“To enrich quality of life in the society we operate in we need to give back to the society manifolds than what we get from it”. – JRD TATA

“Resources businesses must contribute to sustainable development if we are to continue to have access to resources.” – Cynthia Carroll

Introduction

The Corporate Social Responsibility (CSR) is a concept wherein enormous Companies is required to spend a small portion of their Profit (i.e. 2% of Profit) towards CSR Activities which includes promoting health care, promoting education, rural development projects, ensuring environmental sustainability and conservation of natural resources etc. These Companies not only consider their profitability and growth, but also the interest of society and the environment by taking the responsibility for the impact of their activities on stakeholders, environment, consumers, employees, communities, and all other members in the public sphere. The basic premise is that when the corporates get bigger in size, apart from the economic responsibility of earning profits, there are many other responsibilities attached to them which are more of non- financial /social nature.

CSR is not a Philanthropic Activity. Philanthropy means an act of donating money, goods, time or effort to support a charitable cause in regard to a defined objective. It is the active effort to promote human welfare. CSR on the other hand is about how a company aligns their values to social causes by including and collaborating with their investors, suppliers, employees, regulators and the society as a whole.

This write-up covers all the amendments till 30th June, 2021.

Page Contents

- 1. Evolution of CSR in India

- 2. Applicability [Section 135(1)]

- 3.Non-Applicability of CSR Provisions [Rule 3(2)]

- 4. Definition under CSR Rules [Rule 2]

- 5. CSR Committee [Section 135(1) and Rule 5(1)]

- 6. Functions of the CSR Committee [Section 135(3) and Rule 5(2)]

- 7. Functions of CSR Committee can be Discharged by Board [Section 135(9)]

- 8. CSR Expenditure [Section 135(5), Rule 4 and Rule 7(1)]

- 9. Surplus out of CSR Activities [Rule 7(2)]

- 10. Set-off of Excess Amount of CSR Expenditure [Rule 7(3)]

- 11. CSR Expenditure in Capital Assets [Rule 7(4)]

- 12. Transfer of Unspent CSR Amount (Other Than Ongoing Project) to a Fund [Section 135(5) and Rule 10]

- 13. Transfer of Unspent CSR Amount of Ongoing Projects [Section 135(6), Rule 4(6) and Rule 10]

- 14. CSR Implementation and CSR Registration Number from MCA

- 15. Registration under Section 12A and 80G of the Income Tax Act

- 16. CFO Certification [Rule 4(5)]

- 17. Annual Report on CSR and Website Disclosures [Rule 8 and Rule 9]

- 18. Impact Assessment of CSR Projects [Rule 8]

- 19. Reporting under CARO 2020 relevant to CSR

- 20. CSR on COVID-19

- 21. CSR Activities Benefiting Employees

- 22. Deduction of CSR Expenditure under Income Tax Act

- 23. Disclosure in Financial Statements of CSR Expenditure

1. Evolution of CSR in India

The concept of CSR is not new to the corporates in India. The concept can be traced back to times immemorial, our Vedas say – man can live individually but can survive only collectively.

Before the enactment of the Companies Act, 2013, various other laws in India addressed the basic responsibilities of corporate towards its employers and environment through labour laws and environment protection laws.

The Ministry of Corporate Affairs (“MCA”) notified Section 135 and Schedule VII of the Companies Act 2013 as well as the Companies (CSR Policy) Rules, 2014. India is probably the only country to have a law on CSR.

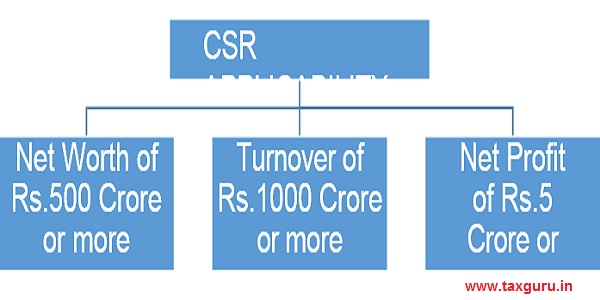

2. Applicability [Section 135(1)]

The CSR provisions are applicable to those Companies which fulfills any of the following criteria’s during the immediately preceding financial year :

- Companies having net worth of rupees five hundred Crore or more, or

- Companies having turnover of rupees one thousand Crore or more or

- Companies having a net profit of rupees five Crore or

- Net Worth : “Net Worth” means the aggregate value of the paid-up share capital (equity and preference) and all reserves created out of the profits, securities premium account and debit or credit balance of profit and loss account, after deducting the aggregate value of the accumulated losses, deferred expenditure and miscellaneous expenditure not written off, as per the audited balance sheet, but does not include reserves created out of revaluation of assets, write-back of depreciation and amalgamation. [Section 2(57)]

“Net Worth = (Paid Up Share Capital + All Reserves Created Out of Profits + Securities Premium Account + debit or credit balance of P&L A/c) – (Accumulated Losses + Deferred Expenditure and Miscellaneous Expenditure not Written Off)”.

Note: It is to be noted that the words used in Section 2(57) are “all reserves created out of the profits” and not “free reserve”. It does not include reserves created out of revaluation of assets and amalgamation.

- Turnover : “Turnover” means the gross amount of revenue* recognized in the profit and loss account from the sale, supply, or distribution of goods or on account of services rendered, or both, by a company during a financial year. [Section 2(91)].

Note: For the purpose of Companies Act, 2013, the gross amount of revenue means amounts inclusive of all taxes.

- Net Profit: “Net profit” means the net profit of a company as per its financial statement prepared in accordance with the applicable provisions of the Act, but shall not include the following, namely: –

(a) any profit arising from any overseas branch or branches of the company, whether operated as a separate company or otherwise; and

(b) any dividend received from other companies in India, which are covered under and complying with the provisions of section 135 of the Act: Provided that in case of a foreign company covered under these rules, net profit means the net profit of such company as per profit and loss account prepared in terms of clause (a) of sub-section (1) of section 381, read with section 198 of the Act;

“Net Profit” shall be calculated in accordance with the provisions of Section 198.

The net worth, turnover or net profit of a foreign Company of the Act shall be computed in accordance with the balance sheet and Profit and loss account of such company prepared in line with the provisions of clause (a) of sub-section (1) of section 381 and section 198 of the Act.

Calculation of Net Profit as per Section 198:

| Sl. No. | Particulars | Amount in Rs. |

| (a) | Profit before tax as per statement of Profit & Loss | — |

| (b) | Add: Amount specified under Section 198(2), 198(5)(b), 198(5)(c) & 198(5)(d) of the Act | — |

| (c) | Less; Sums not allowed to be deducted as per Section

198(3) of the Act |

— |

| (d) | Net Profit under Section 198 [(d)=(a)+(b)-(c)] | — |

| (e) | Less:

(i.) Dividend from Companies complying CSR provisions (ii.) Profit from overseas branches of the Company |

— — |

| (f) | Net Profit for CSR [(f)=(d)-(e)] | — |

3.Non-Applicability of CSR Provisions [Rule 3(2)]

As per sub Sections (1) and (5) of Section 135 of the Companies Act, 2013, every Company is required to constitute CSR Committee and spend CSR amount if such Company satisfies any of the criteria’s as specified above during the immediately preceding financial year.

However, prior to Companies (Amendment) Act, 2017, the applicability for constitution of CSR Committee was required to be ascertained on the basis of net-worth, turnover and net profits during any of the preceding three financial years.

As per Rule 3(2) of the CSR Rules, 2014, every company which ceases to be a company covered under section 135(1) of the Act for three consecutive financial years shall not be required to –

(a) constitute a CSR Committee; and

(b) comply with the provisions contained in sub-section (2) to (6) of the said Section*,

till such time it meets the criteria specified in Section 135(1).

*Note: The MCA by the Companies (CSR) Amendment Rules, 2021 effective from 22.01.2021, has substituted the Rule 3(2)(b) from the words “sub Section (2) to (5)” to words “sub Section (2) to (6)”.

It is evident from the above amendment that MCA wants to keep Rule 3(2) for non-applicability of CSR provisions.

The Company is required to ascertain applicability considering the net-worth, turnover and net profits during the immediately preceding financial year pursuant to the amendment made in Section 135 (1) by way of Companies (Amendment) Act, 2017, however, for non-applicability of CSR provisions, the Company should be ceased to be a company covered under Section 135 (1) for three consecutive financial years.

Thus, considering the above provisions and the intention of the law maker and as per the author’s view, it can be concluded that if a Company does not satisfy any of the criteria’s of Section 135 (1) of the said Act for a consecutive period of three financial years, then such Company shall not be required to comply with the CSR provisions.

For example: A Company have following net profit as per Section 198:

Financial Year 2018-19 – Rs.4.00 Crore

Financial Year 2019-20 – Rs.6.00 Crore

Financial Year 2020-21 – Rs.4.00 Crore

Does Company require to spend in FY 2021-22?

As per Rule 3(2), the Company has to spend 2% of average net profit for next 3 financial years once the CSR provisions applicable. In this case Company has to spend 2% of average net profit of FY 2018-19, FY 2019-20 and 2020-21.

4. Definition under CSR Rules [Rule 2]

(a) “Administrative overheads” means the expenses incurred by the company for ‘general management and administration’ of Corporate Social Responsibility functions in the company but shall not include the expenses directly incurred for the designing, implementation, monitoring, and evaluation of a particular Corporate Social Responsibility project or

(b) “Corporate Social Responsibility (CSR)” means the activities undertaken by a Company in pursuance of its statutory obligation laid down in section 135 of the Act in accordance with the provisions contained in these rules, but shall not include the following, namely: –

(i.) Activities undertaken in pursuance of normal course of business of the Company:

Provided that any company engaged in research and development activity of new vaccine, drugs and medical devices in their normal course of business may undertake research and development activity of new vaccine, drugs and medical devices related to COVID-19 for financial years 2020-21, 2021-22, 2022-23 subject to the conditions that-

1. such research and development activities shall be carried out in collaboration with any of the institutes or organizations mentioned in item (ix) of Schedule VII to the Act; and

2. details of such activity shall be disclosed separately in the Annual report on CSR included in the Board’s

In general, “normal course of business” will include activities entered into in the normal course of business pursuant to or for promoting or in furtherance of the Company’s business objectives, as per charter documents of the Company. (Re: ICSI-GN-RPT).

(ii.) Any activity undertaken by the company outside India except for training of Indian sports personnel representing any State or Union territory at national level or India at international level.

(iii.) Contribution of any amount directly or indirectly to any political party under section 182 of the Act.

(iv.) Activities benefitting employees of the company as defined in clause (k) of Section 2 of the Code on Wages, 2019.

“Employee” means, any person (other than an apprentice engaged under the Apprentices Act, 1961), employed on wages by an establishment to do any skilled, semi-skilled or unskilled, manual, operational, supervisory, managerial, administrative, technical or clerical work for hire or reward, whether the terms of employment be express or implied, and also includes a person declared to be an employee by the appropriate Government, but does not include any member of the Armed Forces of the Union.

(v.) activities supported by the companies on sponsorship basis for deriving marketing benefits for its products or services.

(vi.) activities carried out for fulfilment of any other statutory obligations under any law in force in India.

(c) “CSR Policy” means a statement containing the approach and direction given by the board of a company, taking into account the recommendations of its CSR Committee, and includes guiding principles for selection, implementation and monitoring of activities as well as formulation of the annual action

(d) “Ongoing Project” means a multi-year project undertaken by a Company in fulfilment of its CSR obligation having timelines not exceeding three years excluding the financial year in which it was commenced, and shall include such project that was initially not approved as a multi-year project but whose duration has been extended beyond one year by the board based on reasonable

5. CSR Committee [Section 135(1) and Rule 5(1)]

In accordance with the provisions of Section 135 of the said Act, it is required to constitute CSR Committee with at least three directors as its members and out of which at least one should be an Independent Director.

However, as per CSR Rules, unlisted public companies and private companies which are not required to appoint an Independent Director shall have its CSR Committee without such director. Further, a private company having only two directors on its Board shall constitute its CSR Committee with two such directors.

The CSR Committee of a foreign company shall comprise of at least two persons wherein one or more persons should be resident in India and the other person nominated by the foreign company. The Board’s report shall disclose the composition of the CSR Committee.

6. Functions of the CSR Committee [Section 135(3) and Rule 5(2)]

The CSR Committee shall: –

(a) formulate and recommend to the Board, a CSR Policy which shall indicate the activities to be undertaken by the company in areas or subject specified in Schedule VII;

(b) recommend the amount of expenditure to be incurred on the activities to be undertaken by the company as specified in Schedule VII; and

(c) monitor the Corporate Social Responsibility Policy of the company from time to

As per the new definition, “CSR Policy” means a statement containing the approach and direction given by the board of a company, taking into account the recommendations of its CSR Committee, and includes guiding principles for selection, implementation and monitoring of activities as well as formulation of the annual action plan.

The Annual Action Plan shall include the following, namely: –

(a) the list of CSR projects or programmes which are approved and to be undertaken in areas or subjects specified in Schedule VII of the Act;

(b) the manner of execution of such projects or programmes as specified in point no. (a);

(c) the modalities of utilization of funds and implementation schedules for the projects or programmes;

(d) monitoring and reporting mechanism for the projects or programmes; and

(e) details of need and impact assessment, if any, for the projects undertaken by the company:

The Board may alter such plan at any time during the financial year, as per the recommendation of its CSR Committee, based on the reasonable justification to that effect.

The new definition requires the policy to have approach and direction of Board along with guiding principles for selection, implementation and monitoring of the CSR activities undertaken by the companies. Apart from this, the Policy should also contain annual action plan.

This change in the definition in CSR policy may require the companies to reconsider their existing CSR Policy at the earliest so that the same may be placed in the ensuing CSR and Board meeting.

7. Functions of CSR Committee can be Discharged by Board [Section 135(9)]

As per the Companies (Amendment) Act, 2020, effective from 22nd January, 2021, the constitution of CSR Committee is not required, where the amount to be spent by a Company in a financial year on CSR Activities is less than Rs.50.00 Lakh. The functions of CSR Committee can be discharged by the Board of Directors of the Company.

In case of existing Companies, the Board can dissolve the CSR Committee and in case of new applicability of CSR provisions and the amount to be spent by a Company arriving below Rs.50.00 Lakh, the functions of CSR Committee can be discharged by the Board of Directors of the Company.

8. CSR Expenditure [Section 135(5), Rule 4 and Rule 7(1)]

The Board of every company shall ensure that the company spends, in every financial year, at least two per cent of the average net profits of the company made during the three immediately preceding financial years or where the company has not completed the period of three financial years since its incorporation, during such immediately preceding financial years, in pursuance of its Corporate Social Responsibility Policy.

The Company may also collaborate with other companies for undertaking projects or programmes or CSR activities in such a manner that the CSR committees of respective companies are in a position to report separately on such projects or programmes in accordance with these rules.

The administrative overheads shall not exceed five percent of total CSR expenditure of the company for the financial year.

The definition of administrative overheads covers only expenses incurred by the company for ‘general management and administration’ of CSR project or Programme.

From the above, we may conclude that there is no upper cap on the expenses that can be incurred for monitoring, evaluation and designing of a CSR project or Programme. It should be noted that these expenses shall not be consider for calculating overall CSR expenditure.

The Company may engage international organizations for designing, monitoring and evaluation of the CSR projects or programmes as per its CSR policy as well as for capacity building of their own personnel for CSR.

The company shall give preference to the local area and areas around it where it operates, for spending the amount earmarked for Corporate Social Responsibility activities.

It should be noted that while calculating average net profit of the preceding financial year(s) the company shall consider its loses also.

For example: A Company has following net profit/losses:

| SI. No. | Financial Year | Profit | Loss |

| 1. | 2018-2019 | Rs.6.00 Crore | — |

| 2. | 2019-2020 | — | Rs.4.00 Crore |

| 3. | 2020-2021 | Rs.3.00 Crore | |

| Average Net Profit | 6+3-4

3 |

||

| = Rs.1.60 Crore | |||

9. Surplus out of CSR Activities [Rule 7(2)]

Any surplus arising out of the CSR activities shall not form part of the business profit of a company and shall be: –

- ploughed back into the same project or

- transferred to the Unspent CSR Account and spent in pursuance of CSR policy and annual action plan of the company or

- transfer such surplus amount to a Fund specified in Schedule VII, within a period of six months of the expiry of the financial year.

10. Set-off of Excess Amount of CSR Expenditure [Rule 7(3)]

Where a Company spends an amount in excess of requirement provided under section 135(5), such excess amount may be set off against the requirement of CSR expenditure up to immediate succeeding three financial years’ subject to the conditions that –

(i.) the excess amount available for set off shall not include any amount arising out of the CSR activities; and

(ii.) Board resolution shall be passed by the Company for approving the utilisation of excess amount spend.

Earlier there was no provision of set off and carry forward in the Act.

It is to be noted that set-off of excess amount of CSR expenditure is applicable from financial year 2020-21 i.e. if a Company spends more than 2% of average net profit in FY 2020-21, the Company may set-off such excess amount against the requirement of CSR expenditure up to FY 2023-24 provided that such amount shall not be arise out of CSR Activities and the Board of the Company has passed a resolution approving the set-off of such excess amount.

11. CSR Expenditure in Capital Assets [Rule 7(4)]

The CSR amount may be spent by a company for creation or acquisition of a capital asset, which shall be held by –

(a) a company established under section 8 of the Act, or a Registered Public Trust or Registered Society, having charitable objects and CSR Registration Number; or

(b) beneficiaries of the said CSR project, in the form of self-help groups, collectives, entities; or

(c) a public authority:

Provided that any capital asset created by a company prior to 22nd January, 2021 shall within a period of 180 days from 22nd January, 2021, comply with the requirement of Rule 7(4) as mentioned above, which may be extended by a further period of not more than 90 days with the approval of the Board based on reasonable justification.

The Capital assets ‘created or acquired’ by the company prior to 22nd January, 2021, shall fall under two categories –

- Capital assets ‘created or acquired’ out of the profits of the company (e.g. land, building, etc.) that are incidentally used for CSR

- Capital assets ‘created or acquired’ out of the CSR funds allocated for a financial

The Rule 7(4) requires a transfer of only those capital assets that are ‘created or acquired’ out of CSR funds allocated for a financial year. These capital assets cannot be held directly by the company. On the other hand, capital assets that are created out of profits and used incidentally for CSR activities can be held by the company, and need not be transferred.

12. Transfer of Unspent CSR Amount (Other Than Ongoing Project) to a Fund [Section 135(5) and Rule 10]

If the Company fails to spend 2% of the average net profits, the Board shall, in its report made under Section 134, specify the reasons for not spending the amount and, unless the unspent amount relates to any ongoing project, transfer such unspent amount to a Fund specified in Schedule VII, within a period of six months of the expiry of the financial year.

Until a fund is specified in Schedule VII for above purposes under Section 135(5), the unspent CSR amount, if any, shall be transferred by the company to any fund included in schedule VII of the Act I.e. Prime Minister’s National Relief Fund (“PMNRF”), clean Ganga Fund etc.

Earlier, Companies have to only explain the reasons in their Board’s Report as to why they have not spent the amount towards its CSR activities. However, with the amendment brought in by the Companies (Amendment) Act, 2019 effective from 22.01.2021, the Companies have to explain the reasons and transfer the unspent amount (other than the amount related to on- going project) to fund specified in schedule VII.

Now it becomes mandatory for the Companies to spend the CSR expenditure either itself or through implementing agencies i.e. Section 8 Company/Trust/Society except the ones which are being utilized for ongoing projects.

The above amendment is effective from 22.01.2021 and applicable from financial year 2020-21. If the Company has not spent CSR expenditure for FY 2020-21 then Company have to transfer such CSR amount to a fund specified in Schedule VII before 30th September, 2021

13. Transfer of Unspent CSR Amount of Ongoing Projects [Section 135(6), Rule 4(6) and Rule 10]

In accordance with the definition of Ongoing project which states that CSR expenditure on Ongoing Project shall be consider only for such projects which has a timeline for completion not exceeding 3 financial years excluding the year in which it commenced. Also, projects which were initially commenced with a timeline of a year but in due course has been extended shall also be considered as an eligible Ongoing Project. However, it is still not mentioned in the provisions of such projects which have timeline of more than 4 years.

The Ongoing Project cannot exceed the 4 years (including the financial year in which it was commenced). However, the Company can undertake more than one ongoing project during the financial year.

Commencement of Ongoing Project: The meaning of commencement of Ongoing Project is not clear as per the definition of Ongoing Project, whether Company have to consider disbursement of CSR expenditure or actual commencement of project. The actual meaning of “on-going” will be clear only once the MCA clarify the same.

Transfer of Unspent CSR Amount: Section 135(6) has been newly inserted and pursuant to which any amount remaining unspent pursuant to any ongoing project, fulfilling such conditions as may be prescribed, undertaken by a company in pursuance of its CSR Policy shall be transferred by the company within a period of thirty days from the end of the financial year to a special account to be opened by the company in that behalf for that financial year in any scheduled bank to be called the Unspent Corporate Social Responsibility Account (unspent CSR account), and such amount shall be spent by the company in pursuance of its obligation towards the CSR Policy within a period of three financial years from the date of such transfer, failing which, the company shall transfer the same to a Fund specified in Schedule VII, within a period of thirty days from the date of completion of the third financial year.

The Board of a Company shall monitor the implementation of the project with reference to the approved timelines and year-wise allocation and shall be competent to make modifications, if any, for smooth implementation of the project within the overall permissible time period.

The amount of unspent CSR account shall be spent by the company towards CSR obligation pursuant to CSR Policy within a period of three financial years from the date of such transfer. It is not necessary that such amount shall be spent in the same ongoing project and it can be spent in any project/programme in CSR Policy.

For Example:

Company A Ltd. has to spend Rs.4.00 Crores for FY 2021-22. Now the Board has approved to spend such amount for building up a Hospital (Ongoing Project) and allocated Rs.1.00 crore for each year till FY 2024-25. At the end of FY 2021-22, the Company has unspent CSR amount of of Rs.3.00 Crore and Company has to transfer such amount to Unspent CSR Account within 30 days from the end of FY 2021-22. In the FY 2024-25 the Company has completed the project in Rs.3.00 Crores. Now, the Company has two options in this case:

(a) The Company can transfer such Rs.1.00 Crore as unspent CSR amount in a Fund specified in Schedule VII within 6 month from the end of FY 2024-2025.

OR

(b) The Company can spend such Rs.1.00 Crore in another project/programme pursuant to CSR

Until a fund is specified in Schedule VII for above purposes under Section 135(6), the unspent CSR amount, if any, shall be transferred by the company to any fund included in schedule VII of the Act I.e. Prime Minister’s National Relief Fund (“PMNRF”), clean Ganga Fund etc.

Unspent CSR Account: As per the newly inserted Section 135(6), it is unclear whether the company is required to open Unspent CSR Account project wise in each financial year or whether there will be a single account managed for all on-going projects, however, as per the author’s view, it depends on the feasibility of the Company and the number of ongoing projects of the Company, i.e. a small company having knowledge that such company will operate only 1 or 2 projects for its CSR Activities then such company will prefer to open one Bank Account for all such ongoing project(s) and will keep that account open for coming financial year(s), on the other hand , a big company having knowledge that there will be required to operate multiple projects for CSR activities then such company will prefer to open a single Bank Account in that financial year for all ongoing project(s) and will close that after completion of such projects.

Therefore, it can be concluded that opening of separate Bank Account and keeping it open for successive financial years only depends on the feasibility and discretion of the Company because the Act does not clarify about operating and closing of “Unspent CSR Account”.

14. CSR Implementation and CSR Registration Number from MCA

The Board shall ensure that the CSR activities are undertaken by the company itself or through: –

(a) a company established under Section 8 of the Act, or a registered public trust or a registered society, registered under section 12A and 80G of the Income Tax Act, 1961, established by the company, either singly or along with any other company, or

(b) a company established under section 8 of the Act or a registered trust or a registered society, established by the Central Government or State Government; or

(c) any entity established under an Act of Parliament or a State legislature; or

(d) a company established under section 8 of the Act, or a registered public trust or a registered society, registered under section 12A and 80G of the Income Tax Act, 1961, and having an established track record of at least three years in undertaking similar

Every Section 8 Company/Trust/Society who intends to undertake any CSR activity, shall register itself with the MCA by filing the Form CSR-1 electronically with the Registrar, with effect from the 1st April 2021 to obtain a unique CSR Registration Number.

The above provisions shall not affect the CSR projects or programmes approved prior to the 1st April 2021.

Any amount remaining unspent with the Section 8 Company/trust/NGO should be either transferred to the Unspent CSR Account or transferred to the fund as per subsection (5) and (6) of Section 135.

15. Registration under Section 12A and 80G of the Income Tax Act

The registered Section 8 Company/Trust/Society has to register itself under Section 12A and 80G for undertaking CSR activity. Both applications for registration under Section 12A and 80G can be applied together or it can also be applied separately. If some organization is willing to apply both applications separately, then application for registration u/s 12A will be pursued first. Getting 12A registration is must for applying application for registration u/s 80G of Income Tax Act, 1961.

There are few conditions for registration under Section 80G which are as follows:

- The NGO should not have any Income which is not exempted, such as business income. If the NGO has business income, then it should maintain separate books of account and should not divert donations received for the purpose of such

- The bylaws or objectives of the NGOs should not contain any provision for spending the income or assets of NGO for the purpose other than

- The NGO should not work for the benefit of particular religious’ community or

- The NGO should maintain regular accounts of receipt &

- The NGO should properly register under the societies Regulation Act 1860 or under any law corresponding to that Act or should register under Section 8 of the Companies Act

16. CFO Certification [Rule 4(5)]

The Board of a company shall satisfy itself that the funds so disbursed have been utilized for the purposes and in the manner as approved by it and the Chief Financial Officer or the person responsible for financial management shall certify to the effect.

The CFO shall give Certificate to Board about the utilization of funds so disbursed as approved by Board in their meeting and Board shall take note the same in their meeting.

The certificate can be given quarterly/half yearly/annual basis on the discretion and feasibility of the Company. This Rule makes the CFO more accountable for the entire CSR provision without being part of the CSR committee or the Board of Directors.

17. Annual Report on CSR and Website Disclosures [Rule 8 and Rule 9]

The Board’s Report of a Company shall include an Annual Report on CSR containing particulars specified in annexure I or annexure II, as applicable.

Annexure I is applicable for Financial Year commenced prior to 1st April, 2020 and the Annexure II (new format) is applicable for Financial Year commencing on or after 1st April, 2020.

In case of a foreign company, the balance sheet filed under clause (b) of sub-section (1) of section 381, shall contain an Annual Report on CSR containing particulars specified in Annexure I or Annexure II, as applicable.

The Board of Directors of the Company shall mandatorily disclose the composition of the CSR Committee, and the CSR Policy and Projects approved by the Board on their website, if any, for public access.

This requires the Companies to mandatorily disclose the CSR projects approved by the Board. Till date such disclosure can only be ascertained by Company through their Annual Report after the closure of financial year. This indicates that the Board will have to make a thought-through plan on the recommendation of the CSR Committee as the same will be displayed on the Company’s website.

18. Impact Assessment of CSR Projects [Rule 8]

Every company having average CSR obligation of ten crore rupees or more in pursuance of subsection (5) of Section 135, in the three immediately preceding financial years, shall undertake impact assessment, through an independent agency, of their CSR projects having outlays of one crore rupees or more, and which have been completed not less than one year before undertaking the impact study. The impact assessment reports shall be placed before the Board and shall be annexed to the annual report on CSR.

A Company undertaking impact assessment may book the expenditure towards Corporate Social Responsibility for that financial year, which shall not exceed five percent of the total CSR expenditure for that financial year or fifty lakh rupees, whichever is less.

19. Reporting under CARO 2020 relevant to CSR

The Companies (Auditor’s Report) Order (CARO) 2020 was notified on 25th February 2020 and was to be applicable for the financial years commencing on or after the 1st April, 2019. However, the same was extended by a year by MCA vide Order dated 24th March 2020, to be applicable for the financial years commencing on or after the 1st April, 2020.

The paragraph 3(xx) has been inserted in the CARO which specifically requires reporting on CSR. The same is read as under:

(a) Whether, in respect of other than ongoing projects, the company has transferred unspent amount to a Fund specified in Schedule VII to the Companies Act within a period of six months of the expiry of the financial year in compliance with second proviso to sub-section (5) of Section 135 of the said Act;

(b) Whether any amount remaining unspent under sub-section (5) of Section 135 of the Companies Act, pursuant to any ongoing project, has been transferred to special account in compliance with the provision of subsection (6) of Section 135 of the said Act;

20. CSR on COVID-19

The MCA vide its circular dated 23.03.2020 has clarified that CSR funds can be spent on various activities related to COVID-19 relating to promoting health care including preventive health care and sanitization and disaster management, including relief.

Further, the MCA has clarified on 28.03.2020 that any contribution made to the PM CARES Fund shall qualify as CSR expenditure under the Companies Act 2013 and MCA by notification dated 26.05.2020 has added PM CARES Fund in Schedule VII.

Further, the MCA by general circular dated 13.01.2021 has clarified that spending of CSR funds for carrying out awareness campaigns/programmes or public outreach campaigns on COVID-19 vaccination programme is an eligible CSR activity under specified items of Schedule VII of the Act which are as follows:

(i.) Promoting health care including preventive health care and sanitation.

(ii.) Promoting education, including special education and employment enhancing vocation skills especially among children, women, elderly and the differently abled and livelihood enhancement projects.

(iii.) Disaster management, including relief, rehabilitation and reconstruction activities

Further, the MCA by general circular dated 22.04.2021 has clarified that on spending of CSR funds for setting up makeshift hospitals and temporary COVID care facilities is an eligible CSR activity under Schedule VII of the Act relating to promotion of health care including preventive health care and disaster management.

21. CSR Activities Benefiting Employees

As per Rule 2(1)(d)(iv) of CSR Rules, 2014, activities benefitting employees of the Company as defined in clause (k) of Section 2 of the Code on Wages, 2019 shall not be considered as CSR.

Any CSR activity or Programmes which is exclusively for the benefit of Company’s employees shall not be considered as an eligible CSR expenditure, however, if a Company undertake any CSR activity or programme which is for the benefit of general public (including Company’s employees), then such activities or programmes shall be eligible to be considered as CSR expenditure.

ICAI FAQs on CSR further clarifies that projects or programmes or activities that benefit only the employees of the company and their families shall not be considered as CSR. However, programme or activities that are for the benefit of all, but, which also includes some employees or their families will still be considered as CSR as long as such benefits are not exclusively for the benefit of such employees.

For example, Temporary Covid Care facilities which is exclusively available for Company’s employees shall not considered as an eligible CSR, however, if such facility is also available for the benefit of general public including Company’s employees then such activity shall be eligible to be considered as CSR expenditure.

The MCA vide circular dated 10th April, 2020 issued FAQs for clarification for spending being done by Company for COVID-19 related activities. The FAQs clarified that payment made to employees or contract workers (temporary or permanent) during the time of COVID-19 pandemic is moral or contractual obligation rather CSR expenditure. However, any ex-gratia payment made to any temporary/daily or casual workers shall qualify as CSR if following conditions are fulfilled:

i) Payment is made for the purpose of COVID-19;

ii) Payment is over and above the wages of the worker;

iii) Board declaration for disbursement of such wages have to be obtained; and

iv) Certificate from Auditor for such

22. Deduction of CSR Expenditure under Income Tax Act

The CSR expenditure to be incurred mandatorily under the Co Act is not deductible under section 37(1) of the Income-tax Act, 1961 (IT Act). However, if the expenses are aligned with the other provisions of the Act i.e. Section 35(1)(ii), 35AC etc., tax efficiency can be brought in.

Therefore, inference can be drawn that expense in the nature of CSR may be claimed as deduction under other sections like 35AC of the Income Tax Act, if stipulated conditions are satisfied.

The other contribution made under Section 135 would be eligible for deduction under Section 80G subject to taxpayer satisfying the requisite conditions prescribed for the deduction.

The donation made to the Prime Minister’s Citizen Assistance and Relief in Emergency Situations Fund (PM CARES FUND) would qualify for 100% deduction under Section 80G of the Income Tax Act, 1961. (Effective from 01.04.2020)

23. Disclosure in Financial Statements of CSR Expenditure

The MCA by Notification dated 24th March, 2021 has amended the Schedule III and inserted clauses for disclosing details with respect to CSR by way of a note to the Statement of Profit and Loss in all Divisions of Schedule III which is effective from 1st April, 2021.

The above amendment is applicable for Financial Statement prepared for Financial Year commencing on or after 1st April, 2021.

Where the Company covered under Section 135 of the Companies Act, the following shall be disclosed with regard to CSR activities: –

| (a) | Amount required to be spent by the company during the year | |

| (b) | Amount of expenditure incurred | |

| (c) | Shortfall at the end of the year | |

| (d) | Total of previous years shortfall | |

| (e) | Reason for shortfall | |

| (f) | Nature of CSR activities | |

| (g) | Details of related party transactions, e.g., contribution to a trust controlled by the company in relation to CSR expenditure as per relevant Accounting Standard | |

| (h) | Where a provision is made with respect to a liability incurred by

entering into a contractual obligation, the movements in the provision during the year should be shown separately |

As per the “Technical Guide on Accounting for Expenditure on Corporate Social Responsibility activities issued by ICAI”, the following treatment shall be done for unspent amount of CSR and excess amount of CSR: –

For “ongoing projects”, amount yet to be spent, i.e., transferred to a separate fund account should be shown as current asset under cash and bank balances with description that these funds are earmarked for CSR spend.

For “other than ongoing projects“, unspent amount which is yet to be transferred to a specified fund account, should be shown as current liability with description that this is payable within 6 months of balance sheet date.

Any excess expenditure which Company decides to carry forward as asset, to be shown as current asset under the head loans and advances.

*****

(Written by CS Brajesh Kumar and edited by CS Rahul Das can be contacted at kumarbraj7@gmail.com and rahuldas151292@gmail.com for any kind of query and assistance)

DISCLAIMER: The information given in this document has been made on the basis of the provisions of the Companies Act, 2013 and Rules made thereunder. It is based on the analysis and interpretation of applicable laws as on date. The information in this document is for general informational purposes only and is not a legal advice or a legal opinion. You should seek the advice of legal counsel of your choice before acting upon any of the information in this document. Under no circumstances whatsoever, we are not responsible for any loss, claim, liability, damage(s) resulting from the use, omission or inability to use the information provided in the document.

(Republished with Amendments)

Author Bio