Reverse Charge Mechanism which proved to be most Draconian provision has been now relaxed, of course temporarily till 31st March’ 2018, as per the decision taken at 22nd GST Council meeting on 6th Oct’2017.

Businesses feeling very uncomfortable as on the expenses side there are hundreds of petty purchases mostly from un-registered dealers and on such purchases the buyer as a recipient has to discharge the liability of tax on reverse charge. Finding corresponding HSN / SAC Codes and the rates for such large number of purchases become a herculean task. Since the Input Tax Credit (ITC) on such payments made by the recipient are allowed, effectively there is revenue benefits to Govt, exchequer, leaving the entire exercise worthless but proving most troublesome for everyone. Now however the Govt under tremendous pressure from all the corners made a wise decision.

Let us discuss in this article about how those relaxations benefit the larger section of business.

Even earlier, similar provisions of Reverse Charge are available in Service Tax for the services like, Insurance agent, Services of a director to a company. Manpower supply, Goods Transport Agencies, Non-resident service any service involving aggregators. Reverse Charge was applicable only on Services and not on Goods. However now under the GST the scope of Reverse Charge is broadened to cover both Goods & Services. The objective is mostly to bring all the suppliers under registration as the recipients mostly the corporates forcing the small suppliers to register.

Reverse Charge under GST

“Reverse Charge” as defined in Sec 2(98) of CGST Act means the liability to pay tax by the recipient of supply of goods or services or both instead of the supplier of such goods or services or both under sub-section (3) or sub-section (4) of section 9, or under sub-section (3) or subsection (4) of section 5 of the Integrated Goods and Services Tax Act.

From the definition it is clear that in case of Reverse Charge, the Recipient has to pay Tax instead of the Supplier.

The definition refers to following Two aspects :

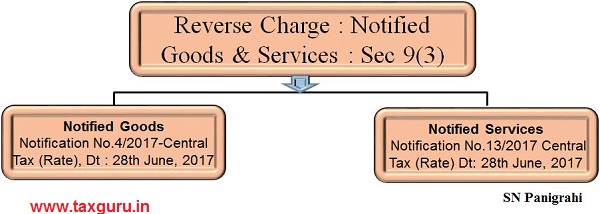

1. Supplies under Sec 9.3 of CGST Act or Sec 5.3 of IGST Act – which refers to Notified Goods or Services that the Govt. may Notify Separately for Supplies that falls under Reverse Charge

2. Supplies under Sec 9.4 of CGST Act or Sec 5.4 of IGST Act – which refers to Supplies from Un-Registered Person

Under Sec 9(3) of CGST Act, Reverse charge shall be applicable in case of supply of notified goods or services or both.

As per Sec 9(4) of CGST Act, the tax in respect of the supply of taxable goods or services or both by a supplier, who is not registered, to a registered person shall be paid by such person on reverse charge basis as the recipient.

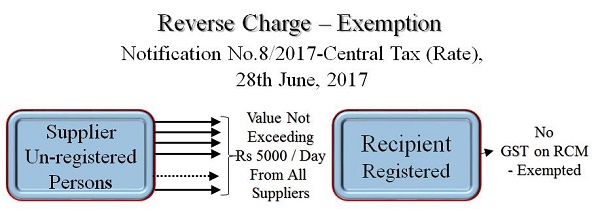

Partial Relaxation Vide Notification : 8/ 2017 – Central Tax Rate, 28th June’ 17

GST payable (under reverse charge) on local procurements (intra-State) from unregistered persons exempted if the aggregate value of such local procurements from all vendors does not exceed INR 5000 per day.

No such exemption for inter-state procurements as vendors making inter-state supplies would mandatorily be required to be registered under GST law.

Complete Exemption to all Registered Persons

As per the GST Council recommendations made on its 22nd Council meeting on 6th Oct’2017, following notifications are issued to defer the applicability of Reverse Charge on Purchases from Un-registered Dealers.

- Notification No. 38/2017–Central Tax (Rate), 13th October, 2017

- Notification No. 32/2017- Integrated Tax (Rate), 13th October, 2017

- Notification No. 38/2017–Union Territory Tax (Rate), 13th October, 2017

Corresponding notifications by state authorities also shall follow.

According to the notifications Tax applicability on Reverse Charge on on Purchases from Un-registered Dealers is suspended till 31st March, 2018.

This Exemption is applicable to All the Registered Persons.

Reverse Charge under Sec 9.3 of CGST Act & Sec 5.3 of IGST Act Shall Continue

Reverse charge still applicable under above provisions as per following Notifications :

Notification No. 4/2017- Central Tax (Rate), Date : 28th June, 2017 – for Supply of Goods like Cashew nuts, not shelled or peeled, Bidi wrapper leaves (tendu), Tobacco leaves, Silk Yarn and Supply of lottery.

Notification No. 13/2017- Central Tax (Rates) Date: 28.06.2017 – for Supply of Services like Any person who is located in a non-taxable territory Goods Transport Agency (GTA), An individual advocate or firm of advocates, An arbitral tribunal, Sponsorship services, Government or local authority, A director of a company or a body corporate, An insurance agent, A recovery agent – to a banking company or a financial institution or a non-banking financial company, Author or music composer, photographer, artist, etc, Taxi driver or Rent a cab operator .

Comments :

1. The Suspension of Applicability of Reverse Charge on Supplies from Un-Registered is temporary till 31st Mar’2018 only. It is suggested Govt should consider to scrap the provision permanently.

2. The Suspension is applicable Prospectively ie effective from 13th Oct’17

3. If it is effective from 13th Oct’ 2017, then while filling the returns for the month of October one has to pay tax on RCM till 12th of October on supplies made by un-registered dealers.

4. Supplies covered under notified Goods & Services as per Sec 9.3 of CGST Act and Sec 5.3 of IGST Act still continue and the Recipient of such supplies shall be liable to pay the Tax on Reverse Charge basis.

Disclaimer : The views and opinions; thoughts and assumptions; analysis and conclusions expressed in this article are those of the authors and do not necessarily reflect any legal standing.

Author : SN Panigrahi, GST Consultant, Practitioner, Corporate Trainer & Author

Can be reached @ snpanigrahi1963@gmail.com

Author Bio

What about IGST to be paid on RCM Basis on Import of Service? Does this notification cover Imports also?

RCM suspension is very good to run GST in smooth way instead of complicate to all registered customer but still i have confuse whether RCM suspension notification is approved or not. please provide link if you have for same.

RCM must be repealed from 01.07.17 forever. All readers are kindly requested to support the same. The author has very well explained the hardships of RCM.

RCM CONCEPT SHOULD BE ABOLISHED FROM THE RETROSPECTIVE DATE JULY 2017 THERE IS MOST CONFUSION TO INDUSTRY AND TRADERS AND ALSO TO CA AND TAX CONSULTANT WHEN FILING RETURNS DUE TO RCM CONCEPT THE ENERGY OF THE BUSINESS MAN IS COMPLETELY WASTED AND MORE COMPLICATION IN FILING GST RETURNS AND MY REQUEST TO MODIJI IS THAT RCM CONCEPT SHOULD BE ELIMINATED FOR EVERY FOR SMOOTH AND EASY RUNNING THE BUSINESS AND TRY TO DO MORE BUSINESS AND TO GENERATE REVENUE

THE RCM SUSPENSION SHOULD BE MADE FROM RETROSPECTIVE DATE OF JULY 17. IMPLEMENTATION PROSPECTIVELY WILL CREATE MORE NUISANCE. WHAT EVER RCM PAYMENTS MADE ANY CAN GET INPUTS AND WILL BE SET OFF AGAINST THE OUTPUT LIABILITY OF FUTURE PERIODS AS WELL..

ALSO RCM ON TRANSPORTATION AND SUBCONTRACTOR WORKS – LABOUR ETC BE ABOLISHED FROM JULY17 – OTHER WISE CONFUSIONS AND LITIGATION WILL REMAIN.

In comments, the date is mentioned as 31.03.2017, instead of 31.03.2018.

DAILY UPDATE