Insolvency and Bankruptcy Board of India

Facilitation/003/2020

7th August, 2020

Disclaimer: This document is issued for the sole purpose of information and educating the Insolvency Professionals. Appropriate Professional discretion and judgement needs to be exercised in using the contents of this document in the context of the actual situations handled by Insolvency Professionals.

Complete document available on www.ibbi.gov.in

About the Red Flag Document

The Insolvency and Bankruptcy Code, 2016 (the Code) mandates the Resolution Professional (RP) and the liquidator to determine if the Corporate Debtor (CD) has been subject to Avoidance transactions such as preferential transactions, fraudulent transactions, undervalued transactions, and extortionate transactions in the past, and if so, casts an obligation on the Insolvency Professional (IP) to file an application to the Adjudicating Authority (AA) for appropriate directions. The, Code, in this manner, enables the RP / Liquidator to facilitate the claw-back or disgorgement of value, if any, lost through avoidance transactions and is aligned with the objective of maximisation of value of the assets of the CD for the relevant stakeholders.

The Insolvency and Bankruptcy Board of India (IBBI) had vide its communication [bearing reference no. Facilitation Note / 001 / 2020] dated 8th May, 2020 provided some guidance on the role of RP / liquidator in respect of Avoidance Transactions for the purpose of educating the IPs and other stakeholders of corporate insolvency resolution and liquidation processes.

In furtherance to its endeavour of achieving the objectives of the Code and keeping in mind the role of an IP, IBBI has facilitated the preparation of this Document for the use of IPs in understanding and identifying various red flags which may point to the need for a review of Avoidance transactions as covered under Sections 43, 45, 50 and 66 of the Code. This document is intended to guide the IPs to identify situations which would merit such Avoidance Transaction review and resultant application to AA.

A preliminary draft of this document was enabled by Ms. Sripriya Kumar, [an IP registered with IBBI bearing registration no. IBBI/IPA-001/IP-P00771/2017-2018/11316]. The same was subsequently reviewed and further refined by other IPs and Professionals engaged in the conduct of Transaction / Forensic Audits, through the discussions and deliberations made at;

- 1st Round Table organised by IBBI on 22nd July, 2020,

- 2nd Round Table organised by IBBI in association with three Insolvency Professional Agencies, namely, the Indian Institute of Insolvency Professionals of ICAI, the ICSI Institute of Insolvency Professionals and the Insolvency Professional Agency of Institute of Cost Accountants of India on 27th July, 2020, and

- 3rd Round Table Meeting organised by IBBI on 31st July, 2020.

For the convenience of IPs, the various Red Flags have been collated and placed under the following six broad categories, namely, Red Flags related to –

a) Entity, Group and Operations

b) Maintenance of Books and Records

c) Regulatory Compliance and Litigation

d) Independent Auditor Reports

e) Financial Statements and Board Reports, and

f) Classification and Reporting of Frauds (as covered under RBI Master Directions).

The same are also explained in detail in various chapters under this document.

Index

List of Chapters.

| Chapter No | Particulars | Page No | |

| From | To | ||

| 1 | Entity, Group and Operations. | 4 | 7 |

| 2 | Maintenance of Books and Records. | 8 | 8 |

| 3 | Regulatory Compliance and Litigation. | 9 | 10 |

| 4 | Independent Auditor Reports. | 11 | 12 |

| 5 | Financial Statements and Board Reports. | 13 | 16 |

| 6 | Classification and Reporting of Frauds (as covered under RBI Master Directions). | 17 | 18 |

List of Annexures.

| Chapter No | Particulars | Page No | |

| From | To | ||

| 1 | List of provisions of Code read with Regulations made thereunder, in connection with Avoidance Transactions. | 19 | 21 |

| 2 | Indicative Flow Chart – Duties and responsibilities of the RP in respect of avoidance transactions. | 22 | 22 |

Chapter-1: Entity, Group and Operations.

This chapter provides some guidance to an IP in understanding certain Red Flags emanating from the entity, nature and scale of an operations, presence and predominance of related and connected entities, and management of the entity.

Entity and Operations

1.1 The IP should gain a thorough understanding of the nature of business of the entity. For instance, certain categories of enterprises operating in domains such as Trading Infrastructure, Construction, EPC Contracts, Real Estate Power, Steel etc. may be more prone to avoidance transactions than others. This is an illustrative list and the IP should review the functioning of the CD in the context of the nature of industry, level and scale of operations, market, finance and supply chain pressures that may have existed.

1.2 Any material changes to the business operations such as acquisition of a new division, sale of a division or a part of the undertaking, new investments in other entities, divestments , transfers of intangible assets of the CD such as Brands, sale of large part of fixed assets or certain categories of fixed assets etc need to be specifically understood as these may be potential Red The Segment Reporting in the Annual Financial Statements of an entity would provide some insights on various business segments of the CD.

1.3 The IP should also gain a thorough understanding of the scale of operations of the CD by reviewing the Balance Sheet, Profit & Loss Account and Cash Flow Statements to identify any unusual variance, across years, in the scale of operations or in the components of the financial statements. Special attention may be paid to large values of prior period items, transaction reversals, write-off of inventories or receivables, large provisions for obsolescence of inventory etc.

1.4 Entities marked by complex or unusual transaction structures such as sole selling arrangements, sole buying arrangements, pre-buy decisions, single sourcing strategies without competitive sourcing, high level of import – export and other related forex transactions etc may also be considered as an entity level Red Flag. High level of trading transactions in case of non – trading entities is also a potential Red Flag.

1.5 Predominance of cash transactions generally undertaken by the entity is a potential Red Flag indicator. Claims, if any, admitted on the basis of cash transactions would also merit review from an Avoidance perspective.

1.6 Due regard may also be given to the fact as to whether the Registered Office of the CD is present at the address which is stated in the records of Ministry of Corporate Affairs (MCA). The non-existence of an office of the CD at such an address is also a Red Flag.

1.7 Presence of the CD / Connected or related entities in foreign locations is a Red Flag indicator and all investment, purchase, sales, loan transactions with such units and entities merits review. Any reports on the non-compliances with provisions of Foreign Exchange Management Act (FEMA) also need to be looked into.

Directors & Key Managerial Personnel

1.8 The IP should review if the affairs of the Company – Financial as well as operations related matters were handled by a competent team in place. If such teams were inadequate and / or absent, the same may be a Red Flag with possibility of Avoidance Transactions having occurred due to lack of relevant checks and balances.

1.9 The Directors being disqualified under Sec 164(2) of the Companies Act, 2013 for non-filing of Annual Financial Statements pertaining to the CD is a Red Flag.

1.10 In certain cases, Directors of the CD may be disqualified for non-filing of financial Statements of any of the connected / related entities of the This is a potential Red Flag to be considered especially if material transactions have been undertaken by the CD with such entities which may now be inactive.

1.11 Frequent changes in Directors, Key Managerial Personnel (KMP) may be a Red Flag which needs to be examined and the IP may make inquiries to ascertain the reasons there for.

1.12 The IP should assess the independence, capability and competence of the directors as well as under whose instructions they are usually accustomed to act. Presence of name-sake directors may be a Red Flag. Where the CD is part of a group with a common promoter and a large number of related and connected entities, the persons appointed as ‘Directors’ merit consideration in terms of the capability and competence to be a director.

1.13 Statutory Audits are mandated for all Companies. The IP should also pay attention to frequent changes of Auditors. Although this aspect is a qualitative assessment, the IP should also consider if the scale of the Audit firm engaged is commensurate with the size of the business operations and the credit exposures of CD. The independence of the Auditor should also be considered with regard to various provisions under the Companies Act, The IP may also conduct discussion with the Auditors to assess the need for an Avoidance review.

Group and Connected Entities

1.14 The presence of a large-number of related / connected entities to the CD is also a red Flag which calls for a thorough review for Avoidance transactions. Such data is available on the MCA website and may be summarised by the IP for all present and past directors of the entity and the various entities they were connected to. The dormancy or status of such entities also needs to be Special attention should be paid to all such entities (and transactions thereto) which are sharing common address / common e-mail address (which is also registered with the MCA) with CD.

1.15 The financial statements of the entity are normally required to present all Related Party transactions. This may be summarised to examine the quantum of such transactions and high values of such transactions is a Red Flag. This information may be corroborated with the books and records and bank statements of the CD.

1.16 The IP may also review all the Related and Connected entities of the CD to identify if any Companies are dormant and are not carrying out any material business Fund movements by the CD to and from such entities needs to be reviewed from a Red Flag perspective.

Adverse Public Domain Information and Wilful Default Status

1.17 The IP may also undertake appropriate enquiries including public domain searches to identity any materially adverse information which may be a potential red flag.

18. The IP may also obtain information whether the promoters / entities and connected entities have been marked as Wilful Defaulters by banks and financial institutions as per RBI directives as this would also be a decisive Red Flag indicator.

Earlier Forensic Reports

1.19 The IP may seek information from the past and present lenders of CD (including Banks and Financial Institutions) on various key issues in relation to the CD as may have been discussed during lenders meetings in the past. IP may consider the impact of such information as to whether the same constitutes a Red Flag.

1.20 The IP may also call for previous Avoidance (during CIRP) / Forensic reports, if The presence of the following as disclosed by the Auditor in such reports are potential Red Flags:-

-

-

- Inadequate data furnished for the purpose of the report

- Non-circulation of reports to promoters and counter party/(ies) for obtaining auditee responses

- Inconclusive reports without proper quantification of findings

- Disclaimers in a report which would vitiate the entire audit findings

-

1.21 In several cases, forensic audit reports may have not been conclusive due to non- submission of data to the audit agency. Inquiries may be made with the recipients of such reports (viz. lenders of CD) to gain a complete perspective of the matter. Circumstances such as these should be considered as Red Flags and impact of such reports on the Avoidance Review process should be duly recognised.

Other Aspects

1.22 Provision of Corporate and Bank Guarantees (BGs) to related parties and / or third parties by the CD is also a Red Flag especially when they are not related to the business of the CD. Significant Bank Guarantees (BGs) invocations and consequent financial creditor claims are a Red Flag and the IP must review the underlying transactions and genuineness of the same as it is a significant Red Flag.

1.23 If the IP or the auditors have made efforts to confirm balances of debtors, creditors, loans and advances and if a substantial amount of such balances cannot be confirmed or mails were returned back due to non-availability of addresses etc, then such matters of concern are to be considered as Red Flags as they may represent fictitious parties.

1.24 The IP should also have due regard to high value receipts and payment transactions made during the look back period to examine the possibility of Avoidance Transactions. The amount of legal and professional fees paid by the entity in the past few years may also be reviewed as a Red Flag indicator to determine possible Avoidance Transaction.

1.25 The IP should assess the quantum of claims vis-a-vis the value of the assets available for the Further, large value of claims where such transactions are not properly reflected in the financial records is also a potential Red Flag indicator.

Chapter-2: Maintenance of Books and Records and Internal Controls.

This chapter covers various red flags as given below, which are associated with Maintenance of Books and Records, aspects connected to Accounting Systems and Internal Control framework of the Company.

2.1 All Companies are required to maintain proper Books of Accounts. In certain circumstances, the very books of accounts and proper records may not be maintained and/or be produced before the IP requiring filing of applications with the Adjudicating Authority, under Sec 19(2) of the Such circumstances are a Red Flag indicator. IP may consider explore alternate procedures to enable identification of Avoidance transactions such as considering a review based on bank statements for which the lenders of CD may directly be approached to obtain such information.

2.2 Non maintenance of Secretarial books and records by the CD including relevant registers, books and records and minutes would merit significant consideration.

2.3 The IP may come across situations where the CD reports to the IP or the Adjudicating Authority a complete or partial loss of books and records due to natural calamities floods, fire etc. The IP should examine the veracity of such circumstances with reference to Board minutes, AGM minutes, Income Tax filings, subsequent financial statements etc.

2.4 In certain circumstances, the IP may notice that basic registers such as Fixed Assets registers, Inventory registers have not been maintained by the Such circumstances are Red Flag indicators and need to be appropriately considered for potential Avoidance transactions.

2.5 The IP should gain an understanding of the Accounting System and whether such systems, processes support robust accounting, checks and balances and unalterable nature of transactions. Controls must exist to prevent ante-dating of transactions. Non- existence of such controls and absence of audit logs is a Red Flag.

The IP should also understand the Internal Controls framework which have been put in place by the management of the entity to prevent and detect frauds and errors.

Chapter-3: Regulatory Compliance and Litigation.

This chapter covers various red flags as given below, which are identifiable based on the status of various regulatory compliances to be made by the CD under various statutes and litigations involving the CD. Some illustrations of major Regulatory Compliances are as under:-

3.1 As per section 204 of the Companies Act, 2013, Secretarial Audit is mandatory for certain categories of Companies. The IP should determine if such Audit was carried out and make enquiries with such Auditor to review the need for an Avoidance Review. The Scope of Secretarial Audits is to ensure compliance with laws such as Companies Act 2013, Securities Contracts (Regulation) Act, 1956, The Depositories Act, 1996, Foreign Exchange Management Act, 1999, Specific Regulations under Securities and Exchange Board of India Act, 1992, Secretarial Standards, Listing Agreements, Other laws as may be applicable specifically to the company and the Regulations made thereunder. If such Audits have not been carried out, the same is a Red Flag. Qualifications in Secretarial Audit Reports are Red Flags and all such qualifications should be properly identified.

2.6. Where Secretarial Audits are not mandated, particular emphasis may also be placed on processes adopted by the entity, in the past, to ensure Board of Directors and Shareholder approvals for certain categories of transactions as may be mandated by the Companies Act, 2013. Illustrations of such transactions would include Loans and Advances, Investments etc. made by the Company, borrowings of the Company as well as transactions undertaken with Related Parties.

3.2 Cost Audit is mandated for certain categories of Companies under the Companies Act, 2013. The non-conduct of such mandatory audit is a Red Flag. Where such audit has been conducted, adverse findings, if any, needs to be reviewed in the context of possible Avoidance transaction.

3.3 Internal Audit is mandated for certain categories of Companies under Section 138 of the Companies Act, 2013. The non-conduct of such audit is a Red Flag. Where such audit has been conducted, adverse findings, if any, needs to be reviewed in the context of possible Avoidance transaction.

3.4 The IP should also review reasons for non-conduct of other Audits such as Tax Audit as required under Section 44AB of the Income Tax Act, GST Audit as required by the GST Act etc. Such non conduct of audit as required under other statues is a potential Red Flag. If such audits were conducted and reports are available, adverse findings, if any, need to be addressed as considered appropriate in the facts and circumstances of the particular case.

3.5 Non-registration of the CD / its connected entities with Goods and Services Tax (GST)/ Income Tax (IT) authorities and other mandatory registrations and non-filing of periodic returns is a Red Returns where filed may also be reviewed to identify possible Avoidance Transactions.

3.6 Any cases filed by Regulatory authorities such as Securities and Exchange Board of India (SEBI), Serious Fraud Investigation Office (SFIO), Central Bureau of Investigation (CBI), Police, RBI, FEMA etc and findings of search and seizures etc by IT/GST/VAT authorities need to be reviewed. In this regard, the IP may call for all such information as well information on all payments to legal counsels and other professionals to identify such instances.

3.7 High value of legal and professional fees consistently paid by the entity may indicate possibility of litigation, the basis of which needs to be examine.

3.8 Various litigations raised by / against the CD by the debtors / creditors of the CD in various judicial and quasi-judicial forums may also provide rationale for conduct of Avoidance reviews. The IP may also obtain information in this regard from Public Domain to the extent possible.

3.9 All arbitrations initiated by / against the CD and involving material amount is also a Red Flag. These should be corroborated with claims admitted on the basis of such awards. Related party litigations and arbitral awards, if any also need to be The IP must obtain details of all Arbitration proceedings by or against the CD before various such Sole Arbitrators or panels. In such cases, all the applications filed before such Tribunals and facts placed should be such forums should be reviewed.

Chapter-4: Audited Financial Statements and Independent Auditor Reports.

This chapter covers various red flags as given below, which may be associated with Annual Audited Financial Statements and Disclosures, Remarks, Qualifications, Matters of Emphasis, Key Audit Matters etc which are mentioned in the Independent Statutory Audit Reports of the Company.

4.1 Preferential, Undervalued, fraudulent and Extortionate transactions can occur in any of the components of the financial statements including off Balance Sheet items such as Contingent Liabilities. IP therefore, must gain a thorough understanding of the Balance Sheet, Profit and Loss Account, Cash Flow Statements, Notes to Accounts in the financial statements, Independent Auditors report, Auditor Report under Company Auditor’s Report Order (CARO), Auditors report on Internal Financial Controls over Financial Reporting (ICOFR) for at least last 8 years preceding the Insolvency Commencement Date (ICD) to ascertain any unusual and material items contained therein.

4.2 The Companies Act, 2013 requires that Audited Financial Statements must be submitted to the MCA every year. Non filing of such statements is a Red Flag.

4.3 The IP may also come across situations where he / she may be informed that such Audited Financial Statements were never prepared. The Annual Financial Statements present a view of the financial position and affairs of the CD and the Reporting framework ensures that the Financial position, profit or loss and other material qualitative and quantitative information is properly disclosed and presented by the management of the entity and opined on by the Auditors. Non preparation and audit of the same is a Red Flag that needs to be duly considered by the IP.

4.4 Certain classes of Companies are required to prepare Consolidated Financial Statements in respect of their Subsidiaries, Joint Ventures (JVs) and Associates as may be applicable. Non-preparation of such statements or non-audit of the books of such entities may also be a Red The IP may also examine and compare the scale of the Standalone Financials vis a vis the Consolidated Financials of CD for potential Red Flags.

4.5 The IP may also approach the Auditor and obtain if any other reports of findings (usually referred to as Management Letters) were issued in the course of the Audit. Adverse remarks, if any, in such communication may also be recognised.

4.6 Clean audit reports, without any qualifications and remarks will not obviate the need for an Avoidance Review as Audits are performed for a specific purpose under a framework.

4.7 Significant qualifications in the Audit reports should be construed as a Red Flag for immediate commencement of Avoidance review of the In this regard, the IP must look at the Audited Financial Statements in its entirety – Independent Auditors Report, CARO and ICOFR. Qualifications should be quantified. Absence of quantification of such qualifications may be a significant issue that needs to be looked-into. If the Auditors Reports contain same qualifications across the various years, they merit extra attention of the IP. Some illustrations of qualifications are as under:-

a. Non-compliance with Accounting Standards on material financial statement items including Revenue recognition, Inventories, Payroll cost liabilities, forex transactions which may have resulted in excess / short statement of financial position.

b. Absence of fixed assets register and / or physical verification reports and CARO non compliances is a Red Flag.

c. Qualifications on investments in other entities – Investee Companies, Associates, Subsidiaries, JVs of the CD is a Red Flag.

d. High value Inventory not verified by the Auditor but certified by the management, and that too for many consecutive years is a Red Flag.

e. Violations of Section 73 (which pertains to acceptance of deposits), Section 74 (which pertains to repayment of deposits), Section 185 (which pertains to loans or advances to directors by a Company), and/or Section 186 (which pertains to loans and investments by a Company) of the Companies Act is a Red Flag.

f. Auditors comments on non-recoverability of advances is a Red Flag.

g. Confirmation of balances not obtainable by the auditors for Receivables, payables and loans and advances although they are material sums is a Red Flag.

h. Invocation of guarantees by bankers and entire amounts considered as receivables by the CD is a Red Flag.

i. Customer payments directly to vendors with clients by unauthorised tripartite agreements is a Red Flag.

j. Interest free transactions undertaken by the CD, is a Red Flag.

k. Any reports on fictitious transactions or transactions reflected as mere book entries as reported by the Auditors is a Red Flag.

l. High value of disputed and undisputed statutory dues of the CD is a Red Flag.

Chapter-5: Financial Statements and Board Report.

This chapter covers various red flags as given below, which are associated with Financial Statements and Board Report of CD:-

5.1 General Red Flags

- Non preparation of financial statements for past years and current

- Non filing of the financial statements to

- Filing of unsigned financial statements to MCA to maintain compliance

- Financial Statements not approved by the Board of Directors &

- Financial Statements signed by Directors who are disqualified under Section 164(2) of Companies Act,

- Incomplete Board Reports not in line with Companies Act,

- Repeat Qualifications by Auditors on the financial statements across many

- Specific matters such as Frequent Changes in Accounting Policies, High value of Related Party Transactions

5.2 Red Flags related to Fixed Assets and Capital Work in Progress

- Lack of Approval process in relation to acquisition / alienation of assets including Board / Shareholder approvals where

- Fixed Assets not properly handed over to the Insolvency Professional after reconciliation of assets held in books vs actual assets physically

- Significant variation between Registered Valuer reports on assets and the actual status of fixed assets of the

- Assets feature in the Balance Sheet of the Company and title not held by the

- Absence of a proper Fixed Assets

- Absence of periodic verification of fixed assets by the

- Assets in transit / not cleared from port for a significant period of

- Assets used by other entities on a free of cost/ lower than charge

- Significant Aging of Capital Work in Progress to be corroborated with Registered Valuation

- Significant Revaluation Reserves in the Balance Sheet of the

- Sale and Lease back transactions of assets pledged in favor of

- Un-authorised creation of security

- Assets used for personal purposes of promoters and cost borne by the

- Large sales of assets – Undervalued sale of assets without valuation reports / competitive sale process resulting in erosion of value.

5.3 Red Flags related to Special Purpose Vehicles (SPVs) and Investments in entities

- Incorporation of SPV and transfer of funds to such entities without underlying business purpose.

- Significant investments in partnership firms and other unincorporated entities.

- Indian SPV subject to strike off and loss of trail of funds.

- Foreign SPV closed without notice to lenders and no trace of funds moved and utilization.

- Creation of assets abroad and creation of assets in related entities.

- Sale / transfer of business divisions or segments which are key revenue earners.

- Funds – investments in connected / related entities with no business purpose without lender consent for diversion.

- Shares of investee entities purchased as investments at exorbitant / unjustified premiums.

- No return on investments in terms of dividends or refund of capital even after long periods of time.

- Large value investments extinguished / written off and recorded as losses without proper rationale and eroding the net worth.

- Shareholding diluted by fraudulent / collusive rights issue process, relinquishments by CD in investee companies.

5.4 Inventories and Purchases

- Inventories not properly handed over to the Insolvency Professional.

- Inventory registers not maintained by the entity or not maintained properly.

- No proper internal controls over receipts, issues and closing balances of inventory.

- No proper physical verification protocols and reconciliation to books of accounts.

- Variances between Stock reporting to lenders and books of accounts.

- Sale of inventory other than in normal course of Business.

- Large sales returns to certain operational creditors to enable preferential payments for current transactions in the ordinary course of Business.

- Significant write offs of inventories.

- Significant provisions carried for obsolete, slow-moving and non-moving inventory.

- Inventories used for personal/ other related entities purposes of promoters and cost borne by the CD.

- Inflated stock and book debts reporting without any underlying inventory.

- Inability of carry out a Registered Valuation of inventories.

- Significant variation between Registered Valuer reports on inventory and actual inventory held as per the books of accounts.

5.5 Revenues and Receivables

- Customer master data is not maintained properly and is incomplete.

- Fraudulent accounting and reporting of sales and inflation of receivable.

- High value discounts offered to some customers and not to others.

- Collections routed through non authorized bank accounts or received in cash.

- Customer payments are made directly to vendors / promoters and receivable balances are not reconciled.

- Significant aging of Receivables balances.

- Assignment of receivables to third parties / related parties.

- Large receivables extinguished / written off and recorded as losses without proper rationale/ legal efforts and eroding the net worth.

- Fictitious Bank receipts (in bank book but not in bank statements).

- Sudden increase in unbilled revenue.

- Receivables written off on the basis of arbitral award.

- Audit qualifications on Revenue recognition, inability to obtain balance confirmations.

- Inflated book debts reporting to bankers not reconciled to books of accounts.

5.6 Bank Transactions

- Presence of a high number of bank accounts and inter-se movement of funds.

- Diversion of funds to parties other than normal business payees.

- Round tripping of funds between various cash credit accounts held with different bankers to enhance debit and credit summations of bank accounts.

- Fund movements not through designated consortium accounts.

5.7 Loans and Advances

- Loans and advances given without any agreements and legal resources.

- Loans to directors / entities for no business purpose and includes related / connected entities.

- Significant aging of loan balances.

- Loans and advances on an interest free basis although interest is paid by the CD.

- Large value loans and advances written off without any legal recourse / attempts to collect and eroding the net worth.

- Loans and advances outstanding in entities which are under “strike-off” as per MCA records and no proceedings are stated as possible.

5.8 Share Capital / Premium and utilization of proceeds

- Share Capital not received by bank funds process but by adjustment entities.

- Return of allotment not filed or filed with wrong facts and figures.

- Exorbitant Share Premium from investor companies not through bank sources and/ or diverted back later.

- Shareholding in the CD is fictitious – the Investor – Shareholders have themselves extinguished the investments in their Balance Sheets.

- Company funds have been used to purchase shares of the Company by directors.

5.9 Loan transactions

- Loans recorded by mere book entries without corresponding bank inflows – Preference / Fraudulent.

- Round Tripping Loans received, diverted to other group / connected entities without any business purpose – Diversion of funds.

- Loans taken without No objection from existing lenders and security interest created thereon.

- Unsecured loan becomes a Secured loan without new value.

- Loans stated as received in Cash.

- Certain loans settled in priority over some other loans.

- Loans received at exorbitant rates of interest or security created.

- Stated as Secured loan by unregistered Memorandum of Deposit of Title Deed (MoDTD) and ante dated transaction.

- Where loans have been recognized due to invocation of Bank Guarantees (BGs), where such BGs did not reflect genuine business transaction.

- Security interests and claims recognized on basis of award by Court or Tribunal.

- Conversion of unsecured loan to secured loans in order to defraud the other secured creditors impacting the waterfall mechanism under section 53 of the Code.

5.8 Payable Accounts

- Fictitious purchases of goods and services and consequent liabilities and losses.

- Transactions especially with Related Parties not on an arms-length basis.

- Significant aging of Payables balances.

- High value Sole Selling or Purchase agents and / or related parties.

- Creditors settled directly by customers but still showing as outstanding both for receivables and payables.

Chapter-6: Classification and Reporting of Frauds. (as covered under RBI Master Directions)

6.1 The RBI had issued Master Directions1 to banks with a view to providing a framework to banks enabling them to detect and report frauds early and taking timely consequent actions and also to enable faster dissemination of information by RBI to banks on the details of frauds, unscrupulous borrowers and related parties, based on banks’ reporting so that necessary safeguards / preventive measures by way of appropriate procedures and internal checks may be introduced and caution exercised while dealing with such parties by banks.

6.2 The Master Directions covers an illustrative list of around 42 signals also called as Early Warning Signals (EWS). The presence of one or more such EWS may indicate suspicion of fraudulent activity in a loan account and put the bank on alert regarding a weakness or wrong doing which may ultimately turn out to be fraudulent.

6.3 IP can consider these 42 EWS as listed below, as equally relevant from the perspective of Avoidance Transactions. Some of these may have already been considered in the above paragraphs of this note.

1. a) Default in undisputed payment to the statutory bodies as declared in the Annual report.

b) Bouncing of high value cheques.

2. Frequent change in the scope of the project to be undertaken by the borrower.

3. Foreign bills remaining outstanding with the bank for a long time and tendency for bills to remain overdue.

4. Delay observed in payment of outstanding dues.

5. Frequent invocation of BGs and devolvement of LCs.

6. Under insured or over insured inventory.

7. Invoices devoid of TAN and other details.

8. Dispute on title of collateral securities.

9. Funds coming from other banks to liquidate the outstanding loan amount unless in normal course.

10. In merchanting trade, import leg not revealed to the bank.

11. Request received from the borrower to postpone the inspection of the godown for flimsy reasons.

12. Funding of the interest by sanctioning additional facilities.

13. Exclusive collateral charged to a number of lenders without NOC of existing charge holders.

14. Concealment of certain vital documents like master agreement, insurance coverage.

15. Floating front / associate companies by investing borrowed money.

16. Critical issues highlighted in the stock audit report.

17. Liabilities appearing in ROC search report, not reported by the borrower in its annual report.

18. Frequent request for general purpose loans.

19. Frequent ad hoc sanctions.

20. Not routing of sales proceeds through consortium member bank/ lenders to the company.

21. LCs issued for local trade related party transactions without underlying trade transaction

22. High value RTGS payment to unrelated parties.

23. Heavy cash withdrawal in loan accounts.

24. Non-production of original bills for verification upon request.

25. Significant movements in inventory, disproportionately differing vis-a-vis change in the turnover.

26. Significant movements in receivables, disproportionately differing vis-a-vis change in the turnover and/or increase in ageing of the receivables.

27. Disproportionate change in other current assets.

28. Significant increase in working capital borrowing as percentage of turnover.

29. Increase in Fixed Assets, without corresponding increase in long term sources (when project is implemented).

30. Increase in borrowings, despite huge cash and cash equivalents in the borrower’s balance sheet.

31. Frequent change in accounting period and/or accounting policies.

32. Costing of the project which is in wide variance with standard cost of installation of the project.

33. Claims not acknowledged as debt high.

34. Substantial increase in unbilled revenue year after year.

35. Large number of transactions with inter-connected companies and large outstanding from such companies.

36. Substantial related party transactions.

37. Material discrepancies in the annual report.

38. Significant inconsistencies within the annual report (between various sections).

39. Poor disclosure of materially adverse information and no qualification by the statutory auditors.

40. Raid by Income tax /sales tax/ central excise duty officials.

41. Significant reduction in the stake of promoter /director or increase in the encumbered shares of promoter/director.

42. Resignation of the key personnel and frequent changes in the management.

Annexure-1

List of provisions of Code read with Regulations made thereunder, in connection with Avoidance Transactions.

- Sections 25 of the Code requires Resolution Professional (RP) to file application for avoidance of transactions in accordance with Chapter III, if any.

- Regulation 35A of the CIRP Regulations provide that;

- Within 75 days of the commencement of CIRP, RP to form an opinion on preferential and other transactions.

- Within 115 days of commencement of CIRP, RP to make a determination on preferential and other transactions.

- Within 135 days of commencement of CIRP, RP to file applications to AA for appropriate relief.

- Regulation 39 (2) of the CIRP Regulations require and IP to submit to the CoC, all resolution plans which comply with the requirements of the Code and regulations made thereunder along with the details of avoidance of transactions, if any, observed, found or determined by him: –

- Section 35 of the Code empowers Liquidator to investigate the financial affairs of the corporate debtor to determine undervalued or preferential transactions.

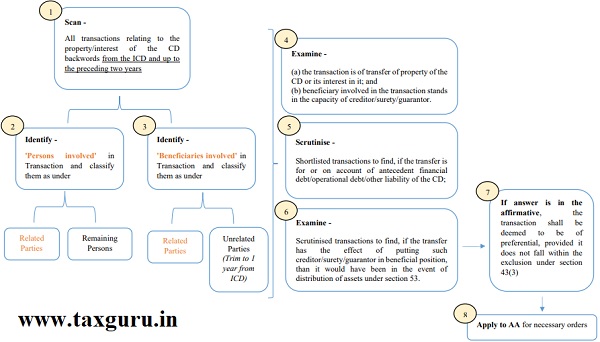

- Section 43 of the Code [Preferential transactions]

- RP or Liquidator to form opinion and apply to AA for order –

- Where RP or Liquidator is of the opinion that CD has at a relevant time given a preference in such transaction in such manner, to any person as referred under the this section, he shall apply to AA for avoidance of such preferential transactions for one or more of the orders as referred to in Section 44 of the Code.

- Manner of giving Preference –

- Transfer of CD’s Property or an interest thereof to creditor/surety/guarantor on account of CD’s antecedent financial /operational debt / other liabilities (i.e. CD’s prepetition obligation which existed before a CD’s transfer of an interest in property).

- The aforesaid transfer puts such creditor/surety/guarantor in a beneficial position than it would have been in the event of distribution of assets as per waterfall mechanism under section 53 of the Code.

- Exclusions to ‘Preference’ –

- Transfer made in the ordinary course of business / financial affairs of CD or the transferee.

- Any transfer creating a security interest in the property acquired by CD to the extent of;

- Such security interest secures a ‘new value’ and was given at the time of or after signing the security agreement that contains a description of such property as ‘security interest’ and was used by the CD to acquire such property and,

- Such transfer was registered with an IU on or before 30 days after the CD receives possessions of such property. New Value means money or its worth in goods, services or new credit, or release by the transferee of property previously transferred to such transferee in a transaction that is neither void nor voidable by the RP or Liquidator including proceeds of such property, but does not include a financial / operational debt substituted for existing financial / operational debt.

- Any transfer made, pursuant to order of Court, shall not preclude (i.e. prevent) such transfer to be deemed as giving of preference by CD.

- Relevant Time and Persons –

- Preference given to a related party (other than by reasons only of being an employee), during the period of 2 years preceding the Insolvency Commencement Date (ICD).

- Preference given to a person other than a related party during the period of 1 year preceding the Insolvency Commencement Date (ICD).

- RP or Liquidator to form opinion and apply to AA for order –

- Section 45 of the Code [Undervalued transactions]

- RP or Liquidator to form opinion and apply to AA for order –

- Where RP or Liquidator is of the opinion that certain transactions were made during the relevant period which were undervalued, he shall make an application to AA to declare such transactions as void and reverse the effect of such transactions.

- Transactions to be considered as undervalued, where CD –

- Makes a gift to a person or,

- Enters into a transaction with such person which involves the transfer of one or more assets of CD for a consideration the value of which is significantly less than the value of consideration provide by the CD, and

- Such transaction has not taken place in the ordinance course of business of CD.

- Exclusions to ‘Undervalued Transactions’ –

- Transactions made in the ordinary course of business of CD

- Relevant Time and Persons –

- Transactions made with a related party within the period of 2 years preceding the Insolvency Commencement Date (ICD).

- Transactions made with any person with the period of 1 year preceding the Insolvency Commencement Date (ICD).

- AA may require an independent expert to assess evidence relating to the value of transactions.

- RP or Liquidator to form opinion and apply to AA for order –

- Section 50 of the Code [Extortionate credit transactions]

- RP or Liquidator to form opinion and apply to AA for order –

- Where the CD has been a party to an extortionate credit transaction, involving the receipt of financial or operational debt during the period within two years preceding the insolvency commencement date, the RP or Liquidator, may make an application for avoidance of such transaction to the AA, Adjudicating Authority if the terms of such transaction required exorbitant payments to be made by the corporate debtor.

- Exclusions –

- Any debt extended by any person providing financial services which is in compliance with any law for the time being in force in relation to such debt shall in no event be considered as an extortionate credit transaction.

- Circumstances in which a transactions which shall be covered [Specified under Regulation 5 of CIRP Regulations] –

- A transaction shall be considered extortionate under section 50(2) where the terms:

- require the CD to make exorbitant payments in respect of the credit provided; or

- are unconscionable under the principles of law relating to contracts.

- A transaction shall be considered extortionate under section 50(2) where the terms:

- RP or Liquidator to form opinion and apply to AA for order –

- Section 66 of the Code [Fraudulent trading or wrongful trading]

- RP or Liquidator to form opinion and apply to AA for order –

- If during the CIRP or a liquidation process, it is found that any business of the CD has been carried on with intent to defraud creditors of the CD or for any fraudulent purpose, the AA may on the application of the RP pass an order that any persons who were knowingly parties to the carrying on of the business in such manner shall be liable to make such contributions to the assets of the CD as it may deem fit.

- AA may by an order direct that a director or partner of the CD, to make such contribution to the assets of the CD as it may deem fit, if

- RP or Liquidator to form opinion and apply to AA for order –

(a) before the insolvency commencement date, such director or partner knew or ought to have known that the there was no reasonable prospect of avoiding the commencement of a CIRP in respect of such CD; and

(b) such director or partner did not exercise due diligence in minimising the potential loss to the creditors of the CD.

Annexure-2

Figure-1: Indicative Flow Chart – Duties and responsibilities of the RP in respect of avoidance transactions