Section 69 read with Section 132: Provision pertaining to arrest under the CGST Act, 2017

Penal provisions always attract in case of violation of Provisions and Rules framed in an Act. GST Act is no exception to this statement,Section 69 read with Section 132 of the GST Act,2017 and rules made thereunder deals with provision pertaining to arrest under the Act for the violation. Offences relating to arrest under GST law can be broadly classified under two categories:

| Point of Difference | Non Cognizable and Bailable Offences | Cognizable and Non Bailable Offences |

| Definition | Non cognizable offences are those where a person cannot be arrested without warrant issued by competent authority. | Cognizable offences are those offences where a person can be arrested without any arrest warrant. |

| Provision under CGST Act, 2017 | Section 132(4) of the Act states that all offences under the Act are Non Cognizable and Bailable except offences referred to in section 132(5).

Sec. 132(5): Where the amount of tax evaded or input tax wrongly availed does not exceed Rs. 5crore, such offences shall be considered Non Cognizable and Bailable. |

Section 132 (5) of the Act states that all offences specified in clause (a) or clause (b) or clause (c) or clause (d) of sub-section (1) of section 132 of the Act and punishable under clause (i) of that sub-section shall be cognizable and non-bailable.

Where the amount of tax evaded or input tax wrongly availed exceeds Rs. 5crore, such offences shall be considered Cognizable and Non Bailable. |

| Who grants bail? | Deputy Commissioner or Assistant Commissioner has power to grant bail in case of offences which are non-cognizable and bailable under GST law. | Such person can be arrested on the spot without any arrest warrant. Where an assessee has reason to believe that he may be arrested on accusation of having committed a non-bailable offence under section 132(5), he can seek anticipatory bail by filing a petition under section 438 of CrPC.

Anticipatory bail may be granted subject to certain conditions:

|

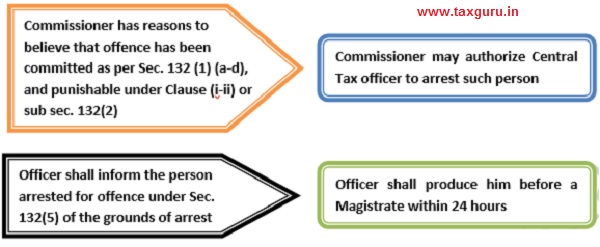

Section 69: Power to Arrest

In a landmark judgement passed by The Hon’ble Supreme Court in the matter of D.K. Basu v State of West Bengal [1997] 1 SCC 416 has prescribed eleven guidelines given below pertaining to arrest a person under any law. Therefore while exercising his power to arrest u/s 69 of the Act GST commissioner should ensure the compliance of guidelines provided by Supreme Court in the case D.K. Basu.

- Police personnel who make the arrest and handle the interrogation of the arrested person must wear precise, visible and clear identifications and identification labels with their designations. Details of all personnel handling the interrogations of the arrested person must be recorded in a register.

- That the police officer making the arrest of the detainee will prepare a memorandum of arrest at the time of the arrest and said memo will be witnessed by at least one witness who may be a member of the family of the arrested person or a respectable person from the locality from where the arrest is made. It must also be signed by the detainee and must contain the time and date of the arrest.

- A person who has been arrested or detained and is detained at a police station or interrogation center or other confinement, shall have the right to have a friend or relative or other person known to him or who has an interest in his well-being will be informed, as soon as possible, that you have been arrested and are being detained in a particular place unless the witness crediting the arrest memorandum is himself a friend or relative of the arrested.

- Police must notify a detainee’s time, place of detention, and place of custody where the detainee’s next friend or relative lives outside the district or city through the District’s Legal Aid Organization and station. Police of the affected area telegraphically within the period of 8 to 12 hours after the arrest.

- The person arrested must be made aware of his right to have someone informed of his arrest or detention as soon he is put under arrest or is detained.

- An entry must be made in the Case Diary at the place of detention regarding the arrest of the person which shall also disclose the name of the next friend of the person who has been informed of the arrest and the names and particulars of the police official in whose custody the arrestee is.

- Upon request, the Arrestee must also be examined at the time of his arrest and major and minor injuries, if present on his body, must be recorded at that time. The “Inspection Memo” must be signed by both the detainee and the arresting police officer and a copy must be provided to the detainee.

- The detainee must undergo a medical examination by a trained physician every 48 hours while in custody by a physician on the panel of approved physicians appointed by the Director of Health Services of the State or Union Territory concerned.

- Copies of all documents, including the arrest memo, must be sent to the Magistrate for registration.

- The Arrestee may be allowed to meet with his attorney during the interrogation, although not throughout the interrogation.

- A Police Control Room must be provided at all central district and state offices, where the arresting officer must communicate information about the arrest and the place of custody of the arrested, within 12 hours after the arrest and in the Police Control Room Board, must be displayed on a visible notice board.

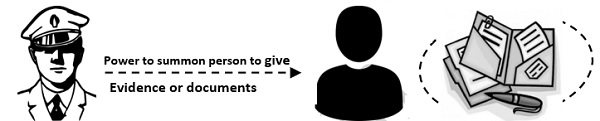

Section 70: Power to summon person to give evidence and produce documents

(1) The proper officer under this Act shall have power to summon any person whose attendance he considers necessary either to give evidence or to produce a document or any other thing in any inquiry in the same manner, as provided in the case of a civil court under the provisions of the Code of Civil Procedure, 1908 (5 of 1908).

(2) Every such inquiry referred to in sub-section (1) shall be deemed to be a “judicial proceedings” within the meaning of section 193 and section 228 of the Indian Penal Code

Section 71: Access to business premises

(1) Any officer under this Act, authorised by the proper officer not below the rank of Joint Commissioner, shall have access to any place of business of a registered person to inspect books of account, documents, computers, computer programs, computer software whether installed in a computer or otherwise and such other things as he may require and which may be available at such place, for the purposes of carrying out any audit, scrutiny, verification and checks as may be necessary to safeguard the interest of revenue.

(2) Every person in charge of place referred to in sub-section (1) shall, on demand, make available to the officer authorised under sub-section (1) or the audit party deputed by the proper officer or a cost accountant or chartered accountant nominated under section 66—

(i) such records as prepared or maintained by the registered person and declared to the proper officer in such manner as may be prescribed;

(ii) trial balance or its equivalent;

(iii) statements of annual financial accounts, duly audited, wherever required;

(iv) cost audit report, if any, under section 148 of the Companies Act, 2013;

(v) the income-tax audit report, if any, under section 44AB of the Income-tax Act, 1961; and

(vi) any other relevant record, for the scrutiny by the officer or audit party or the chartered accountant or cost accountant within a period not exceeding fifteen working days from the day when such demand is made, or such further period as may be allowed by the said officer or the audit party or the chartered accountant or cost accountant.

Section 132: Punishment for certain offences

Sec. 132(2): Where any person convicted of an offence under this section is again convicted of an offence under this section, then, he shall be punishable for the second and for every subsequent offence with imprisonment for a term which may extend to five years and with fine.

Sec. 132(2): Where any person convicted of an offence under this section is again convicted of an offence under this section, then, he shall be punishable for the second and for every subsequent offence with imprisonment for a term which may extend to five years and with fine.

Sec. 132(3): The imprisonment referred to in clauses (i), (ii) and (iii) of sub-section (1) and sub-section (2) shall, in the absence of special and adequate reasons to the contrary to be recorded in the judgment of the Court, be for a term not less than six months.

Sec. 132(4): Notwithstanding anything contained in the Code of Criminal Procedure, 1973 (2 of 1974), all offences under this Act, except the offences referred to in sub-section (5) shall be non-cognizable and bailable.

Sec. 132(5): The offences specified in clause (a) or clause (b) or clause (c) or clause (d) of sub-section (1) and punishable under clause (i) of that sub-section shall be cognizable and non-bailable.

Sec. 132(6): A person shall not be prosecuted for any offence under this section except with the previous sanction of the Commissioner.

Author Bio

Excellent Article on proceedings under GST !!

Good Analysis