HOW TO CLAIM REFUND UNDER GST: Section 54 of Central Goods and Services Tax Act, 2017

Under Article 265 of the Constitution of India which states, “No tax shall be levied or collected except by the authority of law”, so there must be a charging section in the accompanied law for the levy and collection of tax. Article 246 empowers the Central and State to make law as stated in the Article. Taxes are levied as per Section 9 of CGST Act, subject to exemption notification for Supply of Goods and Services on taxable amount as determined as per the valuation rules u/s Section 15 of CGST Act. Usually when GST paid is in excess of the GST liability, a situation for claiming Refund under GST arises. For Example:-Mr. A is liable to pay GST of Rs. 2,000 for the month of March, 2021. However, due to an error, he paid Rs. 20,000. Hence, Mr. A can claim a refund of Rs. 18,000, time limit for claiming such refund is 2 years from the date of payment.

Types of Refund:

How to Claim Refund?

Section 54(1)–Where an assessee claiming refund of any tax and interest, if any, paid on such tax or any other amount paid by him shall be required to make an application to the Government within 2 years from the Relevant date in Form GST RFD-01 and manner as may be prescribed. However, a registered person claiming such refund of any balance in the electronic cash ledger as per Sec. 49(6)may claim such refund in the return furnished under Sec. 39 in Form GSTR-1.

Where petitioner’s refund application had not been processed within 15 days, the department loses its right to point out any deficiency in the petitioner’s refund application. Accordingly, the Refund application shall be deemed to be complete in all respects. [In the matter of Jain International v. Commissioner of Delhi Goods & Services Tax, W.P. (C) NO. 4205 OF 2020 July 22, 2020]

The CBIC through its Circular No. 137/07/2020-GST issued on April 13, 2020 clarified that the taxpayer can apply for refund of GST paid on advances in respect of supply which subsequently gets cancelled by filing FORM GST RFD-01 under the category “Refund of excess payment of tax”. The application can only be filed within 2 years from the date of payment of tax.

“Relevant Date” in accordance with the given section means –

Incase a refund voucher is issued after 2 years, the law does not provide any respite. Also, in case when an invoice is issued before supply of goods or services or both which subsequently gets cancelled after the date mentioned under Section 34, the taxpayer is not allowed any recourse.This limiting factor is detrimental in certain practical situations like construction/works contract service, where invoices are issued before the contract even starts and runs over years and subsequently, the contracts may get cancelled much later than the expiry of time limit under Section 34, leaving the supplier helpless.

Refund to Agencies of UNO, Embassy, etc.

[Sec. 54(2)] – A specialised agency of the United Nations Organisation or any Multilateral Financial Institution and Organisation notified under the United Nations (Privileges and Immunities) Act, 1947, Consulate or Embassy of foreign countries or any other person or class of persons, as notified under section 55, entitled to a refund of tax paid by it on inward supplies of goods or services or both, may make an application for such refund in Form GST RFD-10 along with statement of Inward supply of goods or services or both in Form GSTR-11, before the expiry of 6 months from the last day of the quarter in which such supply was received.

Refund of Unutilised Input tax credit

Sec. 54(3) – A registered person may claim refund of any unutilized input tax credit at the end of any tax period. Such refund can be claimed in the following circumstances:

i) ITC left unutilized when goods/services being supplied are zero rated or exempted from GST

ii) Where input goods or services have a higher rate of tax and the same goods/services have a lesser output tax (other than nil rated or fully exempt supplies), except supplies of goods or services or both as may be notified by the Government on the recommendations of the Council.

As discussed above, in the case of refund on account of inverted duty structure (tax on inputs is higher than on output leading to accumulation of ITC), refund of input tax credit shall be granted as per the following formula:- from 13-06-2018 onwards (NN 26/2018 – CT dated 13.06.2018 with retrospective effect from 01.07.2017)

Maximum Refund Amount = ((Turnover of inverted rated supply of goods and services) x Net ITC ÷ Adjusted Total Turnover) – tax payable on such inverted rated supply of goods and services.

Explanation:- For the purposes of this sub-rule, the expressions – (under Rule 89)

| (a) | Net ITC shall mean input tax credit availed on inputs during the relevant period other than the input tax credit availed for which refund is claimed under sub-rules (4A) or (4B) or both; and | |

| (b) | 1″Adjusted Total turnover” and “relevant period” shall have the same meaning as assigned to them in sub-rule (4) |

However, there has been increasing number of cases where credit has been obtained fraudulently through refund of ITC on exports of goods and inverted duty structure. Few methods opted by such fraudsters are as follows:

i) Cases where the purchase invoices are made for more than the actual goods received and in some cases where no goods are received at all but fake purchase invoices are made.

ii) Cases where goods are sold in cash to unregistered buyers by issuing bogus/fake output invoices and the same goods are sold to some other registered buyer for a negotiable price; thereby making that registered buyer gain ITC Credit without actually receiving any goods and enabling him to claim undue refunds.

iii) Creating bogus firms who sell their fake invoices on commission basis, without any actual movement of goods.

No refund of unutilised ITC shall be allowed:

Refunds of over Rs. 28,000Crore are said to have been filed by over 27,000 taxpayers on account of inverted duty structure in the financial year 2019-20.

- Where goods exported out of India are subjected to export duty.

- Where supplier of goods or services or both avails drawback in respect of central tax or claims refund of the IGST paid

- Notification No. 5/2017-Central Tax (Rate), dated 28-6-2017 for notification specifying supplies of goods in respect of which no refund of unutilised input tax credit shall be allowed.

- Notification No. 15/2017-Central Tax (Rate), dated 28-6-2017 for no refund of unutilised input tax credit under section 54(3) in case of supply of services specified in Item 5(b) of Schedule II of CGST Act.

- Notification No. 37/2017-Central Tax, dated 4-10-2017 for conditions and safeguards for furnishing a letter of undertaking in place of a Bond by a registered person who intends to supply goods or services for export without payment of integrated tax.

[Sec. 54(4)] – Documentary Evidence to be accompanied with the application:

| Documents to be filed [Rule 89(2)] | |

| Refund on account of: | Documents required |

| Export of Goods | Statement containing the number and date of shipping bills or bills of export and export invoices |

| Export of Services | Statement containing the number and date of invoices and relevant bank realization certificates/ Foreign Inward remittance certificates |

| Supply of Goods made to a SEZ unit/ developer | Statement containing number and date of invoices, evidence regarding specified endorsement of goods. Declaration that ITC has not been availed by SEZ unit/ developer |

| Supply of Services made to a SEZ unit/ developer | Statement containing number and date of invoices, evidence regarding specified endorsement and details of payment, along with proof thereof, made by the recipient to the supplier for authorized operations.

Declaration that ITC has not been availed by SEZ unit/ developer |

| Deemed Export (EOU etc) | i) Statement containing number and date of invoices

ii) Acknowledgement by the jurisdictional tax officer that the said deemed export supplies have been received by AA/EPCG holder, or iii) Copy of the tax invoice by the supplier to the recipient EOU that the said supply has been received by it iv) An undertaking by the recipient of deemed export supplies that no input tax credit on such supplies has been availed of by him. v) An undertaking by the recipient of deemed export supplies that he shall not claim the refund in respect of such supplies and the supplier may claim the refund. |

| Unutilised Input Tax credit due to inverted tax structure | Statement containing the number and the date of the invoices received and issued during a tax period |

| Finalisation of provisional assessment | Reference number of the final assessment order and a copy of the said order |

| Wrong payment of CGST instead of IGST | Statement showing the details of transactions considered as intra-state supply, but which is subsequently held to be inter-state supply |

| Excess payment of tax | Statement showing the details of the amount of claim on account of excess payment of tax |

A table illustrating the Forms w.r.t filing of refund application is given below:

| FORM | TIME LIMIT | DETAILS |

| GST RFD-01 | The taxpayer files application for claiming refund of tax, interest, penalty or fees. | |

| GST RFD-02 | Within 15 days from the date of claiming the refund. | The proper officer shall issue an acknowledgement upon scrutiny of the Refund application. |

| GST RFD-03 | Within 15 days from the date of claiming the refund. | The proper officer shall communicate the deficiencies to the applicant. |

| GST RFD-04 | Within 7 days from the date of generation of Form RFD-02 or RFD-03 | The proper officer shall specify the amount of refund to be disbursed on a provisional basis. |

| GST RFD-05 | The tax officer shall issue payment advice electronically.The bank account details mentioned in the refund application shall be validated by Public Financial Management System (PFMS). | |

| Recent Advisory (8/2021) on Refunds dated 20.04.2021 | A taxpayer is entitled to refund of the tax in the same manner by which the tax liability was discharged. The cash part has to be credited to the bank account by issuing Form RFD-05 and credit part to be re-credited to the electronic credit ledger through PMT-03. A new enhanced PMT-03 has been deployed in the portal. | |

| GST RFD-06 | Within 60 days from the date of submission of refund application | The tax officer shall process the application and intimate the taxpayer regarding the admissible/ inadmissible claim of refund along with sufficient reasons for the same. |

| GST RFD-07 | The GST officer shall mention reasons for withholding of provisional/ final refund. | |

| GST RFD-08 | The tax officer shall issue show cause notice stating reasons for rejection of application. | |

| GST RFD-09 | Within 15 days from the date of receipt of RFD-08 | The tax payer submits reply to the show cause notice along with supporting documents. |

| GST RFD-10 | Refund Application by embassies | |

| GST RFD-11 | Statement of inward supplies of goods/ services by embassies, etc. | |

> Where the amount claimed as Refund exceeds Rs. 2lakh, the applicant shall furnish documentary and other evidences including a certificate in Ann 2 of Form GST RFD-01 issued by a Chartered Accountant or a Cost Accountant to the effect that the incidence of tax, interest or any other amount claimed as refund has not been passed on to any other person.

Order of Refund — Sec. 54(5),(6),(7) of CGST Act

Upon receipt of an application, where the proper officer is satisfied, he shall order refund of the amount claimed. Such amount shall be transferred to the Consumer Welfare Fund. In cases of Refund from Electronic Cash ledger, an acknowledgment in Form GST RFD-02 through the common portal shall be made available to the applicant indicating the date of filing of the claim and the time period for issue of order shall be counted from such date of filing.

In other cases acknowledgment shall be made after scrutinizing the application within 15 days of filing.

In case of any deficiency, the proper officer shall intimate the same to the applicant in Form GST RFD-03, instructing him to file a fresh application after rectification.

[However, no Refund shall be processed if the amount claimed is less than Rs. 1,000. It is clarified vide circular 125/44/2019 that the limit of Rs. 1000 shall be applicable for each tax head separately and not cumulatively.]

In case of any claim for refund on account of zero rated supply of goods or services or both, 90% of provisional refund may be granted, excluding the amount of ITC provisionally accepted. The provisional refund shall be issued within 7 days from the date of acknowledgment in Form GST RFD-04.

The proper officer shall issue order within 60 days from the date of receipt of application complete in all respects.

Tracking GST Refund Application status on the GST portal:

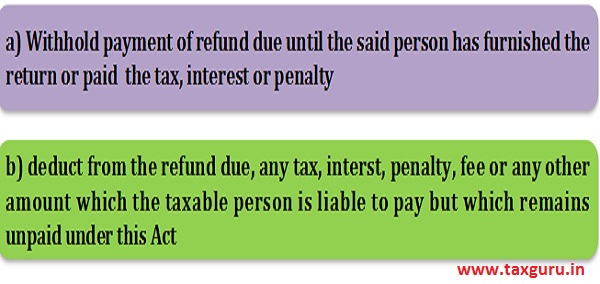

Withholding of Refund: Sec. 54(11),(12)

Where any refund is due to a registered person who has defaulted in furnishing any return or who is required to pay any tax, interest or penalty, which has not been stayed by any court, Tribunal or Appellate authority by the specified date, the proper officer may –

Where a refund is withheld, the taxable person shall be entitled to interest at such rate not exceeding 6%, if as a result of the appeal or further proceedings, he becomes entitled to refund.

Consequences of acceptance of a Refund application by proper officer –

Where the amount of Refund is ordered to be sanctioned provisionally by the authority and a sanction order is passed in accordance with the provisions of rule 91(2) of the CGST Rules, 2017 the Central tax authority shall communicate the same to the State tax authority for making payment of the sanctioned refund amount. The aforesaid communication shall primarily be made through e-mail attaching the scanned copies of the sanction order [FORM GST RFD-04 and FORM GST RFD-06], the application for refund in FORM GST RFD-01A and the Acknowledgement Receipt Number (ARN).

Accordingly, the jurisdictional proper officer shall issue FORM GST RFD-05 and send it to the DDO for onward transmission for release of payment. In case of refund claim for the balance amount in the electronic cash ledger, upon filing of FORM GST RFD-01A, the amount of refund claimed shall get debited in the electronic cash ledger.

Consequences of rejection of a Refund application by proper officer

Where any amount claimed as refund is rejected, either fully or partly, the amount debited, to the extent of rejection, shall be re-credited to the electronic credit ledger by an order made in FORM GST PMT-03. However, a refund shall be deemed to be rejected, if the appeal is finally rejected or if the claimant gives an undertaking in writing to the proper officer that he shall not file an appeal.

What is the time limit within which an appeal against an application rejected by the GST officer is required to be filed?

Any person aggrieved by any order or decision passed under GST Act, 2017 has the right to appeal to the Appellate Authority within 90 days of receiving such order or decision.

What is the manner of filing an appeal to the Appellate Authority?

Section 107 r.w.r 108 of the CGST Rules states the appeal shall be filed in Form GST APL-01 along with relevant documents either electronically or otherwise as may be notified by the Commissioner. A provisional acknowledgement shall be issued to the appellant immediately. A certified copy of the impugned order or decision shall be submitted within 7 days from filing the appeal. The Appellate Authority shall issue a final acknowledgement in Form GST APL-02 indicating appeal number.

Difficulties faced by applicants while applying for Refund:

Case-1:

It has been noticed that the GSTN portal suffers technical glitches when an applicant attempts to upload its application for Refund. In a specific matter held between Atibir Industries Co. Ltd. versus Union of India [W. P. (T) NO. 4061 OF 2019], the petitioner being a manufacturer of Sponge Iron regularly exports goods outside the country. As there is noliability of compensation cess on sponge iron, the entire amount of compensation cess paid by the petitioner on purchase of coal remained as unutilized ITC at the hands of the petitioner and the petitioner was entitled for refund of the said amount.

Facts of the case:

i) The application for refund of the Petitioner for F.Y. 2017-18 was not being accepted on GSTN Portal due to technical glitches and,

ii) The petitioner could not claim the amount of unutilized ITC towards compensation cess as refund pertaining to the financial year 2017-18.

iii) Subsequent application for F.Y. 2018-19 was not being accepted on GSTN Portal with a message directing the Petitioner to first file application for refund for the period 2017-18.

Held:

The Hon’ble Court decided that the Respondents should communicate the petitioner through e-mail as to whether they would open the GSTN portal or accept the refund application manually, thereby the applicant must act in accordance within 15 days from such communication.

Case-2:

Notice for rejection of application for Refund not specifically mentioned. In a specific matter held between Sahibabad printers versus Additional Commissioner CGST (Appeals), the petitioner claimed to be a registered supplier under GST Act and was engaged in job work on cloth and was liable to claim refund on account of inward supply of inverted rated inputs.

Facts of the case:

i) The petitioner filed an application for Refund, to which the Department issued a SCN in Form GST RFD-08 seeking reasons as to why the application should not be rejected. However, the reason disclosed in the SCN was displayed “Other”.

ii) The respondent without giving an opportunity of being heard to petitioner rejected the application without giving any reason to the petitioner.

iii) The petitioner challenged the said order by filing an appeal which was dismissed on the ground that the petitioner had not given any reply to the SCN.

Held:

The Hon’ble High Court held that in proceedings relating to financial adjudication, the proposed reasons for rejection should be specifically mentioned such that the assessee can reply in a conclusive and reasonable manner. In the given case, principle of natural justice has been violated while adjudication of refund claim of the petitioner.

*****

Author – CA PRAVEEN KUMAR SURANA, PRAVEEN SURANA & ASSOCIATES, Chartered Accountant in Practice from Kolkata can be contacted at psurana.associates@gmail.com.

Author Bio

Sir, We are based in state “A” registered with Centre (CGST). We had an order for state “B” and the same was supplied from state “C” (bill-To-Ship). Then there was an issue in respect of E-Way bill in state “B”. The issue was adjudicated and we paid through DRC 03 (IGST + penalty). Now, JC-Commercial Taxes (Appeals), state “B” passed an order in our favour and directed the respondent to refund the IGST and penalty. No we applied for refund in state “A” (CGST) but it was rejected as they were not respondents and told us to file for refund with the SGST, “B”, as they were the respondents and passed the original order. Any advise or suggestion in this regard is highly appreciated. Thanks sir

Read more at: https://taxguru.in/goods-and-service-tax/refund-gst-regime-detailed-analysis.html#pcomments

Copyright © Taxguru.in