Case Law Details

Narsinga Rao Aleti Vs ITO (ITAT Hyderabad)

Hyderabad ITAT: Buyer’s Denial Alone Cannot Justify Section 69A Addition-AO Must Properly Verify Sale Agreement and Evidence

The Hyderabad ITAT held that an addition under section 69A cannot be sustained merely because the purchaser denies having paid consideration over and above the amount recorded in the sale deed. Where the assessee produces a duly executed sale agreement, supported by corroborative evidence such as bank entries, matching signatures, and admitted advance payments, the Assessing Officer is duty-bound to conduct a proper enquiry before rejecting the explanation.

In the present case, the assessee explained that the deposits of ₹59.76 lakh represented part of the sale consideration received for agricultural land under an agreement dated 11.08.2015, which recorded a total consideration of ₹1.65 crore, although the registered sale deed reflected only ₹46.75 lakh. The agreement contained detailed particulars of the property, sale price, payment schedule, and an RTGS token advance of ₹8 lakh, which was admitted by the purchaser and matched the assessee’s bank statement. The agreement also recorded a further payment of ₹30 lakh, which corresponded with deposits in the assessee’s bank account.

The Tribunal observed that although the purchaser, in response to a notice under section 133(6), denied making any cash payment beyond the registered sale consideration, it did not dispute the execution of the sale agreement, and the admitted RTGS payment, matching signatures, and corresponding bank entries lent credibility to the assessee’s explanation. In such circumstances, the Assessing Officer could not simply prefer the purchaser’s self-serving denial without investigating the genuineness of the agreement and the surrounding evidence. Since contradictory stands had been taken by the parties, a comprehensive enquiry was necessary before drawing any adverse inference. The matter was therefore remanded to the Assessing Officer for fresh verification and adjudication after granting the assessee adequate opportunity of hearing.

Cases Discussed:

- Narsinga Rao Aleti, Nalgonda vs. ITO, Ward-1, Suryapet in ITA.No.1265/Hyd./2024, dated 01.01.2025.

- Jignesh Harshadbhai Patel, Ahmedabad vs. ITO, Ward-4(2)(3), Ahmedabad in ITA.No.1655/Ahd./2025, dated 15.05.2026.

- Mariamma Kurian, Bhopal vs. ITO-1(1), Bhopal in ITA.No.2/Ind./2025, dated 28.08.2025.

- ACIT, Central Circle-16, New Delhi vs. Kamlesh Kumar Rathi, New Delhi in ITA.Nos.822 & 823/Del./2018, dated 16.05.2023.

FULL TEXT OF THE ORDER OF ITAT HYDERABAD

This appeal by the Assessee is directed against the Order dated 09.02.2026 of Ld. CIT(A)-National Faceless Appeal Centre [in short “NFAC”], Delhi, for the assessment year 2016-2017.

2. The Assessee has raised the following grounds of appeal

1) “The order of the learned Commissioner of Income Tax (Appeals) is against the law, weight of evidence and probabilities of case.

2) The learned Commissioner ought to have appreciated that the deposits aggregating to Rs.59,76,000/ – are in the nature of advance/ sale consideration received in respect of transfer of agricultural land, therefore, the learned Commissioner erred in confirming the order of the AO, wherein, income is determined at Rs.59,76,000/ – u/s 69A of the IT Act.

3) The learned Commissioner ought to have appreciated that the notice u/s 148 and order u/s 148A(d) are not accompanied by the proceedings of the PCCIT granting approval for issue of notice u/s 148 of the IT Act, therefore, the CIT(A) erred in confirming the order u/s 147 r.w.s 143(3) of the IT Act as the notice is an invalid notice for not following the procedure laid by the CBDT.

4) As seen from the IT Portal, there is no email id in respect of notice issued u/s 148, and order u/s 148A(d), therefore, the notices are not served on the assessee as per the provisions of section 282 of the IT Act, therefore, without service of statutory notice u/s 148 of the IT Act the order passed u/s 147 w.s 144B of the IT Act is to be held bad in law.

5) The learned Commissioner erred in confirming the order u/s 147 r.w.s 144, wherein, the total income is determined at Rs. 59,76,000/ – u/s 69A of the IT Act.

6) The learned Commissioner ought to have appreciated that the assessee responded to the enablement communication on 29.08.2024, therefore, erred in assuming the assessee has not filed any reply to the notices issued and further erred in confirming the order of the learned AO wherein, addition of Rs.59,76,000/ – is made u/s 69A of the IT Act.

7) The learned Commissioner ought to have appreciated that the amount of Rs. 59,76,000/ – received from the purchaser is part of sale consideration of Agricultural Land, owned by the assessee, assessees mother and assessees brother, therefore, not to be charged for tax under the charging sections of the IT Act

8) The appellant craves leave to add to, amend OR modify the above grounds of appeal either before OR at the time of hearing of the appeal, if it is considered necessary.”

3. The solitary issue arises in this appeal of the assessee is whether in the facts and circumstances of the case, the learned CIT(A) has erred in confirming the addition to the extent of Rs.59,76,000/- made u/sec.69A of the Income Tax Act [in short “the Ace], 1961.

4. The learned Authorised Representative of the Assessee has submitted that the assessee has sold agricultural land during the year under consideration vide sale deed dated 19.07.2016. The sale consideration in the sale deed is mentioned at Rs.46.75 lakhs whereas the actual consideration was received at Rs.1.65 crores as per the agreement dated 11.08.2015. The learned Authorised Representative of the Assessee has submitted that the assessee explained the source of deposit in the bank account during the assessment proceedings as sale consideration for sale of agricultural land received by the assessee over and above the consideration shown in the sale deed and also produced the land sale agreement dated 11.08.2015 however, the Assessing Officer has not accepted the said explanation of the assessee and made the addition of Rs.59,76,000/- u/sec.69A of the Act as unexplained deposit in the bank account. The learned Authorised Representative of the Assessee has submitted that the agreement was duly executed between the parties and given all the details of the land, rate of sale price per acre and total sale consideration. Further, this agreement also mentioned the payment made by the buyer to the assessee on various dates including the token advance payment of Rs.8 lakhs through RTGS on 23.01.2015. He has submitted that the assessee is not having any other source of income to deposit the cash in the bank account and therefore, once the assessee has produced the sale agreement containing all the details of the payment made by the buyer to the assessee prior to the sale deed are also correspondingly reflected in the bank account of the assessee then the source explained by the assessee ought to have been accepted by the Assessing Officer and no addition is called for. In support of his contention, he has relied upon the following decisions:

i. Order of ITAT, Ahmedabad Bench in the case of Jignesh Harshadbhai Patel, Ahmedabad vs. ITO, Ward-4(2)(3), Ahmedabad in ITA.No.1655/Ahd./ 2025, dated 15.05.2026.

ii. Order of ITAT, Indore Bench in the case of Mariamma Kurian, Bhopal vs. ITO-1(1), Bhopal in ITA.No.2/Ind./2025, dated 28.08.2025.

iii. Order of ITAT, Hyderabad in the case of Narsinga Rao Aleti, Nalgonda vs. ITO, Ward-1, Suryapet in ITA.No.1265/Hyd./2024, dated 01.01.2025.

iv. Order of ITAT, Delhi in the case of ACIT, Central Circle-16, New Delhi vs. Kamlesh Kumar Rathi, New Delhi in ITA.Nos.822 85823/Del./2018, dated 16.05.2023.

4.1. Thus, the learned Authorised Representative of the Assessee has pleaded that the addition made by the Assessing Officer and confirmed by the learned CIT(A) are not sustainable in law and liable to be deleted.

5. On the other hand, the learned DR has submitted that the Assessing Officer has conducted proper enquiry on this issue by issuing notice u/sec.133(6) of the Act to the buyer of the land who in his reply has denied any payment to the assessee over and above the sale consideration of Rs.46,75,000/- as stated in the sale deed. Further, the buyer has admitted an amount of Rs.8 lakhs paid on 23.01.2015 which was paid through banking channel and also filed the bank account statement by the buyer in support of the said transaction. Thus, the learned DR has submitted that once the purchaser of the property has denied any payment over and above the sale consideration mentioned in the sale deed then, the deposit in the bank account to the extent of Rs.59,76,000/- is unexplained money and liable to be assessed to tax. The learned DR relied upon the Orders of the authorities below.

6. We have considered the rival submissions as well as relevant material on record. The assessee during the course of assessment proceedings has explained the source of the cash deposit in the bank account as sale consideration received by the assessee for sale of agricultural land vide sale deed dated 19.07.2016. The assessee also filed Land Sale Agreement dated 11.08.2015 in support of the claim that the land was sold for a consideration of Rs.1,65,00,000/-. The Assessing Officer issued notice u/sec.133(6) of the Act to Siyora Developers P. Ltd., Hyderabad seeking reply. In reply, the buyer has denied the payment over and above the sale consideration mentioned in the sale deed. The reply of the buyer is reproduced by the Assessing Officer at Page no.7 of the assessment order which reads as under:

“To

National Faceless Assessment Centre

Delhi

Respected Sir/ Madam,

Sub: Reply to notice u/ s 133(6) of the Act.

Ref INSIGHT/ VER/ 02/ 133(6)/ 2023-24/ 5114112685430001

***

In connection with the above notice, we would like to submit that the land sale agreement is not correct and the consideration mentioned of Rs.1,65,00,000/ – is also not correct. The Land admeasuring 5 Acre 20 guntas situated at Nemuragomula Village, Bibinagar Mandal, Nalgonda district belonged to Aleti Balamani, Aleti Balaraju de Aleti Narsing Rao. But in the attached agreement only Aleti Narsing Rao name is appearing which is not correct and cannot be relied upon.

As can be seen from the sale deed attached, we have entered the transaction of purchase of land from Aleti Balamani, Aleti Balaraju & Aleti Narsing Rao vide doc no. 5851/2016 and we have paid the sale consideration through bank and got registered the land in our name on 19.07.2016 for a purchase consideration of Rs 40,75,000/ – and the market Value as per the registered sale deed is Rs.40,75,000/ -and stamp duty paid is Rs. 2,80,700/ -. Apart from the amounts transferred in bank, we confirm that we have not paid any amounts in cash to the above mentioned parties. We have paid an amount of Rs.8,00,000/ -on 23.01.2015 to Aleti Narsing Rao But the other parties Aleti Balamuni & Aleti Balaraju have asked to pay the entire amount of sale consideration as mentioned in the registered sale deed. Accordingly, to complete the transaction of purchase we have paid the sale consideration though bank to the concerned parties. We are attaching copy of bank statement highlighting the amount paid through bank to the above mentioned parties.

Regards,

Siyora Developers P Ltd”

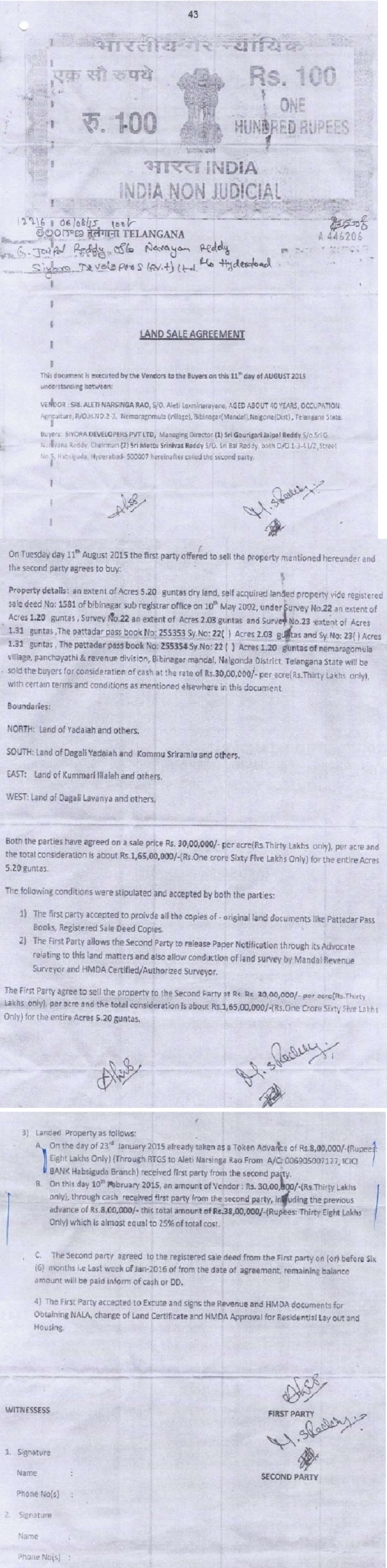

6.1. Thus, the buyer has denied any payment in cash over and above the sale consideration mentioned in the sale deed however, the buyer has also admitted the payment of Rs.8 lakhs as token advance money on 23.01.2015 and also filed copy of the bank statement in respect of the said payment. Based on the said reply, the Assessing Officer has rejected the explanation of the assessee and made the addition of Rs.59,76,000/- u/sec.69A of the Act. It is pertinent to note that the agreement to sale was duly executed between the parties and signature of the parties are apparently not in dispute. For ready reference, we reproduce the agreement dated 11.08.2015 as under:

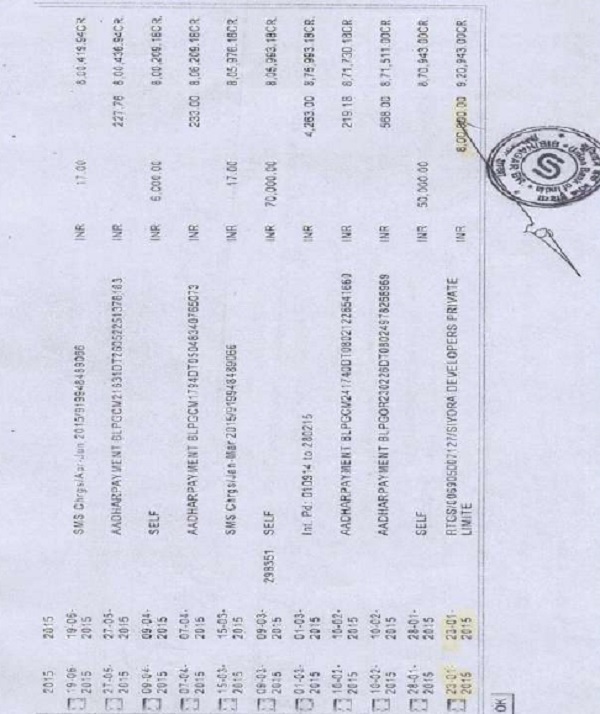

6.2. The said agreement clearly set out all the relevant details of the property in question which are not in dispute and sale price per acre with total consideration of Rs.1,65,00,000/- as well as part payment of Rs.30 lakhs and advance token payment of Rs.8 lakhs is also clearly mentioned in the said agreement. The deposit in the bank account of Rs.30 lakhs is matching with the payment date as stated in the agreement to sale. Further the token amount of Rs.8 lakhs paid through RTGS is admitted by the buyer in his reply and it is also a matter of record as reflected from the bank account of the assessee as under:

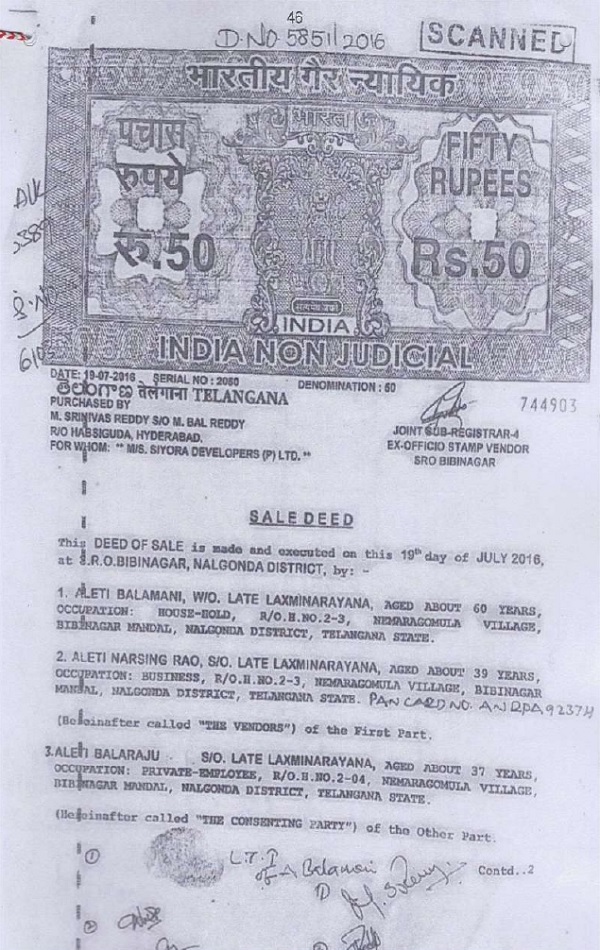

6.3. The last transaction dated 23.01.2015 in the bank account is the same RTGS transfer as stated in the agreement duly reflected in the bank account and therefore, the existence of the agreement and contents of the agreement cannot be disputed. Further, we find from the sale deed as well as this agreement that signatures of the parties are also matching. For the sake of completeness, the signature of the parties in the sale deed as appearing at Page no.46 of the paper book are as under:

6.4. The Assessing Officer has proceeded by accepting the reply of the buyer without conducting the enquiry regarding the execution of the agreement between the parties and the contents of the agreement by considering the corroborating evidence of bank account statement as well as admitted payment of token amount of Rs.8 lakhs through RTGS. Thus, it is apparent and evident from the record comprising of agreement to sale dated 11.08.2015, sale deed dated 19.07.2016, bank account statement of the assessee reflecting the deposit of Rs.30 lakhs on 10.02.2015 which is also mentioned in the agreement. However, there are 3 vendors in the sale deed as against one in the sale agreement and therefore, the entire cash consideration may not be available to assessee. The Assessing Officer has not conducted proper enquiry on this issue and rejected the explanation of assessee by preferring the reply of the buyer. Once the two contradictory stands were taken by the parties before the Assessing Officer, it was the duty of the Assessing Officer to conduct a proper enquiry to reach the concluding finding of fact regarding the existence of the agreement in question and payment of the sale consideration as mentioned in the agreement. In the reply, the buyer has simply stated that the agreement contains the name of Aleti Narsing Rao which is not correct and cannot be relied upon whereas the buyer has not disputed the execution of the sale agreement. Therefore, in our considered view, this issue requires a proper verification and enquiry on the part of the Assessing Officer to give a concluding finding about the existence of the agreement in question and once the agreement is found to be genuine then, the explanation of the assessee cannot be rejected simply on the basis of the stand taken by the buyer which is self-serving to protect it’s interest. Hence, in the facts and circumstances of the case, the matter is remanded to the record of the Assessing Officer to conduct a proper enquiry on this issue and then decide the same as per law and in view of various decisions relied upon by the assessee. Needless to say, the assessee be given proper opportunity of hearing before passing the fresh order.

7. In the result, appeal of the Assessee is allowed for statistical purposes.

Order pronounced in the open court on 15.07.2026.

Author Bio