How to map GSTR 1 vs GSTR 3B

GSTR-1, filed by the supplier, contains invoice-wise and category-wise details of all outward supplies made in a year

GSTR-3B is the summary return based on which tax is deposited by the supplier. It contains category-wise summary of both inward and outward supplies and tax payment details.

Now, the reconciliation of GSTR-3B and GSTR-1 is of utmost importance since GSTR-3B is a manual return, i.e. it is not auto populated on the basis of GSTR-1 and GSTR-2A. There might be instances where supplier has shown an invoice in GSTR-1 but has not paid tax on that invoice in GSTR-3B. GST department uses data analytics to reconcile GSTR-1 and GSTR-3B filed by a supplier. That means it automatically reconciles GSTR-1 with GSTR-3B and issues a GST notice for mismatches.

One of the main reason of the difference is, wrong calculation of revenue & tax liability at the time of filling GSTR-3B For a large business organisation, it is very common to have difference in Actual turnover & the turnover recorded in books. This may result in GST liability if turnover as recorded in books of accounts is less than the actual turnover. Again this may result in late payment of GST, which may lead to applicability of interest. Nominal difference in is still accepted, but large data gaps is matter of concern because this can result in heavy interest liability

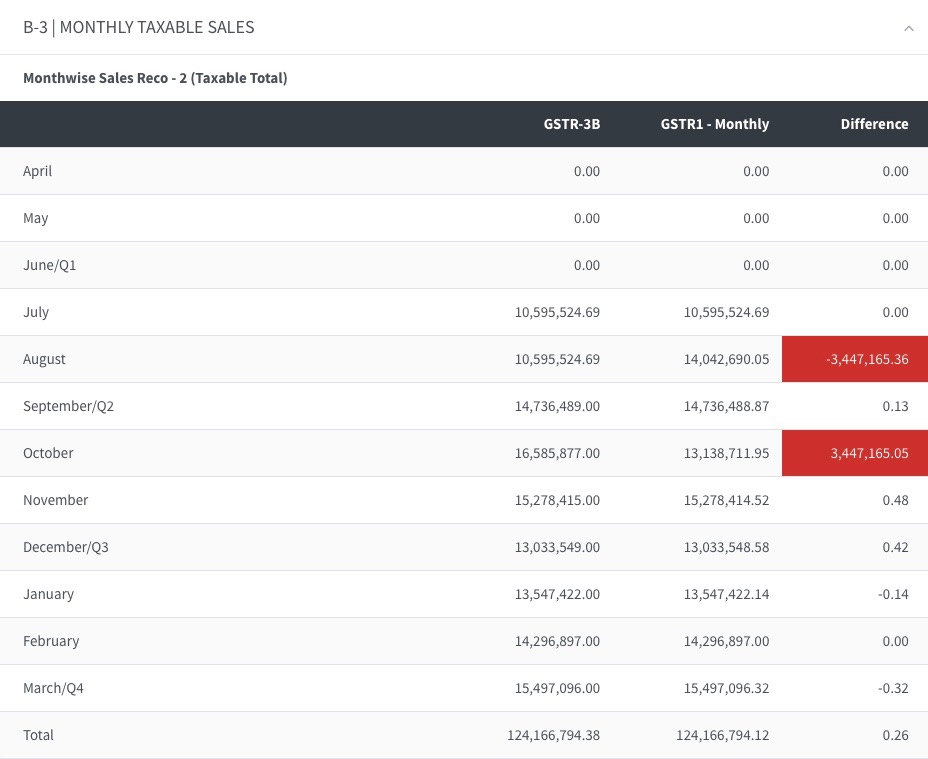

Here is a format for reconciliation

Problems in mapping

1. Downloading all files – All files for each branch and each month need to be downloaded from GST Portal.

2. Conversion to excel – for starting any kind of mapping firstly all the files need to be converted into excel in a format that it can be manipulated

3. Identifying data points to be matched – There are multiple data points in the forms which can be mapped. As GSTR 1 is s detailed return and mapping it with 3B required submission of a number of columns in GSTR 1 for mapping with column of 3B. Illustration is provided at the end of article.

4. Huge data and complex sheets – When preparing these sheet for multiple clients and years the data can become too large to handle. The formulas become complex and chances of manual errors cannot be ignored

5. Data visualization – Data visualization can be tough as making sense of data in such huge sheets can be challenging

What are the data points that can be mapped?

For the purpose of GSTR 3B and GSTR 1 mapping from their summaries only 4 from GSTR 3B and and 9 from GSTR 1 are relevant:

GSTR 3B section 3.1(a) maps with following columns of GSTR 1

- + 4A, 4B, 4C, 6B, 6C

- + 5A, 5B

- – 9B (registered)

- – 9B (unregistered)

- + 7 B2C

- + 11 A (1), 11A(2) Advances received

- – 11 B (1), 11B (2) Adjustment of Advances

GSTR 3B section 3.1 (b) maps with following columns of GSTR 1

- + 6A

GSTR 3B section 3.1 (c) maps with following columns of GSTR 1

- + section 8 but only Nil and Exempted Column

GSTR 3B section 3.1 (e) maps with following columns of GSTR 1

- + section 8 but only Non- GST Supplies

Our GST Health Tool, provides these reconciliations at very low cost in understandable formats with zero errors. Log on to www.gsthealth.com for complete GST Audit Solutions.

Author Bio

am i still liable to pay interest on tax difference of GST 1 and GST 3b, even though i have input tax credit under GST