Though there is no mention of GTA in the GST Act & Rules, however as per Explanation to 9(iii) of Notification No. 11/2017-Central Tax (Rate), Dt.: 28th June, 2017 & Paragraph 2 Clause (ze) to Notification 12-2017 dated 28 June 2017, “Goods Transport Agency” means any person who provides service in relation to transport of goods by road and issues consignment note, by whatever name called.

In the above definition following Two Aspects need to be discussed to understand the scope of GTA services & responsibility.

1. Service in Relation to Transport

2. Consignment Note

Generally Transport Services also covers various other related services. Therefore in the definition of GTA, phrases “Service in Relation to Transport” used to broaden the Scope to cover not only Transportation, but also all other services in relation to transport like loading /unloading, packing /unpacking, transshipment, temporary warehousing, forward distribution or any other such ancillary service etc.

In the definition GTA means, one who provide Transport & Transport Related services as discussed above and who issues Consignment Note. But Consignment Note is also not defined in any of GST Acts, however reference may be drawn from Explanation to Rule 4B, Service Tax Rules, 1994, a “consignment note” means a document, issued by a goods transport agency against the receipt of goods for the purpose of transport of goods by road in a goods carriage, which is serially numbered, and contains the name of the consignor and consignee, registration number of the goods carriage in which the goods are transported, details of the goods transported, details of the place of origin and destination, person liable for paying service tax whether consignor, consignee or the goods transport agency.

Similar to above in a modified way Rule 54(3) of CGST Rules states “Where the supplier of taxable service is a goods transport agency supplying services in relation to transportation of goods by road in a goods carriage, the said supplier shall issue a tax invoice or any other document in lieu thereof, by whatever name called, containing the gross weight of the consignment, name of the consigner and the consignee, registration number of goods carriage in which the goods are transported, details of goods transported, details of place of origin and destination, Goods and Services Tax Identification Number of the person liable for paying tax whether as consigner, consignee or goods transport agency, and also containing other information as mentioned under rule 46”.

In the above rule, instead of word “Consignment Note”, phrases “Tax Invoice or any other Document in lieu thereof” are used. In this rule, the way and manner GTA should issue document (whether Tax Invoice or any other document) is prescribed.

Whether GTA Services are Taxable Supplies?

Since GTA providing services in the course or furtherance of business for consideration, therefore these services are considered as Supply as per Section 7 of CGST Act, 2017,

Moreover as per Notification No. 12/2017- Central Tax (Rate), Dt: 28th June, 2017 – Exempted Supplies

Entry No 18, Heading 9965

Services by way of transportation of goods-

(a) by road except the services of—

(i) a Goods Transportation Agency;

(ii) a courier agency;

Therefore GTA services are Taxable Supplies.

Tax Options to GTA:

A Goods Transport Agent has following Three Options or we may say three situations :

1. Providing Services to Specified Category Recipient – Applicability of Reverse Charge as per Notification No. 13/2017- Central Tax (Rate) Dt : 28.06.2017

2. Services to other than Specified Category Recipient – Forward Charge @5% without ITC – Rate of GST as per Notification No. 11/2017-Central Tax (Rate) Dt : 28th June, 2017

3. Forward Charging with ITC Availment – Forward Charge @12% availing ITC – Notification No. 20/2017 – Central Tax (Rate) dated 22ndAugust, 2017

Option – 1 : Providing Services to Specified Category Recipient – Applicability of Reverse Charge

As per Notification No. 13/2017- Central Tax (Rate) dated 28.06.2017, Supply of Services by a Goods Transport Agency (GTA) in respect of transportation of goods by road to Specified Category Recipients are treated on Reverse Charge and the Recipient is Liable to pay GST.

(a) any factory registered under or governed by the Factories Act, 1948(63 of 1948);or

(b) any society registered under the Societies Registration Act, 1860 (21 of 1860) or under any other law for the time being in force in any part of India; or

(c) any co-operative society established by or under any law; or

(d) any person registered under the Central Goods and Services Tax Act or the Integrated Goods and Services Tax Act or the State Goods and Services Tax Act or the Union Territory Goods and Services Tax Act; or

(e) any body corporate established, by or under any law; or

(f) any partnership firm whether registered or not under any law including association of persons; or

(g) any casual taxable person.

The applicable rate of GST as per Notification No. 11/2017-Central Tax (Rate) Dt : 28th June, 2017, is @ 5% (CGST – 2.5% + SGST – 2.5%). Therefore the Recipient is required to pay GST @ 5% on Reverse Charge Mechanism and of course the Recipient is allowed to take Input Tax Credit (ITC) subject to general eligibility criterion. Since GTA is not charging any GST, he is not entitled to any Credit.

Option – 2 : Services to other than Specified Category Recipient – Forward Charge @5% without ITC

This situation shall arise if GTA is providing services to other than those specified category recipients as discussed above such as to an Individual / Proprietorship Firm/HUF. In such scenario GST shall be paid by GTA itself on forward charge mechanism @ 5%. GTA is not allowed to take any ITC.

Option – 3 : Forward Charging with ITC Availment – Forward Charge @12% by availing ITC

As per Notification No. 20/2017 – Central Tax (Rate) dated 22nd August, 2017, GTA are now allowed to take Input Tax Credit subject to condition that they should charge GST @12% on forward charge. The recipient is also allowed to take credit subject to his eligibility. That means through this way seamless credit is ensured at the GTA end as well as at recipient’s side. However, Once this option to pay @ GST 12% and avail ITC is opted, then other Options can’t be exercised and thenceforth, GTA be liable to pay GST @ 12% on all the services of GTA supplied by it.

This is a beneficial option especially for B2B transactions as GTA can take credit of input taxes and charge the tax @ 12% which the recipient also can avail tax credit.

Services Provided by a GTA – Exempted :

As per 14th GST Council meeting held at Srinagar, J&K held on 19 May 2017 and Notification No. 9/2017-Integrated Tax (Rate), the 28th June, 2017, Entry No : 22, Heading 9965 or Heading 9967 : Services provided by a Goods Transport Agency, by way of transport in a goods carriage of following are Exempted –

(a) agricultural produce;

(b) goods, where consideration charged for the transportation of goods on a consignment transported in a single carriage does not exceed one thousand five hundred rupees;

(c) goods, where consideration charged for transportation of all such goods for a single consignee does not exceed rupees seven hundred and fifty;

(d) milk, salt and food grain including flour, pulses and rice;

(e) organic manure;

(f) newspaper or magazines registered with the Registrar of Newspapers;

(g) relief materials meant for victims of natural or man-made disasters, calamities, accidents or mishap; or

(h) defence or military equipments.

Whether GTA to Register under GST? :

Let us discuss various scenarios as follows: In general if the GTA is providing services which are all falls under Reverse Charge, then they are not required to take registration. However in other cases they need to register subject to conditions.

Case – 1 : GTA Services only to Specified Category Registered Business – on RCM – No Need to Register

In case GTA is providing whole of his services to only those Specified Category Registered Businesses as specified in the Notification No. 13/2017- Central Tax (Rate) dated 28.06.2017, then the recipient is required to pay GST on Reverse Charge. Further as per Notification No. 5/2017- Central Tax dated 19/06/2017, which specifies that the persons who are only engaged in making supplies of taxable goods or services or both, the total tax on which is liable to be paid on reverse charge basis by the recipient of such goods or services or both under sub-section (3) of section 9 of the said Act as the category of persons exempted from obtaining registration under the aforesaid Act.

That means if the GTA is making all his supplies only on reverse charge that is supplies to those specified category supplies as discussed above, then GTA is exempted from obtaining registration of GST.

Even though in case the GTA is supplying inter-state supplies, he is not required to register under above situation as Notification No. 5/2017- Central Tax dated 19/06/2017, is overriding General Clause u/s 24 of CGST Act (Compulsory registration in case of Inter-State supply).

Case – 2 : GTA Services to other than Specified Category Registered Business or Other than Exempted GTA Services – Need to Register Subject to Threshold Limit

In case GTA is Providing Services to Categories other than Specified under Notification No. 13/2017- Central Tax (Rate) dated 28.06.2017 & also Goods other than under Heading 9965 or Heading 9967 (Exempted Supply), then GTA is required to Register if the Threshold Limit of Rs 20 L (Rs 10 L for Special Category States) is crossed or making Inter-state Supply.

In case the threshold limit is less than Rs 20 L / 10 L as the case may be and also not making any inter-state supply, then GTA is not required to Register.

In a situation if the GTA is taken registration then he has two options – Pay GST @ 5% without taking ITC or pay @ 12 and avail ITC.

Case – 3 : Exempted GTA Services – Carrying only Specified Goods – No Need to Register

As per Notification No. 9/2017-Integrated Tax (Rate), the 28th June, 2017, Entry No : 22, Heading 9965 or Heading 9967 : Services provided by a Goods Transport Agency, by way of transport in a goods carriage of Specified Goods are Exempted. In case the GTA is engaged in exclusively carrying those supplies then he is not required to register by following Sec 23(1)(a) of CGST Act which stipulates that person supplying wholly exempted good or services : not be liable to registration.

That means GTA supplying exclusively to Specified Category Recipients on Reverse Charge (as per Notification No. 13/2017- Central Tax (Rate)) and / or exclusively carrying only Specified Goods (as per Notification No. 9/2017-Integrated Tax (Rate)) need not register.

Case – 4 : GTA Opting to Pay GST @ 12% & Avail ITC – Need to Register

In case GTA opt to pay GSt @ 12% and avail ITC as per Notification No. 20/2017 – Central Tax (Rate), then he supposed to be registered.

The GTA opting to pay GST @ 12% under this entry shall, thenceforth, be liable to pay GST @ 12% on all the services of GTA supplied by it”.

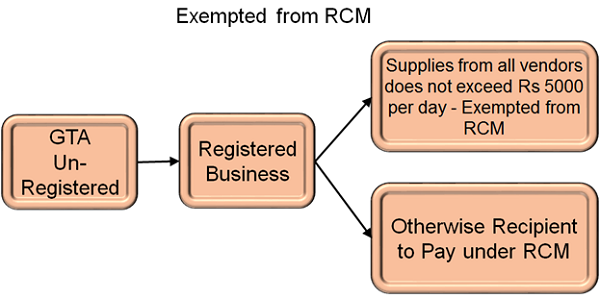

Exemption from RCM to Recipient :

Some relaxation is provided to recipients getting supplies from un-registered. GST payable (under reverse charge) from unregistered persons exempted if the aggregate value of such supplies from all vendors does not exceed INR 5000 per day as per Notification : 8/ 2017 – Central Tax Rate, 28th June’17. This provision is made to exempt for small transactions up to Rs 5,000 per day.

Accordingly in case GTA is un-registered providing transport services to registered person and the value of all such inward receipts by the recipient is less Rs 5,000 per day then the recipient is not required to pay on reverse charge.

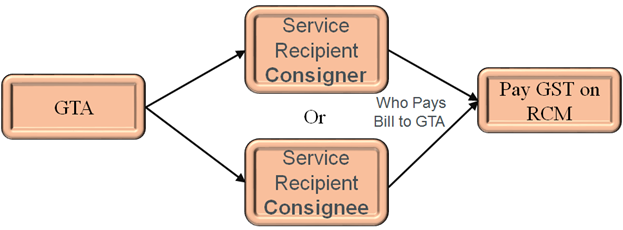

Transport – Who is Liable to Pay GST on RCM ?

“The person who pays or is liable to pay freight for the transportation of goods by road in goods carriage, located in the taxable territory shall be treated as the person who receives the service for the purpose of this notification”

The person who is liable to pay will be the service recipient and he may be either the consigner or the consignee.

Question : When should a tax invoice be issued for goods?

Answer: Tax invoice for goods shall be issued on or before the time of removal/delivery of goods. In case of continuous supply of goods, it shall be issued on or before the time of issue of statement of accounts /receipt of payment.

Question : If goods are transported in semi-knocked down condition, when shall the complete invoice be issued?

Answer: When goods are transported in semi-knocked down condition, the complete invoice shall be issued before dispatch of the first consignment. Delivery challan shall be issued for subsequent consignments. Original copy of invoice shall be sent along with the last consignment.

Exemption Notification for Hiring Services :

In case the owner of the Vehicle gives his vehicle on Hiring to GTA, then the hiring charges are exempt from GST as per below

Notification No. 12/2017- Central Tax (Rate) New Delhi, the 28th June, 2017, Heading 9966 or Heading 9973

Services by way of giving on hire –

(a) to a state transport undertaking, a motor vehicle meant to carry more than twelve passengers; or

(b) to a goods transport agency, a means of transportation of goods.

Records to Maintain by GTA

As per Sec 35(2) of CGST Act : Every owner or operator of warehouse or godown or any other place used for storage of goods and every transporter, irrespective of whether he is a registered person or not, shall maintain records of the consigner, consignee and other relevant details of the goods in such manner as may be prescribed.

Further Rule 58(4) of CGST Rules states

Subject to the provisions of Rule 56,

(a) any person engaged in the business of transporting goods shall maintain records of goods transported, delivered and goods stored in transit by him along with the Goods and Services Tax Identification Number of the registered consigner and consignee for each of his branches.

(b) every owner or operator of a warehouse or godown shall maintain books of accounts with respect to the period for which particular goods remain in the warehouse, including the particulars relating to dispatch, movement, receipt and disposal of such goods.

GTA – Relevant Notifications

Notification No. 13/2017- Central Tax (Rate) Dt : 28.06.2017

Applicability of Reverse Charge on Supply of Services by a GTA in respect of Transportation of Goods by Road to Specified Category of Recipient

Notification No. 11/2017-Central Tax (Rate) Dt : 28th June, 2017

Notifies Central Tax Rates for services subject to condition mentioned there in the notification. Sr No. 9(iii) of that para had prescribed 2.5% Central Tax rate for Services of goods transport agency (GTA) in relation to transportation of goods (including used household goods for personal use) with the condition that “credit of input tax charged on goods and services used in supplying the service has not been taken”. Thus the effective rate for GTA was 5% with no ITC to the transporter.

Notification No. 20/2017 – Central Tax (Rate) dated 22nd August, 2017

Amended Notification No. 11/2017 – Central Tax (Rate) relating to the rates for supply of services under CGST Act. In para (iii) of that notification, Government has allowed an option to pay GST at the central tax rate of 6% (With Full ITC) on “Services of goods transport agency (GTA) in relation to transportation of goods (including used household goods for personal use)”. But in order to avail the option to pay GST at 6%, a new condition has been prescribed which reads as follows: “Provided that the goods transport agency opting to pay central tax @ 6% under this entry shall, thenceforth, be liable to pay central tax @ 6% on all the services of GTA supplied by it”.

Conclusion

> GTA Services are Taxable Supplies

> In case GTA Providing Services to Specified Category Recipient – Reverse Charge Applicable as per Notification No. 13/2017- Central Tax (Rate) Dt : 28.06.2017

> Services to other than Specified Category Recipient – Forward Charge @5% without ITC – Rate of GST as per Notification No. 11/2017-Central Tax (Rate) Dt : 28th June, 2017

> Forward Charging with ITC Availment – Forward Charge @12% availing ITC – Notification No. 20/2017 – Central Tax (Rate) dated 22ndAugust, 2017. This option is beneficial for B2B transactions as GTA can take credit of input taxes and charge the tax @ 12% which the recipient also can avail tax credit.

> Whether GTA to Register

> GTA Services only to Specified Category Registered Business – on RCM – No Need to Register

> GTA Services to other than Specified Category Registered Business or Other than Exempted GTA Services – Need to Register Subject to Threshold Limit

> Exempted GTA Services – Carrying only Specified Goods – No Need to Register

> GTA Opting to Pay GST @ 12% & Avail ITC – Need to Register

> If GTA is unregistered person and providing services which are subject to reverse charge then payment of reverse charge is exempted if the aggregate value of such supplies from all vendors does not exceed INR 5000 per day.

Author Bio

GTA service to any unregistered person other than notified person then such would be exempt as per entry no 21A

sir, I am registered LLP company having own vehicles and supplying Transport services to the registered Private limited manufacturing Company for their Goods movement to their customer by way of Road. we raise Consignment Note and for this transaction Freight has been paid to us by the recipient of Services (Manufacturing company). GST has been paid by recipient under RCM. My question is, as a registered transporter, Whether I need to show the Value of turnover towards such transation has to be declared my GST returns? if yes, where to show it in GSTR1 as well as in GSTR3B?

Kindly reply sir

What if One GTA provide service to another GTA as a Sub- Transporter. Who is liable to issue Consignment Note . Assuming both are registered person under GST ?

we are the Transporter, carrying the goods from various station to Assam. There are lots of parties who not taken the delivery even in 2 months. Will you guide us in the matter? In the GST rule is it compulsory to take delivery within the particular period.

great article … good work sir

i just want to know that i m GTA registered in 2 states, in one i am following the rule of reverse charge and my clients are paying reverse charge, but in another state i am charging them gst @12% as some clients do not go in reverse charge method.

i just want to confirm that i can do this or am i doing anything wrong.

i Am GTA I Wants To Pay 12% Gst As Per Notification no. 20/2017 Central Tax Then, What is procedure For Go This Rate Slab

Sir, i have a query, there is a Transporter who is Presentaly Raising Invoices 5% without ITC, Now he has purchased some Capital Goods they have huge amount of ITC so He wants to go for 12% with ITC,

My Query

1. he can go for 12%.????

2. if Yes, When He has claimed all ITC, whether he can opt again 5% GST without ITC

GTA-What is the GST rate on Loading and unloading charges and Halting charges apart from Freight.And who is the liable to pay.please rply.

GTA supplier charged the IGST @ 5 % and pay to Govt. the payment of IGST @5% pay to GTA supplier allow to ITC credit . further the supplier charged correct bill or not

Hi, If gta is having two work order , first with 12% in X industry and second with 5% in Y industry ( under rcm) then what will the scenario of input tax credit by gta.

If a GTA registered under GST (RCM 5%) is giving its vehicle to unregistered GTA and Consignment Note is being issued by unregistered GTA then who will be liable to pay GST.

GTA service from registered person with no GST charged in Transport of goods Invoice. At this case

(1) pay 5% on RCM and can’t take ITC

or

(2) pay 5% on RCM and can take ITC

or

(3) pay 12% and can take ITC

or

what is the possible way to take ITC

or

need not want to worry about GST to pay.

I would like to have definite ITC. Based on that please suggest.

One GTA has raised bill charging 12% and has also raised consignment note under RCM where 5% RCM was paid by Recipient. But the GTA has taken ITC on full value of sale both 12% + RCM of 5%. What is the solution : whether to reverse the excess ITC availed on the portion of 5% RCM or to pay 12% also on such RCM value. Please enlighten on legal position.

transport agency ko comission amount par bhi koi GST tax pay karna hoga????

can the rule of 12% be availed from 1st july(retrospective)?

This is the best article i have ever read on GST on GTA. Thanks for such a nice article. You have cleared all the things. .

Excellent article

Factory register under GST in Maharashtra and avails GTA services of GTA registered in gujrat and goods are delivered at Jammu and Kashmir and also paying freight to GTA ,So Whether factory in maharashtra has to pay IGST or CGST and SGST.Please reply

dear sir

limit of 5000 will not apply on GTA because Notification No.8/2017-Central Tax (Rate) only cover 9(4)

and GTA comes under Section 9(3) compulsory RCM

Dear sir

limit of 5000 will not apply on GTA because Notification No.8/2017-Central Tax (Rate) only cover 9(4)

.and GTA comes under Section 9(3) compulsory RCM

Good analysis.. As rightly stated in all B2B transaction s,the forward tax at 12% with ITC for GTA will be beneficial and ideal as well..

All recipient s also get ITC and no headache of RCM payment..

Hopefully, all estd.GTAs also may opt for this..

Real Estate & multistoried complexes etirity please

request to feed me suitably.

sir we are one of trader we are supplying oil seeds within state and interstate can i know what is the rate of tax on freight and if i pay in rcm can i take itc in netx month

The exemption of Rs. 5,000/- per day for urd expenses is not applicable to expenses u/s 9(3). As per notification 8/2017 dated 28/6/2017 it is applicable for expenses u/s 9(4). Hence if the GTA bill is of Rs. 2,000/- 5% WILL BE PAYABLE UNDER RCM

If a person/firm/company is a registered 3PL logistics concern. It is availing services of GTA who is URD and at the same time raising its freight charges to principal company.

01. Will the 3PL need to do RCM on GTA services received.

02. Will the 3PL need to charge GST on its invoice to principal company. If yes then at what rate.

03. 3PL is already charging GST @ 18% on Logistic Charges excluding freight. So will GST on GTA be counted as bundled service and GST @ 18% would be applied or not.

The article is very good and eloborate and simple to follow.I like to ask a query:

If the owner of vehicle rent out to GTA/others for rent, the hire received is not liable for GST.OK. Will it not be subjected to GST under the head letting out of tangible assets service? Kindly enlighten me.

Mr. A is GTA service provider to Factories registered and paying GST on RCM Basis. Mr. A dont have vehicle of his own. He obtain services from other vehicle owners who are unregistered. Whether RCM applicable on such transaction?

Mr. Panigrahi

Hats Off-truly professional

Well done Sir, Nice article

But at one place, I think that the exemption of Rs 5000 is not applicable in case of goods or services mentioned under Sec 9(3).

And GTA service is mentioned under this section.

Correct me if I’m wrong.

Thanks sir for your guidance on GTA Service. Pls let me know whether a service provided by GTA to GTA will be taxable? and if it is taxable then at which rate tax should be payable.

Reverse charge on GTA is under section 9 (3).Taxpayers cannot avail exemption limit of Rs 5000 for GTA payments.

VERY USEFUL AND LUCID ARTICLE ON GTA. MAY I REQUEST SRI S N PANIGRAHI ABOUT PUBLICATION OF ANALYSIS ON EMPLOYEE AND EMPLOYER GST LIABILITY

In my opinion a person receiving the services of specified service for whom he is to pay GST u/s 9(3), is required to pay tax even if the total value is less than Rs 5000/- in a day. The notification in this regard is applicable only to those who are to pay tax u/s 9(4).

Also provide clarity on following issue

“Service by way of transport of goods by road other then by gta are exempted.

Gta is a person who issues consignment note

Say u have a dumper and u transport my crusher gitty and charge transporation charges without issuing consignment note and only bill for transport is issued

Whether chargeable to GST??”

Under Notification No. 8/2017-Central Tax (Rate) , reverse charge payable u/s 9(4) of CGST act is exempted upto Rs.5000/- per day and not to services mentioned u/s 9(3). GTA service has been notified u/s 9(3) of CGST act wide Notification No. 13/2017- Central Tax (Rate) New Delhi, the 28th June, 2017

Comprehensive note on GTA. Great!

In Last para ..as per my openion …Rs. 5000 limit is available to Purchase from URD u/s 9(4) only.Hence GTA is not covered

Conditions are embedded in 5% tax rate and recipient under option -1 is liable to discharge the tax liability. To discharge the tax liability at concessional rate , recipient is required to fulfil the conditions attached to the rate. Since the conditions are supplier specific, recipient can not fulfil the conditions.

Since recipient fails to fulfil the conditions, concessional rate, i.e. 5% can not be availed by the recipient.