Hello, looking to lesser number of filling GSTR 9, I would like to give some inputs which might motivates to those who have yet not started filling GSTR 9. Even for all those who are struggling anywhere in GSTR 9.

Page Contents

- A. What Is The Barometer For Comparison While Filling GSTR 9?

- B. How To Proceed For GSTR 9? Whom To Take First?

- C. Steps To Follow Before Filling GSTR 9 – Use Of Comparison Tables & System Drafted Tables

- D. Which Tables Are More Important in GSTR 9?

- E. Documents Required For GSTR 9

- F. Check-Points For Filling Error-Free GSTR-9

- G. GSTR 9 – One Page Guide

A. What Is The Barometer For Comparison While Filling GSTR 9?

It’s always Books. If data not matches with BOOKS. Then there is mismatch. Comparing GSTR 3B data with BOOKS is utmost priority. Auto-filled data of GSTR 1 might confuse you.

E. G. Issues like

a. claimed more ITC mistakenly; b. Paid lesser tax on Outward, c. Paid less tax on RCM.

Need to be solved by paying in DRC. Decide it and convey to clients… We have to make call. So, the crux is.

Pay difference in DRC if at all any difference with books n then File GSTR 9.

B. How To Proceed For GSTR 9? Whom To Take First?

Here is strategy

1. Start with GSTR 9A…complete all Composition dealers. It hardly takes time.

2. For normal taxpayer… Go for all those who had NIL Turnover or negligible Turnover…in 17-18 Remember filling GSTR 9 is compulsory for all…Even for NIL.

3. then Start with small clients for GSTR 9. Which have no much problematic issues…?

4. then there is absolute green signal for all those clients where 3B=1… And it again matches with BOOKS Your half battle is won… Just filling data in diff Tables of GSTR 9 is to be done. You might complete 75% of you clients till August end

C. Steps To Follow Before Filling GSTR 9 – Use Of Comparison Tables & System Drafted Tables

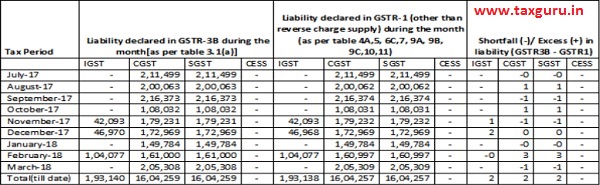

Don’t just jump to file GSTR 9. First follow these 3 steps and then go to filling GSTR 9. FIRST CHECK COMPARISON TABLES ON PORTAL. AND THESE ARE VERY VERY VERY USEFUL FOR OUTWARD SIDE

1. Matching “TAX AS PER 3B = TAX AS PER GSTR 1 “

First check TAX paid as per GSTR 3B and TAX payable as per GSTR 1 should match perfectly.

| WHERE TO CHECK?

EVERYTHING is on PORTAL. COMPARISON TABLES are given under RETURN DASHBOARD. ITS NEW & VERY HELPFUL FEATURE. There are 4 tables. We are concerned with 2 left side tables related to OUTWARD SUPPLIES. Table 1. LOCAL TURNOVER TABLE i.e. Liability (other than zero rated and reverse charge supply) under GSTR 3B VS GSTR 1 Table 2. EXPORT + SEZ TURNOVER TABLE i.e. Liability (Export and supplies to SEZ) |

PURPOSE

In first step, we will check whatever tax should have been paid as per GSTR1 should be matching with actual tax paid by GSTR 3B. All this available readymade on portal in comparison table so You will check -> TAX as per two different GST returns that is payable as per GSTR 1 and actually paid as per GSTR 3B. Because GSTR 1 & GSTR 3B is separate Return, there might be chances of Mismatch. |

SCREENSHOT for EXAMPLE – OF COMPARISION TABLE – 1 – Liability (other than zero rated and reverse charge supply. Same way you can download Comparison Table – 2 for Export + SEZ supplies

2. Matching “ SALES as per books ” vs. “SALES as per GST”

Secondly, Checking GST TURNOVER vs. TURNOVER as per BOOKS OF ACCOUNTS. This exercise is really important for Reconciliation purpose

| WHERE TO CHECK | PURPOSE |

| FOR SALES AS PER BOOKS = PLEASE CHECK PROFIT LOSS ACCOUNTS FOR 9 MONTHS i.e. FROM 01/072017 TO 31/03/2018

FOR SALES AS PER GST = YOU CAN AGAIN CHECK ABOVE TABLES FOR CHECKING SALES FIGURE. |

If everything is matched in the in the first step then the next step is to match books of accounts with GST returns. I.e. check the sales data as per books of accounts with Sales data as per GST portal.We are again checking SALES only but this time with Books of Accounts.Sales data should match for 9 months of 17-18 with sales data as per GST. It is really important to check GST TURNOVER SHOULD BE RECONCILLING WITH TURNOVER AS PER BOOKS. ( This will make you assure that whatever INCOME TAX RETURN FILED by you is having perfect data as far as SALES is concerned ) |

Matching “ SYSTEM GENERATED ANNUAL GSTR 3B & GSTR 1 summary “ with “ COMBINED GSTR 1 & GSTR 3B GENERATED from Accounting software

| WHERE TO CHECK | PURPOSE |

| 1. SYSTEM GENERATED ANNUAL GSTR 3B & GSTR 1 summary – GO TO Annual Return module on portal. You will find SYSTEM GENERATED ANNUAL GSTR 3B & GSTR 1 summary on upper right side. This is combined GSTR 3B and COMBINED GSTR 1 FROM Jul-17 to Mar-18.

2. GST RETURNS GENERATED from Accounting software ” – You can generate a combined 3B AND a combined GSTR 1 summary from your Accounting software. |

1. Not only sales, But ITC claimed in actual 3B vs. ITC figure as per books can be checked.

2. You can see if any changes done in data after filling monthly returns. This exercise will let you know that Books of accounts is matching or not with GSTR RETURNS. FOR OUWARD SIDE AS WELL AS INWARD SIDE |

D. Which Tables Are More Important in GSTR 9?

Many are struggling in TABLE 8, TABLE 18 & 19 of GSTR 9. I have listed some difficult areas of GSTR 9 which are taking lot of time however, these all tables hardly makes sense as far as revenue is concerned.

E. G

1. Table 6 – need of Bifurcation into 3 heads which are input, input services and CG…

2. Table 8 – need of matching ITC with GSTR 2A

3. Table 8- need of giving information on Ineligible and unavailable ITC…

4. Table 18 &19 – need of HSN summary for outward and inward…

GSTR 9 is still achievable till 31st August if Govt. Straight give relaxations for these Tables. I am not saying that you should not fill these tables. If data available, then you should definitely fill these tables. If they give these relaxation for this unnecessary tables then there will be more than 50% percentage filling for 9.

I have seen many Professionals wasting time in above useless tables and because of that many are delaying filling GSTR 9 or waiting for more extension. Don’t wait for more extension.

On last week of August, THESE same Professionals will be filling in rush without even focusing more on Table 4,table 5, table 6 ( as a whole) ,table 7 & table 9 of GSTR 9.. Which I find more crucial than other. So it better you make your focus clear for GSTR 9.

E. Documents Required For GSTR 9

DOCUMENTS REQUIRED FOR FILLING GSTR 9 – GST ANNUAL RETURN FOR 17-18- FOR THOSE USING TALLY

1. Print – Annual GSTR 3B –

how to print? –> (Open Tally > Display > Statutory Reports > > GST > GSTR 3B > Period 01-7-17 to 31-3-18 (PRESS F12 & CLICK YES for Separate columns for Tax)

(Also Press “VIEW RETURN FORMAT” on right side panel)

2. Print – Annual GSTR 1 SUMMARY –

how to print? –> (Open Tally > Display > Statutory Reports > > GST > GSTR 1 > Period 01-7-17 to 31-3-18 (PRESS F12 & CLICK YES for Separate columns for Tax)

(Also Press “VIEW RETURN FORMAT” on right side panel)

3. Print these ledgers for period of Jul-17 To March-18– Direct income ledgers, Indirect income ledgers. E.g. Rent income might have been skipped from GST levy during 17-18

4. Ask for PENDING ITC list… ITC which client might have claimed in 18-19 which is pertaining to 17-18

5. Ask for List of ITC claimed for CAPITAL GOODS (out of Total ITC) or FIXED ASSET LEDGERS

6. Ask for List OF ITC of services claimed during year (out of Total ITC) or its ledgers

7. Print Ledgers for those EXPENSSES which attracts RCM like Transportation and Advocate Fees

8. Print Jul–17 To March-18 – Balance sheet and Profit Loss – TO RECONSILE TURNOVER REPORTED IN PROFIT LOSS ACCOUNT.

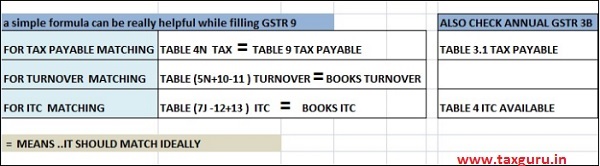

F. Check-Points For Filling Error-Free GSTR-9

3 simple Formulas which Serves as CHECK-POINT for TAX PAYABLE AMOUNT, TURNOVER FIGURE, & ITC MATCHING

G. GSTR 9 – One Page Guide

What will be Treatment of transactions shown in 2017-18 or you might have shown 18-19 or You have never shown?? . This chart will guide you for presentation of such transaction in GSTR9.

–

–

Hope this post give some help to all those who have not yet started GSTR 9. I am nobody to give any advice to learned professionals. But still I hope it’s useful . Thanks for reading. Please give feedback on my number or email if you find this article worth.

DISCLAIMER – All views are personal

Dear sir,

Please resolve my Query:

If in case sales in GST3B is less than books but in GSTR-1 it reconcile with books, then how to adjust this in annual return GSTR-9 as this form is taking all values from GSTR-1 . We have paid the tax payable on that sale but how to Reconcile?

Good one, thank you keep posting

Very much useful sir.

Thanks

Thank you for a very good article

Sir what is the difference between point 8c and 13 in gstr 9