This article is all about things you should follow before you think of filling GSTR 9 . Don’t just jump to file GSTR 9. First follow these 3 steps and then go to filling GSTR 9.

1. Matching “TAX AS PER 3B = TAX AS PER GSTR 1 “

First check TAX paid as per GSTR 3B and TAX payable as per GSTR 1 should match perfectly.

| WHERE TO CHECK? | PURPOSE |

| EVERYTHING is on PORTAL. COMPARISON TABLES are given under RETURN DASHBOARD. ITS NEW & VERY HELPFUL FEATURE. There are 4 tables. We are concerned with 2 left side tables related to OUTWARD SUPPLIES.

Table 1. LOCAL TURNOVER TABLE i.e Liability (other than zero rated and reverse charge supply) under GSTR 3B VS GSTR 1 Table 2. EXPORT + SEZ TURNOVER TABLE i.e Liability (Export and supplies to SEZ) |

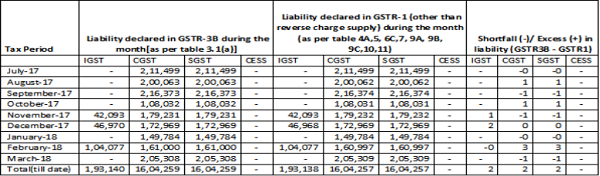

In first step, we will check whatever tax should have been paid as per GSTR1 should be matching with actual tax paid by GSTR3B. All this available ready-made on portal in comparison table so You will check -> TAX as per two different GST returns that is payable as per GSTR 1 and actually paid as per GSTR 3B.Because GSTR 1 & GSTR 3B are separate Return, there might be chances of Mismatch . |

SCREENSHOT for EXAMPLE – OF COMPARISION TABLE – 1 – Liability (other than zero rated and reverse charge supply . Same way you can download Comparison Table – 2 for Export + SEZ supplies

Points to ponder

There will be different treatment of putting figures in GSTR 9 when Outward Supplies & Tax will not be matching in GSTR 1 & GSTR 3B.

2. Matching “ SALES as per books ” vs. “SALES as per GST”

Secondly, Checking GST TURNOVER vs. TURNOVER as per BOOKS OF ACCOUNTS. This exercise is really important for Reconciliation purpose

| WHERE TO CHECK | PURPOSE |

|

FOR SALES AS PER BOOKS = PLEASE CHECK PROFIT LOSS ACCOUNTS FOR 9 MONTHS i.e. FROM 01/07/2017 TO 31/03/2018 FOR SALES AS PER GST = YOU CAN AGAIN CHECK ABOVE TABLES FOR CHECKING SALES FIGURE. |

If everything is matched in the in the first step then the next step is to match books of accounts with GST returns.

I.e. check the sales data as per books of accounts with Sales data as per GST portal.We are again checking SALES only but this time with Books of Accounts. Sales data should match for 9 months of 17-18 with sales data as per GST. It is really important to check GST TURNOVER SHOULD BE RECONCILING WITH TURNOVER AS PER BOOKS. ( This will make you assure that whatever INCOME TAX RETURN FILED by you is having perfect data as far as SALES is concerned ) |

Points to ponder

1. From Profit loss accounts, you can find out that whether any income On which GST is laviable , is not being missed in GST RETURNS For e.g. RENT Income on Commercial Property.

2. From profit loss accounts, You can go in-depth analysis, whether any Expenses on which Tax is payable as RCM, is actually discharged in 3B or not. E.g. Transportation exp., Advocate Fees. Etc

3. From Profit loss account scrutiny, You can also check Discount income is being treated properly with GST effect.

4. From Profit loss account scrutiny, You may find out that Some of sales is Not reflected in GSTR-1 and GSTR 3B (or any one) for 2017-18 but reflected in 2018-19 or you might have completely forgotten.

3. Matching “ SYSTEM GENERATED ANNUAL GSTR 3B & GSTR 1 summary ” with “ COMBINED GSTR 1 & GSTR 3B GENERATED from Accounting software

| WHERE TO CHECK | PURPOSE |

| 1. SYSTEM GENERATED ANNUAL GSTR 3B & GSTR 1 summary – GO TO Annual Return module on portal . You will find SYSTEM GENERATED ANNUAL GSTR 3B & GSTR 1 summary on upper right side. This is combined GSTR 3B and COMBINED GSTR 1 FROM Jul-17 to Mar-18.

2. GST RETURNS GENERATED from Accounting software ” – You can generate a combined 3B AND a combined GSTR 1 summary from your Accounting software. |

1. Not only sales, But ITC claimed in actual 3B vs. ITC figure as per books can be checked.

2. You can see if any changes done in data after filling monthly returns. This exercise will let you know that Books of accounts is matching or not with GSTR RETURNS. FOR OUWARD SIDE AS WELL AS INWARD SIDE |

Points to ponder

1. ITC might have been claimed more than what is actual ITC as per books. We fear that you might need to pay by DRC 3.

2. ITC might not have been reversed during the whole year for Ineligible portion. Again , You should find out BY CHECKING in your Books of accounts & pay in DRC 3

very informative

Waste time of annual retun

Very nice. useful information. Thanks Harshil

good and perfect articles

Very nice artical

Good articles