Ministry of Corporate Affairs vide its notification dated 10th September, 2018 has amended the Companies (Prospectus and Allotment of Securities) Rules, 2014 by issuing Companies (Prospectus and Allotment of Securities) Third Amendment Rules, 2018 which is effective from 02nd October 2018. Rule 9A has been inserted in the said rule which deals with the issue of securities in dematerialised form by unlisted public companies. Sub rule 8 of rule 9A deals with the filing of Share Capital Reconciliation Audit report on half yearly basis with Registrar of Companies. In the previous month there was a lot of confusion in the mind of professionals regarding filing of this report with the Registrar of Companies. The rule is itself ambiguous regarding filing of report, therefore the ministry came again with amendment in the rules and amended the Companies (Prospectus and Allotment of Securities) Rules, 2014 by issuing Companies (Prospectus and Allotment of Securities) Third Amendment Rules, 2019 vide its notification dated 22nd May 2019 which is effective from 30th September 2019.

Before discussing about latest amendment regarding filing of reconciliation of share capital audit report by unlisted public companies, let’s discuss some frequently asked questions regarding applicability of Rule 9A, dematerialisation of securities, ISIN, penal provisions and others.

GENERAL FAQs:

- What is Dematerialisation:

It is the process by which an investor can get its physical share certificates converted into an equivalent number of securities in electronic form.

- Applicability of the rules:

The provisions of the rules are applicable to all unlisted public companies except to an unlisted public company which is-

1. a Nidhi Company;

2. a Government Company; or

3. a wholly owned subsidiary company

- Whether this rule is applicable to the unlisted public companies issuing debentures or other securities too?

The answer will be yes, as rule 9A(1) clearly states that every unlisted public company shall issue the securities only in dematerialized form and facilitate dematerialisation of all its existing securities. Here securities shall have the same meaning as mentioned in Securities Contracts(Regulations) Act, 1956.

As per section 2(h) of the Securities Contracts (Regulations) Act, 1956 “securities” include (i) shares, scrips, stocks, bonds, debentures, debenture stock or other marketable securities of a like nature in or of any incorporated company or other body corporate.

So if any unlisted public company is issuing debentures or any other securities after 02nd October 2018, it shall issue the same in dematerialised form only.

- What is ISIN:

An ISIN (International Securities Identification Number) is a unique 12 character alphanumeric identification number allotted for a security (e.g.‐ INE383D02568). It will be unique for each type of securities issued by the same issuer.

- RESPONSIBILITY ON THE PART OF COMPANY:

As per rule 9A(4) every unlisted public company shall:

- facilitate dematerialisation of all its existing securities by making necessary application to a depository;

- secure ISIN for each type of security; and

- inform all its existing security holders about such facility.

As per rule 9A(2) every unlisted public company shall ensure that entire holding of securities of its promoters, directors and key managerial personnel has been dematerialised in accordance with the provisions of the Depositories Act, 1996, and if not, then the company shall not be allowed to do the following:

- issue of any securities;

- buyback of securities;

- issue of bonus shares;

- right offer

As per rule 9A(5) every unlisted public company shall ensure that:

- it makes timely payment of fees (admission as well as annual) to depository, registrar to an issue and share transfer agent;

- it maintains security deposit at all times of at least 2 years Fees with depository, registrar to an issue and share transfer agent;

- it complies with the regulations or directions or guidelines issued by SEBI or Depository from time to time with respect to dematerialisation of shares of unlisted public companies.

- RESPONSIBILITY ON THE PART OF SECURITY HOLDERS:

As per rule 9A(3) every holder of securities of an unlisted public company:

- who intends to transfer its securities; or

- who intends to subscribe to any securities of an unlisted public company

on or after 02nd October 2018

shall make sure that all his existing securities are held in dematerialised form before making such transfer or subscription, and if not, then the security holder shall not be able to make such transfer or subscription.

- PENAL CONSEQUENCES:

As there is no penalty prescribed under rule 9A for non-compliance thereof, therefore section 450 (Residuary provision for penalty) will come into picture.

As per section 450 of the Companies Act, 2013, if penalty has not been prescribed for non-compliance of any section or rule, then penalty shall be levied as per section 450.

Penalty: The Company and every officer of the company who is in default or such other person shall be punishable with fine which may extend to ten thousand rupees, and where the contravention is continuing one, with a further fine which may extend to one thousand rupees for every day after the first during which the contravention continues.

⇒ RECONCILIATION OF SHARE CAPITAL AUDIT REPORT

- Pre-amendment / Earlier Provisions related to filing of report with ROC:

As per rule 9A(8), the audit report provided under regulation 55A of the Securities and Exchange Board of India (Depositories and Participants) Regulations, 1996 shall be submitted by the unlisted public company on a half-yearly basis to the Registrar under whose jurisdiction the registered office of the company is situated.

- Post-amendment / Current Provisions related to filing of report with ROC:

As per rule 9A(8), Every unlisted public company governed by this rule shall submit Form PAS-6 to the Registrar with such fee as provided in Companies (Registration Offices and Fees) Rules, 2014 within sixty days from the conclusion of each half year duly certified by a company secretary in practice or chartered accountant in practice.

A new sub rule 8A has also been inserted which states that the company shall immediately bring to the notice of the depositories any difference observed in its issued capital and the capital held in dematerialised form.

Author’s Comment:The earlier provisions relating to filing of reconciliation of share capital audit report with ROC was ambiguous as it didn’t provide for the form in which and time within which such report to be filed with ROC. Further Securities and Exchange Board of India (Depositories and Participants) Regulations, 1996 has also been replaced by Securities and Exchange Board of India (Depositories and Participants) Regulations, 2018 w.e.f. 03rd October 2018. But as the earlier rule has been notified vide dated 10th September 2018, so new regulation has not been mentioned in the said rule.

ICSI had also made a representation before the Ministry of Corporate Affairs regarding practical difficulties faced by the professionals and company while filing such report to ROC.

Therefore it was very much imperative for the ministry to amend the rules and clear all the confusions regarding filing of such report to the ROC.

Now the Ministry of Corporate Affairs has amended the said provisions by issuing Companies (Prospectus and Allotment of Securities) Third Amendment Rules, 2019 vide its notification dated 22nd May 2019 and clarified about the form(PAS-6) and time (within 60 days from the closure of half year) for filing of Reconciliation of Share Capital audit report with Registrar of Companies.

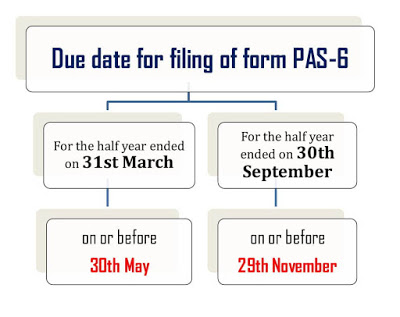

As the new rules is applicable w.e.f. 30th September 2019, so we can say that for the first time such report shall be filed for the half year ended on 30th September 2019 on or before 29th November 2019 in e-form PAS-6.

DUE DATE:

- PENAL PROVISIONS in case of non-filing of form PAS-6:

As there is no penalty prescribed under rule 9A for non-compliance thereof, therefore section 450 (Residuary provision for penalty) will come into picture.

As per section 450 of the Companies Act, 2013, if penalty has not been prescribed for non-compliance of any section or rule, then penalty shall be levied as per section 450.

Penalty: The Company and every officer of the company who is in default or such other person shall be punishable with fine which may extend to ten thousand rupees, and where the contravention is continuing one, with a further fine which may extend to one thousand rupees for every day after the first during which the contravention continues.

Disclaimer: The entire contents of this article are solely for information purpose and have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation by the Author. The Author of this Article does not constitute any sort of professional advice or a formal recommendation. The author has undertaken utmost care to disseminate the true and correct view and don’t accept liability for any errors or omissions. You are kindly requested to verify and confirm the updates from the genuine sources before acting on any of the information’s provided hereinabove. In no event the author shall be responsible for any loss or damage in any circumstances whatsoever resulting from or arising out of or in connection with the use of aforesaid information.