials purchased were, in certain instances, directly delivered by the supplier to the appellant’s customers. In such circumstances, the goods did not physically reach the appellant’s premises and, consequently, no inward entry or transport record reflecting receipt at the appellant’s yard would be available. The explanation offered by the appellant is consistent with accepted commercial practice, particularly in the trade of construction materials and quarry products, where direct dispatch to customers is undertaken to reduce handling costs, avoid double transportation, and meet time-sensitive supply commitments. The absence of inward movement at the appellant’s premises, therefore, cannot, by itself, lead to the conclusion that the purchases are fictitious, unless it is further demonstrated that the corresponding outward supplies, sales realization, or quantitative records are also unverifiable.

5.3.11 As per the assessment order, due inquiries were conducted with the supplier of impugned blue metals, namely the proprietor of M/s P.S. Blue Metals, who is also a partner in the appellant-firm and had been simultaneously searched along with the appellant. The proprietor, Sri Perumal confirmed the sales made through his proprietary concern and, as per the appellant, provided all relevant records in his possession, including GST returns, income tax filings, and other documentary evidence substantiating the transactions. However, despite the supplier’s confirmation and the submission of comprehensive records, the Assessing Officer did not undertake any independent verification of these documents or examine the consistency of the supplied data with statutory filings. No adverse observation was recorded regarding the completeness or authenticity of the documents furnished by the supplier but referred that no quarry details were furnished, including PAN and address of the primary suppliers. For the year under consideration, there is only one supplier of aggregate metals, and that is the partner of the firm, in the capacity of proprietor of M/s P.S. Blue Metals. When the supplier also was searched and assessed with the same AO, the observations of the AO that ‘no details were furnished’ is factually incorrect. In effect, the AO’s observation ignores the undisputed fact that all relevant transactions and statutory filings of the sole supplier were made available and verified to the extent of the documents in his possession. The absence of additional supplier details is immaterial, as no other supplier existed for the year under consideration, and no evidence was produced to suggest that the transactions were not genuine. Consequently, the basis for disbelieving the purchases is wholly unsubstantiated, not based on any objective evidence found during the course of search. In this regard, the contention of the appellant that no incriminating material was found either at its premises or at the premises of the supplier during the course of search, so as to indicate any bogus supply or purchase of goods, assumes considerable significance. In the absence of any seized material evidencing fictitious transactions, accommodation entries, or unaccounted movement of funds, the allegation of non-genuine purchases lacks foundational support.

5.3.12 Added to the above, the appellant has furnished copies of the GST assessment orders in the case of the supplier, M/s P.S. Blue Metals, as well as in its own case, as purchaser. It is an undisputed fact that no adverse view has been taken by the GST Department in respect of the impugned purchases and corresponding sales. The transactions have been duly reported in the statutory returns filed under the GST law, and the tax liability arising therefrom has been accepted by the competent authority. While proceedings under the Income-tax Act and the GST enactments operate independently, the fact that the very same transactions have been scrutinized under a parallel fiscal statute and have not been found to be sham or fictitious / circuitous assumes evidentiary significance. In the absence of any material demonstrating that the GST findings were erroneous or that the transactions were merely accommodation entries, it would be inconsistent to disregard the purchases solely on presumptive grounds. Thus, the acceptance of the transactions by the GST authorities further fortifies the appellant’s contention that the purchases from M/s P.S. Blue Metals are genuine and duly supported by statutory compliance and documentary evidence.

5.3.13 To conclude, in view of the foregoing discussion, when the Tally data found during the course of search has been substantially reconciled; when the allegation of excessive mining is unsupported by any material evidence; when the absence of inward movement stands satisfactorily explained in light of direct dispatch to customers; when the sole supplier has confirmed the transactions and furnished statutory records; when the supplier himself was subjected to search and assessment by the same Assessing Officer; and when the impugned transactions have been accepted by the GST authorities without any adverse finding — the cumulative effect of these facts leaves no room to sustain the disallowance of purchase of blue metal aggregates and accordingly, the AO is directed to delete the addition made at Rs.2,45,13,346/-. As such, ground No.2 is allowed.”

57. On the basis of the aforesaid findings and the reasons recorded therein, the Ld.CIT(A) deleted the additions made by the AO in respect of the purchases effected from M/s.P S Blue Metals for the A.Y.2019-20. Similarly, for the A.Y.2020-21, the Ld.CIT(A) deleted the additions relating to the purchases made from M/s.P.S.Blue Metals as well as M/s.Shri Chennai Mines, holding that the AO was not justified in treating the said purchases as non-genuine.

58. The findings recorded by the Ld.CIT(A) while upholding the addition of Rs.1,10,97,410/- made by the AO on account of purchases effected from M/s.RKG Earth Movers for the A.Y.2020-21 are reproduced hereunder:

“5.3.13 As discussed in para 5.3.5 above, the total purchases disallowed by the Assessing Officer pertain to three parties, namely: (1) M/s PS Blue Metals – Rs.7,77,33,236/-, (2) M/s RKG Earth Movers – Rs.1,10,97,410/-, and (3) M/s Shri Chennai Mines – Rs.17,68,467/-. The evidences furnished in respect of M/s PS Blue Metals and M/s Shri Chennai Mines have already been examined in detail and found to be satisfactory. The purchases from these two parties stand duly substantiated and are accepted as genuine. However, the position is materially different in respect of purchases from M/s RKG Earth Movers. In this case, the appellant has merely furnished copies of GST returns and bank account statements to demonstrate that payments were made through banking channels. No further corroborative evidence has been produced to prove the genuineness of the sales like the GST assessment order, income-tax particulars of the supplier, or any other independent documentary evidence to establish the genuineness of the transactions, as was done in the case of the other two suppliers. The onus to substantiate the genuineness of the purchases squarely rests upon the appellant. The general contention that, since the corresponding sales have not been doubted, no adverse inference can be drawn with regard to the impugned purchases, is untenable. The allowability of purchases cannot be accepted merely on the strength of recorded sales, particularly when the impugned purchases constitute a specific and identifiable portion of the total purchases reported. The ratio of such disputed purchases to the overall purchases, when examined vis-à-vis the sales turnover declared by the appellant, does not ipso facto validate the genuineness of the transactions. Each purchase transaction must independently withstand scrutiny, and failure to substantiate the same with cogent and corroborative evidence cannot be cured merely by the existence of corresponding sales entries.

5.3.14 As regards production of evidences, mere production of GST returns and proof of payment through banking channels, without supporting evidence establishing the identity, creditworthiness, and business activity of the supplier, cannot by itself discharge this burden. The evidentiary deficiency in respect of M/s RKG Earth Movers, therefore, remains unaddressed and cannot be overlooked. In view of the foregoing discussion, it is evident that the appellant has failed to discharge the primary onus cast upon it to substantiate the genuineness of the purchases claimed from M/s RKG Earth Movers. Mere filing of GST returns and proof of payment through banking channels, in the absence of further supporting evidence, is insufficient to conclusively establish the genuineness of the transactions. Accordingly, the disallowance made by the Assessing Officer in respect of purchases amounting to Rs.1,10,97,410/- from M/s RKG Earth Movers is found to be justified and is hereby sustained.

5.3.15 To conclude, in view of the foregoing discussion, when the Tally data found during the course of search has been substantially reconciled in respect of two concerns – M/s PS Blue Metals and M/s Shri Chennai Mines; when the allegation of excessive mining is unsupported by any material evidence; when the absence of inward movement stands satisfactorily explained in light of direct dispatch to customers; when the two supplier has confirmed the transactions and furnished statutory records; when one of the supplier himself was subjected to search and assessment of the two concerns was made by the same Assessing Officer; and when the impugned transactions have been accepted by the GST authorities without any adverse finding — the cumulative effect of these facts leaves no room to sustain the disallowance of purchase of blue metal aggregates from M/s PS Blue Metals and M/s Shri Chennai Mines. As such, the appellant gets relief of Rs.8,32,31,270/- out of the total addition of Rs.9,43,28,680/- made under this head. Accordingly, ground No.2 is partly allowed.”

59. The relevant findings and observations of the Ld.CIT(A), whereby the addition of Rs.39,02,344/- made by the AO, representing the payments pertaining to M/s.RKG Earth Movers as reflected in the seized Tally data for the A.Y.2020-21, came to be deleted, are reproduced hereunder:

“6. The last Ground No.4 is against the disallowance of Rs.39,02,344/-, being payments to M/s RKG Earth Movers, as reflected in the seized Tally. The AO had not made any specific comments on these payments but has broadly analysed the figures appearing in the seized Tally and made the disallowance. Against this disallowance, the appellant submits that the payments to M/s RKG Earth Movers are towards aggregate purchases; that the said payments are made through proper banking channels leaving no scope for any inference of cash transactions / nongenuine transactions; that the AO had not disputed the genuineness of the payments or that the expenditure was incurred for any purpose other than their legitimate business; that the AO had not rejected the books of account and the sales declared are accepted as such and therefore, partial disallowance of business expenditure without identifying the specific discrepancy cannot be sustained.

6.1 I have gone through the assessment order and the submissions of the appellant. As discussed in para 5.3 above, the total purchases from M/s RKG Earth Movers were disallowed in the absence of any corroborative evidences furnished by the appellant, as was done while substantiating the purchases from the other two parties. Since the entire purchases of Rs.1,10,97,410/- from this party for the year have already been held to be unsubstantiated and disallowed, any further disallowance of payments made to the same party would result in duplication of addition. Once the purchases themselves stand disallowed, the corresponding payments cannot again be subjected to separate disallowance. Therefore, the addition, to the extent it pertains to the disallowance of payments made to M/s RKG Earth Movers over and above the purchase disallowance, is not sustainable and is accordingly deleted. As such, Ground No.4 is allowed.”

60. The relevant observations and findings of the Ld.CIT(A), while upholding the addition of Rs.1,06,81,717/- made by the AO for the A.Y.2021-22, are reproduced hereunder:

“5.6 I have carefully examined the assessment order and the submissions made by the appellant. Though the general observations of the AO for disbelieving the purchases that the appellant had access to sufficient boulders through alleged excessive mining from its own quarry without incurring expenses are not so acceptable and does not meet the threshold of evidentiary standards required to sustain an addition, added to the submissions made by the appellant in this regard for earlier years, at the same time the appellant had also not furnished any further evidences in respect of purchases, except invoices, from M/s RKG and submitted that these cash purchases account for only 4.75% and be accepted. !n the absence of further corroborative evidence to prove the genuineness of the sales like the GST assessment order, income-tax particulars of the supplier, or any other independent documentary evidence to establish the genuineness of the transactions, as was done in the case of the other two suppliers for earlier assessment years, the claim of the appellant with regard to purchases cannot be accepted.

5.7 The general contention that, since the corresponding sales have not been doubted, no adverse inference can be drawn with regard to the impugned purchases is untenable. The allowability of purchases cannot be accepted merely on the strength of recorded sales, particularly when the impugned purchases constitute a specific and identifiable portion of the total purchases reported. The ratio of such disputed purchases to the overall purchases, when examined vis-à-vis the sales turnover declared by the appellant, does not ipso facto validate the genuineness of the transactions. Each purchase transaction must independently withstand scrutiny, and failure to substantiate the same with cogent and corroborative evidence cannot be cured merely by the existence of corresponding sales entries.

5.8 As regards production of evidences, mere production of invoices, without supporting evidence establishing the identity, creditworthiness, and business activity of the supplier, cannot by itself discharge this burden. The evidentiary deficiency in respect of M/s RKG Earth Movers, therefore, remains unaddressed and cannot be overlooked. In view of the foregoing discussion, it is evident that the appellant has failed to discharge the primary onus cast upon it to substantiate the genuineness of the purchases claimed from M/s RKG Earth Movers.

5.9 The above discussion leaves for consideration the alternate claim of the appellant that only the profit element embedded in the alleged purchases should be disallowed. However, from the submissions and material placed on record, it is evident that the appellant has admitted that the impugned transactions were cash purchases. The issue in the present case, therefore, is not merely one of possible inflation of purchase price through accommodation entries, but one where the genuineness and verifiability of the transactions themselves remain unsubstantiated. In circumstances where the appellant has failed to furnish supporting documentary evidence such as confirmations, transportation details, delivery challans, or other corroborative material to establish the identity of the supplier and the genuineness of the transactions, the deficiency is not confined to estimation of excess profit. The foundational requirement of proving the authenticity of the purchases has not been discharged.

5.10 Accordingly, this is not a fit case for applying or estimating a profit percentage on the alleged purchases, particularly when the quantum of purchases from M/s RKG accounts for only 4.75% of the total sales, as worked out by the appellant. Given the relatively small proportion of such purchases vis-à-vis the overall turnover, and considering the nature of the business, there exists a reasonable possibility that the appellant might not have procured the material at all and merely recorded payments against such purchases. When there is an admitted cash outflow, but no credible evidence demonstrating the corresponding inflow of goods/boulders—such as transportation details, delivery challans, stock register entries, or confirmation from the supplier—the genuineness of the transactions remains unproved. In such circumstances, the defect goes to the root of the claim and is not amenable to estimation of profit element. Accordingly, the balance addition made by the Assessing Officer (after considering the amount of Rs.1 crore admitted by the appellant in the revised return) in respect of purchases from M/s RKG at Rs.1,06,81,717/- is sustained in full. The ground No 3 to 3.4 are dismissed.”

61. Being aggrieved by the impugned order of the Ld.CIT(A), whereby substantial additions were deleted and the remaining additions were sustained, both the Revenue as well as the assessee have preferred the present cross appeals before this Tribunal.

62. The Ld.DR, Ms.Nayani Swapna, CIT, appearing on behalf of the Revenue, relied upon the assessment order as well as the grounds of appeal raised by the Revenue. The Ld.DR submitted that the Ld.CIT(A) was no justified in deleting the addition made by the AO towards alleged bogus purchases of aggregates.

63. The Ld.DR contended that the Ld.CIT(A) failed to properly appreciate the findings recorded by the AO regarding the lack of genuineness of the impugned purchase transactions. According to the Ld.DR, the AO had categorically recorded that the assessee failed to produce primary evidence, such as transportation documents, inward stock registers, delivery challans or any other evidence establishing the actual movement and receipt of goods. The Ld.DR further submitted that the purchases were claimed to have been made from a related concern, wherein Shri Subramani Perumal, a partner of the assessee-firm, was the proprietor/partner, thereby increasing the possibility of accommodation entries. In such circumstances, mere production of ledger accounts or self-serving confirmations could not discharge the burden cast upon the assessee to establish the genuineness of the purchases.

64. The Ld.DR further submitted that the Ld.CIT(A) accepted the explanation of the assessee primarily on the basis of GST returns and confirmation furnished by the supplier concern, without undertaking any independent verification of the transactions. According to the Ld.DR, the object and scope of proceedings under the GST law are entirely distinct from those under the Income-tax Act. Merely because the transactions were reflected in the GST returns or accepted by the GST authorities would not, by itself, establish the genuineness of the purchases for the purposes of the Income-tax Act. At best, the GST records only demonstrate that the supplier had collected and remitted GST on the alleged supplies, which, according to the Ld.DR, cannot be regarded as conclusive proof of the actual movement and delivery of goods.

65. The Ld.DR further submitted that the findings of the Ld.CIT(A) also overlooked the statements recorded during the course of search proceedings. The Ld.DR pointed out that Shri Perumal Subramani had stated that his proprietary concern, M/s.P.S.Blue Metals, was engaged in trading of blue metal aggregates procured from various third-party suppliers for onward supply to the assessee-firm. However, neither the assessee nor Shri Perumal Subramani had furnished the particulars of such third-party suppliers, including their names, addresses, PAN, purchase invoices or transportation details. According to the Ld.DR, in the absence of these basic evidence, the source of the goods itself remained unverified, thereby casting serious doubt on the genuineness of the purchase transactions.

66. The Ld.DR, therefore, submitted that the failure of the assessee to establish the identity and capacity of the alleged suppliers, coupled with the absence of evidence regarding the actual movement of goods, clearly indicated that the impugned purchases were not supported by credible evidence and could well represent accommodation entries. The Ld.DR contended that reliance merely on ledger accounts, GST returns and confirmations from a related party could not substitute independent corroborative evidence, particularly in the context of search proceedings involving related-party transactions. The Ld.DR, therefore, submitted that the Ld.CIT(A) erred in treating the purchases as genuine without addressing these material deficiencies and prayed that the order of the AO on this issue be restored.

67. In so far as the additions sustained by the Ld.CIT(A) for the AY(s) 202021 and 2021-22 are concerned, the Ld.DR placed reliance on the findings recorded in the impugned appellate orders and submitted that the same are well-reasoned and do not call for any interference. The Ld.DR therefore, prayed that the orders of the Ld.CIT(A), to the extent they sustain the additions, be upheld.

68. Per contra, Shri R.Venkata Raman, CA, the Ld.AR appearing on behalf of the assessee, strongly supported the impugned order of the Ld.CIT(A), in so far as it relates to the deletion of the additions made for the AY(s) 2018-19, 2019-20 and 2020-21. The Ld.AR submitted that the findings recorded by the Ld.CIT(A) are based upon a proper appreciation of the facts and material available on record, are supported by cogent reasons, and do not suffer from any legal or factual infirmity warranting interference by this Tribunal.

69. The Ld.AR submitted that the assessee, Shri Subramani Perumal, Proprietor of M/s.P.S. Blue Metals, and M/s.Shri Chennai Mines were all subjected to search proceedings on the same date, namely, 02.03.2022. It was contended that no incriminating material whatsoever was found or seized from any of the searched premises to establish that the purchases of aggregates made by the assessee from M/s.P.S.Blue Metals or M/s.Shri Chennai Mines were either fictitious or represented accommodation entries. It was further submitted that the AO had neither conducted any independent investigation nor brought on record any material to establish that the assessee had indulged in bogus purchases or accommodation transactions. According to the Ld.AR, in the complete absence of any incriminating evidence, the additions made by the AO rest merely upon suspicion and conjectures and, therefore, the Ld.CIT(A) was fully justified in deleting the same.

70. Replying to the submissions advanced by the Ld.DR, the Ld.AR submitted that even before this Tribunal, the Revenue has failed to place any material on record to demonstrate that the purchases treated as bogus by the AO were, in fact, non-genuine. It was submitted that merely because the purchases were made from related concerns, the same could not, by itself, constitute a valid ground to treat the transactions as bogus.

71. Inviting our attention to page 7 of the assessment order for the A.Y.2018-19, the Ld.AR pointed out that the AO himself had examined Shri Subramani Perumal during the course of assessment proceedings, wherein he had categorically confirmed the supply of aggregates to the assessee. It was submitted that it is not even the case of the Revenue that Shri Subramani Perumal had admitted that the transactions were fictitious or represented accommodation entries.

72. The Ld.AR further submitted that the assessee had duly discharged the burden cast upon it under the provisions of the Act by producing overwhelming documentary evidence establishing the genuineness of the purchases. It was submitted that the purchases are duly reflected in the assessee’s GSTR-2A; the corresponding tax invoices containing GST particulars have been furnished; the ledger account of the supplier appearing in the books of the assessee evidences the transactions; the corresponding sales have been duly recorded in the books of M/s.P.S.Blue Metals and offered to tax; payments have been made entirely through normal banking channels; and the supplier has accounted for the receipts in its regular books of account. According to the Ld.AR, each link in the chain of transactions thus stands fully corroborated by contemporaneous documentary evidence.

73. The Ld.AR further invited our attention to the proceedings before the GST authorities and submitted that the very same transactions between the assessee and M/s.P.S.Blue Metals were subjected to scrutiny by the State Tax Department and were accepted as genuine. Likewise, in the assessment proceedings relating to the supplier, the Assistant Commissioner (State Tax) had also accepted the sales effected to the assessee without recording any adverse finding. It was therefore contended that once the competent statutory authority entrusted with examining indirect tax transactions had accepted the genuineness of the purchases, the AO could not have independently characterised the same as bogus without bringing any cogent material on record.

74. In support of the above proposition, the Ld.AR placed reliance upon the decision of the Hon’ble Bombay High Court in PCIT v. SVD Resins & Plastics Pvt. Ltd. and submitted that purchases cannot be disallowed merely on the basis of general information, suspicion or surmises and that due weight ought to be given to the findings recorded by the Sales Tax authorities wherever the transactions have been accepted by them. It was submitted that the ratio laid down therein squarely applies to the facts of the present case.

75. The Ld.AR further submitted that no incriminating material was found during the course of search indicating that the impugned purchases were fictitious or represented accommodation entries. It was argued that no material has been brought on record to establish that the assessee had procured materials from the grey market or that any cash had flown back from the supplier to the assessee. Even the sworn statement of Shri P. Subramani recorded during the course of search does not contain any admission that the purchases were bogus. According to the Ld.AR, the additions are therefore founded entirely upon suspicion and presumptions unsupported by any tangible evidence.

76. Placing reliance upon the judgment of the Hon’ble Gujarat High Court in CIT v. M.K. Brothers, the Ld.AR submitted that in the absence of any material to establish that payments made through banking channels had returned to the assessee in cash, purchases cannot be treated as bogus merely on suspicion. Similar principles, according to the Ld.AR, have also been reiterated by the Hon’ble Bombay High Court in the case of SVD Resins & Plastics Pvt. Ltd. (supra).

77. The Ld.AR further submitted that the AO has accepted the books of account maintained by the assessee as well as the sales disclosed therein. The turnover declared by the assessee has not been disturbed, nor has any adverse finding been recorded with regard to the quantitative details, stock records or sales effected during the relevant years. It was argued that once the corresponding sales have been accepted, the purchases resulting in such sales cannot simultaneously be regarded as non-genuine.

78. In support of the aforesaid contention, the Ld.AR placed reliance upon the decisions of the Hon’ble Bombay High Court in CIT v. Nikunj Eximp Enterprises (P.) Ltd. and PCIT v. Nitin Ramdeoji Lohia, wherein it has been consistently held that where the sales have been accepted and the purchases are duly supported by books of account, invoices and banking transactions, no addition towards alleged bogus purchases can be sustained merely on the basis of doubts entertained by the AO regarding the supplier.

79. The Ld.AR also submitted that the gross profit declared by the assessee during the relevant assessment years is broadly in line with the gross profit disclosed in the preceding years and there is no abnormal suppression of profits. It was contended that if the entire purchases is disallowed, the resultant gross profit would exceed 21%, which is commercially unrealistic and wholly inconsistent with the prevailing standards in the mining industry. Such an artificial enhancement of profitability itself demonstrates the unsustainability of the approach adopted by the AO.

80. Dealing with the specific observations made in the assessment order, the Ld.AR submitted that the allegation regarding excessive mining operations is not supported by any technical report, survey report or any finding recorded by the competent regulatory authorities. Likewise, the observation regarding the absence of inward movement of materials proceeds on an erroneous appreciation of the business model adopted by the parties, since the aggregates were directly dispatched from the crushing unit of M/s.P.S.Blue Metals to the customers of the assessee, and therefore there was no occasion for the goods to physically enter the quarry premises of the assessee. It was further submitted that the inability of the supplier to furnish details relating to its own vendors cannot be held against the assessee, particularly when the supplier is an existing taxable entity whose sales have been accepted by the GST authorities. Summing up his arguments, the Ld.AR submitted that the AO has neither rejected the books of account maintained by the assessee nor disproved any of the documentary evidence produced in support of the purchases. No cash trail has been established, no incriminating material has been unearthed during the course of search, and neither the sales nor the consumption of materials has been disputed. The impugned additions, according to the Ld.AR, are thus based entirely on assumptions, conjectures and suspicion, which cannot legally sustain an addition under the provisions of the Act.

81. In the light of the aforesaid submissions, the Ld.AR prayed that the well-reasoned order passed by the Ld.CIT(A) deleting the additions made towards alleged bogus purchases be upheld and that the grounds raised by the Revenue challenging such deletion be dismissed.

82. In so far as the addition of Rs.1,10,97,410/- pertaining to the purchases made from M/s.R K G Earth Movers for the A.Y.2020-21 is concerned, the Ld.AR submitted that the impugned purchases are duly supported by GST invoices and have been duly accounted for in the books of account. It was further submitted that the goods so purchased have been utilized in the course of business and the corresponding sales arising therefrom have been accepted by the Revenue without any adverse finding. Therefore, according to the Ld.AR, once the sales have been accepted as genuine, the corresponding purchases cannot, in the absence of any cogent material to the contrary, be treated as bogus. In support of the said contention, the Ld.AR placed reliance on various judicial precedents and contended that the Ld.CIT(A) was not justified in sustaining the addition of Rs.1,10,97,410/-. Accordingly, the Ld.AR prayed for deletion of the impugned addition.

83. With regard to the addition of Rs.1,06,84,717/- sustained by the Ld.CIT(A) for the A.Y.2021-22, the Ld.AR submitted that the addition of Rs.1,06,84,717/- towards alleged bogus purchases was wholly unjustified both on facts and in law. It was contended that the assessee had disclosed a GP ratio of 20.38% during the year under consideration as against 19.32% in the immediately preceding assessment year. ince the GP ratio had improved and there was no abnormal fall in profitability, the allegation of inflation of purchases was devoid of merit. It was further submitted that if the entire disputed purchases were disallowed, the resultant GP ratio would increase to 25.14%, which was commercially unrealistic and unsupported by any industry benchmark.

84. The Ld. AR pointed out that, considering certain deficiencies in the supporting documents relating to aggregate purchases, the appellant had voluntarily disallowed a sum of Rs.1,00,00,000/-, resulting in an enhanced GP ratio of 22.68%, which was substantially higher than that of the earlier year. Therefore, the further disallowance of Rs.1,06,84,717/- was unwarranted. Reliance was placed on the decision of the Coordinate Agra Bench of the Tribunal in Shri Shanti Swaroop Jain v. CIT, wherein it was held that no addition towards bogus purchases could be sustained in the absence of conclusive evidence, particularly when the declared GP ratio was reasonable and the addition resulted in an abnormally high GP ratio.

85. The Ld.AR further submitted that the corresponding sales had been fully accepted by the AO and the books of account, duly audited u/s.44AB of the Act, had not been rejected. It was argued that the impugned purchases had been converted into sales during the relevant previous year and the AO had not disputed the sales disclosed by the appellant. Therefore, once the sales were accepted as genuine, the corresponding purchases could not be treated as bogus, as no business could effect sales without procuring the corresponding goods. Reliance was placed on the decisions of the Hon’ble Bombay High Court in PCIT v. Nitin Ramdeoji Lohia and CIT v. Nikunj Eximp Enterprises (P.) Ltd., as well as the decisions of the Kolkata and Chennai Benches of the Tribunal in ITO v. Sri Puspal Kumar Das and Syed Mubarak Ali v. ACIT, to contend that where sales are accepted and books are not rejected, disallowance of purchases is unsustainable.

86. Without prejudice to the above submissions, the ld.AR contended that even assuming there were deficiencies in the purchase documentation, settled judicial principles permitted only the profit element embedded in such purchases to be brought to tax and not the entire purchase value. Reliance was placed on the judgments of the Hon’ble Gujarat High Court in CIT v. Bholanath Polyfab (P.) Ltd. and PCIT v. Sunil Mittal (HUF), wherein it was held that only the profit element embedded in purchases from non-genuine parties could be assessed. The ld.AR further relied upon the recent decision of the coordinate bench of this Tribunal in DCIT v. Radiance Realty Developers India Ltd., wherein the Tribunal upheld the estimation of only the embedded profit in alleged bogus purchases, and on the judgment of the Hon’ble Madras High Court in CIT v. SPL Infrastructure Pvt. Ltd., wherein the Court held that complete disallowance of expenditure leading to unrealistic profitability was not justified and that only a reasonable estimate of profit could be made based on past results.

87. The Ld.AR submitted that if the GP ratio of 20.38% was applied to the disputed purchases of Rs.2,06,84,717/-, the embedded profit would work out only to Rs.42,15,545/-. Since the appellant had already voluntarily offered a sum of Rs.1,00,00,000/- for taxation, which was substantially higher than the possible profit element, no further disallowance was warranted. It was, therefore, prayed that the addition of Rs.1,06,84,717/- made u/s.37 of the Act be deleted in full.

88. We have duly considered the rival contentions, perused the assessment orders, the impugned orders passed by the Ld.CIT(A), the voluminous paper books filed before us, the documentary evidences placed on record, the written submissions, the judicial precedents relied upon by the respective parties and the entire material available on record.