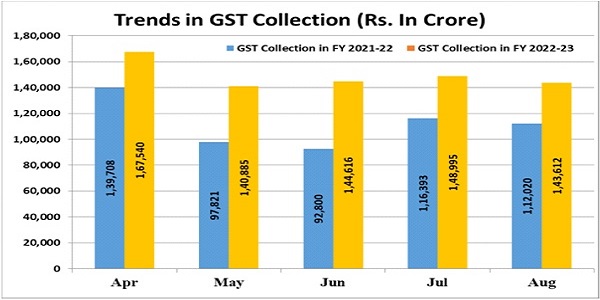

GST Revenue collection for August, 2022

₹1,43,612 crore gross GST revenue collected in the month of August, 2022

The gross GST revenue collected in the month of August, 2022 is ₹1,43,612 crore of which CGST is ₹24,710 crore, SGST is ₹30,951 crore, IGST is ₹77,782 crore (including ₹ 42,067 crore collected on import of goods) and cess is ₹10,168 crore (including ₹ 1,018 crore collected on import of goods).

The government has settled ₹29,524 crore to CGST and ₹25,119 crore to SGST from IGST. The total revenue of Centre and the States in the month of August, 2022 after regular settlement is ₹54,234 crore for CGST and ₹56,070 crore for the SGST.

The revenue collections for the month of August, 2022 are 28% higher than the GST revenue collections in the same month last year of ₹ 1,12,020 crore. During the month, revenue collection from import of goods was 57% higher and the revenue collections from domestic transaction (including import of services) are 19% higher than the revenue collections from these sources during the same month last year.

For six months in a row now, the monthly GST revenue collections have been more than the ₹ 1.4 lakh crore mark.The growth in GST revenue till August, 2022 over the same period last year is 33%, continuing to display very high buoyancy. This is a clear impact of various measures taken by the Council in the past to ensure better compliance. Better reporting coupled with economic recovery has been having positive impact on the GST revenues on a consistent basis. During the month of July, 2022, 7.6 crore e-way bills were generated, which was marginally higher than 7.4 crore in June, 2022 and 19% higher than 6.4 crore in June, 2021.

Source: PIB Press Release dated 01.09.2022

Notification

> Notification No. 17/2022-Central Tax dated 01.08.2022 regarding implementation of e-invoicing.

Vide the said Notification the Central government has made e-invoicing mandatory for taxpayers having aggregate annual turnover of more than ₹10 crore (in any preceding financial year from 2017-18 onwards) with effect from 01.10.2022. At present, e-invoice is compulsory for businesses with an aggregate annual turnover of over ₹ 20 crore.

Circulars

> Circular No. 179/11/2022-GST dated 03.08.2022 regarding GST rates & classification (goods).

Vide the aforesaid circular following clarifications were issued, with reference to levy of GST –

1. Electric vehicles whether or not fitted with a battery pack, attract GST rate of 5%.

The circular clarified that electrically operated vehicle is classifiable under HSN 8703 even if the battery is not fitted to such vehicle at the time of supply and thereby attracting GST at the rate of 5% in terms of entry 242A of Schedule I of Notification No. 1/2017-Central Tax (Rate), Dated: 28/06/2017.

2. Stones otherwise covered in S. No. 123 of Schedule-I (such as Napa stones), which are not mirror polished, are eligible for concessional rate under said entry.

Napa Stones, which are ready to use and polished in ways other than mirror-polished it was clarified that Napa Stone is a variety of dimensional limestone and hence leviable to GST rate at 5% . Being brittle in nature, stones like Napa Stone, even though ready for use, are not subject to extensive polishing and that such minor polished stones do not qualify as mirror polished stones. Currently, S. No. 123 of Schedule-I prescribes GST rate of 5% for ‘Ecaussine and other calcareous monumental or building stone; alabaster [other than marble and travertine], other than mirror polished stone which is ready to use.’

Therefore, it was clarified that S. No. 123 in Schedule-I to the Notification No. 1/2017-Central Tax (Rate) Dated: 28.06.2017 covers such minor polished stones.

3. Mangoes under CTH 0804 including mango pulp, but other than fresh mangoes and sliced, dried mangoes, attract GST at 12% rate.

Regarding the applicable GST rates on different forms of mangoes including mango Pulp it was clarified that mangoes, fresh falling under heading 0804 are exempt from GST [S. No. 51 of Notification No. 2/2017-Central Tax (Rate), dated 28.06.2017]. Whereas mangoes, sliced and dried, falling under 0804 are chargeable to a concessional rate of 5%; while all other forms of dried mango, including Mango pulp, attract GST at the rate of 12%.

To bring clarity, the relevant entry at S. No. 16 of Schedule-II of Notification No. 1/2017-Central Tax (Rate), Dated: 28.06.2017, has been amended vide Notification No. 6/2022-Central Tax (Rate), dated the 13.07.2022.

4. Treated sewage water attracts NIL rate of GST.

Clarification was sought with respect to applicable GST rate on treated sewage water as it was not meant to be construed as falling under “purified” water for the purpose of levy of GST. In general, water, falling under heading 2201, with certain specified exclusions, is exempt from GST vide entry at S. No. 99 of Notification No. 2/2017-Central Tax (Rate), dated 28.06.2017.

Vide the circular it was clarified that supply of treated sewage water, falling under heading 2201, is exempt under GST and to further clarify the issue, the word ‘purified’ was being omitted from the above-mentioned entry vide Notification No. 7/2022-Central Tax (Rate), dated 13.07.2022.

5. Nicotine Polacrilex Gum attracts a GST rate of 18%.

The WCO 2022 HS Codes has inter alia introduced a new entry 2404 91 00 comprising of products for oral application containing nicotine and intended to assist tobacco use cessation with effect from 01.01.2022. Accordingly, a technical change, without any consequential rate change, has been made vide Notification No. 18/2021 – Central Tax (Rate), dated the 28.12.2021, wherein S. No. 26B in Schedule III of Notification No. 1/2017-Central Tax (Rate), Dated: 28.06.2017, has been inserted to include products for oral application containing nicotine and intended to assist in cessation of use of tobacco, and falling under tariff item 2404 91 00.

The circular has clarified that Nicotine Polacrilex gum which is commonly applied orally and is intended to assist tobacco use cessation is appropriately classifiable under tariff item 2404 91 00 with applicable GST rate of 18%.

6. Fly ash bricks and aggregate – condition of 90% fly ash content applied only to fly ash aggregate, and not fly ash bricks.

In accordance with the entry at S. No. 176B of the Schedule II the items of description “Fly ash bricks or fly ash aggregate with 90% or more fly ash content; Fly ash blocks” attracts a GST rate of 12%.

Confusion had arisen about the applicability of 90% condition on fly ash aggregates and fly ash bricks as in accordance with the recommendations of the GST Council in the 23rd Meeting, the condition of 90% or more fly ash content was applicable only for fly ash aggregate. Vide the circular it is clarified that the condition of 90% or more fly ash content applied only to Fly Ash Aggregates and not to fly ash bricks and fly ash blocks. Further, with effect from 18.07.2022 the condition is omitted from the description.

7. Applicability of GST on by-products of milling of Dal/ Pulses such as Chilka, Khanda and Churi.

Regarding the applicable GST rate on by-products of milling of Dal/ Pulses such as Chilka, Khanda and Churi there was dispute as to whether the above-mentioned by-products are meant for direct consumption as cattle feed and thereby attract exemption under S. No. 102 of Notification No. 2/2017-Central Tax (Rate), dated 28.06.2017 or are otherwise not meant for direct consumption and are thus covered under S. No. 103A of Notification No. 1/2017-Central Tax (Rate), Dated: 28.06.2017 attracting a GST rate of 5%.

While milling of pulses/ dal, a wide range of by-products such as Chilka, Khanda, Churi, among others, are obtained which are preferred as cattle feed by dairy industry for better palatability and higher nutritive value. The mentioned by-products are required to go through varying degrees of processing in order to customize it as per needs of the customers. Further, as per the specification, issued by Government of India, grain by-products have been categorized as one of the ingredients of the compounded cattle feed.

After considering these factors the circular clarifies that the subject goods which inter alia are used as cattle feed ingredient are appropriately classifiable under heading 2302 and attract GST at the rate of 5% vide S. No. 103A of Schedule-I of Notification No. 1/2017-Central Tax (Rate), Dated: 28.06.2017 and that for the past, the matter would be regularized on as is basis.

> Circular no. 178/10/2022-GST dated regarding scope of the entry at para 5 (e) of Schedule II of CGST Act, 2017.

Vide the said circular the Central Government has issued clarifications regarding taxability of an activity or transaction as the supply of service of agreeing to the obligation to refrain from an act or to tolerate an act or a situation, or to do an act. Applicability of GST on payments in the nature of liquidated damage, compensation, penalty, cancellation charges, late payment surcharge etc. arising out of breach of contract or otherwise and scope of the entry at para 5 (e) of Schedule II of Central Goods and Services Tax Act, in this context has been examined.

“Agreeing to the obligation to refrain from an act or to tolerate an act or a situation, or to do an act” has been specifically declared to be a supply of service in para 5 (e) of Schedule II of CGST Act if the same constitutes a “supply” within the meaning of the Act.

Further, the description of the declared service in question as provided in para 5 (e) of Schedule II of CGST Act is strikingly similar to the definition of contract in the Contract Act, 1872. A contract to do something or to abstain from doing something cannot be said to have taken place unless there are two parties, one of which expressly or impliedly agrees to do or abstain from doing something and the other agrees to pay consideration to the first party for doing or abstaining from such an act.

In light of above, the aforesaid circular has clarified the following:

i. Liquidated Damages

Regarding the taxability of ‘liquidated damages’ the reasonable view is that where the amount paid as ‘liquidated damages’ is an amount paid only to compensate for injury, loss or damage suffered by the aggrieved party due to breach of the contract and there is no agreement, express or implied, by the aggrieved party receiving the liquidated damages, to refrain from or tolerate an act or to do anything for the party paying the liquidated damages, in such cases liquidated damages are mere a flow of money from the party who causes breach of the contract to the party who suffers loss or damage due to such breach. Such payments do not constitute consideration for a supply and are not taxable.

Examples of such cases are damages resulting from damage to property, negligence, piracy, unauthorized use of trade name, copyright, etc.

Other examples that may be covered here are the penalty stipulated in a contract for delayed construction of houses.

However, if a payment constitutes a consideration for a supply, then it is taxable irrespective of by what name it is called; a “consideration” cannot be considered de hors an agreement/contract between two persons wherein one person does something for another and that other pays the first in return. Therefore, such payments, even though they may be referred to as fine or penalty, are actually payments that amount to consideration for supply, and are subject to GST, in cases where such supply is taxable. Since these supplies are ancillary to the principal supply for which the contract is signed, they shall be eligible to be assessed as the principal supply. Naturally, such payments will not be taxable if the principal supply is exempt.

ii. Compensation for cancellation of coal blocks

The compensation paid for cancellation of coal blocks pursuant to the order of the Supreme Court is not taxable as there was no agreement between the prior allottees of coal blocks and the Government that the previous allottees shall agree to or tolerate cancellation of the coal blocks allocated to them if the Government pays compensation to them.

The compensation was given to them for such cancellation, not under a contract between the allottees and the Government, but under the provisions of the statute and in pursuance of the Supreme Court Order. Therefore, it would be incorrect to say that the prior allottees of the coal blocks supplied a service to the Government by way of agreeing to tolerate the cancellation of the allocations made to them by the Government or that the compensation paid by the Government for such cancellation in pursuance to the order of the Supreme Court was a consideration for such service. Therefore, the compensation paid for cancellation of coal blocks pursuant to the order of the Supreme Court in the above case was not taxable.

iii. Cheque dishonor fine/penalty

The promise made by any supplier of goods or services is to make supply against payment within an agreed time (including the agreed permissible time with late payment) through a valid instrument. There is never an implied or express offer or willingness on part of the supplier that he would tolerate deposit of an invalid, fake or unworthy instrument of payment against consideration in the form of cheque dishonour fine or penalty.

The fine or penalty that the supplier or a banker imposes, for dishonor of a cheque, is a penalty imposed not for tolerating the act or situation but a fine, or penalty imposed for not tolerating, penalizing and thereby deterring and discouraging such an act or situation. Therefore, cheque dishonor fine or penalty is not a consideration for any service and not taxable.

iv. Penalty imposed for violation of law

Penalty imposed for violation of laws such as traffic violations, or for violation of pollution norms or other laws are also not consideration for any supply received and are not taxable. Same is the case with fines, penalties imposed by the mining Department of a Central or State Government or a local authority on discovering mining of excess mineral beyond the permissible limit or of mining activities in violation of the mining permit. Such penalties imposed for violation of laws cannot be regarded as consideration charged by Government or a Local Authority for tolerating violation of laws. Laws are not framed for tolerating their violation. They stipulate penalty not for tolerating violation but for not tolerating, penalizing and deterring such violations. There is no agreement between the Government and the violator specifying that violation would be allowed or permitted against payment of fine or penalty. There cannot be such an agreement as violation of law is never a lawful object or consideration.

It was also clarified vide Circular No. 192/02/2016-Service Tax, dated 13.04.2016 that fines and penalty chargeable by Government or a local authority imposed for violation of a statute, bye-laws, rules or regulations are not leviable to Service Tax. The same holds true for GST also.

v. Forfeiture of salary or payment of bond amount in the event of the employee leaving the employment before the minimum agreed period

An employer carries out an elaborate selection process and incurs expenditure in recruiting an employee, invests in his training and makes him a part of the organization, privy to its processes and business secrets in the expectation that the recruited employee would work for the organization for a certain minimum period. Premature leaving of the employment results in disruption of work and an undesirable situation. The provisions for forfeiture of salary or recovery of bond amount in the event of the employee leaving the employment before the minimum agreed period are incorporated in the employment contract to discourage non-serious candidates from taking up employment.

The said amounts are recovered by the employer not as a consideration for tolerating the act of such premature quitting of employment but as penalties for dissuading the non-serious employees from taking up employment and to discourage and deter such a situation. Further, the employee does not get anything in return from the employer against payment of such amounts. Therefore, such amounts recovered by the employer are not taxable as consideration for the service of agreeing to tolerate an act or a situation.

vi. Compensation for not collecting toll charges

During the period from 08.11.2016 to 01.12.2016, the service of access to a road or bridge continued to be provided without collection of tolls from users, the consideration being compensated later by the project authority. A question arose whether the compensation paid to the concessionaire by project authorities (NHAI) in lieu of suspension of toll collection during the aforesaid period was taxable as a service by way of agreeing to refrain from collection of tolls from users.

It has been clarified vide Circular No. 212/2/2019-ST dated 21.05.2019 that the service that is provided by toll operators is that of access to a road or bridge, toll charges being merely a consideration for that service. During the period from 08.11.2016 to 01.12.2016, the service of access to a road or bridge continued to be provided without collection of toll from users. Consideration came from the project authority. The fact that for this period, for the same service, consideration came from a person other than the actual user of service does not mean that the service has changed.

vii. Late payment of surcharge or fee (should be assessed at the same rate as Principal supply)

The facility of accepting late payments with interest or late payment fee, fine or penalty is a facility granted by supplier naturally bundled with the main supply. It is not uncommon or unnatural for customers to sometimes miss the last date of payment of electricity, water, telecommunication services etc.

Even if this service is described as a service of tolerating the act of late payment, it is an ancillary supply naturally bundled and supplied in conjunction with the principal supply, and therefore should be assessed as the principal supply. Since it is ancillary to and naturally bundled with the principal supply such as of electricity, water, telecommunication, cooking gas, insurance etc. it should be assessed at the same rate as the principal supply.

viii. Fixed Capacity charges for power

The price charged for electricity by the power generating companies from the State Electricity Boards (SEBs)/DISCOMS or by SEBs/DISCOMs from individual customers has two components, namely, a minimum fixed charge (or capacity charge) and variable per unit charge. The minimum fixed charges have to be paid by the SEBs/DISCOMS/individual customers irrespective of the quantity of electricity scheduled or purchased by them during a month. The variable charges are charged per unit of electricity purchased and increase or decrease every month depending on the quantity of electricity consumed.

The fact that the minimum fixed charges remain the same whether electricity is consumed or not or it is scheduled/consumed below the contracted or available capacity or a minimum threshold, does not mean that minimum fixed charge or part of it is a charge for tolerating the act of not scheduling or consuming the minimum the contracted or available capacity or a minimum threshold.

It has been clarified that the minimum fixed charges/capacity charges and the variable/energy charges are both charged for sale of electricity and are thus not taxable as electricity is exempt from GST.

ix. Cancellation charges (depends upon nature of supply) A supply contracted for, such as booking of hotel accommodation, an entertainment event or a journey, may be cancelled by a customer or may not proceed as intended due to his failure to show up for availing the same at the designated place and time. The supplier may allow cancelation of supply by the customer within a certain specified time period on payment of cancellation fee as per commercial terms of the contract. In case the customer does not show up for availing the service, the supplier may retain or forfeit part of the consideration or security deposit or earnest money paid by the customer for the intended supply

Cancellation fee can be considered as the charges for the costs involved in making arrangements for the intended supply and the costs involved in cancellation of the supply, such as in cancellation of reserved tickets by the Indian Railways.

The facilitation service of allowing cancellation against payment of cancellation charges naturally constitute a bundle of services. It is invariably supplied by all suppliers of passenger transportation service as naturally bundled and in conjunction with the principal supply of transportation in the ordinary course of business. Therefore, facilitation supply of allowing cancellation of an intended supply against payment of cancellation fee or retention or forfeiture of a part or whole of the consideration or security deposit in such cases should be assessed as the principal supply.

Accordingly, the amount forfeited in the case of nonrefundable ticket for air travel or security deposit or earnest money forfeited in case of the customer failing to avail the travel, tour operator or hotel accommodation service or such other intended supplies should be assessed at the same rate as applicable to the service contract, say air transport or tour operator service, or other such services.

However, forfeiture of earnest money by a seller in case of breach of ‘an agreement to sell’ an immovable property by the buyer or such forfeiture by Government or local authority in the event of a successful bidder failing to act after winning the bid for allotment of natural resources, is a mere flow of money, as the buyer or the successful bidder does not get anything in return for such forfeiture of earnest money. Forfeiture of earnest money is stipulated in such cases not as a consideration for tolerating the breach of contract but as a compensation for the losses suffered and as a penalty for discouraging the non-serious buyers or bidders. Such payments being merely flow of money are not a consideration for any supply and are not taxable.

> Circular no. 177/09/2022-GST dated 03.08.2022 regarding applicable GST rates & exemptions on certain services.

Certain issues have been examined by GST Council in the 47th meeting held on 28th and 29th June, 2022. The following issues are clarified vide this Circular:

1. Rate of GST applicable on supply of ice-cream by ice-cream parlors during the period from 01.07.2017 to 05.10.2021.

Vide Circular 164/20/2021-GST dated 06.10.2021, it was clarified that ice cream parlors sell already manufactured ice-cream and they do not have a character of a restaurant and hence, ice cream sold by a parlor or any similar outlet attracts standard rate of GST @ 18% with ITC.

It has been represented that ice cream parlors which paid GST @ 5% without ITC in view of prevailing doubt before the issuance of the Circular dated 06.10.2021 did not avail ITC and paid 5% in cash. Such ice-cream parlors have thus foregone significant ITC benefit. In this regard, it is clarified that past cases of payment of GST on supply of ice-cream by ice-cream parlors @ 5% without ITC shall be treated as GST fully paid to avoid unnecessary litigation. Since the decision is only to regularize the past practice, no refund of GST shall be allowed, if already paid at 18%.

With effect from 06.10.2021, ice cream parlors are required to pay GST on supply of ice-cream at the rate of 18% with ITC.

2. Applicability of GST on application fee charged for entrance or the fee charged for issuance of eligibility certificate for admission or for issuance of migration certificate by educational institutions.

The amount or fee charged from prospective students for entrance or admission, or for issuance of eligibility certificate to them in the process of their entrance/admission as well as the fee charged for issuance of migration certificates by educational institutions to the leaving or ex-students is covered by exemption under S. No. 66 of Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017.

3. Whether storage or warehousing of cotton in baled or ginned form is covered under entry 24B of Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017. which exempted services by way of storage and warehousing of raw vegetable fibers such as cotton before 18.07.2022.

Prior to 18.07.2022, entry 24 B of Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017. exempted services by way of storage and warehousing of, inter alia, raw vegetable fibers such as cotton, flax, jute etc. Further, CESTAT Chandigarh in the case of R.K.& Sons vs CCE, Rohtak dated 14th July 2016 has observed as under:

“Cotton (with seeds) as plucked from cotton plants can hardly be called cotton fibre in which case cotton fibre would come into existence only after the seeds are ginned away from cotton plucked from cotton plants. Cotton fibre obtained by ginning cotton plucked cotton plants is nothing but raw cotton fibre because there cannot be rawer form of cotton fibre obtained from cotton-with-seeds plucked from cotton plants.”

It is clarified that service by way of storage or warehousing of cotton in ginned and/or baled form was covered under entry 24B of Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017 in the category of raw vegetable fibres such as cotton. It may however be noted that this exemption has been withdrawn with effect from 18.07.2022.

4. Whether exemption under S. No. 9B of Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017 covers services associated with transit cargo both to and from Nepal and Bhutan.

Exemption under S. No. 9B of Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017 covers services associated with transit cargo both to and from Nepal and Bhutan. It is also clarified that movement of empty containers from Nepal and Bhutan, after delivery of goods there, is a service associated with the transit cargo to Nepal and Bhutan and is therefore covered by the exemption.

Pertinently, the cargo has to be transshipped / transited to Nepal and Bhutan, as per Regulations under the Customs Act read with the Treaties for Trade & Transit with Nepal & Bhutan. The regulations governing transit / transshipment have to be followed in addition to the ensuring that an electronic track and trace facility is in place.

5. Applicability of GST on sanitation and conservancy services supplied to Army and other Central and State Government departments.

Services by Central Government, State Government, Union Territory or any local authority by way of any activity in relation to a function entrusted to a Panchayat under article 243G of the constitution or to a municipality under article 243W of the constitution have been declared as ‘neither a supply of goods nor a supply of service’ vide Notification No. 14/2017-Central Tax (Rate) dated 28.06.2017.

The exemption under Entry 3& 3A of Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017 has been given on pure services & composite supplies procured by Central Government, State Government, Union Territories or local authorities for performing functions listed in the 11th and 12th Schedule of the Constitution.

It is clarified that if such services are procured by Indian Army or any other Government Ministry/Department which does not perform any functions listed in the 11th and 12th Schedule of the Constitution of India, in the manner as a local authority does for the general public, the same are not eligible for exemption under S. No. 3 and 3A of Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017

6. Whether the activity of selling of space for advertisement in souvenirs is eligible for concessional rate of 5%.

Regarding the GST rate applicable on selling of space for advertisement in souvenirs published in the form of books by different institutions/organizations like educational institutions, social, cultural and religious organizations including clubs etc it clarified that ‘book’ has been defined in the Press and Registration of Books Act, 1867 in an inclusive manner with a wide ambit which would cover souvenir book also.

It is clarified, that sale of space for advertisement in souvenir book is covered under serial number (i) of entry 21 of Notification No. 11/2017-Central Tax (Rate) and attracts GST @ 5%.

7. Taxability and applicable rate of GST on transport of minerals from mining pit head to railway siding, beneficiation plant etc., by vehicles deployed with driver for a specific duration of time.

Regarding the question of taxability of transport of minerals within a mining area, say from mining pit head to railway siding, beneficiation plant etc., by vehicles deployed with driver for a specific duration of time and whether the same would be covered under S. No. 18 of Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017 which exempts transport of goods by road except by a GTA it is clarified that such renting of trucks and other freight vehicles with driver for a period of time is a service of renting of transport vehicles with operator falling under Heading 9966 and not service of transportation of goods by road. This being so, it is not eligible for exemption under S. No. 18 of Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017 . On such rental services of goods carriages where the cost of fuel is included in the consideration charged from the recipient of service, GST rate has been reduced from 18% to 12% with effect from 18.07.2022. Prior to 18.07.2022, it attracted GST at the rate of 18%.

8. Whether location charges or preferential location charges (PLC) collected in addition to the lease premium for long term lease of land constitute part of the lease premium or upfront amount charged for long term lease of land and are eligible for the same tax treatment.

As per entry 41 of the Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017 upfront amount, which is defined as “upfront amount (called as premium, salami, cost, price, development charges or by any other name) payable in respect of service by way of granting of long term lease (of thirty years, or more) of industrial plots or plots for development of infrastructure for financial business, provided by the State Government Industrial Development Corporations or Undertakings or by any other entity having 20 per cent or more ownership of Central Government, State Government, Union territory to the industrial units or the developers in any industrial or financial business area”, is exempt from GST.

The Circular clarifies that location charges or preferential location charges (PLC) paid upfront in addition to the lease premium for long term lease of land constitute part of upfront amount charged for long term lease of land and are eligible for the same tax treatment, and thus eligible for exemption under S. No. 41 of Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017 .

9. Applicability of GST on payment of honorarium to the Guest Anchors.

Regarding applicability of GST on honorarium paid to Guest Anchors by TV channels for participating in their shows it is clarified that supply of all goods & services are taxable unless exempt or declared as ‘neither a supply of goods nor a supply of service’.

Services provided by guest anchors in lieu of honorarium attract GST liability. However, guest anchors whose aggregate turnover in a financial year does not exceed ₹ 20 lakhs (₹ 10 lakhs in case of special category states) shall not be liable to take registration and pay GST.

10. Whether the additional toll fees collected in the form of higher toll charges from vehicles not having Fastag is exempt from GST.

Regarding taxability of additional toll fees collected by the Concessionaires from the vehicles which is not having Fastag, it is clarified that additional fee collected in the form of higher toll charges from vehicles not having Fastag is essentially payment of toll for allowing access to roads or bridges to such vehicles and may be given the same treatment as given to toll charges

11. Applicability of GST on services in the form of Assisted Reproductive Technology (ART)/In vitro fertilization (IVF).

Health care services provided by a clinical establishment, an authorized medical practitioner or para-medics are exempt. [S. No. 74 of Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017 ].

Regarding applicability of GST on services by way of Assisted Reproductive Technology (ART) procedures such as In vitro fertilization (IVF) it is clarified that services by way of IVF are also covered under the definition of health care services for the purpose of exemption.

12. Whether sale of land after levelling, laying down of drainage lines etc., is taxable under GST.

As per S. No. 5 of Schedule III of the Central Goods and Services Tax Act, 2017, ‘sale of land’ is neither a supply of goods nor a supply of services, therefore, sale of land does not attract GST.

Regarding applicability of GST on sale of land after levelling, laying down of drainage lines etc. it is clarified that sale of such developed land is also sale of land and is covered by S. No. 5 of Schedule III of the Central Goods and Services Tax Act, 2017 and accordingly does not attract GST. However, it may be noted that any service provided for development of land, like levelling, laying of drainage lines (as may be received by developers) shall attract GST at applicable rate for such services.

13. Situations in which corporate recipients are liable to pay GST on renting of motor vehicles designed to carry passengers.

In case of services provided by a non-body corporate to a body corporate by way of renting of any motor vehicle for transport of passengers, tax is required to be paid by the body corporate under RCM.

As to whether RCM is applicable on service of transportation of passengers (Heading 9964) or on renting of motor vehicle designed to carry passengers (Heading 9966), it is clarified that where the body corporate hires the motor vehicle (for transport of employees etc.) for a period of time, during which the motor vehicle shall be at the disposal of the body corporate, the service would fall under Heading 9966, and the body corporate shall be liable to pay GST on the same under RCM. It may be seen that reverse charge thus would apply on act of renting of vehicles by body corporate and in such a case, it is for the body corporate to use in the manner as it likes subject to agreement with the person providing vehicle on rent.

However, where the body corporate avails the passenger transport service for specific journeys or voyages and does not take vehicle on rent for any particular period of time, the service would fall under Heading 9964 and the body corporate shall not be liable to pay GST on the same under RCM.

14. Whether hiring of vehicles by firms for transportation of their employees to and from work is exempt under S. No. 15(b) of Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017 transport of passengers by non-air-conditioned contract carriage.

s. No. 15 (b) of Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017 exempts “transport of passengers, with or without accompanied belongings, by non-air conditioned contract carriage, other than radio taxi, for transport of passengers, excluding tourism, conducted tour, charter or hire.”

Regarding whether the engagement of non-air-conditioned contract carriages by firms for transportation of their employees to and from work is exempt under entry at S. No. 15(b) of Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017 it is clarified that ‘charter or hire’ excluded from the above exemption entry is charter or hire of a motor vehicle for a period of time, where the renter defines how and when the vehicles will be operated, determining schedules, routes and other operational considerations.

In other words, the said exemption would apply to passenger transportation services by non-air-conditioned contract carriages falling under Heading 9964 where according to explanatory notes, transportation takes place over pre-determined route on a pre-determined schedule. The exemption shall not be applicable where contract carriage is hired for a period of time, during which the contract carriage is at the disposal of the service recipient and the recipient is thus free to decide the manner of usage (route and schedule) subject to conditions of agreement entered into with the service provider.

15. Whether supply of service of construction, supply, installation and commissioning of dairy plant on turn-key basis constitutes a composite supply of works contract service and is eligible for concessional rate of GST prior to 18.07.2022.

In case of a turn key project for construction, supply, installation and commissioning of a 2.00 LLPD dairy plant, it has been held by Advance Ruling Authorities of Bihar and Gujarat that the same does not result into an immovable property and is therefore not a supply of works contract. This being so, such supply is not eligible for concessional rate of 12% applicable on works contract supplied by way of construction, erection, commissioning, or installation of original works pertaining to mechanized food grain handling system, machinery or equipment for units processing agricultural produce as food stuff excluding alcoholic beverages.

Prior to 18.07.2022, S. No. 3(v)(f) of Notification No. 11/2017-Central Tax (Rate) prescribed GST rate of 12 % on the composite supply of works contract by way of construction, erection, commissioning, or installation of original works pertaining to mechanized food grain handling system, machinery or equipment for units processing agricultural produce as food stuff excluding alcoholic beverages.

Regarding the applicable GST rate on service of construction, supply, installation and commissioning of a 2.00 LLPD dairy plant on turn-key basis it is clarified that a contract of the nature described here for construction, installation and commissioning of a dairy plant constitutes supply of works contract. There is no doubt that dairy plant which comes into existence as a result of such contracts is an immovable property.

It is also clarified that such works contract services were eligible for concessional rate of 12% GST under serial number 3(v)(f) of Notification No. 11/2017-Central Tax (Rate) prior to 18.07.2022. With effect from 18.07.2022, such works contract services would attract GST at the rate of 18% in view of amendment carried out in Notification No. 11/2017-Central Tax (Rate) vide Notification No. 03/2022- Central Tax (Rate).

16. Applicability of GST on tickets of private ferry used for passenger transportation.

As per S. No 17 (d) of Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017 “transportation of passengers by public transport, other than predominantly for tourism purpose, in a vessel between places located in India” is exempted.

Regarding applicability of GST on private ferry tickets it is clarified that this exemption would apply to tickets purchased for transportation from one point to another irrespective of whether the ferry is owned or operated by a private sector enterprise or by a PSU/government. It is further clarified that the expression ‘public transport’ used in the exemption notification only means that the transport should be open to public. It can be privately or publicly owned. Only exclusion is on transportation which is predominantly for tourism, such as services which may combine with transportation, sightseeing, food and beverages, music, accommodation such as in shikara, cruise etc.

Instructions

> Instruction No. 02/2022-23-[GST-INV] dated 17.08.2022 providing guidelines for arrest and bail under CGST Act, 2017

The abovementioned Instruction is issued by the Central Government in furtherance of the Judgment passed by the Hon’ble Supreme Court of India dated 16th August, 2021 in Criminal Appeal No. 838 of 2021, arising out of SLP (Cr1.) No. 5442/2021 in the matter of Siddharth v. The State of Uttar Pradesh and Anr., wherein, the Hon’ble Court has observed that if arrests are made routine, they can cause incalculable harm to the reputation and self-esteem of a person. If the investigating officer has no reason to believe that the accused will abscond or disobey summons and has, in fact, cooperated with the investigation, then why should there be a compulsion on the officer to arrest the accused.

The Central Government has examined the above-mentioned judgment and has issued the following guidelines with respect to arrest under CGST Act, 2017 vide the aforementioned instruction;

1. Conditions precedent to arrest:

The legal requirements as provided under Section 132 and Section 69 of the CGST Act, 2017 must be fulfilled before placing a person under arrest. The reasons to arrive at a decision to place an alleged offender under arrest must be unambiguous, amply clear and must be based on credible material. The arrest should not be made in routine and mechanical manner even if all the legal conditions precedent to arrest mentioned in Section 132 of the CGST Act, 2017 are fulfilled.

Pursuant to identification of the legal ingredients of the offence, the Commissioner or the competent authority must determine if the answer to any or some of the following questions is in the affirmative:

- Whether the person was concerned in the non-bailable offence or credible information has been received, or a reasonable suspicion exists, of his having been so concerned?

- Whether arrest is necessary to ensure proper investigation of the offence?

- Whether the person, if not restricted, is likely to tamper the course of further investigation or is likely to tamper with evidence or intimidate or influence witnesses?

- Whether person is mastermind or key operator effecting proxy/ benami transaction in the name of dummy GSTIN or non-existent persons, etc. for passing fraudulent input tax credit etc.?

Thereafter, in instances where arrest is necessary in order to ensure presence of such person before investigating officer then approval to arrest should be granted only where the intent to evade tax or commit acts leading to availment or utilization of wrongful Input Tax Credit or fraudulent refund of tax or failure to pay amount collected as tax as is evident and element of mens rea / guilty mind is palpable.

However, arrest should not be resorted to in cases of technical nature i.e., where the demand of tax is based on a difference of opinion regarding interpretation of law. The prevalent practice of assessment could also be one of the determining factors while ascribing intention to evade tax to the alleged offender. Other factors influencing the decision to arrest could be if the alleged offender is co-operating in the investigation, viz. compliance to summons, furnishing of documents called for, not giving evasive replies, voluntary payment of tax etc.

2. Procedure for arrest:

The Pr. Commissioner/Commissioner shall record on file that after considering the nature of offence, the role of person involved and evidence available in instances where he has reason to believe that the person has committed an offence as mentioned in Section 132 and may authorize an officer of central tax to arrest the concerned person(s). The provisions of the Code of Criminal Procedure, 1973 (2 of 1974) read with Section 69(3) of CGST Act relating to arrest and the procedure thereof, must be adhered to during the process.

The arrest memo must be in compliance with the directions of Hon’ble Supreme Court and it should indicate the relevant Section (s) of the CGST Act, 2017 or other laws attracted to the case and to the arrested person and inapplicable provisions should be struck off.

The grounds of arrest must be explained to the arrested person and must be noted in the arrest memo. A nominated or authorized person (as per the details provided by arrested person) of the arrested person should be informed immediately and this fact shall be mentioned in the arrest memo with the date and time of arrest and the arrest memo should be given to the person arrested under proper acknowledgment. When there are several arrests in a single case a separate arrest memo has to be made and provided to each individual/arrested person.

Document Identification Number (DIN) must be mandatory on communication issued by officers to tax payers and other concerned persons for the purpose of investigation in accordance with Board’s Circular No. 122/41/2019-GST dated 5th November, 2019

Further, the following modalities should also be complied with at the time of arrest and pursuant to an arrest:

- A woman should be arrested only by a woman officer in accordance with Section 46 of Code of Criminal Procedure, 1973.

- Medical examination of an arrested person should be conducted by a medical officer in the service of Central or State Government and in case the medical officer is not available, by a registered medical practitioner, soon after the arrest is made. If an arrested person is a female, then such an examination shall be made only by or under supervision of a female medical officer, and in case the female medical officer is not available, by a female registered medical practitioner.

- It shall be the duty of the person having the custody of an arrested person to take reasonable care of the health and safety of the arrested person.

- Arrest should be made with minimal use of force and publicity, and without violence. The person arrested should be subjected to reasonable restraint to prevent escape.

3. Post arrest formalities:

In cases, where a person is arrested under Sub-section (1) of Section 69 of the CGST Act, 2017, for an offence specified under Sub-section (4) of Section 132 of the CGST Act, 2017, the Assistant Commissioner or Deputy Commissioner is bound to release a person on bail against a bail bond. The bail conditions should be informed in writing to the arrested person and also on telephone to the nominated person of the person (s) arrested. The arrested person should also be allowed to talk to the nominated person. If the conditions of the bail are fulfilled by the arrested person, it is instructed that he shall be released by the officer concerned on bail forthwith.

However, only in cases where the conditions for granting bail are not fulfilled, the arrested person shall be produced before the appropriate Magistrate without unnecessary delay and within twenty-four hours of arrest. If necessary, the arrested person may be handed over to the nearest police station for his safe custody, during the night under a challan, before he is produced before the Court.

In cases, where a person is arrested under Sub-section (1) of Section 69 of the CGST Act, 2017, for an offence specified under Sub-section (5) of Section 132 of the CGST Act, 2017, the officer authorized to arrest the person shall inform such person of the grounds of arrest and produce him before a Magistrate within twenty-four hours. However, in the event of circumstances preventing the production of the arrested person before a Magistrate, if necessary, the arrested person may be handed over to nearest Police Station for his safe custody under a proper challan and produced before the Magistrate on the next day, and the nominated person of the arrested person may also be informed accordingly. In any case, it must be ensured that the arrested person should be produced before the appropriate Magistrate within twenty-four hours of arrest, exclusive of the time necessary for the journey from the place of arrest to the Magistrate’s Court.

After arrest of the accused, efforts should be made to file prosecution complaint under Section 132 of the Act, before the competent court at the earliest, preferably within sixty days of arrest, where no bail is granted. In all other cases of arrest also, prosecution complaint should be filed within a definite time frame.

Every Commissionerate/Directorate should maintain a Bail Register containing the details of the case, arrested person, bail amount, surety amount etc. The money/ instruments/documents received as surety should be kept in safe custody of a single nominated officer who shall ensure that these instruments/ documents received as surety are kept valid till the bail is discharged.

4. Reports to be sent Member (Compliance) & Zonal Member on every arrest:

Pr. Director-General (DGGI)/ Pr. Chief Commissioner(s)/ Chief Commissioner(s) shall send a report on every arrest to Member (Compliance Management) as well as to the Zonal Member within 24 hours of the arrest giving relevant details as prescribed. Further, from September, 2022 onwards, a monthly report of all persons arrested in the Zone shall be sent by the Principal Chief Commissioner(s)/ Chief Commissioner(s) to the Directorate General of GST Intelligence, Headquarters, New Delhi, by the 5th of the succeeding month.

> Instruction No. 03/2022-23[GST-INV] dated 17.08.2022 regarding issuance of summons under Section 70 of the CGST Act, 2017.

It provides that while issuing of summons is one of the instruments with the Department to get/obtain information or documents or statement from any person to find out the evasion of the tax etc., however, it needs to be ensured that exercise of such power is done judiciously and with due consideration. It advises the officers to explore instances when instead of resorting to summons, a letter for requisition of information may suffice.

Taking this into consideration the Central Government vide aforesaid instruction has issued following guidelines in matters related to investigation under CGST:

I Power to issue summons is generally exercised by Superintendents, though higher officers may also issue summons. Summons by Superintendents should be issued after obtaining prior written permission from an officer not below the rank of Deputy/ Assistant Commissioner with the reasons for issuance of summons to be recorded in writing.

ii Where for operational reasons it is not possible to obtain such prior written permission, oral/telephonic permission from such officer must be obtained and the same should be reduced to writing and intimated to the officer according such permission at the earliest opportunity.

iii In all cases, where summons are issued, the officer issuing summons should record in file about appearance/ nonappearance of the summoned person and place a copy of statement recorded in file.

iv Summons should normally indicate the name of the offender(s) against whom the case is being investigated unless revelation of the name of the offender is detrimental to the cause of investigation, so that the recipient of summons has prima-facie understanding as whether he has been summoned as an accused, co accused or as witness.

v Issuance of summons may be avoided to call upon statutory documents which are digitally/ online available in the GST portal.

vi Senior management officials such as CMD / MD/ CEO/ CFO/ similar officers of any company or a PSU should not generally be issued summons in the first instance. They should be summoned when there are clear indications in the investigation of their involvement in the decision-making process which led to loss of revenue.

vii Attention is also invited to Board’s Circular No. 122/41/2019-GST dated 5th November, 2019 which makes generation and quoting of Document Identification Number (DIN) mandatory on communication issued by officers of CBIC to tax payers and other concerned persons for the purpose of investigation. Format of summons has been prescribed under Board’s Circular No. 128/47/2019-GST dated 23rd December, 2019.

viii The summoning officer must be present at the time and date for which summons is issued. In case of any exigency, the summoned person must be informed in advance in writing or orally.

ix All persons summoned are bound to appear before the officers concerned, the only exception being women who do not by tradition appear in public or privileged persons. The exemption so available to these persons under Section 132 and 133 of CPC, may be kept in consideration while investigating the case.

x Issuance of repeated summons without ensuring service of the summons must be avoided. Sometimes it may so happen that summoned person does not join investigations even after being repeatedly summoned. In such cases, after giving reasonable opportunity, generally three summons at reasonable intervals, a complaint should be filed with the jurisdictional magistrate alleging that the accused has committed offence under Sections 172 of Indian Penal Code and/or 174 of Indian Penal Code. Before filing such complaints, it must be ensured that summons have adequately been served upon the intended person in accordance with Section 169 of the CGST Act. However, this does not bar to issue further summons to the said person under Section 70 of the Act.

State Best Practices

Government of Kerala launches the Lucky Bill Mobile Application.

The Government of Kerala has launched the Lucky Bill Mobile Application for online submission of bills. The bills for supply of Goods and Services shall be submitted to the State Goods and Service Tax Department through the Lucky Bill Mobile Application. The Government has declared attractive prizes for invoices uploaded on this app through lucky draws. The app is expected to encourage general public to ask for bills during purchases, and also makes dealers and taxpayer’s vigilant in issuing bills for their sales.

Government of Kerala Press release vide File No. CT/15318/2019-P2 dated 14.08.2022

GST Portal Updates

Single click NIL filing of GSTR-1 has been introduced on the GSTN portal to improve the user experience and performance of GSTR-1/IFF filing. Taxpayers can now file NIL GSTR-1 return by simply ticking the checkbox File NIL GSTR-1 available at GSTR-1 dashboard. For the detailed advisory please click here.

> Module wise new functionalities deployed on the GST Portal for taxpayers

Various new functionalities are implemented on the GST Portal, from time to time, for GST stakeholders. These functionalities pertain to different modules such as Registration, Returns, Advance Ruling, Payment, Refund and other miscellaneous topics. Various webinars are also conducted as well as informational videos prepared on these functionalities and posted on GSTNs dedicated YouTube channel for the benefit of the stakeholders.

To view module wise functionalities deployed on the GST Portal and webinars conducted/ Videos posted on our YouTube channel, refer to table below:

S. No. |

Taxpayer functionalities deployed on the GST Portal during |

Click link below |

1. |

July, 2022 |

https://taxguru.in/goods-and-service-tax/functionalities-taxpayers-gst-portal-july-2022.html |

2. |

May, 2022 |

https://taxguru.in/goods-and-service-tax/functionalities-taxpayers-gst-portal-may-2022.html |

3. |

January-March, 2022 |

https://tutorial.gst.gov.in/downloads/news/new_functionalities_compilation_jan_mar_2022.pdf |

4. |

December, 2021 |

https://taxguru.in/goods-and-service-tax/functionalities-taxpayers-gst-portal-december-2021.html |

5. |

November, 2021 |

https://taxguru.in/goods-and-service-tax/functionalities-taxpayers-gst-portal-new-functionalities-for-taxpayers-on-gst-portal-november-2021.html |

6. |

July-September, 2021 |

https://taxguru.in/goods-and-service-tax/functionalities-taxpayers-gst-portal-july-september-2021.html |

7. |

April-June, 2021 |

https://tutorial.gst.gov.in/downloads/news/newfunctionalities_compilationaprjun2021.pdf |

8. |

January-March, 2021 |

https://tutorial.gst.gov.in/downloads/news/newfunctionalitiescompilation_janmar2021.pdf |

9. |

October-December, 2020 |

https://taxguru.in/goods-and-service-tax/functionalities-gst-portal-october-december-2020.html |

10. |

Compilation of short videos on Taxpayer functionalities |

https://tutorial.gst.gov.in/downloads/news/compilation_of_short_videos_uploaded_on_gstn_ you_tube_channel_from_2020_to_2022.pdf |

Legal Corner

> Doctrine of Per Incuriam

The maxim ‘per incuriam’ is derived from the Latin expression which means ‘through inadvertence’. It was developed in in relaxation of the rule of stare decisis. In India, this principle of law has been accepted and adopted by courts while interpreting Article 141 of the Constitution which embodies the doctrine of precedents as a matter of law.

A decision can be said to be given ‘per incuriam’ when the court of record has acted in ignorance of any previous decision of its own, or a subordinate court has acted in ignorance of a decision of the court of record. As per the principle of ‘per incuriam’ a judgement passed in ignorance or omission of a certain precedent or law is not a proper and valid judgement and has no value as a precedent

> Doctrine of Lex non cogit ad impossibilia

The maxim ‘Lex Non Cogit ad impossibilia’ is derived from the Latin expression which means that the law does not compel a man to do which he cannot possibly perform. This is a principle in equity recognized and applied by the courts in cases where a party to a contract is unable to perform its contractual obligation due to a supervening impossibility which the party could not prevent/anticipate. This maxim intends to cover such situations where a promise to perform is rendered impossible on account of change in circumstances where the change in circumstances is of such a nature that it could not have been reasonably anticipated by the party.

The fundamental tests which have been applied by courts before applying this maxim to the facts of a case, is to see whether the event (i.e. noncompliance with a law) was beyond the control of the person, occurred without any fault of the person and it resulted in an impossibility. Thus, while applying this maxim it should be borne in mind that not every inability is an impossibility.

This principle is embodied in Section 56 of the Indian Contract Act, 1872 which provides that Agreements to do an act impossible in itself is void.

Meetings with Stakeholders

> Meeting with representatives of ASSOCHAM

A meeting was held on 05.08.2022 with representatives of ASSOCHAM at the office of GST Council Secretariat. The Association brought forth various issues that were being faced by the trade on GST front. During the meeting various issues were deliberated in detail such as issues related to cross charge, refund of inverted duty for input services, permitting conversion of unutilized ITC into transferable scrips etc. Few suggestions were also made by the Association to improve tax compliance and ease of doing business. The representatives suggested that requirement of e-way bill may be discontinued on account of introduction of e-invoice and that the requirements of e-way bill may be merged with e-invoice. To improve ease of doing business they suggested that GSTN should consider rating the tax-payers based on their compliance behavior. A request was also made regarding issuance of a detailed SOP on issues such as Summons, multiplicity of notices, arrests, blocking of credit, attachment, multiplicity of notices, etc.

In this regard CBIC vide Instruction No. 02/2022-23-[GST-INV] and Instruction No. 03/2022-23[GST-INV] both dated 17.08.2022, has issued detailed guidelines with respect to arrest and bail under CGST Act, 2017 and with respect to issuance of summons under Section 70 of the CGST Act, 2017 respectively.

> Meeting with representatives of the International Spirits & Wines Association of India (ISWAI).

The representatives of ISWAI requested for clarification on taxability of Extra Neutral Alcohol (ENA) under GST/VAT law. They stressed upon the difficulties faced by industry on account of varied practices being followed by different States.

The representatives drew attention to the decision of 20th GSTC meeting held on 5th August, 2017 wherein it was decided that until an opinion is obtained from Learned Attorney General of India, the status quo shall continue w..r.t. ENA.

This decision of Council was reiterated by GST Council in 37th meeting where it was decided that states will follow the decision taken by council in 20th meeting. Further, the representatives stated that this issue was deferred by the GST Council in its 43rd meeting and it was decided that status-quo as recommended in 20th GST Council Meeting shall be maintained.

They stressed upon the various cases pending in courts across India on account of varied practices. Further, they also highlighted that a Special Leave Petition has been preferred by the State of UP on this issue before the Hon’ble Supreme Court.

Source of Newsletter – https://gstcouncil.gov.in/