A tax reform launched in 2017, Goods and Service Tax (GST) in India, was a revolutionary movement since its independence. The new scheme has been picturised as an efficient mechanism of taxation. It also simplifies the taxation mechanism by making a unified market and following the approach of “One Nation, One Tax” in India.

An audit under GST is all about checking and verifying the financial documents maintained and submitted to the tax authority under GST. The GST Act, 2017 makes it compulsory for the registered taxpayers to get their account books audited. Therefore, the GST Audit under section 35 (5) of the Act mentions that the GST registered taxpayer should submit an audited document of their annual accounts by an Accountant assigned by the Commissioner.

GST follows a trust-based mechanism. Accordingly, the registered person he himself assess the tax liability; pay the taxes and files GST returns. Hence, GST audit is very important to make sure the correctness of the self-assessment done by the registered person.

Sec 2(13): Audit

Audit” means the examination of records, returns and other documents maintained or furnished by the registered person under this Act or the rules made thereunder or under any other law for the time being in force to verify the correctness of turnover declared, taxes paid, refund claimed and input tax credit availed, and to assess his compliance with the provisions of this Act or the rules made thereunder

Place of business – Section 2 (85) of The CGST Bill, 2017 defines “place of business” to include

a) a place from where the business is ordinarily carried on, and includes a warehouse, a godown or any other place where a taxable person stores his goods, provides or receives goods services or both; or b) a place where a taxable person maintains his books of account; or c)a place where a taxable person is engaged in business through an agent, by whatever name called;

‘Principal place of business’- Section 2(89) of defines to mean the place of business specified as the principal place of business in the certificate of registration.

Audit

- Audit by Tax Authorities (S. 65)

- Special Audit (S. 66)

Access to business premises Section 71

SECTION 35 ACCOUNTS AND OTHER RECORDS

Introduction

- This Section mandates the upkeep and maintenance of records, at the place(s) of business in electronic or other forms.

- Power is vested with the Commissioner for relaxation as well as for prescribing additional records for certain classes of taxable persons.

- Furnishing of an audited statement of accounts and reconciliation statement is also contemplated for persons having turnover exceeding prescribed limit.

- Failure to maintain records or accounts may entail payment of tax as determined by a proper officer in respect of unaccounted transactions.

- Every owner or operator, of a place of storage, or every transporter whether such owner or operator or transporter is registered or not, shall maintain records and other relevant details as may be prescribed.

(1) Every registered person shall keep and maintain, at his principal place of business, as mentioned in the certificate of registration, a true and correct account of—

(a) production or manufacture of goods;

(b) inward and outward supply of goods or services or both;

(c) stock of goods;

(d) input tax credit availed;

(e) output tax payable and paid; and

(f) such other particulars as may be prescribed:

Provided that where more than one place of business is specified in the certificate of registration, the accounts relating to each place of business shall be kept at such places of business: Provided further that the registered person may keep and maintain such accounts and other particulars in electronic form in such manner as may be prescribed.

(2) Every owner or operator of warehouse or godown or any other place used for storage of goods and every transporter, irrespective of whether he is a registered person or not, shall maintain records of the consigner, consignee and other relevant details of the goods in such manner as may be prescribed.

(3) The Commissioner may notify a class of taxable persons to maintain additional accounts or documents for such purpose as may be specified therein.

(4) Where the Commissioner considers that any class of taxable person is not in a position to keep and maintain accounts in accordance with the provisions of this section, he may, for reasons to be recorded in writing, permit such class of taxable persons to maintain accounts in such manner as may be prescribed.

(5) Every registered person whose turnover during a financial year exceeds the prescribed limit shall get his accounts audited by a chartered accountant or a cost accountant Accounts and other records and shall submit a copy of the audited annual accounts, the reconciliation statement under sub-section (2) of section 44 and such other documents in such form and manner as may be prescribed.

(6) Subject to the provisions of clause (h) of sub-section (5) of section 17, where the registered person fails to account for the goods or services or both in accordance with the provisions of sub- section (1), the proper officer shall determine the amount of tax payable on the goods or services or both that are not accounted for, as if such goods or services or both had been supplied by such person and the provisions of section 73 or section 74, as the case may be, shall, mutatis mutandis, apply for determination of such tax.

TYPES OF DEPARTMENTAL GST AUDITS

As per section 2(13) of the CGST Act, audit means-

- In-depth examination of records, statements and other documents that are maintained/ furnished by a registered person.

- The purpose of conducting such examination is to verify the correctness of turnover; taxes paid; refund claimed; input step-down availed and compliance with the provisions of the CBIC CGST Act and CGST rules.

|

GOVERNING SECTION |

PARTICULARS | AUDIT CONDUCTING PERSONNEL |

| SECTION 65 | AUDIT BY TAX AUTHORITIES | AUTHORIZED DEPARTMENTAL OFFICER |

| SECTION 66 | SPECIAL AUDIT | CA/ CMA NOMINATED BY THE COMMISSIONER |

Sec 65(1): Audit by Tax Authorities: • The Commissioner or any officer authorized by him, by way of a general or a specific order, may undertake audit of any registered person for such period, at such frequency and in such manner as may be prescribed

The officers referred to in sub-section (1) may conduct audit at the place of business of the registered person or in their office;

- Section 2(85) – Place of business includes–

- a place from where the business is ordinarily carried on, and includes a warehouse, a godown or any other place where a taxable person stores his goods, supplies or receives goods or services or both; or

- a place where a taxable person maintains his books of account; or

- a place where a taxable person is engaged in business through an agent, by whatever name called.

Section 65(2): Place of Conduct of Audit: • The officers referred to in sub-Section (1) may conduct audit at the place of business of the registered person and/or in their office.

Section 65(3) The registered person shall be informed, by way of a notice, not less than fifteen working days, prior to the conduct of audit in such manner as may be prescribed. Intimation of audit is to be issued to the taxable person at least 15 days in advance in Form GSTADT-01.

Section 65(4) Period of Completion:

- The audit under sub-Section (1) shall be completed within a period of three months from the date of commencement of audit:

- Provided that where the Commissioner is satisfied that audit in respect of such registered person cannot be completed within three months, he may, for the reasons to be recorded in writing, extend the period by a further period not exceeding six months.

- Explanation.- For the purposes of this sub-Section, ‘commencement of audit’ shall mean the date on which the records and other documents, called for by the tax authorities, are made available by the registered person or the actual institution of audit at the place of business, whichever is later. Such audit is to be completed within 3 months from the date of commencement of audit, which may be extended by the Commissioner, where required, by a further period not exceeding 6 months. The Commissioner needs to record reasons in writing for grant of any such extension.

Section 65(5) Obligation of the auditee:

During the course of audit, the authorized officer may require the registered person,

(i) to afford him the necessary facility to verify the books of account or other documents as he may require,

(ii) to furnish such information as he may require and render assistance for timely completion of audit.

Section 65(6) Audit Report)

On conclusion of audit, the proper officer shall within thirty days, inform the registered person, whose records are audited, about the findings, his rights and obligations and the reasons for the findings. On audit completion, information is required to be Provided to the registered person including the findings during the audit in FORM GSTADT-02 within thirty days of conclusion of the audit.

Section 65(7) Consequences:

Where the audit conducted under sub-Section (1) results in detection of tax not paid or such short paid or erroneously refunded, or input tax credit wrongly availed or utilized, the proper officer may initiate action under Section 73 or 74.

In cases where tax liability is identified during the audit or input tax credit wrongly availed or utilized by the auditee , the procedure laid down under Section 73 or 74 is to be followed. Audit cannot conclude automatically resulting in a demand. Independent application of mind is necessary for a valid demand to be raised.

Access to business Premises – Section 71.

Any officer under this Act, authorised by the proper officer not below the rank of Joint Commissioner, shall have access to any place of business of a registered person, To inspect books of account, documents, computers, computer programs, computer software whether installed in a computer or otherwise and such other things as he may require and which may be available at such place, For the purposes of carrying out any audit, scrutiny, verification and checks as may be necessary to safeguard the interest of revenue. Every person in charge shall, make available to the audit party the following: such records as prepared or maintained by the registered person and declared to the proper officer in such manner as may be prescribed; trial balance or its equivalent; statements of annual financial accounts, duly audited, wherever required; Cost audit report, if any, under section 148 of the Companies Act, 2013; Income-tax audit report, if any, under section 44AB of the Income-tax Act, 1961; any other relevant record,

Option given to conduct audit either at the place of business of a registered person or in their office. In view of emphasis on trade facilitation, intelligent enforcement and providing non-intrusive environment to taxpayers, it has been decided to move from the present system of premises-based audit to desk-based (office) audit in case of small category of taxpayers. However, in case of non-cooperation by the taxpayers, premises-based audit may be carried out after approval by the Commissioner. (Para 5.7.7 of the GST Audit Manual)

Rule 101 – Audit

This rule was made and amended vide the following notifications

(1) The period of audit to be conducted under sub-section (1) of section 65 shall be a financial year 1or part thereof or multiples thereof.

(2) Where it is decided to undertake the audit of a registered person in accordance with the provisions of section 65, the proper officer shall issue a notice in FORM GST ADT-01 in accordance with the provisions of sub-section (3) of the said section.

(3) The proper officer authorised to conduct audit of the records and the books of account of the registered person shall, with the assistance of the team of officers and officials accompanying him, verify the documents on the basis of which the books of account are maintained and the returns and statements furnished under the provisions of the Act and the rules made thereunder, the correctness of the turnover, exemptions and deductions claimed, the rate of tax applied in respect of the supply of goods or services or both, the input tax credit availed and utilised, refund claimed, and other relevant issues and record the observations in his audit notes.

(4) The proper officer may inform the registered person of the discrepancies noticed, if any, as observed in the audit and the said person may file his reply and the proper officer shall finalise the findings of the audit after due consideration of the reply furnished.

(5) On conclusion of the audit, the proper officer shall inform the findings of audit to the registered person in accordance with the provisions of sub-section (6) of section 65 in FORM GST ADT-02.

(1 Inserted in Central Goods and Services Tax (Fourteenth Amendment) Rules, 2018, vide Notification No. 74/2018 Central Tax (dated 31st December 2018))

The registered person shall be informed by way of a notice not less than fifteen working days prior to the conduct of audit in Form ADT 01. If department letter for conducting audit is not replied, following actions to be taken: Note sent to executive Commissionerate for taking appropriate action; Inclusion in the Risk Parameters for future – To be identified for audit on priority; Downgrading of the GST compliance ratings, The audit shall be completed within a period of three months from the date of commencement of the audit.

If commissioner is satisfied that audit in respect of such registered person cannot be completed within three months, he may, for the reasons to be recorded in writing, extend the period by a further period not exceeding six months. Commencement of audit shall mean the date on which the records and other documents, called for by the tax authorities, are made available by the registered person or the actual institution of audit at the place of business, (whichever is later).

- During the course of audit, the authorized officer may require the registered person,

- To afford him the necessary facility to verify the books of account or other documents as he may require;

- To furnish such information as he may require and render assistance for timely completion of the audit.

- On conclusion of audit, the proper officer shall, within thirty days, inform the registered person about findings, rights and obligations and the reasons for such findings in Form ADT 02. – [Proper officer is AC/ DC]

Where the audit results in detection of tax not paid or short paid or erroneously refunded, or input tax credit wrongly availed or utilised, the proper officer may initiate action under section 73 or section 74 – [Superintendent for S. 73 and AC/ DC for S.74].

Periodicity of Audit & Selection Criteria.

Audit to be conducted for a financial year [or part thereof] or multiples thereof;Audit is sample selection driven, Criteria for selection to be as under:

Risk Based Selection v/s earlier turnover/ taxes paid basis selection Theme Based Selection

Deferment for Accredited Taxpayers – 3 years from the date of last audit 20% cases to be identified based on the local risk parameters as under:

Taxpayer did not provide/delayed in providing documents sought by the Audit Team;

♦ Inconsistency in filing of tax returns by the taxpayers;

♦ Taxpayer’s return was previously investigated for evasion;

♦ Taxpayer received notices from other governmental entities;

♦ Quality of the Taxpayer’s books and records not well-kept;

♦ Taxpayer has supplied goods on which there has been reduction in rate of duty, in order to examine the possibility of profiteering u/s 171 of the CGST Act, 2017;

♦ Higher incidence of supplies without issuance of e-way Bills have been noticed.

SEC: 66 SPECIAL AUDIT

Section 66(1)

If at any stage of scrutiny, enquiry, investigation or any other proceedings before him, any officer not below the rank of Assistant Commissioner having regard to the nature and complexity of the case and interest of revenue, is of the opinion that the value has not been correctly declared or the credit availed is not within the normal limits, he may, with the prior approval of the commissioner, direct such taxable person by a communication in writing to get his records including books of account examined and audited by a chartered accountant or a cost accountant as may be nominated by the Commissioner.

An Assistant commissioner based on the nature and complexity of business and is of the opinion that

— Value has not been correctly declared; or ,

— Credit availed is not within the normal limits.,

after commencement and before completion of any scrutiny, enquiry, investigation or any other proceedings under the Act, may direct a registered person to get his books of accounts audited by an expert. Such direction is to be issued in FORM GST ADT-03.

The Assistant Commissioner needs to obtain prior permission of the Commissioner to issue such direction to the taxable person Identifying the expert is not left to the registered person whose audit is to be conducted but the expert is to be nominated by the Commissioner.

Section 66(2)

The chartered accountant or cost accountant so nominated shall, within the period of ninety days, submit a report of such audit duly signed and certified by him to the said Assistant Commissioner mentioning therein such other particulars as may be specified:

Provided that the Assistant Commissioner may, on an application made to him in this behalf by the registered person or the chartered accountant or cost accountant or for any material and sufficient reason, extend the said period by a further period of ninety days.

Section 66(3)

The provision of sub-Section (1) shall have effect notwithstanding that the accounts of the registered person have been audited under any other provision of this Act or any other law for the time being in force.

Section 66(4)

The registered person shall be given an opportunity of being heard in respect of any material gathered on the basis of special audit under sub-Section (1) which is proposed to be used in any proceedings under this Act or rules made thereunder:

Section 66(5)

The expenses of the examination and audit of records under sub-Section (1), including the remuneration of such chartered accountant or cost accountant, shall be determined and paid by the Commissioner and such determination shall be final.

The Chartered Accountant or the Cost Accountant so appointed shall submit the audit report, mentioning the specified particulars therein, within a period of 90 days, to the Assistant Commissioner in FORM GSTADT-04.

Section 66(6)

Where the special audit conducted under sub-Section (1) results in detection of

- tax not paid or

- short paid or

- erroneously refunded, or

- input tax credit wrongly availed or utilized,

- the proper officer may initiate action under Section 73 or 74.

OBJECTIVES AND PRINCIPLES OF AUDIT:

- To measure the level of compliance of taxpayer in the light of various provisions of GST Act and rules thereof.

- To examine the accuracy of declarations made by assessee

- To examine if results produced by accounting system are correct wrt to the liability and ITC

- To assess under reporting of outward liability due to error,omission or deliberate deception

- To get the ‘’right tax at the right time’’

GUIDELINES TO THE DEPARTMENTAL AUDITOR

- Auditor to keep in view prevalent trade practices and economic realities of industry in which it operates.

- ‘’Auditor has to take balanced and rational approach while conducting audit’’

- To promote voluntary compliance by asessee

- Officer to maintain ‘’speaking documents’’ clearly explaining why a particular area was included in the audit plan as well as the basis for every objection.

- Officers to maintain transparency and confidentiality.

AUIDT PERIOD CAN BE:

- Financial Year

- Part of Financial year

- Multiples thereof to cover retrospective period up to the previous audit or the limitation period specified in sec 73,74 of CGST act

DURATION AND TIMELINE FOR AUDIT

- Internal guidelines state that:

- Audit that is inclusive of desk review, preparation and approval of audit plan and preparation of audit report-

- be completed within the following time period:

- LargeTaxpayers:6 to 8 working days

- MediumTaxpayers:4 to 6 working days

- SmallTaxpayers:2 to 4 working days.

- If audit is for multiple FY then above timeline to be increased by 25% for each additional year of coverage.

STAGEWISE ACTION FOR AUDIT

The processes involved in conducting GST audit are enumerated below for the ease of the officers involved in the auditing.

- Creation of Audit teams.

- Preparation of schedule on the basis of the risk assessment list provided by DG (Audit). The same is divided into annual and quarterly audit schedules.

- Allotment of taxpayers to the audit groups.

- Intimation to the Registered Person (GSTADT-01).

- Reviewing the taxpayer data -Tax Payer at a Glance (TAG), Registration, Returns, Payments, Dispute Resolution, Audit Report Utility, E-way bills &Third Party data if available.

- Conducting desk review in offline / online mode (wherever available) and uploading the result of desk review.

Preparing the audit plan in offline / online mode (wherever available) and uploading the audit plan.

- Carrying out verification and uploading the verification report,within twenty four hours of completion of audit.

- Uploading the draft audit report (DAR) for the MCM,within 10 – 15 days

- Examining the audit paras in MCM.

- Uploading the minutes of the monthly monitoring committee meetings (MCM), within twenty-four hours of the meeting.

- Uploading final audit report, within thirty days of the Meeting.

- Communicating the audit report to taxpayer (ADT-02).• Communicating to the Registered Person the future course of action in case of contested paras.

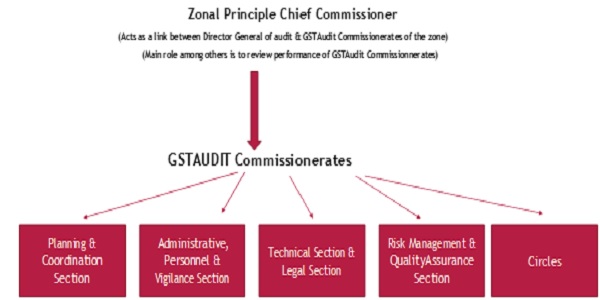

ROLE OF AUDIT COMMISSIONARATE:

Principle Commissioners & Commissioners

- To ensure selection of assesses/taxpayers, to be audited during the year, on the basis of risk assessment in consultation with the Directorate of Audit.To also ensure that 20% of the taxpayers to be audited are selected based on local risk factors and obtain the approval of the Chief Commissioner.

- To approve the Desk Review and Audit Plan, in respect of top 5 assesses of each audit circle

- To hold either circle-wise (or any number of circles together as deemed necessary), Monitoring Committee Meeting (MCM), once a month to take various decisions

- To ensure that MCM is held by using the offline Audit Report Utility and no paper-based audit report is prepared. Also, to ensure that after the MCM, each Audit Report Utility is uploaded in the Systems.

- To review audit performance and to take steps for improvement

- To take remedial measures based on the report of audit group

- To review the performance and participation of the Additional/ Joint Commissioner and Deputy/ Assistant Commissioner of audit circles

- To interact with the major assessees/trade associations, to obtain feedback on the audit system

- To submit periodical reports to various formations including Zonal ADG (Audit) or

Director General (Audit) as prescribed from time to time. To send a list containing details of show cause notices issued by the Audit Commissionerate (including Circles), during the month, to each of the Executive Commissionerate’s, on monthly basis.

Additional and Joint Commissioners

- Co-ordination, planning and overall management of the audit sections and circles including supervision of work

- To approve the desk review and audit plan, in respect of all the large and medium units, other than the top 5 units

- To review audit plans of small units approved by the Deputy/Assistant Commissioners of circles

- To interact with the management of the large units at the time of audit in order to hare major audit findings and compliance issues.

- To ensure that the Audit Report Utility is used in MCM and the reports are uploaded in system and no paper-based audit reports are prepared

- Scrutiny of NIL DARs files received from audit circles.

Deputy and Assistant Commissioners in charge of sections of Audit Commissionerate’s

To supervise the work relating to the respective sections of Headquarters viz., Planning and Co- ordination Section, administration, Personnel and Vigilance Section, Technical Section and Risk Management and Quality Assurance Section and theme-based audit

Deputy and Assistant Commissioners in charge of Circles

- Co-ordination, planning and overall management of the audit circle.

- To monitor maintenance of Registered person’s master files and registers.

- To approve the desk review and audit plan, in respect of all the small units, after ensuring that all the steps have been completed and forward a copy to JC/ADC for review.

- To interact with registered persons at the time of audit in order to share major audit findings and compliance issues.

- To approve and issue draft audit reports before placing the same in MCM meeting.

- To attend MCM and to represent the Circle in case of all DARs (Draft Audit reports) taken up for discussion during MCM.

- To issue final audit reports after approval in the MCM meeting.

- To issue show cause notices falling under his purview as per monetary limits fixed by CBIC from time to time both under Section 73 and 74 of CGST Act.

- To ensure timely preparation and forwarding of DSCNs along-with relevant documents to the Audit Commissionerate.

FACING OF DEPARTMENT AUDIT:

DOCUMENTS REQUIRED TO BE FILED DURING THE COURSE OF AUDIT

- Submission of soft copy or hard copy

- Visit of Departmental Officers

- Submission of further documents/ clarifications

- Final Audit points

- Payment of Tax/ Reply to Audit points

- Issue of Show Cause Notice

- Keep your patience

- Do not try to fight with the Officers even if they are saying something which you feel is incorrect; do not try to teach them the law

- Make your submissions in a polite manner

- Let them have small victories

- Evaluate payment vs litigation

- Good hospitality always works

- Audit = Audit points; no audit will complete unless there are audit points, so allow audit points

- This will also be a proof for future that audit for a certain period was completed

- Keep the dialogue going, do not be evasive in your reply

- If there is a non-compliance (which is not litigated and is not a point of law) e.g. late submission of returns, non-availability of documents, etc. – ADMIT without a fuss

- Finally – Co-operate, Co-operate, Co-operate with audit officers and department

ISSUES INVOLVED AT THE TIME OF AUDIT:

- Tax Payer’s Profile may not be updated one

- Address of Warehouse/ Godown not updated/not found in the Portal

- Changes in the address not updated

- Additional place of business particulars not updated

- Books of Accounts not maintained in Registered place of business address

- Storage/ Transportation documents not maintained.

- Registered place of business may be found locked.

- No proper person to answer in the registered place

- Delay in producing the required documents.

Normal audit objections raised during the course of audit:

The list is exhaustive however major items are listed:

- Input Tax Credit documents could not be made available

- Matching/ Reconciliations of ITC as per GSTR 3B, 2A, 9, 9C and Books of Accounts, then matching with Physical Invoices

- Reconciliation of annual turnover as per P/L A/c and VAT + 9/9C may be varying

- Liability under Reverse Charge Mechanism would not have been met by the dealers

- Ocean Freight liability, freight charges and other details may not be furnished, stating that own transportation.

- Liability under Service Tax/ Central Excise; maybe VAT (if audited by SGST)

- Blocked Input Tax Credit u/s 17(5)

- Liability of interest for late payment of taxes

- TRAN 1 credit documents (if TRAN 1 audit has not been done)

- Import documents/BE/BRS may not be furnished.

Other items

- Proof of payment details would not have been furnished

- Input output reconciliation could not be made as the dealers have not maintained proper statement

- Purchase orders for export would not be made available to the auditors.

- Export documents

- Claim of refund and other related documents

- Proper Reversal of ITC on required fields would not have been made.

- Wrong claim of input tax credit

- Details for income shown in the profit and loss account could not be explained.

- Stock Reconciliation could not be made as stock registers are not maintained.

Conclusion

Considering the detailed audit that can be carried out by the GST authorities, it is vital that the taxable person remains GST compliant by filing timely and correct GST returns and statements, ensuring that reconciled details are submitted across all the government departments and maintenance of all relevant records properly.

About the Author:

Name M.S. VIJAYAKUMAR

EUDCATIONAL QUALIFICATION: M.COM. B. ED.M.B.A. M. PHIL.HDNC.,

OCCUPATION: ASSISTANT COMMISSIONER GST (Retd), Tamilnadu India

Present position:

1 Part Time Guest Lecturer in GTN ARTS and Science College Dindigul, on Indirect Taxation.

2. Part Time Guest Lecturer in Madurai Kamaraj University Evening College Dindigul on indirect taxation and Business Management Subjects

Other Activities: 1 Updating knowledge of GST, by attending GST seminar, conference, Conducted by various platforms

2. Giving lectures and Seminars on GST on all areas in various platforms.

Publishing of Articles: So far wrote Eight Articles on various Areas of GST.

********

Author Bio