GOVERNMENT OF INDIA

MINISTRY OF CORPORATE AFFAIRS,

OFFICE OF REGISTRAR OF COMPANIES,

Uttar Pradesh

37/17, Westcott Building, The Mall,

Kanpur — 208001 (U.P.)

Phone : 0512 — 2310443/2310227

Order No. 03/05/SBO/UP/2024/Khvatec/ Dated: /06/ 2024

ORDER OF ADJUDICATION OF PENALTY UNDER SECTION 454 OF COMPANIES ACT, 2013 READ WITH RULE 3 OF THE COMPANIES (ADJUDICATION OF PENALTIES) RULES, 2014 FOR VIOLATION OF PROVISIONS OF SECTION 90 OF THE COMPANIES ACT, 2013

Date of Hearings: 21.05.2024 and 12.06.2024

Present on behalf of Company and Applicants: Ms. Sandhya Pandey, Company Secretary, KMP of the Company appeared on 21.05.2024 and Mr. Suresh Pandey, Practicing Company Secretary appeared on 12.06.2024.

1. The Ministry of Corporate Affairs vide its gazette notification no A-42011/112/2014-Ad.II dated 24.3.2015, appointed the Registrar of Companies, Uttar Pradesh as the Adjudicating Officer in exercise of the powers conferred by Section 454(1) of the Companies Act, 2013 (hereinafter known as “the Act”) read with Companies (Adjudication of Penalties) Rules, 2014 for adjudging penalties under the provisions of this Act.

2. Whereas the company viz. KHVATEC INDIA PRIVATE LIMITED (hereinafter as “the reporting company”) was incorporated under the provisions of the Companies Act, 2013 on 25.03.2019 and has its registered office situated at A-3, Block- Ecotech-VI, Sector – Ecotech -VI, Kasna, Greater Noida, Gautam Buddha Nagar, Uttar Pradesh, 201310, India. The shareholding details of the reporting company as per list of shareholders attached with e-form MGT-7 for financial year 2022-23 is as follows:-

| Shareholding Details* | |||

| Si. No. |

Name of Shareholder(s) | Number of Equity shares (face value of Rs. 10 each) | % Holding |

| 1. | Khvatec Co. Ltd. | 8,60,10,122 | 99.99 |

| 2. | jang Kuk Nam (Nominee of Khvatec Co. Ltd.) | 01 | 0.01 |

| Total | 8,60,10,123 | 100 | |

*As per reply of the Company dated 11.06.2024., Khvatec Co. Ltd. is the holding Company of the Company since incorporation.

3. That the provisions of Section 90 of the Companies Act, 2013 reads:-

Section 90:- (1) Every individual, who acting alone or together, or through one or more persons or trust, including a trust and persons resident outside India, holds beneficial interests, of not less than twenty-five per cent. or such other percentage as may be prescribed, in shares of a company or the right to exercise, or the actual exercising of significant influence or control as defined in clause (27) of section 2, over the company (herein referred to as “significant beneficial owner”), shall make a declaration to the company, specifying the nature of his interest and other particulars, in such manner and within such period of acquisition of the beneficial interest or rights and any change thereof, as may be prescribed:

Provided that the Central Government may prescribe a class or classes of persons who shall not be required to make declaration under this sub-section.

(2) Every company shall maintain a register of the interest declared by individuals under sub-section (1) and changes therein which shall include the name of individual, his date of birth, address, details of ownership in the company and such other details as may be prescribed.

(3) The register maintained under sub-section (2) shall be open to inspection by any member of the company on payment of such fees as may be prescribed.

(4) Every company shall file a return of significant beneficial owners of the company and changes therein with the Registrar containing names, addresses and other details as may be prescribed within such time, in such form and manner as may be prescribed.

(4A) Every company shall take necessary steps to identify an individual who is a significant beneficial owner in relation to the company and require him to comply with the provisions of this section.]

(5) A company shall give notice, in the prescribed manner, to any person (whether or not a member of the company) whom the company knows or has reasonable cause to believe

(a) to be a significant beneficial owner of the company;

(b) to be having knowledge of the identity of a significant beneficial owner or another person likely to have such knowledge; or

(c) to have been a significant beneficial owner of the company at any time during the three years immediately preceding the date on which the notice is issued, and who is not registered as a significant beneficial owner with the company as required under this section.

(6) The information required by the notice under sub-section (5) shall be given by the concerned person within a period not exceeding thirty days of the date of the notice.

(7) The company shall,—

(a) where that person fails to give the company the information required by the notice within the time specified therein; or

(b) where the information given is not satisfactory, apply to the Tribunal within a period of fifteen days of the expiry of the period specified in the notice, for an order directing that the shares in question be subject to restrictions with regard to transfer of interest, suspension of all rights attached to the shares and such other matters as may be prescribed.

(8) On any application made under sub-section (7), the Tribunal may, after giving an opportunity of being heard to the parties concerned, make such order restricting the rights attached with the shares within a period of sixty days of receipt of application or such other period as may be prescribed.

(9) The company or the person aggrieved by the order of the Tribunal may make an application to the Tribunal for relaxation or lifting of the restrictions placed under subsection (8), within a period of one year from the date of such order:

Provided that if no such application has been filed within a period of one year from the date of the order under sub-section (8), such shares shall be transferred,without any restrictions,to the authority constituted under sub-section (5) of section 125, in such manner as may be prescribed;

(9A) The Central Government may make rules for the purposes of this section.

(10) If any person fails to make a declaration as required under sub-section (1), he shall be liable to a penalty of fifty thousand rupees and in case of continuing failure, with a further penalty of one thousand rupees for each day after the first during which such failure continues, subject to a maximum of two latch rupees.

(11) If a company, required to maintain register under sub-section (2) and file the information under sub-section (4) or required to take necessary steps under sub-section (4A), fails to do so or denies inspection as provided therein, the company shall be liable to a penalty of one lakh rupees and in case of continuing failure, with a further penalty of five hundred rupees for each day, after the first during which such failure continues, subject to a maximum of five lakh rupees and every officer of the company who is in default shall be liable to a penalty of twenty-five thousand rupees and in case of continuing failure, with a further penalty of two hundred rupees for each day, after the first during which such failure continues, subject to a maximum of one lakh rupees.

(12) If any person willfully furnishes any false or incorrect information or suppresses any material information of which he is aware in the declaration made under this section, he shall be liable to action under section 447.

4. (1) That Section 2(27) of the Act defines ‘Control’

“control” shall include the right to appoint majority of the Directors or to control the management or policy decisions exercisable by a person or persons acting individually or in concert, directly or indirectly, including by virtue of their shareholding or management rights or shareholder’s agreements or voting agreements or in any other manner;

(ii) That Section 2(1) of the Companies (Significant Beneficial Owners) Rules, 2018 of the Act defines “significant influence” means the power to participate, directly or indirectly, in the financial and operating policy decisions of the reporting company but is not control or joint control of those policies.

5. That Rule 2(1)(h) of the Companies (Significant Beneficial Owners) Rules, 2018 of the Act defines

“significant beneficial owner” in relation to a reporting company means an individual referred to in sub-section (1) of Section 90, who acting alone or together, or through one or more persons or trust, possesses one or more of the following rights or entitlements in such reporting company, namely: (i) holds indirectly, or together with any direct holdings, not less than ten percent, of the shares; (ii) holds indirectly, or together with any direct holdings, not less than ten percent, of the voting rights in the shares; (iii) has right to receive or participate in not less than ten per cent, of the total distributable dividend, or any other distribution, in a financial year through indirect holdings alone, or together with any direct holdings; (iv) has right to exercise, or actually exercises, significant influence or control, in any manner other than through direct-holdings alone:

Explanation I – For the purpose of this clause, if an individual does not hold any right or entitlement indirectly under sub-clauses (i), (ii) or (iii), he shall not be considered to be a significant beneficial owner.

Explanation II – For the purpose of this clause, an individual shall be considered to hold a right or entitlement directly in the reporting company, if he satisfies any of the following criteria, namely.’

(i) the shares in the reporting company representing such right or entitlement are held in the name of the individual;

(ii) the individual holds or acquires a beneficial interest in the share of the reporting company under sub-section (2) of section 89, and has made a declaration in this regard to the reporting company.

Explanation III – For the purpose of this clause, an individual shall be considered to hold a right or entitlement indirectly in the reporting company, if he satisfies any of the following criteria, in respect of a member of the reporting company, namely: – (i) where the member of the reporting company is a body corporate (whether incorporated or registered in India or abroad), other than a limited liability partnership, and the individual, (a) holds majority stake in that member; or (b) holds majority stake in the ultimate holding company (whether incorporated or registered in India or abroad) of that member.

6. That as per Reserve Bank of India vide Master Direction DBR.AML.BC.No.81/14.01.001/2015-16 – Know Your Customer (KYC) Direction, 25.02.2016 which states:-

“3 (iv). Beneficial Owner (BO)

a. Where the customer is a company, the beneficial owner is the natural person(s), who, whether acting alone or together, or through one or more juridical person, has/have a controlling ownership interest or who exercise control through other means.

Explanation- For the purpose of this sub-clause-

1. “Controlling ownership interest” means ownership of/entitlement to more than 25 per cent of the shares or capital or profits of the company.

2 .”Control” shall include the right to appoint majority of the directors or to control the management or policy decisions including by virtue of their shareholding or management rights or shareholders agreements or voting agreements.

b. Where the customer is a partnership firm, the beneficial owner is the natural person(s), who, whether acting alone or together, or through one or more juridical person, has/have ownership of/entitlement to more than 15 per cent of capital or profits of the partnership.

c. Where the customer is an unincorporated association or body of individuals, the beneficial owner is the natural person(s), who, whether acting alone or together, or through one or more juridical person, has/have ownership of/entitlement to more than 15 per cent of the property or capital or profits of the unincorporated association or body of individuals.

Explanation: Term ‘body of individuals’ includes societies. Where no natural person is identified under (a), (b) or (c) above, the beneficial owner is the relevant natural person who holds the position of senior managing official.

d. Where the customer is a trust, the identification of beneficial owner(s) shall include identification of the author of the trust, the trustee, the beneficiaries with 15% or more interest in the trust and any other natural person exercising ultimate effective control over the trust through a chain of control or ownership.

Part IV-Identification of Beneficial Owner

34. For opening an account of a Legal Person who is not a natural person, the beneficial owner(s) shall be identified and all reasonable steps in terms of Rule 9(3) of the Rules to verify his/her identity shall be undertaken keeping in view the following:

a. Where the customer or the owner of the controlling interest is a company listed on a stock exchange, or is a subsidiary of such a company, it is not necessary to identify and verify the identity of any shareholder or beneficial owner of such companies.

b. In cases of trust/nominee or fiduciary accounts whether the customer is acting on behalf of another person as trustee/nominee or any other intermediary is determined. In such cases, satisfactory evidence of the identity of the intermediaries and of the persons on whose behalf they are acting, as also details of the nature of the trust or other arrangements in place shall be qbtained.

7. The ‘reporting company’ being a wholly owned subsidiary of Khvatec Co., Ltd, Korea and on examination of the filings made by ‘the reporting company’ in MCA- 21 Registry there is no e-form BEN-2 that has been filed by the ‘reporting company’ and it was reason to believe that the ‘reporting company’ ought to have made compliance with Section 90 of the Companies Act, 2013 i.e. declaration of beneficial ownership by filing e-form BEN-2 of the ‘reporting company’ till the time of issuance of notice under Section 206(1) of the Act vide letter No. 03/05/SBO/UP/2024/Khvatec/7026 to 7028 dated 13.02.2024.

The reporting company submitted its first reply vide letter dated 23.02.2024 duly signed by its Company Secretary i.e., Ms. Sandhya Pandey, wherein the details of the shareholding in the reporting company, details of other companies in which the directors of Khvatec Co. Ltd. are either shareholders or directors was provided. Further, ‘the reporting company’ also submitted that the Company has taken various steps to identify the Significant Beneficial Owner (SBO) in the Company, if any, including the issuance of notice in form BEN-4 to the shareholder of the Company, in past.

The response submitted by the Company states that the reporting company had issued notice in form BEN-4 dated 13.09.2019 to Khvatec Co. Ltd. for the identification of Significant Beneficial Owners under the provisions of Section 90 read with the Companies (Significant Beneficial Owners) Rules, 2018.

Further, ‘the reporting company’ stated that they are subsidiary of Khvatec Co. Ltd., Korea with two shareholders i.e. Khvatec Co. Ltd., Korea [99.99% shares] and Jang Kuk Nam (Nominee of Khvatec Co. Ltd.) [0.01% shares] and Khvatec Co. Ltd., Korea is listed on the Korean Stock Exchange.

8. On examination of the submission(s) made by the reporting Company, show cause notice (SCN) was issued to the ‘reporting company’, its Directors and KMP u/s 90 of the Companies Act, 2013 read with Companies (Significant Beneficial Owners) Rules, 2018, vide letter no. 03/05/SBO/UP/2024/Khvatec/566 to 569 dated 25.04.2024 and a date of hearing was fixed for 21.05.2024.

9. The Company submitted its reply vide letter dated 14.05.2024 duly signed by its Company Secretary, Ms. Sandhya Pandey, wherein the details of the shareholders of the Company from 31st March 2020 to 31st March 2024 and as on 14th May 2024, list of shareholders of Khvatec Co. Ltd. i.e. holding company of reporting company from 2019 to 2024 and as on 14th May 2024 were submitted.

10. Sandhya Pandey, Company Secretary of the reporting company appeared on behalf of the Company on the date of hearing i.e. 21.05.2024. The representative of the reporting Company explained the efforts taken by the Company to identify the Significant Beneficial Ownership which includes sending of the notice in form BEN-4 to any person falling under the criteria as per the requirements of Section 90(5) of the Companies Act, 2013 read with Rule 2A of the Companies (Significant Beneficial Owners) Rules, 2018, who holds not less than 10% of its shares or voting rights or right to participate in dividend. Accordingly, a notice in form BEN-4 dated 13.09.2019 was issued to the holding Company. In response to the form BEN-4 notice issued to the holding company of the ‘reporting company’ i.e. Khvatec Co. Ltd., the ‘reporting company’ received BEN-1 declaration dated 19.09.2019 from the holding Company confirming its non-applicability.

11. The documents/ information submitted by the reporting company were further reexamined and an email was sent to the ‘reporting company’, Directors and KMP of the Company dated 30.05.2024 wherein additional documents/ information were sought from the reporting company inter-alia including the copy of the Ultimate Beneficial Ownership (UBO) declaration as per the Master Direction – Know Your Customer (KYC) Direction, 2016 of RBI given by the Company to the Banks, copies of the bank account details in the respective bank accounts till date, list of employees of the ‘reporting company’, detail of the notice in the form of form BEN-4 issued along with the proof of service etc.

12. The ‘reporting company’ submitted its reply vide letter dated 11.06.2024 duly signed by Mr. Hyun Sik Yoon, Director of the Company and Ms. Sandhya Pandey, Company Secretary of the Company, wherein, the details of the UBO declaration to Citi Bank, N.A., list of employees of the Company from the financial year 2020 — 21 till 31St May 2024, organizational structure dated 31st May 2024, employment agreement of Mr. Nam Jang Kuk and Mr. Yoon Hyun Sik, copy of notice issued in the form of Form BEN-4 to the holding Company dated 13.09.2019 along with the proof of service, copy of BEN-1 declaration confirming the non-applicability of the SBO declaration on the Company dated 19.09.2019 duly signed by Moon Jinwon, authorized signatory, Strategic Planning Team, Khvatec Co. Ltd., list of its directors as on 31st March 2019 to 31st March, 2024 and the details of shareholders along with its shareholding structure from 31st March 2020 to 31st March 2024 were submitted.

The copy of BEN-3 i.e. register maintained by the Company for SBO, wherein non-applicability of the BEN-1 has been noted was also submitted.

13. Mr. Suresh Pandey, Practicing Company Secretary (Membership Number: F7776, COP No. 8529) appeared on behalf of the ‘reporting company’ on the date of hearing i.e. on 12.06.2024. The authorised representative of the reporting company explained the Compliance of Section 90(5) of the Companies Act, 2013 w.r.t. issuance of notice to the holding Company in the form of BEN-4 w.r.t. seeking the information of the Significant Beneficial Ownership details. The authorised representative also confirmed that the `reporting company’ has also made the Compliance of Section 89 of the Companies At, 2013 read with rules made thereunder.

14. The ‘reporting company’ submitted the list of shareholders along with their shareholding structure for the year ended March 31, 2020, March 31, 2021, March 31, 2022, March 31, 2023 and March 31, 2024 wherein the holding of Mr. Nam Kwang Hee is 14.06%, 13.90%, 13.90%, 13.90% and 13.90%, respectively. Although, Mr. Nam Kwang Hee is holding more than 10% shares in the holding Company, the Company being a listed entity in South Korea with more than 70% holding with the general public, the decisions and control is not in the hands of Mr. Nam Kwang Hee. The Reporting Company also, vide its reply dated 11.06.2024, confirmed that no individual associated with Khvatec Co. Ltd., Korea currently exercises control or significant influence over the ‘reporting company’ and all decisions taken by the Board of Khvatec India Private Limited are made independently, in accordance with the governing laws and regulations, and are aimed at promoting the best interests of Khvatec India and its stakeholders and the control is with the Directors of the ‘reporting company’ present in India as per their respective employment agreements.

Furthermore, no individual holds significant influence and Control that would qualify them as an SBO under the aforementioned provision.

The Reporting Company has submitted the details of its four bank accounts maintained with Citibank N.A., ICICI Bank Ltd, Industrial Bank of Korea and State Bank of India all maintained in India. As per the information submitted by the ‘reporting Company’, only three (3) Bank Accounts are operative and the account with the State Bank of India is closed as per the SBI letter dated 12.07.2021.

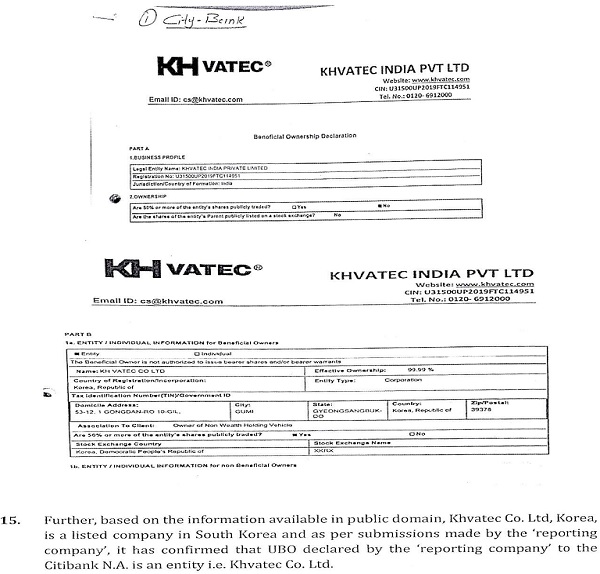

The ‘reporting company’ has also submitted the copy of UBO declaration of Citibank N.A., wherein, the name of the UBO is an entity i.e. Khvatec Co. Ltd, Korea. Further, as per Direction No. 34(a) of the Reserve Bank of India Master Direction No. DBR.AML.BC.No.81/14.01.001/2015-16 dated 25.02.2016 where the customer or the owner of the controlling interest is a company listed on a stock exchange, or is a subsidiary of such a company, it is not necessary to identify and verify the identity of any shareholder or beneficial owner of such companies.

Further, the company has also submitted documents w.r.t. to approaching the other banks for seeking copies of the UBO declaration submitted at the time of account opening. The response is awaited from the other three banks.

The extract of the UBO declaration received from Citibank N.A. is as follows:

–

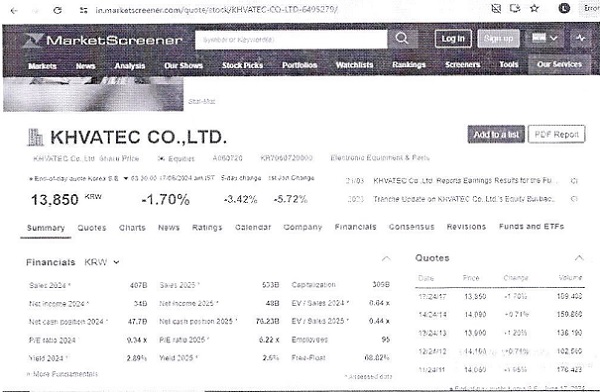

Reference: Details available on the website market scanner.

16. On examination of the documents and information submitted by the ‘reporting company’, it was observed that the ‘reporting company’ has taken the necessary steps to identify the SBO in relation to the Company and issued notice in form BEN-4 dated 13.09.2019 to the holding company. In response to the form BEN-4 issued to the Holding Company, the ‘reporting company’ has received duly signed declaration in BEN-1, wherein its non-applicability has been confirmed. Further, the holding company being the listed Korean entity, was declared as the UBO by the reporting company under direction 34(a) as per the Master Circular Number as per Reserve Bank of India vide Master Direction DBR.AMLBC.No.81/14.01.001/2015-16 dated 25.02.2016.

17. Adjudication of Penalty:

The submissions of the company are taken on record along with the documentary information and evidences and accordingly the provisions of Section 90 read with rules made thereunder of the Act are not attracted in light of the above facts and submissions.

(Seema Rath)

Registrar of Companies & Adjudicating Officer

Uttar Pradesh, Kanpur

No. 03/05/SBO/UP/2024/Khvatec 1919 to 1922

Dated: 28-06-2024