1. Introduction

The GST ecosystem has taken another important digital step for the hospitality sector. With Notification No. 05/2025 – Central Tax (Rate), dated January 16, 2025, the Government introduced a mechanism for declaring hotel accommodation premises as “Specified Premises.”

Initially, these declarations were required to be filed manually with the jurisdictional GST authority. However, the GST Department has now enabled electronic filing of these declarations on the GST Portal, bringing much-needed clarity, transparency, and ease of compliance for hotel service providers.

This article explains who can file, which annexure applies, timelines, step-by-step filing process, and important compliance points—all in one place.

2. What is a “Specified Premises”?

For GST purposes, a specified premises refers to hotel accommodation premises that are declared by the supplier under the relevant GST notification, impacting the rate of tax applicable on accommodation services.

Correct declaration is crucial, as wrong or missed declaration may lead to tax disputes, demand notices, and penalties.

3. Who Can Opt and File the Declaration?

i. Eligible Persons

The facility is available to the following categories supplying hotel accommodation services:

-

- Regular GST taxpayers

- Active registrations

- Suspended registrations

- Applicants for new GST registration who wish to declare premises as specified premises

- Regular GST taxpayers

ii. Not Eligible

The following cannot use this facility:

-

- Composition taxpayers

- TDS / TCS taxpayers

- SEZ units or developers

- Casual taxable persons

- Taxpayers with cancelled GST registration

4. Types of Declarations Available on GST Portal

i. Annexure VII – Opt-In Declaration (Existing Registered Persons)

-

- For already registered GST taxpayers

- Used to declare premises as specified premises for a subsequent financial year

ii. Annexure VIII – Opt-In Declaration (New Registration Applicants)

-

- For persons applying for GST registration

- Declaration effective from the date of registration

iii. Annexure IX – Opt-Out Declaration

-

- Will be enabled separately in due course

5. Timeline for Filing Declarations

A. Existing Registered Taxpayers – Annexure VII

-

- Filing window: 1st January to 31st March of the preceding financial year

- For FY 2026–27:

Filing allowed from 01.01.2026 to 31.03.2026

B. New GST Registration Applicants – Annexure VIII

-

- Must be filed within 15 days from ARN generation

- Allowed even if:

- GSTIN not yet allotted

- Application is under processing

- Not allowed if the registration application is rejected

- After 15 days lapse → filing possible only during Annexure VII window (Jan–Mar)

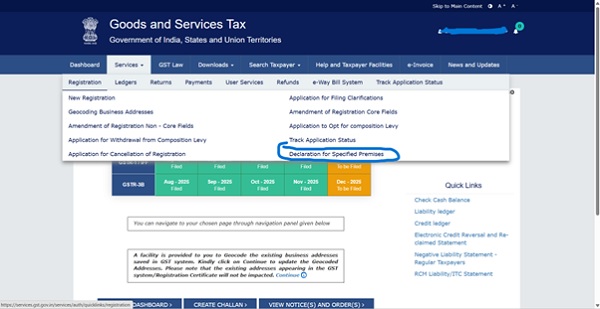

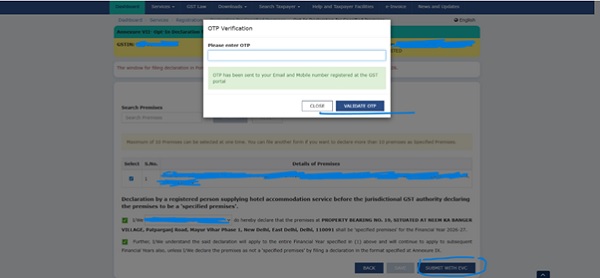

6. Step-by-Step: How to File a Declaration on the GST Portal

i. Log in to the GST Portal

ii. Go to:

Services → Registration → Declaration for Specified Premises

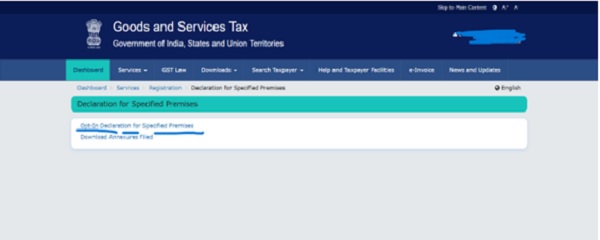

iii. Choose one option:

- Opt-In Declaration for Specified Premises, or

- Download Annexure Filed

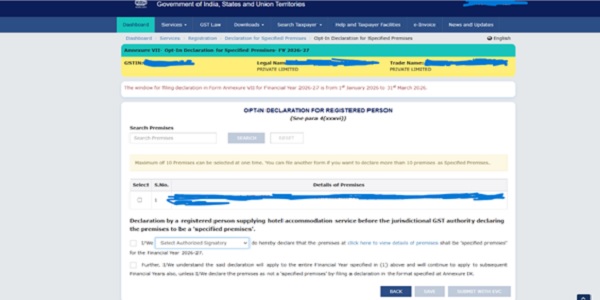

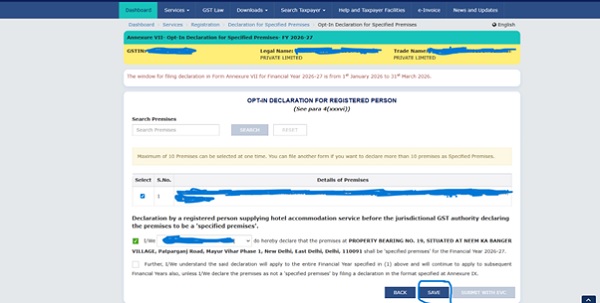

iv. Select eligible premises

v. Fill in declaration details and save the form

vi. Submit using EVC

vii. On successful submission, an ARN is generated

7. Important Points You Must Not Miss

- A maximum of 10 premises can be selected in one declaration

- If more premises exist → additional declarations can be filed

- Separate PDF & reference number generated for each premise

- Left-out premises can be added later within the same financial year window

- Suspended registrations can file

- Cancelled registrations cannot file

- Once opted, the declaration continues for future years automatically

- Unless Annexure IX (Opt-Out) is filed within the prescribed time

8. Downloading Filed Declarations

- Path:

Services → Registration → Declaration for Specified Premises → Download - Annexure VII / VIII available for download

- Each declared premise has a separate reference number

9. Email & SMS Confirmation

On successful filing:

- Email and SMS alerts are sent

- Intimation goes to all authorised signatories

10. Special Notes for FY 2025–26 & FY 2026–27

- For FY 2025–26

- Declarations were filed manually

- Since the online facility is now live, re-filing electronically is mandatory for:

FY 2026–27 (01.01.2026 to 31.03.2026)

- First-Time Declaration of Specified Premises

- Taxpayers declaring specified premises for the first time must:

-

-

- File Annexure VII

- During 01.2026 to 31.03.2026

- Applicable for FY 2026–27

-

11. Why This Update is Important

- Eliminates manual interface with tax officers

- Ensures digital trail & transparency

- Reduces litigation on hotel accommodation GST rates

- Helps businesses plan pricing & compliance in advance

12. Conclusion

The online availability of Specified Premises Declarations on the GST Portal is a significant compliance relief for hotel accommodation service providers. However, missing timelines or filing incorrect annexures can create serious GST exposure.

If you are:

- A hotel owner

- A GST consultant

- A professional advising a hospitality client

Mark your calendar for 1st January – 31st March 2026 and ensure timely electronic filing for FY 2026–27.

Staying proactive today can save penalties, notices, and unnecessary stress tomorrow.

Disclaimer: –

The information provided is for educational purposes and should not be considered as professional advice. The author shall not be liable for any direct, indirect, special, or incidental damage resulting from, arising out of, or in connection with the use of the information.

Author Bio