Transitional PROVISIONS

Sec 175: Input removed for job work and returned on or after the appointed day

> If Input received in a factory & removed as such or after being partially processed to Job worker for further processing, repair, testing etc prior to appointed day (i.e. 31.03.2017): No tax shall be payable if such input returned to said factory within 6 months from the appointed day (i.e. Up to 30.09.2017)

> Extension of 6 months time period: Permissible by competent authority on sufficient cause being shown (1st proviso)

> If Input not returned within 6 months: Input Tax credit, claimed by principle, shall be liable to be recovered under sec 184. (2nd proviso)

> Input held in stock by job worker on behalf of manufacturer as on appointed day shall be declare the details by job worker & manufacturer for availing benefit of above mentioned provision.

Sec 176: Semi-finished goods removed for job work and returned on or after the appointed day

> If Semi-finished goods removed from factory to Job worker for carrying out manufacturing process prior to appointed day (i.e. 31.03.2017): No tax shall be payable if such semi-finished goods returned to said factory within 6 months from the appointed day (i.e. Up to 30.09.2017)

> Extension of 6 months time period: Permissible by competent authority on sufficient cause being shown (1st proviso)

> If Semi-finished goods not returned within 6 months: Input Tax credit, claimed by principal, shall be liable to be recovered under sec 184. (2nd proviso)

> Manufacturer may transfer the said goods within 6 months to the premises of registered taxable person for the purpose of supplying therefrom on payment of tax in India or without payment of tax for export.

> Semi-finished goods held in stock by job worker on behalf of manufacturer as on appointed day shall be declare the details by job worker & manufacturer for availing benefit of the said provision.

Sec 177: Finished goods removed for carrying out certain process and returned on or after the appointed day

> If any excisable goods manufactured had been removed without payment of duty for carrying out test or other process, not amounting to manufacture, to any other premises prior to appointed day (i.e. 31.03.2017): No tax shall be payable if such goods returned to said factory within 6 months from the appointed day (i.e. Up to 30.09.2017)

> Extension of 6 months time period: Permissible by competent authority on sufficient cause being shown (1st proviso)

> If Such goods not returned within 6 months: Input Tax credit, claimed by principal, shall be liable to be recovered under sec 184. (2nd proviso)

> Manufacturer may transfer the said goods within 6 months to the premises of registered taxable person for the purpose of supplying therefrom on payment of tax

> In case of finished goods, no need to declare the details of stock held as on appointed day

CHAPTER-XIII

Sec 55: Special Procedure for removal of goods for certain purposes.

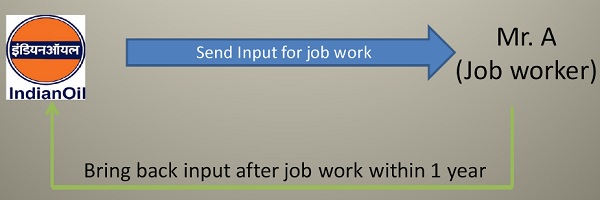

> A registered taxable person may send input and/or capital goods, without payment of tax, to job-worker for job work and from there subsequently to another Job worker.

> Time limit to bring back Input into said factory after such job work: 1 year & 3 years for input and capital goods respectively.

> Capital Goods exclude: moulds and dies, jigs and fixtures, or tools

CASE-1

> A registered taxable person may supply such input and/or capital goods, after job work, within 1 year of their being sent out from the place of business of job worker on payment of tax or without payment of tax (in case of export).

> In such case, principal will have to declare the place of business of job worker as his additional place of business except in case

-If job worker is registered under sec 23 ; or

-If principal engaged in supply of notify goods

IOC will have to declare the place of business of job worker as his additional place of business except

(1)if Job worker is registered

(2) If IOC engaged in supply of notify goods.

> The responsibility for accountability of the input/capital goods shall lie with the “principal”.

> If input/capital goods (other than moulds and dies, jigs and fixture, or tools) sent for job work are not received back by principal or are not supplied from the place of business of job worker within 1 year: It shall be deemed that such input had been supplied by the principal to the job worker on the day when the said inputs were sent out. If input/capital goods sent directly to job worker, period of 1 year shall be counted from the date of receipts of inputs by the job worker.

> Notwithstanding anything contained in Sec 55(1) & (2), Any waste & Scrap may be supplied by job worker directly from his place of business on payment of tax if such job worker is registered, or by the principal, if the job worker is not registered.

Sec 20: Taking Input tax credit in respect of inputs sent for job work

> The “Principal” shall be allowed input tax credit on input/capital goods sent to a job-worker for job-work subject to such conditions and restrictions as may be prescribed.

> The “Principal” shall be entitled to take credit of input/capital goods tax on inputs even if the inputs directly sent to a job-worker without their being first brought to his place of business.

> Nothing contained in this section shall apply to moulds and dies, jigs and fixtures, tools sent out to a job-worker for job work.

(Author can be reached umeshkumar.kumar14@gmail.com)

We are Contractor and providing services to the Private Company for their Packing and Loading Job and Construction services in three to four states.Can we take single registeration for all these states or not what will be procedure.

Sir, Please allow to take print/View in PDF and support us or you can send e-mails based on our request for the Articles/Updates available in Taxguru.

Sir,

Realised that print option has been disabled. Person working indirect tax dept, All articles provided in TAXGURU are use useful and we take printout for further use. Kindly enable the print option or PDF provision. Thanks in advance.